Chapter 17—Financial Reporting Issues Key

1. The GASB Statement No. 34 reporting model includes, but is not limited to which of the following reports?

2. Required supplementary information includes all of the following except for:

3. Which of the following statements relating to the requirements for financial reporting is not true?

4. Which of the following could be considered a component unit of a primary government unit?

5. When operations of component units of government are blended with the primary government unit, they are

reported by

6. Which of the following were innovations in financial reporting introduced by GASB Statement No. 34?

7. The purpose of the Management Discussion and Analysis section is

8. Which of the following is/are reporting requirements in funds-based statements under GASB Statement

No.34?

9. Major funds are described as

10. GASB Statement No. 34 requires the reporting for internal service funds by

11. Which of the following is not a classification of the net asset accounts of a proprietary fund?

12. Under the requirements for a Statement of Cash Flow, what sections must be included in the statement?

1)

Operating cash flows

2)

Cash Flows from noncapital financing

3)

Capital and related financing cash flows

4)

Investing cash flows

13. GASB Statement No. 34 requirements for the reporting for general fixed assets include

14. Reciprocal interfund activities include all but which of the following?

15. Key characteristics of the statement of net assets include all of the following except:

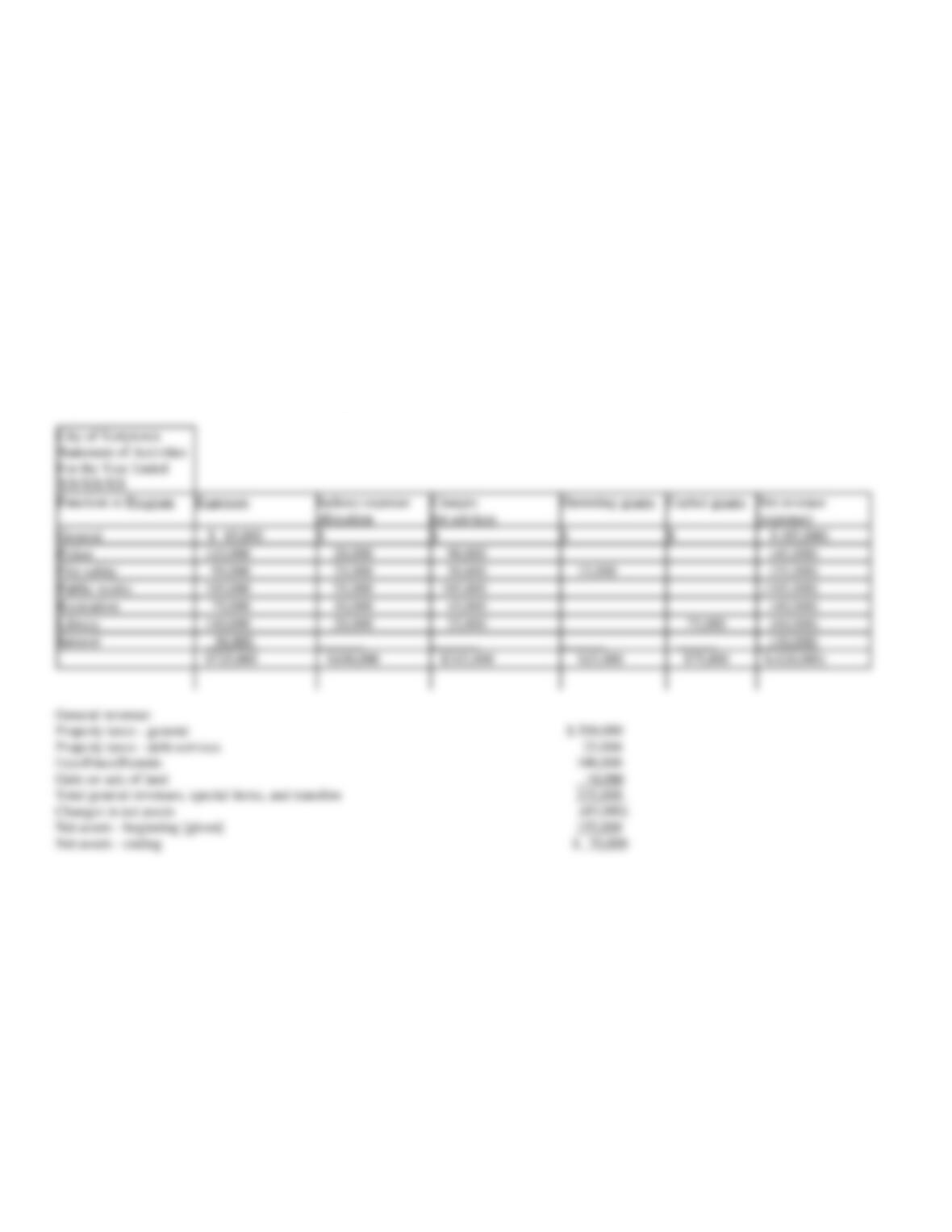

16. Which of the following combination of items reported is included on the statement of activities?

Revenue

Direct Allocated specifically Program

expenses by indirect connected to general

program expenses programs fixed assets

17. GASB Statement No.34 requires the reporting for infrastructure assets. Special provisions for reporting

include

18. The most common difference between funds-based and government-wide financial statements is

19. Converting the governmental fund balance sheet to a government-wide statement of net assets requires

which of the following activities?

1)

Add general fixed assets, net of accumulated depreciation

2)

Add general long-term debt, using the effective interest method

3)

Eliminate the assets and liabilities of most internal service funds (those whose primary customer is the general government)

4)

Eliminate the fund balance and classify the net assets into invested in capital assets, restricted net assets, and unrestricted net assets

20. In order to convert the governmental fund statement of revenues, expenditures, and changes in fund

balances to a government wide statement of activities, which of the following activities is necessary?

1)

Eliminate capital outlay expenditures

2)

Reclassify revenues between program revenues and general revenues

3)

Record bad debt expenses

4)

Convert revenues from the economic flow of resources accrual basis to the current financial resources modified accrual basis

21. Which of the following is not a purpose of the financial audit that accompanies statements?

22. The Single Audit Act requires that a governmental unit have a single audit if they

23. Audit reports prepared under the Single Audit Act include which of the following?

24. Which of the following is not a category included in the statistical section of government’s audit report?

25. From the following information, prepare a statement of net assets for the city of Franklin as of June 30,

20X3:

Cash and Cash equivalents, Governmental

$ 500,000

Cash and Cash equivalents, Business Activities

300,000

Receivables, net, Governmental

280,000

Inventories, Business Activities

135,000

Capital Assets, net, Governmental

1,330,000

Capital Assets, net, Business Activities

750,000

Accounts Payable, Governmental

158,000

Accounts Payable, Business Activities

96,000

Noncurrent liabilities, Governmental

1,005,000

Noncurrent liabilities, Business Activities

585,000

Net Assets invested in Capital Assets (net of Debt)

Governmental

733,000

Business activities

465,000

Net Assets Restricted:

Governmental

132,000

Business Activities

93,000

Net Assets Unrestricted:

Governmental

82,000

Business Activities

(54,000)

City of Franklin

Statement of Net Assets

June 30, 20X3

26. The City of Terrytown reports the following information:

Government Activities:

General-Direct Expenses

$ 85,000

Police-Direct Expenses

115,000

Fire Safety-Direct Expenses

95,000

Public Works-Direct Expenses

185,000

Recreation-Direct Expenses

75,000

Library-Direct Expenses

140,000

Interest on Long term Debt-Direct

30,000

Police-Indirect Allocation

20,000

Fire Safety-Indirect Allocation

25,000

Public Works-Indirect Allocation

25,000

Governmental

Business Type

Total

Activities

Activities

Primary Government

Cash and cash equivalents

$ 500,000

$ 300,000

$ 800,000

Receivables, net

280,000

280,000

Inventories

135,000

135,000

Capital Assets, net

1,330,000

750,000

2,080,000

Total Assets

2,110,000

1,185,000

3,295,000

Accounts payable

158,000

96,000

254,000

Noncurrent liabilities

1,005,000

585,000

1,590,000

Total Liabilities

1,163,000

681,000

1,844,000

Invested in Capital Assets, net of debt

733,000

465,000

1,198,000

Restricted

132,000

93,000

225,000

Unrestricted

82,000

(54,000)

28,000

Total Net Assets

$ 947,000

$ 504,000

$1,451,000

Recreation-Indirect Allocation

10,000

Library-Indirect Allocation

20,000

Charges for Police service

90,000

Charges for Fire Safety

50,000

Charges for Public Works

105,000

Charges for Recreation

45,000

Charges for Library

25,000

Operating Grants for Fire Safety

15,000

Capital Grants for Library

75,000

There are no business type activities for this city or other component units. Taxes raised for general revenues equal $200,000 and taxes raised for

debt service equal $25,000. Other general revenues were generated through fines, fees, and permits that total $100,000. The city also sold a plot of

land for a gain of $10,000. The beginning of the year net assets totaled $155,000.

Required:

Prepare a statement of activities schedule for the city.

27. GASB Statement No. 34 requires a separate set of financial statements for each of the three categories of

funds. Prepare an analysis of the basic types of fund categories, what the measurement focus is and the basis of

accounting, and which basic financial statements are needed.

28. Briefly discuss the minimum requirements of the Management Discussion and Analysis section in the

comprehensive annual financial report.

29. Governmental entities are required to present fund financial statements for the governmental funds based on

the modified accrual basis of accounting and government-wide financial statements where all funds, included

the governmental funds, are presented using the accrual basis of accounting. Explain the required

reconciliations and describe the major reconciling items.