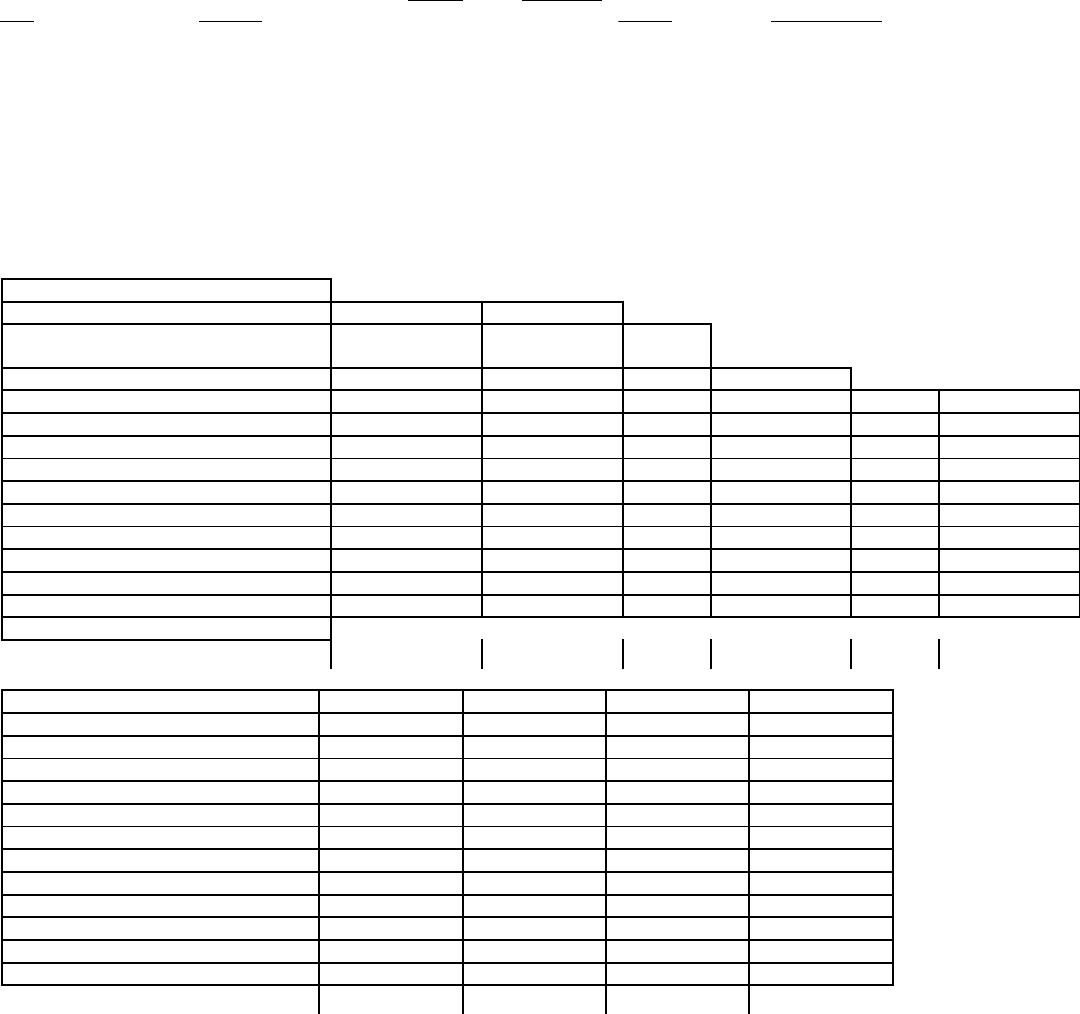

47. On January 1, 20X1 Parent Company acquired 90% of the common stock of Subsidiary Company for

$360,000. On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $50,000,

$100,000, and $200,000 respectively. Any excess of cost over book value is due to goodwill. Parent accounts

for the Investment in Subsidiary using the simple equity method.

On January 1, 20X2, Parent purchased equipment for $204,110 and immediately leased the equipment to

Subsidiary on a 4-year lease. The minimum lease payments of $60,000 are to be made annually on January 1,

beginning immediately, for a total of 4 payments. The implicit interest rate is 12%. The lease provides for an

automatic transfer of title at the end of 4 years. The estimated useful life of the equipment is 6 years. The lease

has been capitalized by both companies. The lease amortization schedule is presented below:

Date

Payment

Interest on

previous balance

Gross Receivable

Unearned

Interest

Carrying Value

1/1/X2

240,000

(35,890)

204,110

1/1/X2

60,000

180,000

(35,890)

144,110

1/1/X3

60,000

17,293

120,000

(18,597)

101,403

1/1/X4

60,000

12,168

60,000

(6,429)

53,571

1/1/X5

60,000

6,429

0

0

0

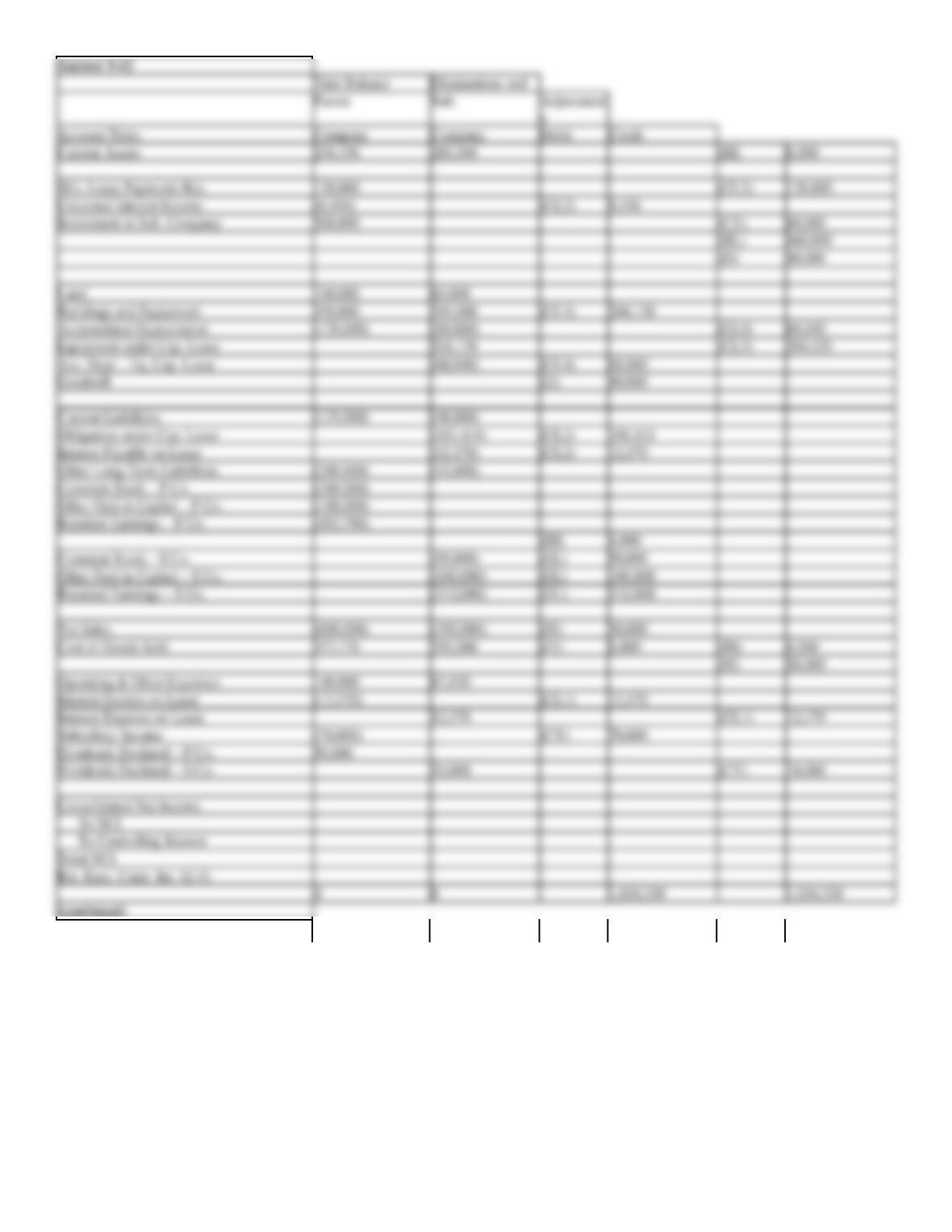

Required:

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-10 partial worksheet as of December 31, 20X2. Key and

explain all eliminations and adjustments.

Figure 5-10

Trial Balance

Eliminations and

Parent

Sub.

Adjustment

s

Account Titles

Company

Company

Debit

Credit

Min. Lease Payments Rec.

180,000

Unearned Interest Income

(18,597)

Buildings and Equipment

350,000

300,000

Accumulated Depreciation

(100,000)

(50,000)

Equipment under Cap. Lease

204,110

Acc. Depr. – Eq. Cap. Lease

(34,018)

Obligation under Cap. Lease

(144,110)

Interest Payable on Lease

(17,293)

Interest Income on Lease

(17,293)

Interest Expense on Lease

17,293

(continued)

Consol.

Control.

Consol.

Income

Retained

Balance

Account Titles

Statement

NCI

Earnings

Sheet

Min. Lease Payments Rec.

Unearned Interest Income

Buildings and Equipment

Acc. Depr. – Bldg & Equip

Equipment under Cap. Lease

Acc. Depr. – Eq. Cap. Lease

Obligation under Cap. Lease

Interest Payable on Lease

Interest Income on Lease

Interest Expense on Lease

For the partial worksheet solution, please refer to Answer 5-10.

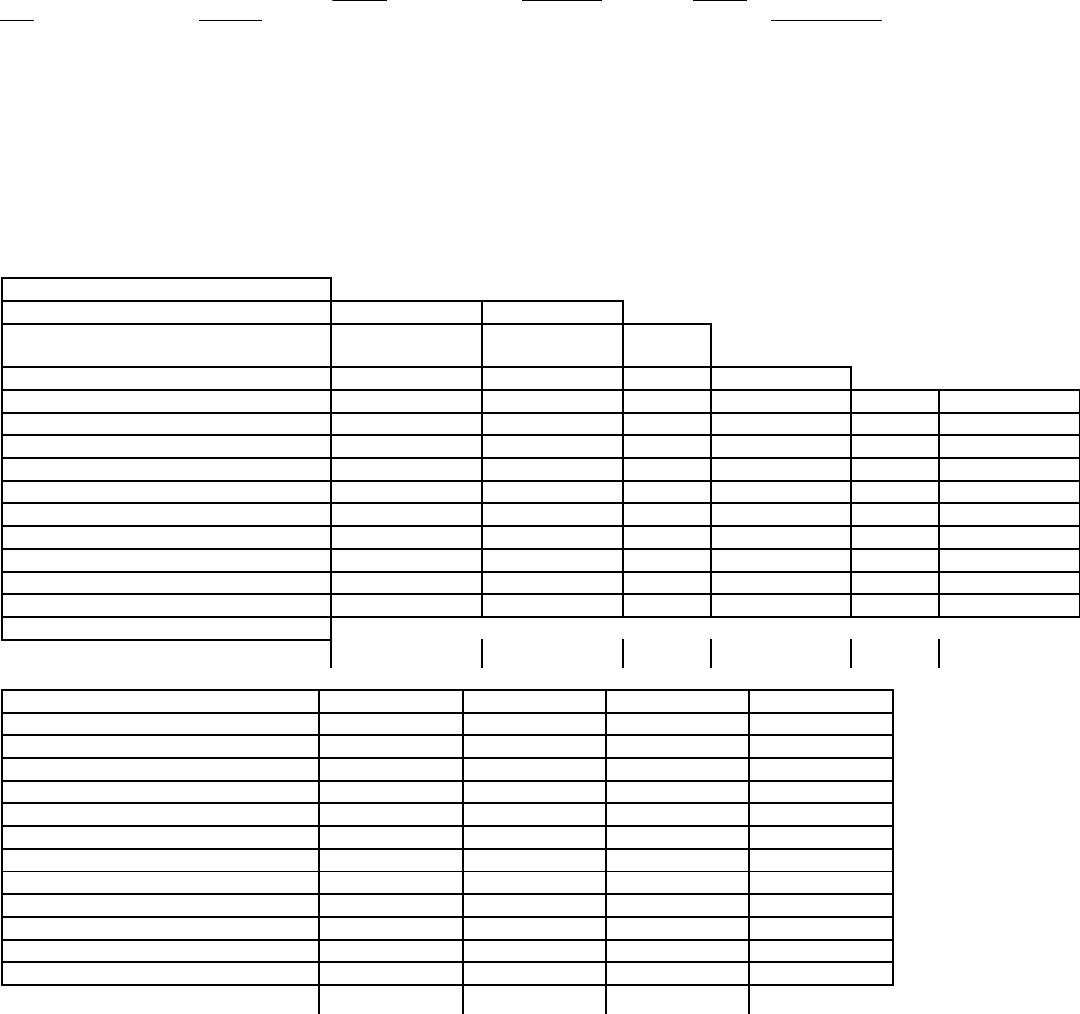

48. On January 1, 20X1, Parent Company acquired 90% of the common stock of Subsidiary Company for

$360,000. On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $50,000,

$100,000, and $200,000 respectively. Any excess of cost over book value is due to goodwill. Parent uses the

simple equity method to account for its investment in subsidiary.

On January 1, 20X2, Parent purchased equipment for $204,110 and immediately leased the equipment to

Subsidiary on a 4-year lease. The minimum lease payments of $60,000 are to be made annually on January 1,

beginning immediately, for a total of 4 payments. The implicit interest rate is 12%. The lease provides for an

automatic transfer of title at the end of 4 years. The estimated useful life of the equipment is 6 years. The lease

has been capitalized by both companies. A lease amortization schedule, applicable to either company, is

presented below:

Date

Payment

Interest on previous

balance

Gross Receivable

Unearned Interest

Carrying Value

1/1/X2

240,000

(35,890)

204,110

1/1/X2

60,000

180,000

(35,890)

144,110

1/1/X3

60,000

17,293

120,000

(18,597)

101,403

1/1/X4

60,000

12,168

60,000

(6,429)

53,571

1/1/X5

60,000

6,429

0

0

0

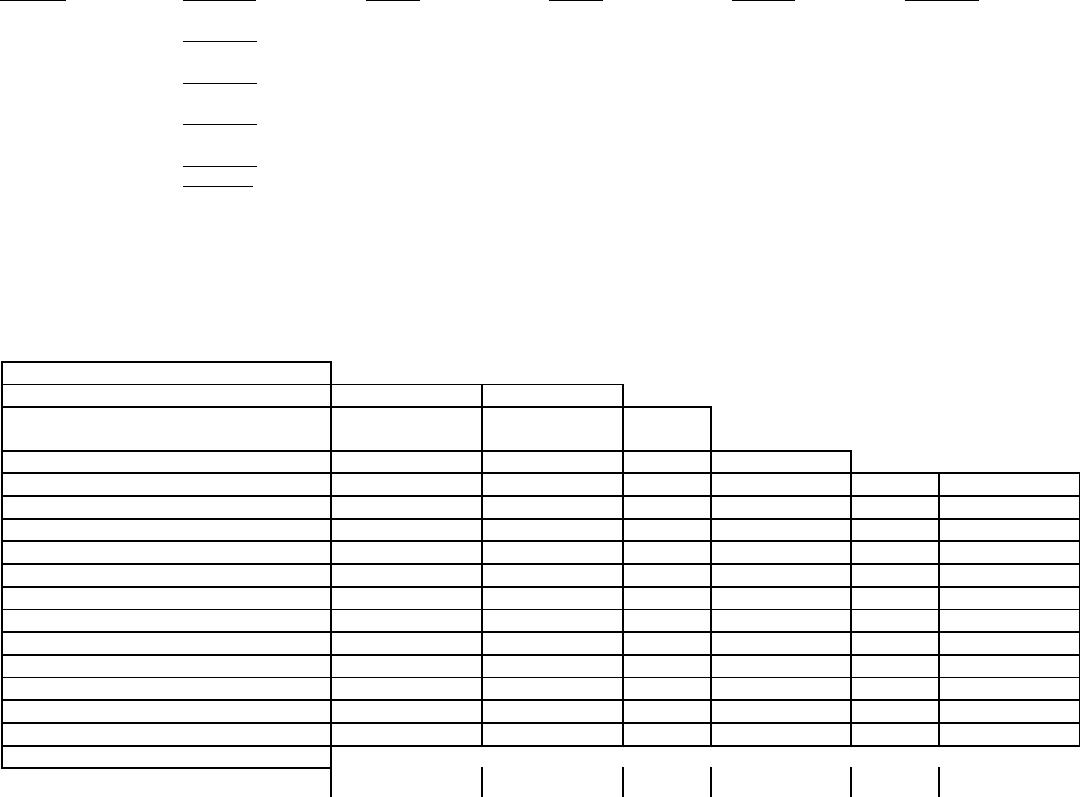

Required:

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-11 partial worksheet as of December 31, 20X3. Key

and explain all eliminations and adjustments.

Figure 5-11

Trial Balance

Eliminations and

Parent

Sub.

Adjustment

s

Account Titles

Company

Company

Debit

Credit

Min. Lease Payments Rec.

120,000

Unearned Interest Income

(6,429)

Buildings and Equipment

350,000

300,000

Accumulated Depreciation

(120,000)

(80,000)

Equipment under Cap. Lease

204,110

Acc. Depr. – Eq. Cap. Lease

(68,037)

Obligation under Cap. Lease

(101,403)

Interest Payable on Lease

(12,168)

Interest Income on Lease

(12,168)

Interest Expense on Lease

12,168

(continued)

Consol.

Control.

Consol.

Income

Retained

Balance

Account Titles

Statement

NCI

Earnings

Sheet

Min. Lease Payments Rec.

Unearned Interest Income

Buildings and Equipment

Accumulated Depreciation

Equipment under Cap. Lease

Acc. Depr. – Eq. Cap. Lease

Obligation under Cap. Lease

Interest Payable on Lease

Interest Income on Lease

Interest Expense on Lease

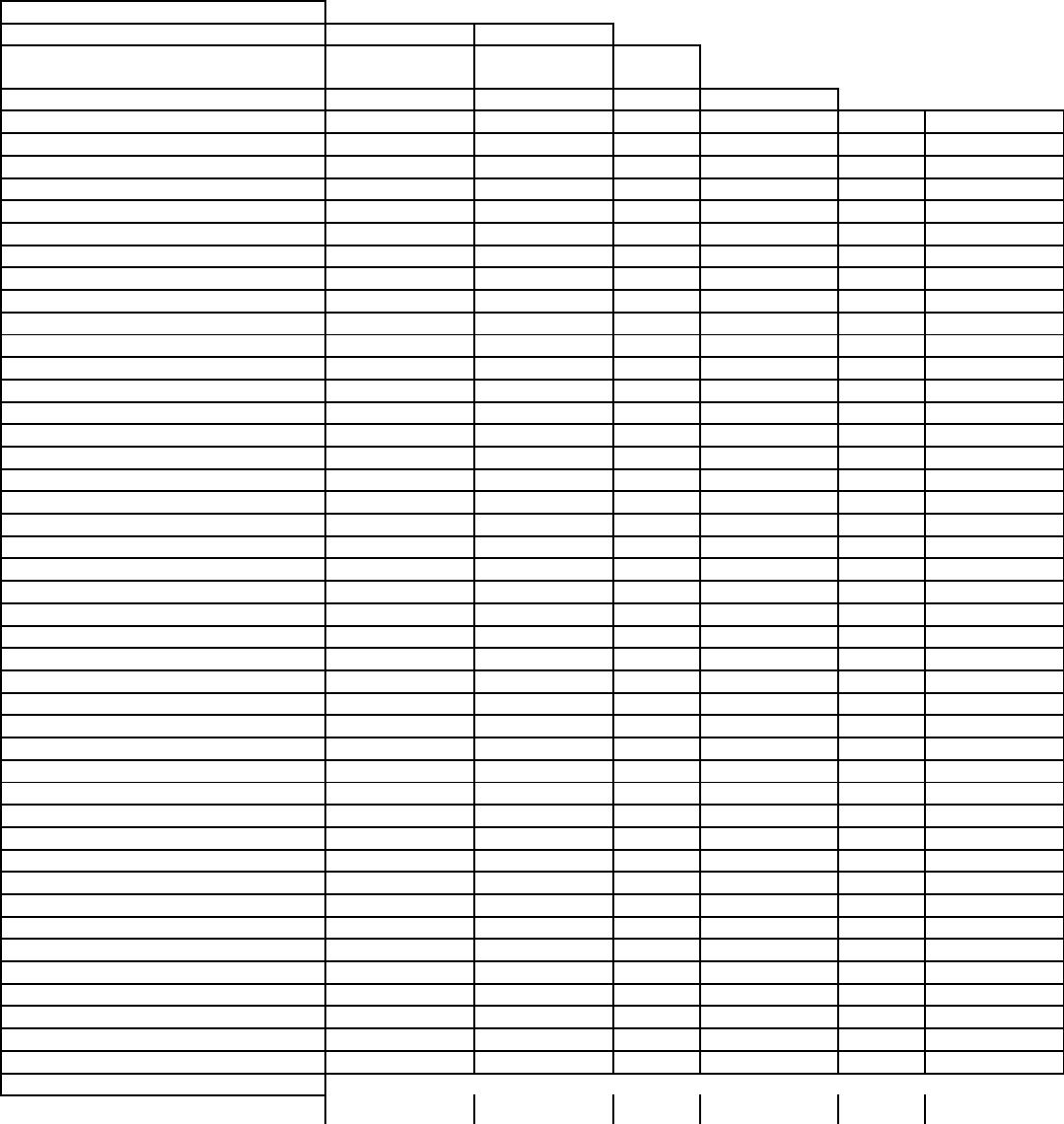

49. On January 1, 20X1, Parent Company purchased 100% of the common stock of Subsidiary Company for

$390,000. On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $50,000,

$100,000, and $200,000 respectively. Any excess of cost over book value is due to goodwill. Parent accounts

for the Investment in Subsidiary using the simple equity method.

On January 1, 20X2, Parent purchased equipment for $204,120 and immediately leased the equipment to

Subsidiary on a 4-year lease. The minimum lease payments of $60,000 are to be made annually on January 1,

beginning immediately, for a total of 4 payments. The implicit interest rate is 12%. The lease provides for an

automatic transfer of title at the end of 4 years. The estimated useful life of the equipment is 6 years. The lease

has been capitalized by both companies.

A lease amortization schedule, applicable to either company, is presented below:

Carrying

Carrying

Interest

Principal

Value on

Value

Rate

Interest

Payment

Reduction

1-1-X2

$204,120

– 60,000

1-1-X2

144,120

12%

$17,294

$60,000

$42,706

– 42,706

1-1-X3

101,414

12%

12,170

60,000

47,830

– 47,830

1-1-X4

53,584

12%

6,416*

60,000

53,584

– 53,584

1-1-X5

$ 0

*Adjusted for

rounding error.

On January 1, 20X3, Parent held merchandise acquired from Subsidiary for $10,000. During 20X3, subsidiary sold merchandise to Parent for

$50,000, of which $15,000 is held by Parent on December 31, 20X3. Subsidiary’s usual gross profit on affiliated sales is 40%.

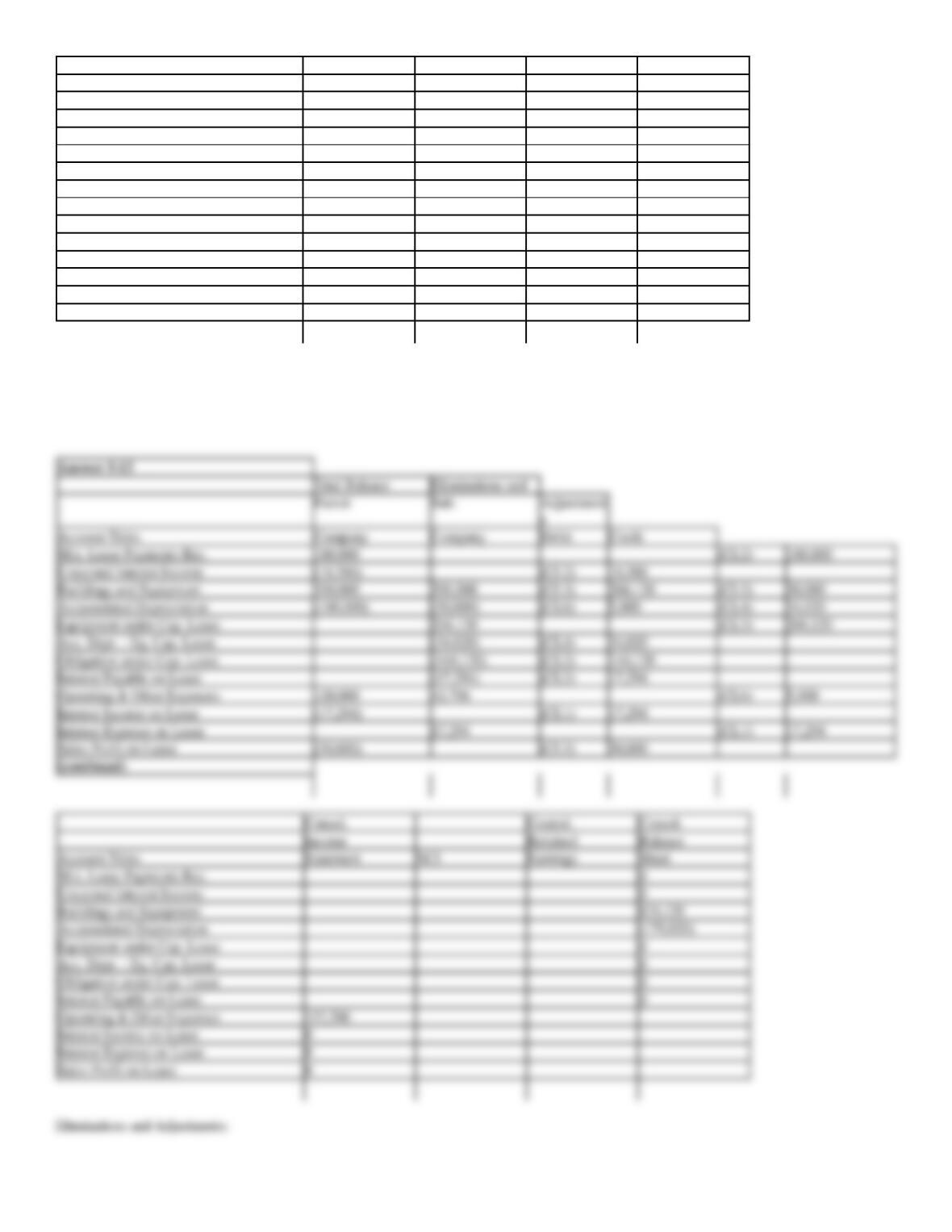

Required:

Complete the Figure 5-12 worksheet for consolidated financial statements for the year ended December 31, 20X3. Round all computations to the

nearest dollar.

Figure 5-12

Trial Balance

Eliminations and

Parent

Sub.

Adjustment

s

Account Titles

Company

Company

Debit

Credit

Current Assets

234,196

280,504

Min. Lease Payments Rec.

120,000

Unearned Interest Income

(6,416)

Investment in Sub. Company

560,000

Land

100,000

60,000

Buildings and Equipment

350,000

300,000

Accumulated Depreciation

(120,000)

(80,000)

Equipment under Cap. Lease

204,120

Acc. Depr. – Eq. Cap. Lease

(68,040)

Goodwill

Current Liabilities

(135,000)

(48,000)

Obligation under Cap. Lease

(101,414)

Interest Payable on Lease

(12,170)

Other Long-Term Liabilities

(200,000)

(15,000)

Common Stock – P Co.

(200,000)

Other Paid-in Capital – P Co.

(100,000)

Retained Earnings – P Co.

(482,780)

Common Stock – S Co.

(50,000)

Other Paid-in Capital – S Co.

(100,000)

Retained Earnings – S Co.

(310,000)

Net Sales

(600,000)

(350,000)

Cost of Goods Sold

372,170

200,000

Operating & Other Expenses

140,000

67,830

Interest Income on Lease

(12,170)

Interest Expense on Lease

12,170

Subsidiary Income

(70,000)

Dividends Declared – P Co.

50,000

Dividends Declared – S Co.

10,000

Consolidated Net Income

To NCI

To Controlling Interest

Total NCI

Ret. Earn. Contr. Int. 12-31

0

0

(continued)

Consol.

Control.

Consol.

Income

Retained

Balance

Account Titles

Statement

NCI

Earnings

Sheet

Current Assets

Min. Lease Payments Rec.

Unearned Interest Income

Investment in Sub. Company

Land

Buildings and Equipment

Accumulated Depreciation

Equipment under Cap. Lease

Acc. Depr. – Eq. Cap. Lease

Goodwill

Current Liabilities

Obligation under Cap. Lease

Interest Payable on Lease

Other Long-Term Liabilities

Common Stock – P Co.

Other Paid-in Capital – P Co.

Retained Earnings – P Co.

Common Stock – S Co.

Other Paid-in Capital – S Co.

Retained Earnings – S Co.

Net Sales

Cost of Goods Sold

Operating & Other Expenses

Interest Income on Lease

Interest Expense on Lease

Subsidiary Income

Dividends Declared – P Co.

Dividends Declared – S Co.

Consolidated Net Income

To NCI

To Controlling Interest

Total NCI

Ret. Earn. Contr. Int. 12-31

For the worksheet solution, please refer to Answer 5-12.

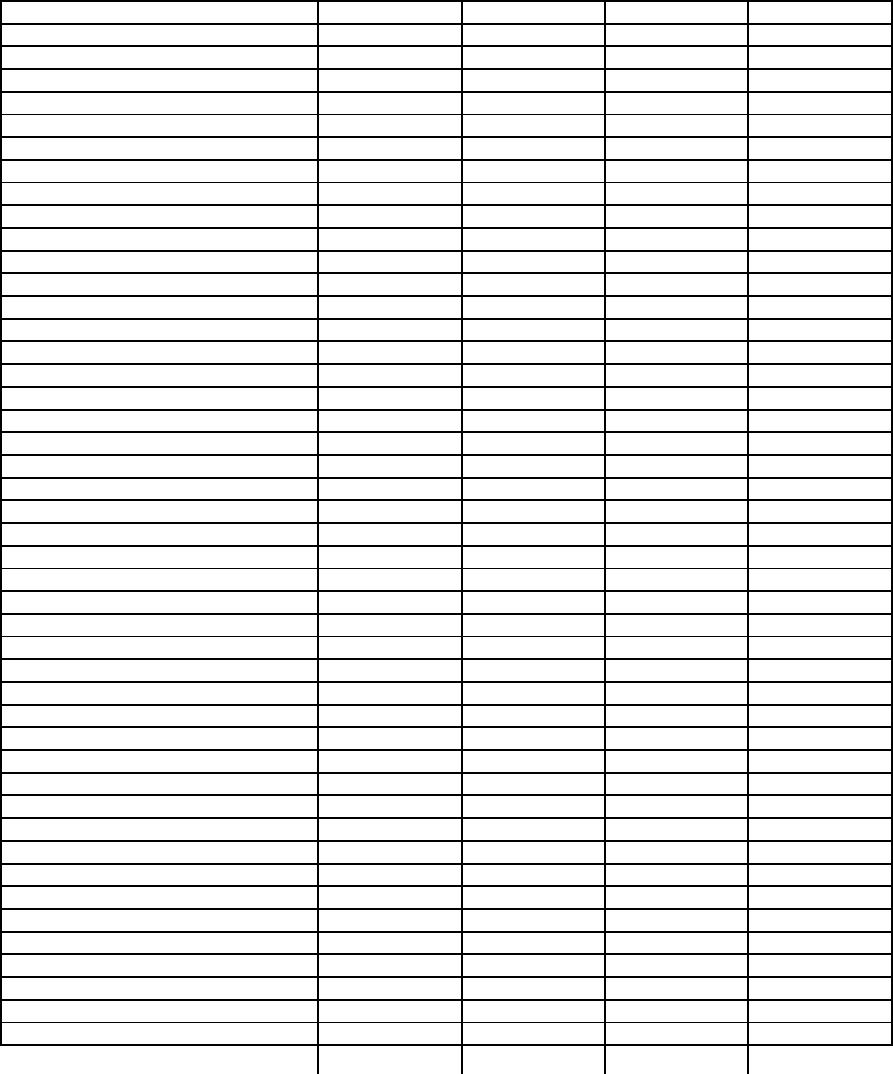

50. On January 1, 20X1, Parent Company acquired 100% of the common stock of Subsidiary Company for

$365,000. On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $50,000,

$100,000, and $200,000 respectively. Any excess of cost over book value is due to goodwill. Parent uses the

simple equity method to account for its investment in subsidiary.

On January 1, 20X2, Parent purchased equipment for $174,120 and immediately leased the equipment to

Subsidiary on a 4-year lease. The transaction was legally structured as a sales-type lease with a present value for

the minimum lease payments of $204,120. Parent recorded the following entry:

Minimum Lease Payments Receivable

240,000

Unearned Interest Income

35,880

Equipment

174,120

Sales Profit on Lease

30,000

The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments. The implicit

interest rate is 12%. The lease provides for an automatic transfer of title at the end of 4 years. The estimated useful life of the equipment is 6 years.

The lease has been capitalized by both companies.

A lease amortization schedule, applicable to either company, is presented below:

Carrying

Carrying

Interest

Principal

Value on

Value

Rate

Interest

Payment

Reduction

1-1-X2

$204,120

– 60,000

1-1-X2

144,120

12%

$17,294

$60,000

$42,706

– 42,706

1-1-X3

101,414

12%

12,170

60,000

47,830

– 47,830

1-1-X4

53,584

12%

6,416*

60,000

53,584

– 53,584

1-1-X5

$ 0

*Adjusted for

rounding error.

Required:

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-13 partial worksheet as of December 31, 20X2. Key and

explain all eliminations and adjustments.

Figure 5-13

Trial Balance

Eliminations and

Parent

Sub.

Adjustment

s

Account Titles

Company

Company

Debit

Credit

Min. Lease Payments Rec.

180,000

Unearned Interest Income

(18,586)

Buildings and Equipment

350,000

300,000

Accumulated Depreciation

(100,000)

(50,000)

Equipment under Cap. Lease

204,120

Acc. Depr. – Eq. Cap. Lease

(34,020)

Obligation under Cap. Lease

(144,120)

Interest Payable on Lease

(17,294)

Operating & Other Expenses

120,000

42,706

Interest Income on Lease

(17,294)

Interest Expense on Lease

17,294

Sales Profit on Lease

(30,000)

(continued)

Consol.

Control.

Consol.

Income

Retained

Balance

Account Titles

Statement

NCI

Earnings

Sheet

Min. Lease Payments Rec.

Unearned Interest Income

Buildings and Equipment

Accumulated Depreciation

Equipment under Cap. Lease

Acc. Depr. – Eq. Cap. Lease

Obligation under Cap. Lease

Interest Payable on Lease

Operating & Other Expenses

Interest Income on Lease

Interest Expense on Lease

Sales Profit on Lease

For the parital worksheet solution, please refer to Answer 5-13.

Trial Balance

Eliminations and

Account Titles

Company

Company

Debit

Credit

Min. Lease Payments Rec.

180,000

(CL2)

180,000

Unearned Interest Income

(18,586)

(CL2)

18,586

Buildings and Equipment

350,000

300,000

(CL3)

204,120

(CL5)

30,000

Accumulated Depreciation

(100,000)

(50,000)

(CL6)

5,000

(CL4)

34,020

Equipment under Cap. Lease

204,120

(CL3)

204,120

Acc. Depr. – Eq. Cap. Lease

(34,020)

(CL4)

34,020

Obligation under Cap. Lease

(144,120)

(CL2)

144,120

Interest Payable on Lease

(17,294)

(CL2)

17,294

Operating & Other Expenses

120,000

42,706

(CL6)

5,000

Interest Income on Lease

(17,294)

(CL1)

17,294

Interest Expense on Lease

17,294

(CL1)

17,294

Sales Profit on Lease

(30,000)

(CL5)

30,000

Consol.

Control.

Consol.

Income

Retained

Balance

Account Titles

Statement

NCI

Earnings

Sheet

Min. Lease Payments Rec.

0

Unearned Interest Income

0

Buildings and Equipment

824,120

Accumulated Depreciation

(179,020)

Equipment under Cap. Lease

0

Acc. Depr. – Eq. Cap. Lease

0

Obligation under Cap. Lease

0

Interest Payable on Lease

0

Operating & Other Expenses

157,706

Interest Income on Lease

0

Interest Expense on Lease

0

51. The Planes Company owns 100% of the outstanding common stock of the Sands Company. Sands issued

$100,000 of face value, 9%, 10-year bonds on January 1, 20X3, for $96,000. The discount is being amortized

on a straight-line basis. On January 1, 20X8, Planes purchased all the bonds as an investment for $95,000.

Required:

Be specific in answering the following questions and include numerical explanations.

a.

How will this bond issue be recorded and accounted for in 20X8 on the separate books of Planes and Sands?

b.

How will this bond issue be accounted for on the 20X8 consolidated statements?

c.

How will this bond issue be recorded and accounted for in 20X9 on the separate books of Planes and Sands?

d.

How will this bond issue be accounted for on the 20X9 consolidated statements?

(CL1)

Eliminate the intercompany interest income and expense on the lease obligation (per table).

The payable is also $161,414 ($144,120 lease obligation payable plus $17,294 interest payable).

(CL3)

Reclassify the leased equipment as ordinary Building and Equipment.

(CL5)

Eliminate the Sales Profit on Lease and adjust the leased asset back to cost.

52. The Park Company owns 80% of the outstanding common stock of the Sea Company. Park is about to lease

a machine with a 5-year life to the Sea Company. The lease would begin January 1, 20X3.

Required:

Explain the adjustments that will be required in the consolidation process if each of the following occurs.

a.

The lease is an operating lease.

b.

The lease is a direct financing lease with a bargain purchase option.

c.

The lease is a sales-type lease with a bargain purchase option.

a normal productive asset.