48. The following are selected activities for the Monterey City Natural Gas Company, a governmental entity:

a.

Billing for the year:

To outside customers

$400,000

To other Monterey City funds

70,000

b.

Service provided to outside customers but not billed by year end totaled $28,000.

c.

During the year, $2,500 was collected from new customers as a refundable connection fee.

d.

The utility sold $300,000 of 6% revenue bonds at 97 on an interest payment date. Proceeds are earmarked for

construction.

e.

Depreciation for the year was as follows:

Buildings

$30,000

Improvements other than buildings

14,000

Machinery and equipment

96,000

f.

The utility refunded $1,000 of deposits to customers who had moved.

Required:

Prepare journal entries to record the activities.

a.

Accounts Receivable

400,000

Due from Other Funds

70,000

Operating Revenues

470,000

b.

Accounts Receivable

28,000

Operating Revenues

28,000

c.

Restricted Assets—Customers’ Deposits

Cash

2,500

Customers’ Deposits Payable from

Restricted Assets

2,500

d.

Restricted Assets—Revenue Bond

Construction Cash

291,000

Unamortized Bond Discount on Revenue

Bonds

9,000

6% Revenue Bonds Payable

300,000

e.

Depreciation Expense

140,000

Accumulated Depreciation—Building

30,000

Accumulated Depreciation—Improvements

Other Than Building

14,000

Accumulated Depreciation—Machinery

and Equipment

96,000

Customers’ Deposits Payable from

Restricted Assets

1,000

Restricted Assets—Customers’ Deposits

Cash

1,000

49. Given the following information for the City of Youngstown Municipal Golf Course:

Cash Balance 1/1/01

$ 25,000

User Fees-Green Fees

375,000

Net Repayment-Revolving Loan

35,000

Operating Transfer Out-General Fund (property taxes)

50,000

User Fees-League Fees and outings

100,000

User Fees-Memberships

25,000

Cash Expenses Paid to suppliers

95,000

Interest/Dividends Received

12,000

Acquisition/Improvement to Clubhouse

75,000

Cash Expenses Paid to employees

105,000

Cash Expenses Paid Maintenance and Upkeep

100,000

Principal and Interest Payments on Bond

50,000

Prepare a cash flow statement for this enterprise fund.

City of Youngstown

Municipal Golf Course Fund

Statement of Cash Flows

Increase/(Decrease) in Cash and Cash Equivalents

For Year Ended 12/31/01

Cash Flows from Operating Activities:

Cash Received from Customers (1)

500,000

Cash Paid for Operating Expenses (2)

(300,000)

Net Cash Provided by Operating Activities

200,000

Cash Flows from Noncapital

Financing Activities:

Net Repayments-Revolving Loan

(35,000)

Operating Transfers Out-to other funds

(50,000)

Net Cash Used in Noncapital

Financing Activities

(85,000)

Cash Flows from Capital

and Related Financing Activities:

Principal and interest paid on bonds

(50,000)

Acquisition and

construction-capital assets

(75,000)

Net Cash Used in Capital and Related

Financing Activities

(125,000)

Cash Flows from Investing Activities:

Interest and Dividends Received

12,000

Net Cash Provided by Investing Activities

12,000

Net Increase in Cash and Cash Equivalents

2,000

Cash and Cash Equivalents 1/1/01

25,000

Cash and Cash Equivalents 12/31/01

27,000

50. Rankin City established a Central Printing and Reproductions Fund during the fiscal year ending 6/30/05.

Transactions affecting the fund are as follows:

a.

The fund was established with a $100,000 contribution from the General Fund on 7/1/04. The transfer will be recorded as Contributed

Capital for the fund.

b.

Equipment costing $30,000 was acquired on 7/3/04. The equipment is assigned a 10 year life, no salvage. It will be paid at a future date.

c.

Supplies costing $65,000 were acquired. A physical inventory was taken on 6/30/05 of the supplies, the count showed supplies valued at

$11,000. The voucher will be paid at a later date.

d.

Various operating expenses were incurred for a total of $67,000. Of that amount, $7,000 represented charges from the city’s electric utility

(an enterprise fund). All the vouchers were then paid. The payments for the equipment and supplies acquisition are also made.

e.

Total billings to the city’s various departments were $125,000. Of this amount, $9,000 pertained to services performed for the city’s electric

utility (enterprise fund).

f.

Cash was collected on the above billings in full.

Required:

Make the necessary journal entries for fiscal year 2004-2005 (ending 6/30/05) for Rankin City’s Internal Service Fund including any year end

adjusting entries. Closing entries are not required.

Cash

100,000

Interfund transfers-in—Contributions from Municipality

100,000

b.

Equipment

30,000

Vouchers Payable

30,000

Supplies Inventory

65,000

Vouchers Payable

65,000

d.

Operating Expenses

67,000

Vouchers Payable

60,000

Due to Electric Utility Fund

7,000

Vouchers Payable

155,000

Due to Electric Utility Fund

7,000

Cash

162,000

Due from the General Fund

116,000

Due from Electric Utility Fund

9,000

Operating Revenues

125,000

f.

Cash

125,000

Due from the General Fund

116,000

Due from Electric Utility Fund

9,000

Necessary Year End Adjustments

Depreciation Expense

3,000

Accumulated Depreciation

3,000

Operating Expenses

54,000

Supplies Inventory

54,000

51. The City of Light Falls operates a centralized garage and charges the other departments on a per-mile basis

for the purchase and maintenance of most city-owned vehicles.

Required:

Make journal entries to record the following selection of transactions concerning the motor pool during the

following year:

a.

Salaries of $360,000 were paid during the year.

b.

A bill from the Water and Sewer Enterprise Fund for $8,000 was received and paid.

c.

Eight new vehicles costing $24,000 each were purchased for cash.

d.

Billing to other city funds were as follows:

General Fund

$550,000

Utility Fund

130,000

Special Revenue Fund

20,000

e.

All of the billings in (d) except $50,000 from the Utility Fund were paid.

f.

Depreciation expense on the motor pool assets was $225,000 for the year.

a.

Operating Expenses

360,000

Cash

360,000

b.

Operating Expenses

8,000

Cash

8,000

c.

Vehicles

192,000

Cash

192,000

d.

Due from General Fund

550,000

Due from Utility Fund

130,000

Due from Special Revenue Fund

20,000

Operating Revenue

700,000

e.

Cash

650,000

Due from General Fund

550,000

Due from Utility Fund

80,000

Due from Special Revenue Fund

20,000

Operating Expenses

225,000

Allowance for Depreciation—Vehicles

225,000

52. The following selected events occurred in Hershey City’s Internal Service Fund for its automobile fleet:

a.

An automobile fleet Internal Service Fund was established. The General Fund

provided $85,000 for its working capital. Of this amount, $40,000 is to be repaid

in equal annual installments over a five-year period. The remaining $45,000 is a

contribution that will not be repaid.

b.

Billings for services to other funds are as follows:

To the General Fund

$608,000

To an Enterprise Fund

$112,000

c.

A one-year insurance policy is purchased. By year end, one-half of the $18,000

premium payment has expired.

d.

Depreciation for the period:

Building

$ 4,500

Machinery and equipment

$65,000

e.

Invoices for various goods and services received totaled $127,000.

Required:

Omitting explanations, prepare journal entries for all funds and groups affected, using the following format:

Funds or Account

Event

Groups Affected

Journal Entries

53. A Nonexpendable Trust Fund was established to help pay for Little League baseball. A total of $100,000

was donated to Babe City. The earnings, not the principal, from the donation could be used to fund baseball.

Required:

Make the entries and identify the fund into which the following transactions should be made:

a.

The donation is received and invested immediately in a mutual stock fund.

b.

Cash dividends of $8,500 were received from the mutual fund and made available for spending.

c.

During the first baseball season, $8,300 was spent from the fund.

d.

The closing entries were made.

a.

Endowment Principal Fund

Cash

100,000

Fund Balance

100,000

Investments

100,000

Cash

100,000

b.

Endowment Principal Fund

Cash

8,500

Revenue

8,500

Cash

8,500

Endowment Earnings Fund

Cash

8,500

Other Financing Sources

8,500

Endowment Earnings Fund

Expenditures

8,300

Cash

8,300

d.

Endowment Principal Fund

Revenue

8,500

Operating Transfer Out

8,500

Endowment Earnings Fund

Other Financing Sources

8,500

Expenditures

8,300

Fund Balance—Unassigned

200

54. Consider the following transactions:

a.

The Cline County Tax Agency Fund was established to account for the county’s responsibility of collecting Brent City and Cline County

property taxes. The levies for 20X1 were $800,000 for the County General Fund and $400,000 for the City General Fund.

b.

Collections were $750,000 (in proportion to levies).

c.

The county is entitled to a fee of 1% of taxes collected for Brent City; the net amount due is sent to the city. Liabilities to all funds and

units were recorded to date.

d.

All moneys collected to date were released to each government unit.

Required:

Prepare the general journal entries required to record the following transactions in Cline County Tax Agency Fund.

Tax Receivable for All Units

1,200,000

Due to Other Governmental Funds and Units

1,200,000

b.

Cash

750,000

Tax Receivable for All Units

750,000

Due to Other Governmental Funds and Units

750,000

Due to Cline County General Fund (1)

502,500

Due to Brent City (2)

247,500

d.

Due to Cline County General Fund

502,500

Due to Brent City

247,500

Cash

750,000

55. In the space provided, fill in the name of the one fund or account group in which each of the following items

is most likely to be recorded.

Item

Name of Fund or Group

(1)

Services financed by user fees charged against other funds

_______________________________

(2)

Resources used for construction of major general fixed assets

_______________________________

(3)

Operations of general governmental functions

_______________________________

(4)

Assets held for distribution to other governments or for individuals

_______________________________

(5)

Accumulation of resources for and payment of general long-term

debt assets

_______________________________

(6)

Total historical cost of buildings owned by the government

_______________________________

(7)

Activities related to an employee retirement program

_______________________________

(8)

Services financed by user charges against the general public

_______________________________

(9)

Accountability for assets whose principal must be preserved and are

invested to produce earnings for a designated external purpose

_______________________________

Internal Service Fund

Capital Projects Fund

General Fund

Agency Fund

Debt Service Fund

General Fixed Assets Account Group

Pension Trust Fund

Enterprise Fund

Private Purpose Trust

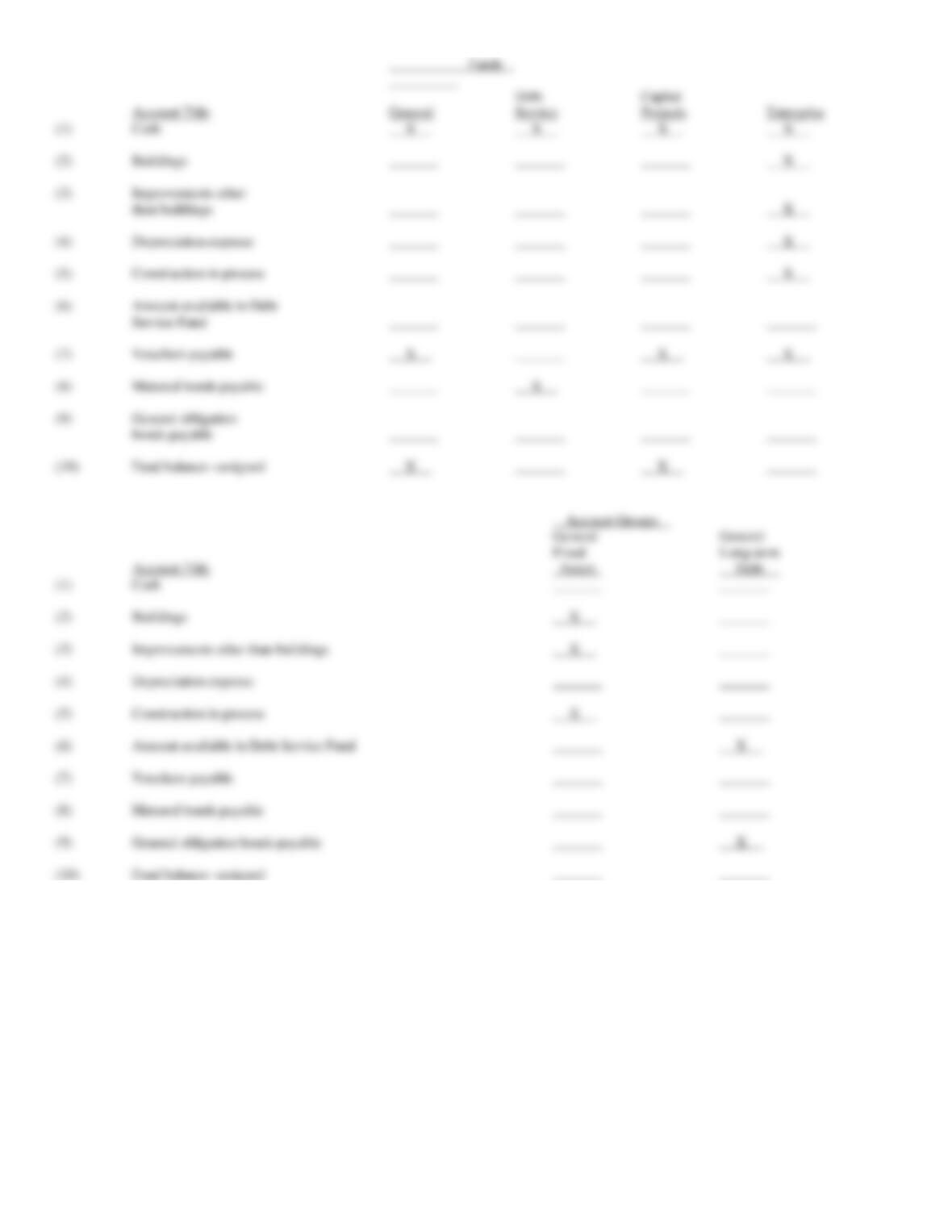

56. Place a check mark in the appropriate column to indicate in which of the following funds and accounts

groups the given accounts would commonly be found:

Funds

Debt

Capital

Account Title

General

Service

Projects

Enterprise

(1)

Cash

_______

_______

_______

_______

(2)

Buildings

_______

_______

_______

_______

(3)

Improvements other

than buildings

_______

_______

_______

_______

(4)

Depreciation expense

_______

_______

_______

_______

(5)

Construction in process

_______

_______

_______

_______

(6)

Amount available in

Debt Service Fund

_______

_______

_______

_______

(7)

Vouchers payable

_______

_______

_______

_______

(8)

Matured bonds payable

_______

_______

_______

_______

(9)

General obligation

bonds payable

_______

_______

_______

_______

(10)

Fund balance—assigned

_______

_______

_______

_______

Account Groups

General

General

Fixed

Long-term

Account Title

Assets

Debt

(1)

Cash

_______

_______

(2)

Buildings

_______

_______

(3)

Improvements other than buildings

_______

_______

(4)

Depreciation expense

_______

_______

(5)

Construction in process

_______

_______

(6)

Amount available in Debt Service Fund

_______

_______

(7)

Vouchers payable

_______

_______

(8)

Matured bonds payable

_______

_______

(9)

General obligation bonds payable

_______

_______

(10)

Fund balance—assigned

_______

_______

57. The following selected events occurred in the City of Canterbury.

a.

On December 31, 20X7, $250,000 was transferred from the General Fund to establish a central garage

to service the city’s vehicles. Of this amount, $150,000 was spent on January 2, 20X8, to acquire a

building with an estimated life of 25 years, $30,000 was spent for the acquisition of land, and $60,000

was paid for equipment with an estimated life of 10 years.

b.

During the six months of operation to June 30, 20X8, the garage billed the General Fund for $24,000

and Enterprise Funds for $50,000. Except for $8,000 still due from Enterprise Funds, the balance is

collected.

c.

Canceled checks revealed the following payments for garage activities:

Salaries (ignore deductions and taxes)

$31,000

Parts and supplies (perpetual system)

19,000

Service provided by the city-owned utility

2,000

Total payments

$52,000

d.

At fiscal year end, the following adjustments were related to garage operations:

Inventory of parts and supplies on hand

$7,000

Depreciation

To be

computed.

e.

On July 1, 20X7, the city issued 10-year, $400,000, 8% general obligation serial bonds at 101 to

finance the construction of a public health center for the aging. The premium on the bond sale is

transferred to the Debt Service Fund for interest payment. Each $40,000 serial is redeemable on June

30, along with annual interest on the outstanding bond face value. The project is estimated to cost

$430,000 and will be completed in less than one year. The General Fund will transfer resources, if

needed, to cover the total cost. The city uses budgetary accounts for these projects.

f.

During the fiscal year, construction of the public health center was completed at a cost of $426,000, of

which $400,000 was paid, the remainder is payable after one year under a retained percentage contract

arrangement. The $26,000 deficiency was transferred from the General Fund.

g.

On June 28, 20X8, $68,000 is transferred from the General Fund to be applied to the payment of the

first $40,000 bond serial mentioned in e., plus interest. On this date, the Debt Service Fund records the

maturing bonds and interest.

h.

On June 30, the payment for the matured bond serial and interest is made.

Required:

For each event, prepare the necessary journal entries for all funds and account groups involved during the fiscal year ended June 30, 20X8. Indicate

the fund or group in which the entries are made.

58. The City of Newport operates its own solid waste landfill and charges fees to users who dump solid waste in

the landfill. When should estimated costs for closure and post-closure care be accounted for?

59. What is escheat property and how do we account for it?

60. What reporting is required for the accounting for employee Pension Trust Funds.