39. On January 1, 20X1, Powers Company acquired 80% of the common stock of Sculley Company for

$195,000. On this date Sculley had total owners’ equity of $200,000 (common stock, other paid-in capital, and

retained earnings of $10,000, $90,000, and $100,000 respectively).

Any excess of cost over book value is attributable to inventory (worth $6,250 more than cost), to equipment

(worth $12,500 more than book value), and to patents. FIFO is used for inventories. The equipment has a

remaining life of five years and straight-line depreciation is used. The excess to the patents is to be amortized

over 20 years.

On July 1, 20X2 Sculley borrowed $100,000 from Powers with a 10% 1-year note; interest is due at maturity.

On January 1, 20X2, Powers held merchandise acquired from Sculley for $10,000. During 20X2, Sculley sold

merchandise to Powers for $50,000, $20,000 of which is still held by Powers on December 31, 20X2. Sculley’s

usual gross profit on affiliated sales is 50%.

On December 31, 20X1, Powers sold equipment to Sculley at a gain of $10,000. During 20X2, the equipment

was used by Sculley. Depreciation is being computed using the straight-line method, a five-year life, and no

salvage value.

Both companies have a calendar-year fiscal year.

Assume that during 20X1 and 20X2, Powers has appropriately accounted for its investment in Sculley using the

cost method.

Required:

a.

Using the information above or on the Figure 4-5 worksheet, prepare a determination and distribution of excess schedule.

b.

Complete the Figure 4-5 worksheet for consolidated financial statements for the year ended December 31, 20X2.

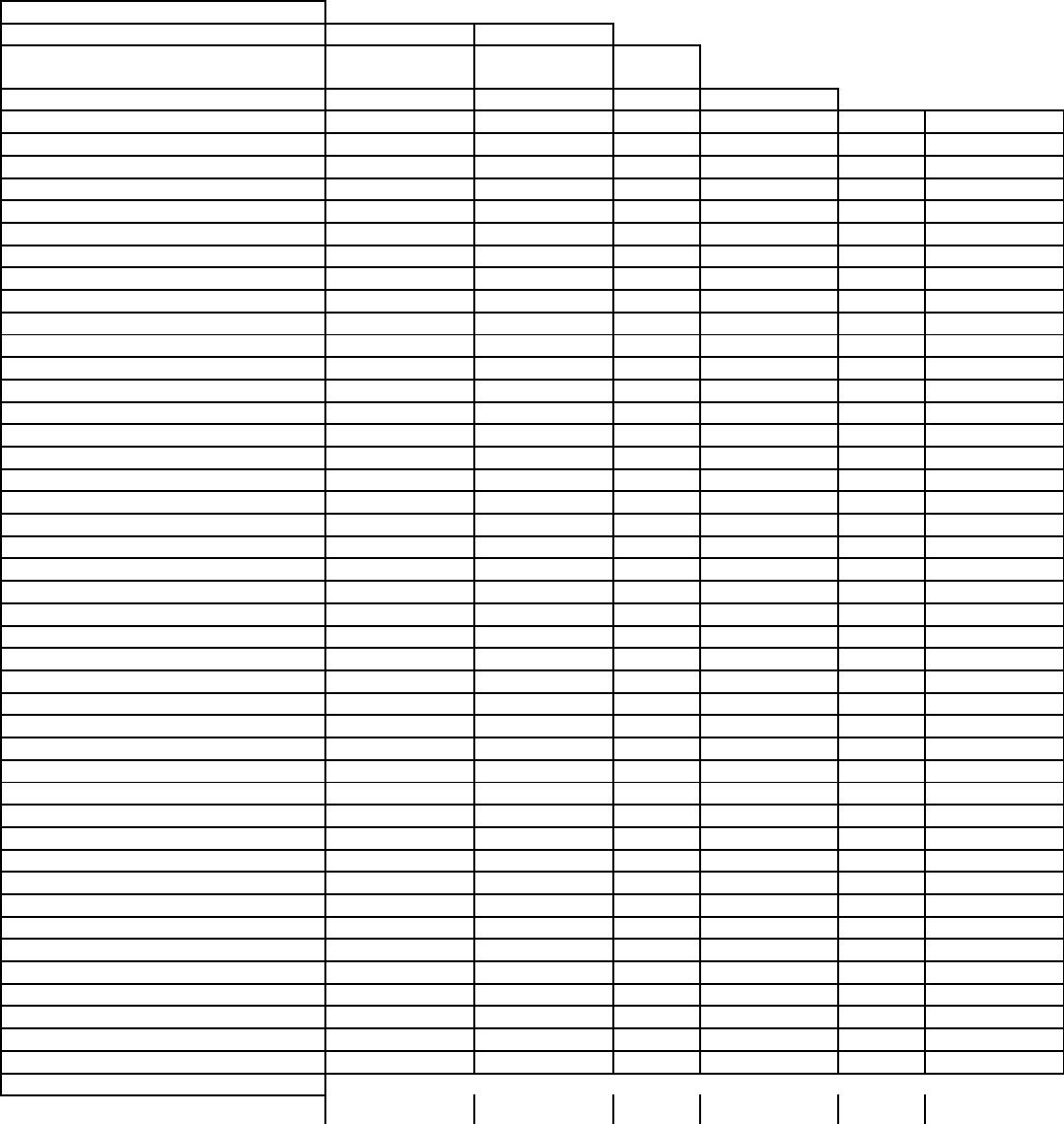

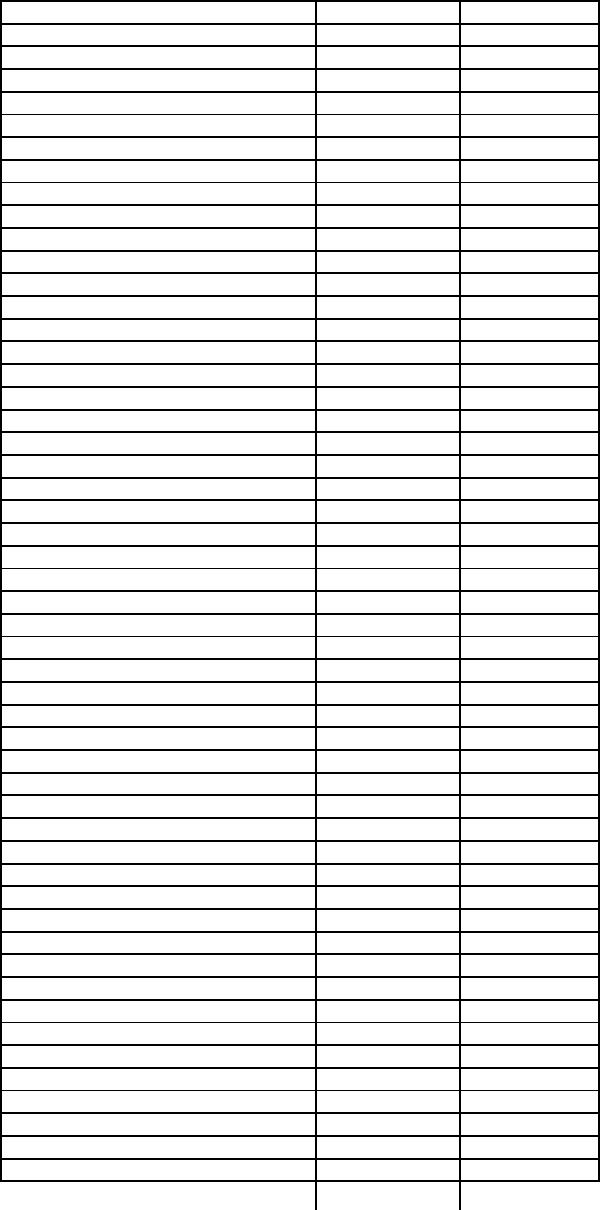

Figure 4-5

Trial Balance

Eliminations and

Powers

Sculley

Adjustment

s

Account Titles

Company

Company

Debit

Credit

Inventory, December 31

145,000

55,000

Other Current Assets

249,000

205,000

Investment in Sub. Company

195,000

Land

140,000

100,000

Buildings and Equipment

400,000

200,000

Accumulated Depreciation

(150,000)

(50,000)

Current Liabilities

(150,000)

(120,000)

Bonds Payable

(100,000)

(50,000)

Other Long-Term Liabilities

(50,000)

(20,000)

Common Stock – P Co.

(100,000)

Other Paid in Capital – P Co.

(200,000)

Retained Earnings – P Co.

(310,000)

Common Stock – S Co.

(10,000)

Other Paid in Capital – S Co.

(90,000)

Retained Earnings – S Co.

(150,000)

Net Sales

(610,000)

(365,000)

Cost of Goods Sold

360,000

190,000

Operating Expenses

150,000

70,000

Interest Revenue

(5,000)

Interest Expense

5,000

Dividend Income

(24,000)

Dividends Declared – P Co.

60,000

Dividends Declared – S Co.

30,000

Consolidated Net Income

NCI

Controlling Interest

Total NCI

Ret. Earn. Contr. Int. 12-31

0

0

(continued)

Consol.

Control.

Consol.

Income

Retained

Balance

Account Titles

Statement

NCI

Earnings

Sheet

Inventory, December 31

Other Current Assets

Investment in Sub. Company

Land

Buildings and Equipment

Accumulated Depreciation

Current Liabilities

Bonds Payable

Other Long-Term Liabilities

Common Stock – P Co.

Other Paid in Capital – P Co.

Retained Earnings – P Co.

Common Stock – S Co.

Other Paid in Capital – S Co.

Retained Earnings – S Co.

Net Sales

Cost of Goods Sold

Operating Expenses

Interest Revenue

Interest Expense

Dividend Income

Dividends Declared – P Co.

Dividends Declared – S Co.

Consolidated Net Income

NCI

Controlling Interest

Total NCI

Ret. Earn. Contr. Int. 12-31

a.

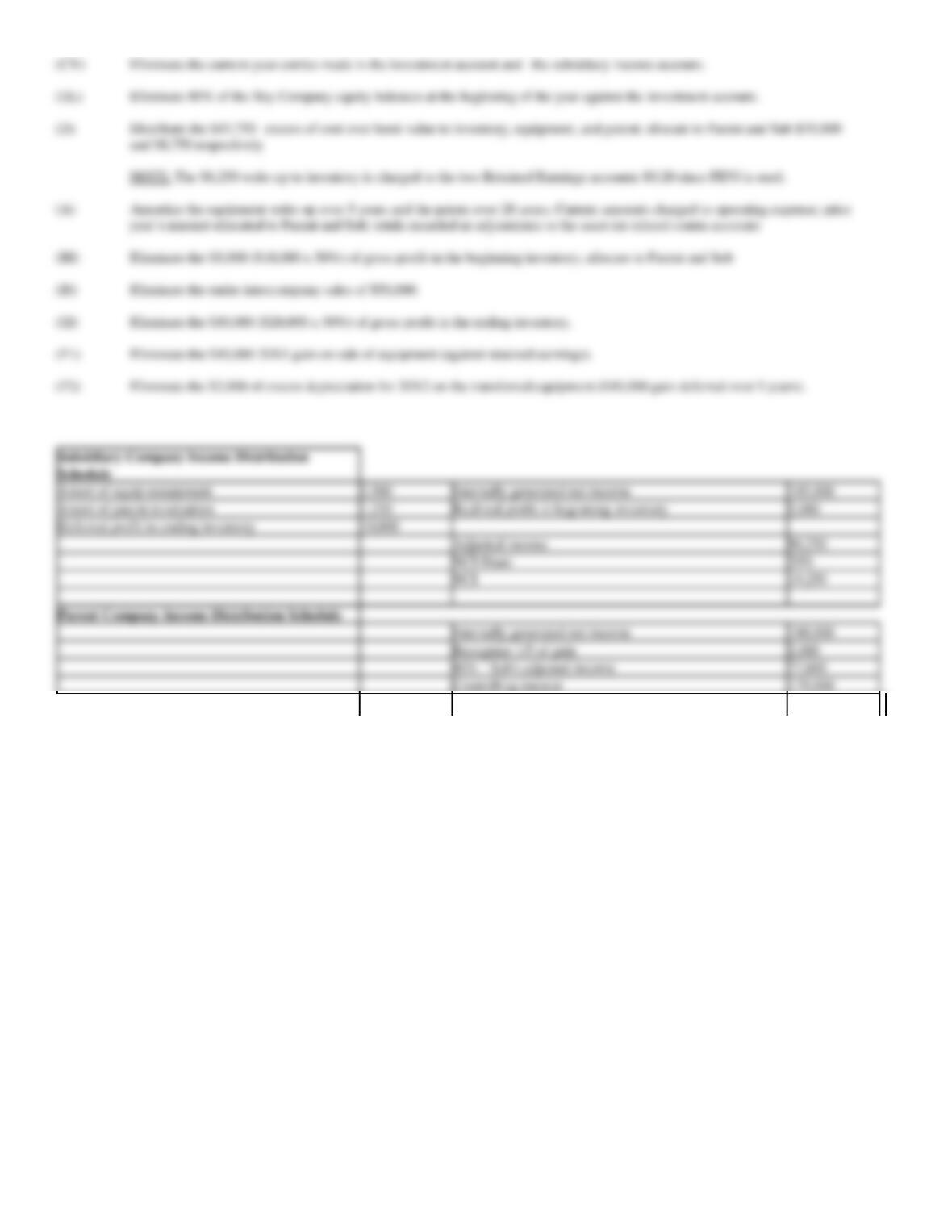

40. On January 1, 20X1, Pep Company acquired 80% of the common stock of Sky Company for $195,000. On

this date Sky had total owners’ equity of $200,000 (common stock, other paid-in capital, and retained earnings

of $10,000, $90,000, and $100,000 respectively).

Any excess of cost over book value is attributable to inventory (worth $6,250 more than cost), to equipment

(worth $12,500 more than book value), and to patents. FIFO is used for inventories. The equipment has a

remaining life of five years and straight-line depreciation is used. The excess attributable to the patents is to be

amortized over 20 years.

During 20X1 and 20X2, Pep has appropriately accounted for its investment in Sky using the simple equity

method.

On January 1, 20X2, Pep held merchandise acquired from Sky for $10,000. During 20X2, Sky sold

merchandise to Pep for $50,000, $20,000 of which is still held by Pep on December 31, 20X2. Sky’s usual gross

profit on affiliated sales is 50%.

On December 31, 20X1, Pep sold equipment to Sky at a gain of $10,000. During 20X2, the equipment was used

by Sky. Depreciation is being computed using the straight-line method, a five-year life, and no salvage value.

Required:

a.

Using the information above or on the Figure 4-6 worksheet, prepare a determination and distribution of excess schedule.

b.

Complete the Figure 4-6 worksheet for consolidated financial statements for the year ended December 31, 20X2.

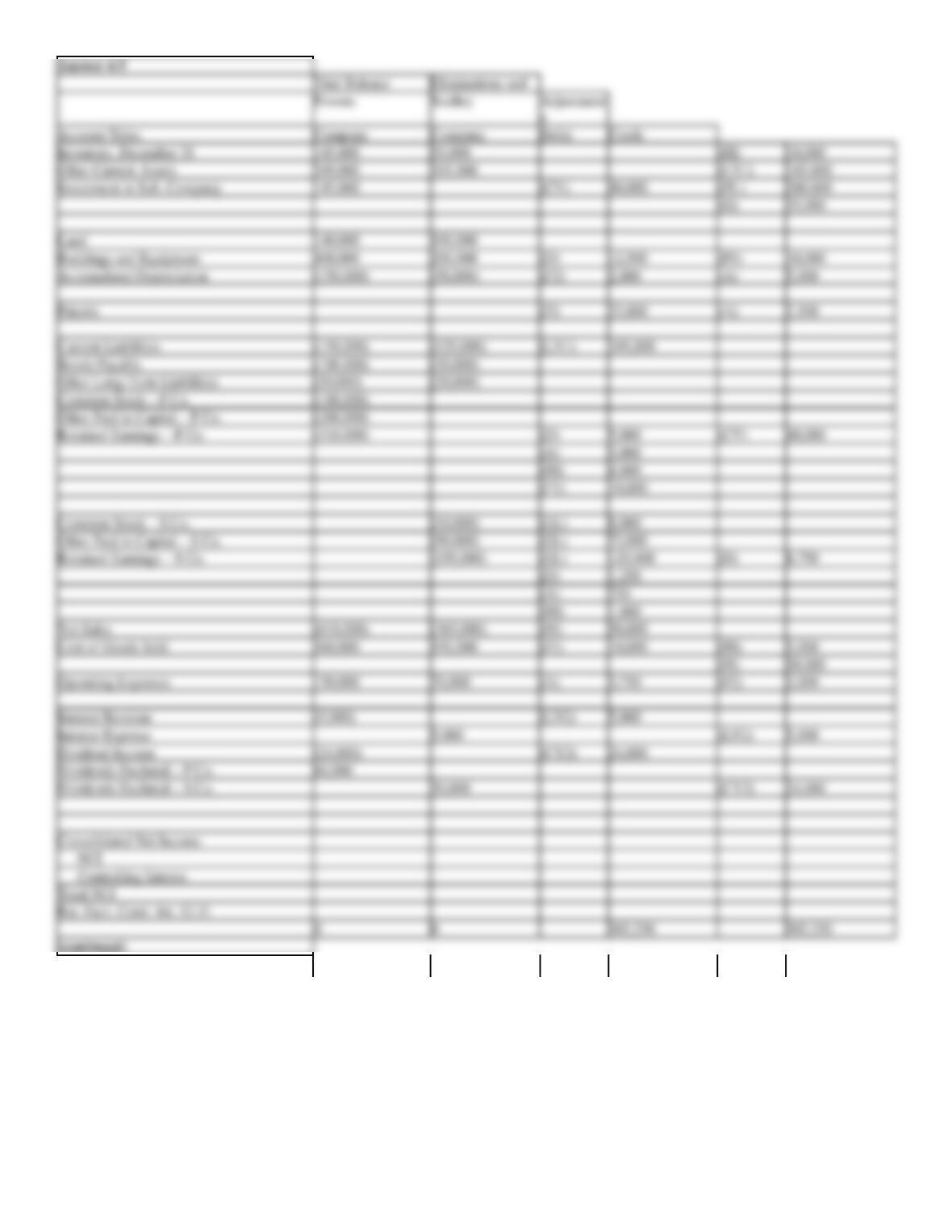

Figure 4-6

Trial Balance

Eliminations and

Pep

Sky

Adjustment

s

Statement – Accounts

Company

Company

Debit

Debit

Credit

Income Statement:

Net Sales

(610,000)

(365,000)

Cost of Goods Sold

360,000

190,000

Operating Expenses

150,000

70,000

Subsidiary Income

(84,000)

Net Income

(184,000)

(105,000)

NCI Interest

NCI

NCI

NCI

Controlling interest

Retained Earnings Statement:

Balance, January 1 – P Co.

(350,000)

Balance, January 1 – S Co.

(150,000)

Net Income (From Above)

(184,000)

(105,000)

Dividends Declared – P Co.

60,000

Dividends Declared – S Co.

30,000

Balance, December 31

(474,000)

(225,000)

Consolidated Balance Sheet:

Inventory, December 31

140,000

60,000

Other Current Assets

249,000

205,000

Investment in Sub. Company

295,000

Land

140,000

100,000

Building and Equipment

400,000

200,000

Accumulated Depreciation

(150,000)

(50,000)

Current Liabilities

(150,000)

(120,000)

Bonds Payable

(100,000)

(50,000)

Other Long-Term Liabilities

(50,000)

(20,000)

Common Stock – P Co.

(100,000)

Other Paid in Capital – P Co.

(200,000)

Common Stock – S Co.

(10,000)

Other Paid in Capital – S Co.

(90,000)

Retained Earnings – 12/31

(474,000)

(225,000)

(From Above)

Total NCI

0

0

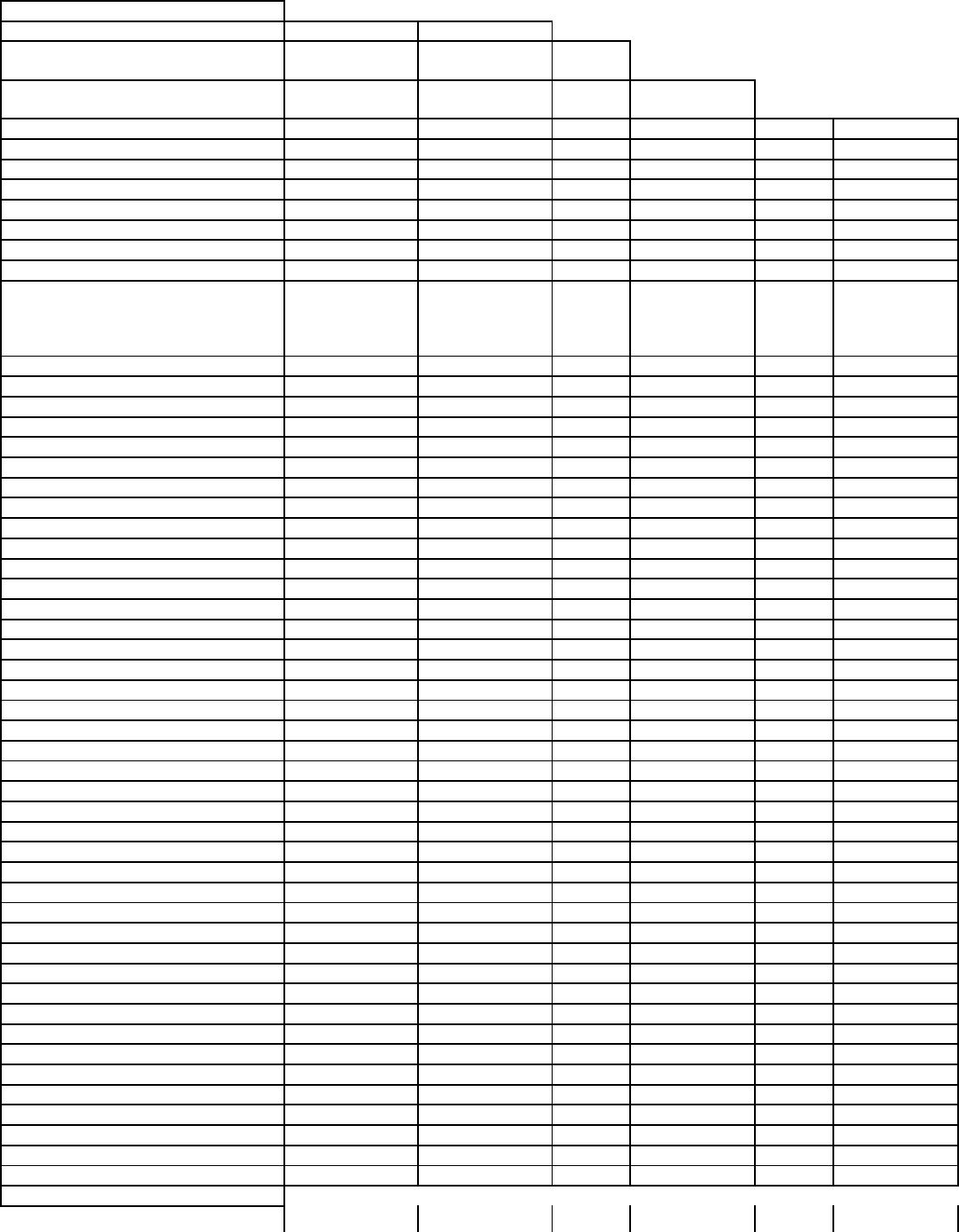

(continued)

Consol.

Financial

Statement – Accounts

NCI

Statements

Income Statement:

Net Sales

Cost of Goods Sold

Operating Expenses

Subsidiary Income

NCI in Income

Net Income

Retained Earnings Statement:

Balance, January 1 – P Co.

Balance, January 1 – S Co.

Net Income (From Above)

Dividends Declared – P Co.

Dividends Declared – S Co.

Balance, December 31

Consolidated Balance Sheet:

Inventory, December 31

Other Current Assets

Investment in Sub. Company

Land

Building and Equipment

Accumulated Depreciation

Current Liabilities

Bonds Payable

Other Long-Term Liabilities

Common Stock – P Co.

Other Paid in Capital – P Co.

Common Stock – S Co.

Other Paid in Capital – S Co.

Retained Earnings – 12/31

(From Above)

Total NCI

41. For each of the following intercompany transactions, state the principle to be used in accounting for

intercompany gains on current and future consolidated income statements:

a.

Gains on merchandise sales

b.

Gains on the sale of land

c.

Gains on the sale of depreciable fixed assets

d.

Interest on intercompany notes

the time of a sale of the asset to an outside party is recognized at the time of the sale.