42. On January 1, 20X4, Parent Company purchased 90% of the common stock of Subsidiary Company for

$360,000. On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $20,000,

$130,000, and $200,000, respectively. Any excess of cost over book value is due to goodwill. Parent accounts

for the Investment in Subsidiary using the simple equity method.

On January 1, 20X4, Subsidiary sold $100,000 par value of 6%, ten-year bonds for $97,000. The bonds pay

interest semi-annually on January 1 and July 1 of each year.

On January 1, 20X5, Parent repurchased all of Subsidiary’s bonds for $96,400. The bonds are still held on

December 31, 20X5.

Both companies have correctly recorded all entries relative to bonds and interest, using straight-line

amortization for premium or discount.

Required:

Prepare the eliminating entries pertaining to the intercompany purchase of bonds for the year ended December

31, 20X5.

Eliminations and Adjustments:

43. On January 1, 20X4, Parent Company purchased 90% of the common stock of Subsidiary Company for

$360,000. On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $20,000,

$130,000, and $200,000 respectively. Any excess of cost over book value is due to goodwill. Parent account for

the Investment in Subsidiary using the simple equity method.

On July 1, 20X4, Subsidiary sold $100,000 par value of 9%, ten-year bonds for $106,755, which resulted in an

effective interest rate of 8%. The bonds pay interest semi-annually on January 1 and July 1 of each year.

Subsidiary uses the effective-interest method of amortizing the premium.

An amortization table for 20X4 and 20X5 is presented below:

Date

Cash Int

Interest Exp

Premium Amort

Premium Bal

Carrying Value

7/1/X4

6,755

106,755

12/31/X4

4,500

4,270

230

6,525

106,525

7/1/X5

4,500

4,261

239

6,286

106,286

12/31/X5

4,500

4,251

249

6,037

106,037

On July 1, 20X5, Parent repurchased all of Par’s bonds for $94,153, which resulted in an effective interest rate of 10%. The bonds are still held at

year end.

Both companies have correctly recorded all entries relative to bonds and interest. The balance in the Investment in Subsidiary Bonds account is

$94,361 at December 31, 20X5, and the parent recognized interest income of $4,708 during the period.

Required:

Prepare the eliminating entries pertaining to the intercompany purchase of bonds for the year ending December 31, 20X5.

Eliminations and Adjustments:

Interest payable

(1) 4,500

Interest receivable

4,500

Interest income – Parent

4,708

Interest expense – Subsidiary

4,251

Bonds payable – Subsidiary

100,000

Premium on bond payable

6,037

Investment in Subsidiary bonds

94,361

Gain on retirement of bonds

To recognize the gain on the retirement of the bonds

44. On January 1, 20X1, Parent Company purchased 80% of the common stock of Subsidiary Company for

$402,000. On this date Subsidiary had total owners’ equity of $440,000. Any excess of cost over book value is

due to goodwill. Parent accounts for its investment in Subsidiary using the simple equity method.

On January 1, 20X3, Parent held merchandise acquired from Subsidiary for $50,000. During 20X3, Subsidiary

sold merchandise to Parent for $120,000, of which Parent holds $30,000 on December 31, 20X3. Subsidiary’s

gross profit on sales is 40%. On December 31, 20X3, Parent still owes Subsidiary $5,000 for merchandise.

On December 31, 20X1, Parent sold $100,000 par value of 11%, 10-year bonds for $106,232, which resulted in

an effective interest rate of 10%. The bonds pay interest semi-annually on June 30 and December 31. Parent

uses the effective-interest method of amortization for the premium.

An amortization table for 20X2 and 20X3 is presented below:

Cash

Interest

Interest Expense

Premium

Amortization

Premium Balance

Debt Carrying Value

12/31/X1

6,232

106,232

6/30/X2

5,500

5,312

(188)

6,044

106,044

12/31/X2

5,500

5,302

(198)

5,846

105,846

6/30/X3

5,500

5,292

(208)

5,638

105,638

12/31/X3

5,500

5,282

(218)

5,420

105,420

On December 31, 20X2, Subsidiary repurchased $50,000 par value of the bonds, paying a price equal to par. The bonds are still held on December

31, 20X3.

On December 31, 20X3, Parent sold equipment with a cost of $50,000 and accumulated depreciation of $30,000 to Subsidiary for $40,000.

Subsidiary will use the equipment beginning in 20X4.

Required:

Complete the Figure 5-7 worksheet for consolidated financial statements for the year ended December 31, 20X3. Round all computations to the

nearest dollar.

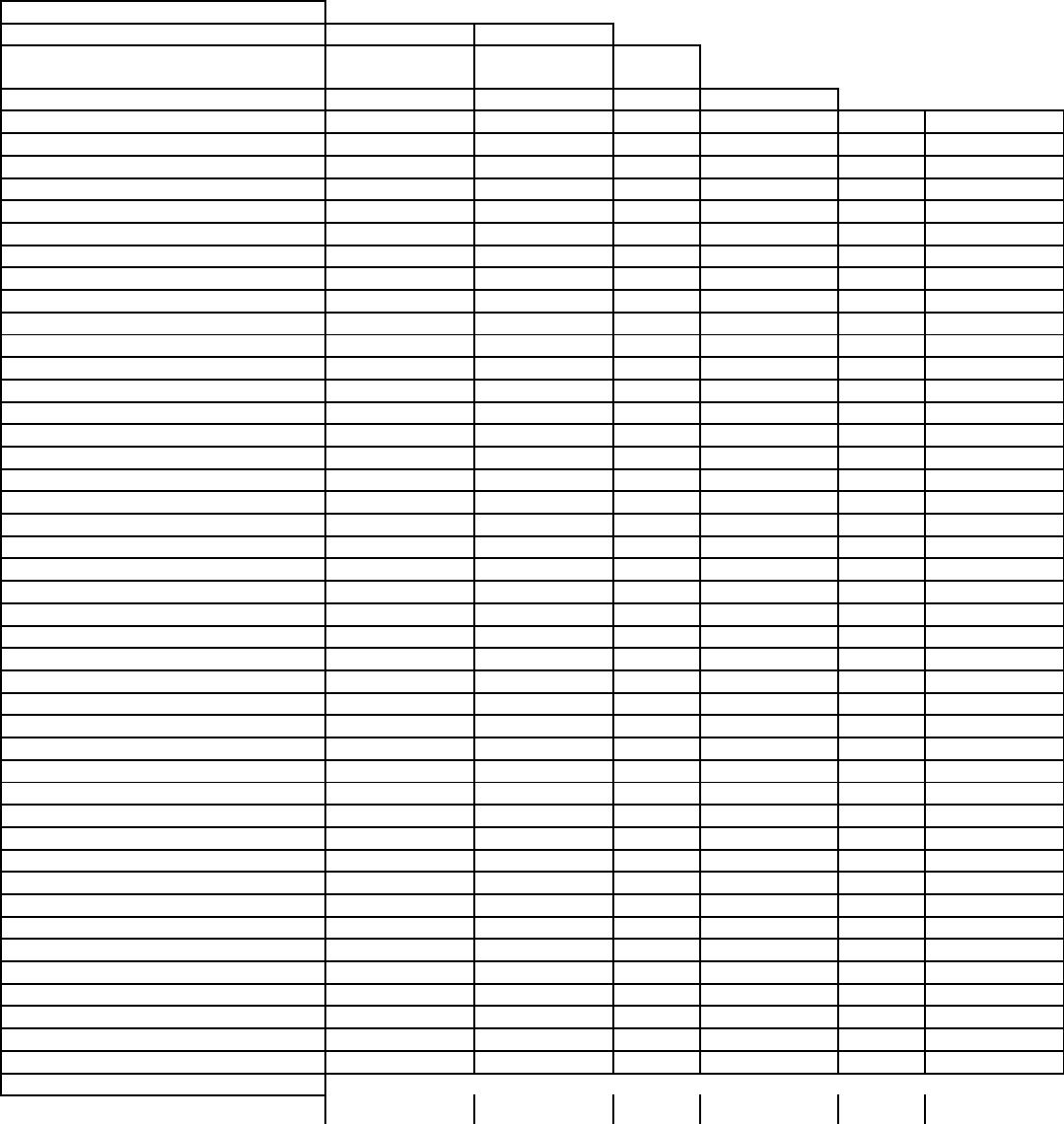

Figure 5-7

Trial Balance

Eliminations and

Parent

Sub.

Adjustment

s

Account Titles

Company

Company

Debit

Credit

Inventory, December 31

120,000

60,000

Other Current Assets

399,620

325,000

Investment in Sub. Company

550,000

Investment in Parent Bonds

50,000

Land

140,000

100,000

Buildings and Equipment

325,000

440,000

Accumulated Depreciation

(120,000)

(130,000)

Goodwill

Current Liabilities

(160,000)

(80,000)

Bonds Payable, 10%

(100,000)

Premium on Bonds Payable

(5,420)

Other Long-Term Liabilities

(200,000)

(140,000)

Common Stock – P Co.

(200,000)

Other Paid-in Capital – P Co.

(100,000)

Retained Earnings – P Co.

(489,200)

Common Stock – S Co.

(100,000)

Other Paid-in Capital – S Co.

(200,000)

Retained Earnings – S Co.

(250,000)

Net Sales

(590,000)

(520,000)

Cost of Goods Sold

355,000

310,000

Operating Expenses

114,426

115,500

Interest Income

(5,500)

Interest Expense

10,574

Subsidiary Income

(80,000)

Gain on Sale of Equipment

(20,000)

Dividends Declared – P Co.

50,000

Dividends Declared – S Co.

25,000

Consolidated Net Income

To NCI

To Controlling Interest

Total NCI

Ret. Earn. Contr. Int. 12-31

0

0

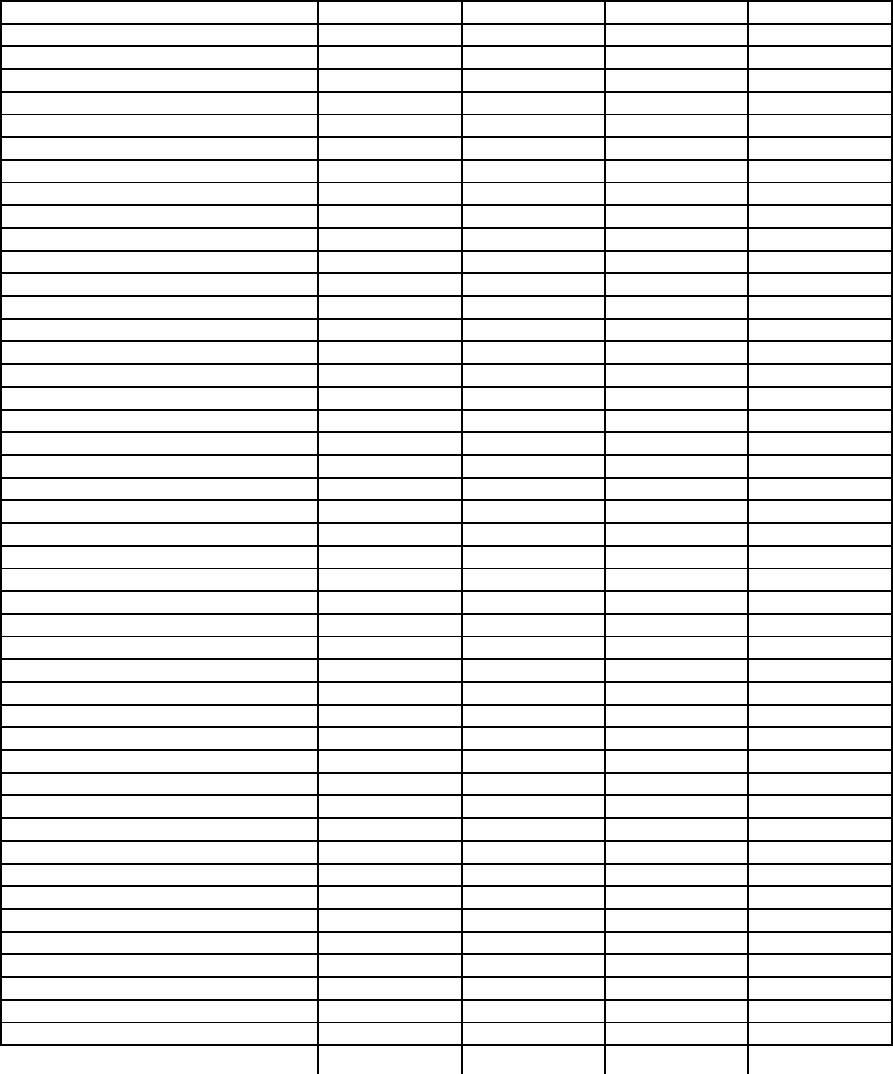

(continued)

Consol.

Control.

Consol.

Income

Retained

Balance

Account Titles

Statement

NCI

Earnings

Sheet

Inventory, December 31

Other Current Assets

Investment in Sub. Company

Investment in Parent Bonds

Land

Buildings and Equipment

Accumulated Depreciation

Goodwill

Current Liabilities

Bonds Payable, 10%

Premium on Bonds Payable

Other Long-Term Liabilities

Common Stock – P Co.

Other Paid-in Capital – P Co.

Retained Earnings – P Co.

Common Stock – S Co.

Other Paid-in Capital – S Co.

Retained Earnings – S Co.

Net Sales

Cost of Goods Sold

Operating Expenses

Interest Income

Interest Expense

Subsidiary Income

Gain on Sale of Equipment

Dividends Declared – P Co.

Dividends Declared – S Co.

Consolidated Net Income

To NCI

To Controlling Interest

Total NCI

Ret. Earn. Contr. Int. 12-31

For the worksheet solution, please refer to Answer 5-7.

45. Smart Corporation is a 90%-owned subsidiary of Phan Inc. On January 2, 20X1, Smart agreed to lease

$400,000 of construction equipment from Phan for $3,000 a month on an operating lease. The equipment has a

10-year life and is being depreciated using the straight-line method.

Required:

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-8 partial

worksheet for December 31, 20X3. Key and explain all eliminations and adjustments.

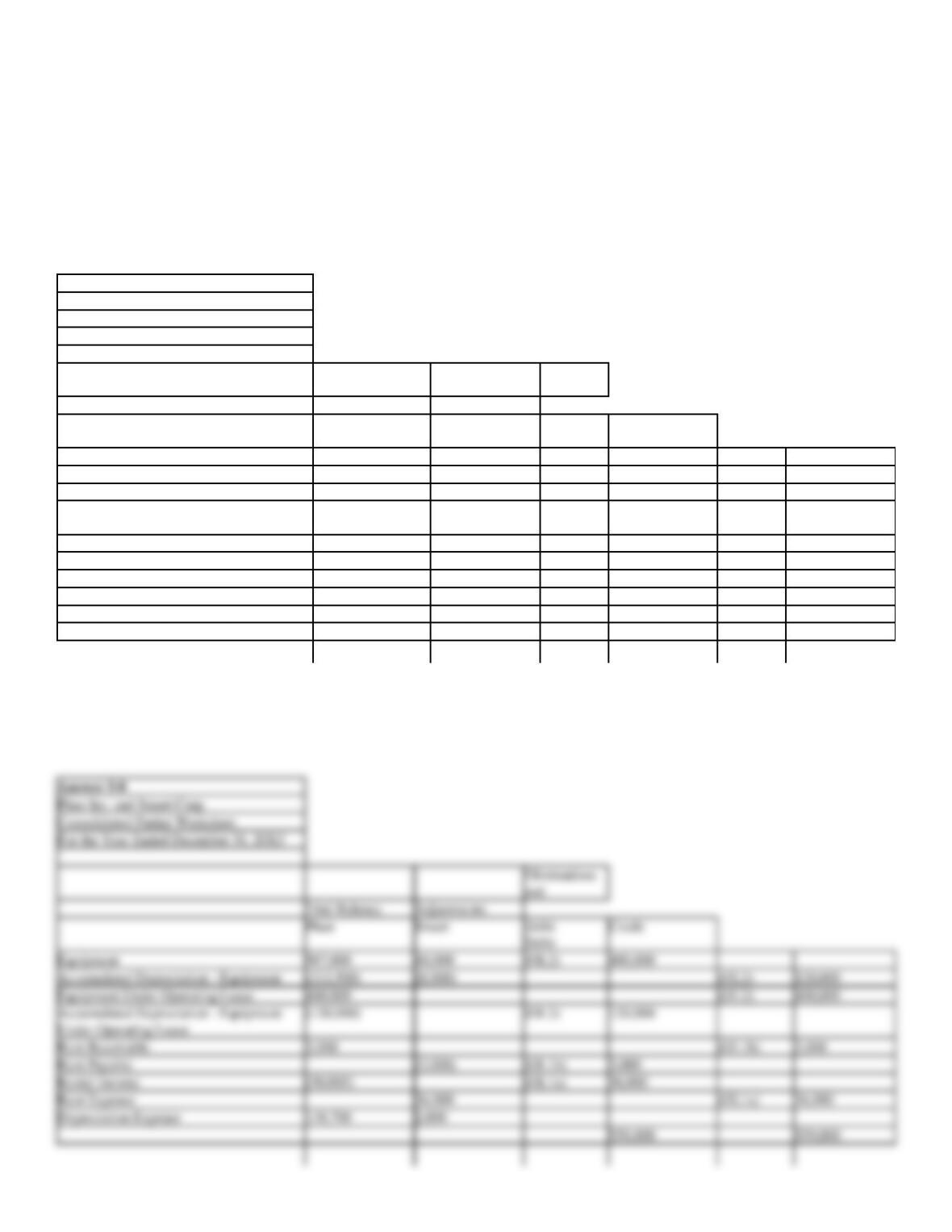

Figure 5-8

Phan Inc. and Smart Corp.

Consolidated Partial Worksheet

For the Year Ended December 31, 20X3

Elimination

s and

Trial Balance

Adjustments

Phan

Smart

Debit

Debit

Credit

Equipment

987,000

40,000

Accumulated Depreciation – Equipment

(212,500)

(8,000)

Equipment Under Operating Lease

400,000

Accumulated Depreciation – Equipment

Under Operating Lease

(120,000)

Rent Receivable

3,000

Rent Payable

(3,000)

Rental Income

(50,000)

Rent Expense

36,000

Depreciation Expense

138,700

2,000

For the worksheet solution, please refer to Answer 5-8.

Phan Inc. and Smart Corp.

Consolidated Partial Worksheet

For the Year Ended December 31, 20X3

Eliminations

and

Trial Balance

Adjustments

Phan

Smart

Debit

Debit

Credit

Equipment

987,000

40,000

(OL2)

400,000

Accumulated Depreciation – Equipment

(212,500)

(8,000)

(OL2)

120,000

Equipment Under Operating Lease

400,000

(OL2)

400,000

Accumulated Depreciation – Equipment

Under Operating Lease

(120,000)

(OL2)

120,000

Rent Receivable

3,000

(OL1b)

3,000

Rent Payable

(3,000)

(OL1b)

3,000

Rental Income

(50,000)

(OL1a)

36,000

Depreciation Expense

138,700

2,000

559,000

559,000

46. Tempo Industries is an 80%-owned subsidiary of Dalie Inc. On January 1, 20X2, Dalie leased an asset to

Tempo and the following journal entries were made:

Tempo

Assets Under Capital Lease

21,561

Cash

5,000

Obligations Under Capital Lease

16,561

Dalie

Minimum Lease Payments Receivable

20,000

Cash

5,000

Unearned Interest Income

3,439

Asset (cost of asset leased)

18,000

Sales Profit on Leases

3,561

The terms of the lease agreement require Tempo to make five payments of $5,000 each at the beginning of each year. The implicit interest rate used

by both Dalie and Tempo is 8%.

Required:

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-9 partial worksheet of December 31, 20X2. Key and

explain all eliminations and adjustments.

Figure 5-9

Dalie and Tempo Industries

Consolidated Partial Worksheet

For the Year Ended December 31, 20X2

Elimination

s and

Trial Balance

Adjustments

Account Titles

Dalie

Tempo

Debit

Credit

Minimum Lease Payments Receivable

20,000

Unearned Interest Income

(2,114)

Assets Under Capital Lease

21,561

Accumulated Depreciation – Assets Under

Capital Lease

(4,312)

Plant Assets

410,000

260,000

Accumulated Depreciation – Plant Assets

(167,000)

(98,000)

Obligations Under Capital lease

(16,561)

Interest Payable

(1,325)

Interest Income

(1,325)

Sales Profit on Leases

(3,561)

Interest Expense

1,325

Depreciation Expense

17,500

10,470

For the worksheet solution, please refer to Answer 5-9.