Archives: Solution Manual

978-1118096895 Chapter 7 Part 2

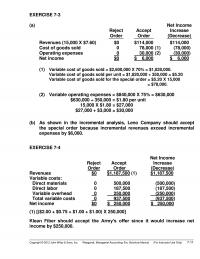

EXERCISE 7-3 (a) Reject Order Accept Order Net Income Increase (Decrease) Revenues (15,000 X $7.60) Cost of goods sold Operating expenses Net income $0 0 0 $0 $114,000 78,000 30,000 $ 6,000 (1) (2) ($114,000) ( (78,000) ( (30,000) ($ […]

978-1118096895 Chapter 7 Part 1

CHAPTER 7 Incremental Analysis ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Identify the steps in management’s decision- making process. 1, 2 1 1 2. Describe the concept of incremental analysis. 3, […]

978-1118096895 Chapter 6 Part 8

BYP 6-3 (Continued) (e) In order to solve for the sales level where net income would be equal under either approach, set the two CVP equations equal to each other and solve for sales: Sales – ((1 – .75) X […]

978-1118096895 Chapter 6 Part 7

Copyright © 2012 John Wiley & Sons, Inc. Weygandt, Managerial Accounting, 6/e, Solutions Manual (For Instructor Use Only) 6-61 *PROBLEM 6-7B (Continued) FAB COMPANY Income Statement For the Year Ended December 31, 2014 Variable Costing Sales (500,000 yards X $2.50) […]

978-1118096895 Chapter 6 Part 6

PROBLEM 6-2B (Continued) (2) Contribution margin ratio = $314,000 ÷ $1,000,000 = .314 (3) Break-even point in dollars = $431,000 ÷ .314 = $1,372,611 (rounded) The break-even point in dollars declined from $1,690,000 to $1,372,611. This means that overall the […]

978-1118096895 Chapter 6 Part 5

PROBLEM 6-6A (Continued) The calculations indicate that at a sales level of $75 million, a percentage change in sales and contribution margin will result in 2.70 times that percentage change in operating income if Bonita continues to use sales agents. […]

978-1118096895 Chapter 6 Part 4

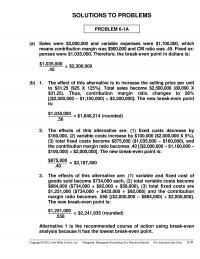

SOLUTIONS TO PROBLEMS PROBLEM 6-1A (a) Sales were $2,000,000 and variable expenses were $1,100,000, which means contribution margin was $900,000 and CM ratio was .45. Fixed ex- penses were $1,035,000. Therefore, the break-even point in dollars is: $1,035,000 = $2,300,000 […]

978-1118096895 Chapter 6 Part 3

Copyright © 2012 John Wiley & Sons, Inc. Weygandt, Managerial Accounting, 6/e, Solutions Manual (For Instructor Use Only) 6-21 EXERCISE 6-8 (Continued) Sales Mix Percentage Total Break- even Sales in Dollars Sales Dollars Needed Per Product Mail pouches and small […]

978-1118096895 Chapter 6 Part 2

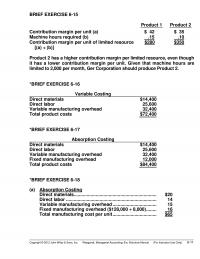

BRIEF EXERCISE 6-15 Product 1 Product 2 Contribution margin per unit (a) Machine hours required (b) Contribution margin per unit of limited resource [(a) ÷ (b)] $ 42 .15 $280 $ 35 .10 $350 Product 2 has a higher contribution […]

978-1118096895 Chapter 6 Part 1

CHAPTER 6 Cost-Volume-Profit Analysis: Additional Issues ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Describe the essential features of a cost-volume-profit income statement. 1, 2, 3, 4 1, 2, 3, 4, 5, […]

978-1118096895 Chapter 5 Part 5

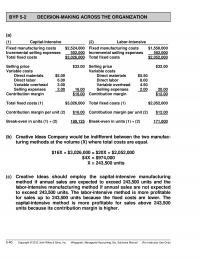

BYP 5-2 DECISION-MAKING ACROSS THE ORGANIZATION (a) (1) Capital-Intensive (2) Labor-Intensive Fixed manufacturing costs $2,524,000 Incremental selling expenses 502,000 Total fixed costs $3,026,000 Fixed manufacturing costs $1,550,000 Incremental selling expenses 502,000 Total fixed costs $2,052,000 Selling price $32.00 Variable costs […]

978-1118096895 Chapter 5 Part 4

PROBLEM 5-1B (a) Variable costs (per haircut) Fixed costs (per month) Barbers’ commission $3.00 Rent .60 Barber supplies .40 Total variable $4.00 Barbers’ salaries $7,500* Rent 700 Depreciation 400 Utilities 300 Advertising 100 Total fixed $9,000 *($1,500 X 3) + […]

978-1118096895 Chapter 5 Part 3

EXERCISE 5-14 (a) Units sold in 2013 = $570,000 +$210,000 $150 –$90 = 13,000 units (b) Units needed in 2014 = $570,000 + $262,000 * $150 –$90 = 13,867 units (rounded) *$210,000 + $52,000 = $262,000 (c) $570,000 +$262,000 X […]

978-1118096895 Chapter 5 Part 2

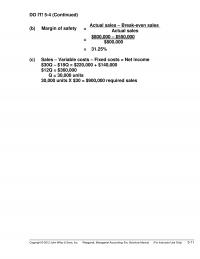

DO IT! 5-4 (Continued) (b) Margin of safety = Actual sales – Break-even sales Actual sales = $800,000 – $550,000 $800,000 = 31.25% (c) Sales – Variable costs – Fixed costs = Net income $30Q – $18Q = $220,000 + […]

978-1118096895 Chapter 5 Part 1

CHAPTER 5 Cost-Volume-Profit ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Distinguish between variable and fixed costs. 1, 2, 3, 6 1 1 1, 2, 3, 4, 5, 6 1A, 6A 1B, […]

978-1118096895 Chapter 4 Part 6

BYP 4-3 (Continued) (d) Activity-based costing permits the company to identify its R&D costs by the activities that cause the costs; that is, ABC allows closer scrutiny of the causes for cost incurrences; hence, greater control. By charging in-house manufacturing […]

978-1118096895 Chapter 4 Part 5

Copyright © 2012 John Wiley & Sons, Inc. Weygandt, Managerial Accounting, 6/e, Solutions Manual (For Instructor Use Only) 4-41 PROBLEM 4-4B (a) Computation of unit costs—traditional costing Overhead cost per labor hour is $1,150,000 ÷ (30,000 + 20,000) =$23 Products […]

978-1118096895 Chapter 4 Part 4

PROBLEM 4-3A (Continued) Total manufacturing cost per stairway under ABC: Direct materials ……………………………………………………………. $ 103,600 Direct labor ………………………………………………………………….. 112,000 Overhead …………………………………………………………………….. 67,950 Total cost of 250 stairs ………………………………………….. $ 283,550 Total cost per stairway ($283,550 ÷ 250) ………………………… $1,134.20 (d) […]

978-1118096895 Chapter 4 Part 3

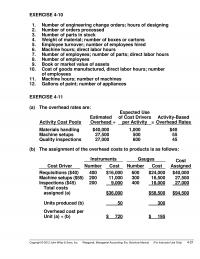

Copyright © 2012 John Wiley & Sons, Inc. Weygandt, Managerial Accounting, 6/e, Solutions Manual (For Instructor Use Only) 4-21 EXERCISE 4-10 1. Number of engineering change orders; hours of designing 2. Number of orders processed 3. Number of parts in […]

978-1118096895 Chapter 4 Part 2

DO IT! 4-2 (Continued) (d) These computations show that the total overhead assigned to Product AD908 is more than two and a half times that assigned to BC113. On a per unit basis, the overhead assigned to AD908 is close […]

978-1118096895 Chapter 4 Part 1

CHAPTER 4 Activity-Based Costing ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems *1. Recognize the difference between traditional costing and activity-based costing. 1, 2, 3, 4, 5 1, 2 1 1, 2, 3, […]

978-1118096895 Chapter 3 Part 7

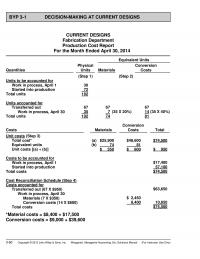

3-60 Copyright © 2012 John Wiley & Sons, Inc. Weygandt, Managerial Accounting, 6/e, Solutions Manual (For Instructor Use Only) BYP 3-1 DECISION-MAKING AT CURRENT DESIGNS CURRENT DESIGNS Fabrication Department Production Cost Report For the Month Ended April 30, 2014 Equivalent […]

978-1118096895 Chapter 3 Part 6

Copyright © 2012 John Wiley & Sons, Inc. Weygandt, Managerial Accounting, 6/e, Solutions Manual (For Instructor Use Only) 3-51 PROBLEM 3-4B (a) Equivalent Units Physical Units Materials Conversion Costs Units to be accounted for Work in process, October 1 Started […]

978-1118096895 Chapter 3 Part 5

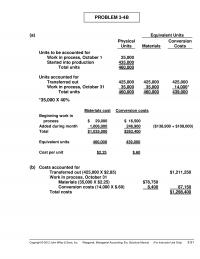

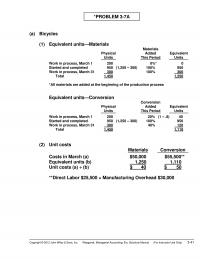

*PROBLEM 3-7A (a) Bicycles (1) Equivalent units—Materials Physical Units Materials Added This Period Equivalent Units Work in process, March 1 Started and completed Work in process, March 31 Total 200 950 300 1,450 (1,250 – 300) * 0%* 100% 100% […]

978-1118096895 Chapter 3 Part 4

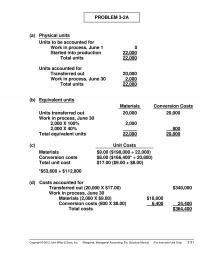

Copyright © 2012 John Wiley & Sons, Inc. Weygandt, Managerial Accounting, 6/e, Solutions Manual (For Instructor Use Only) 3-31 PROBLEM 3-2A (a) Physical units Units to be accounted for Work in process, June 1 Started into production Total units Units […]

978-1118096895 Chapter 3 Part 3

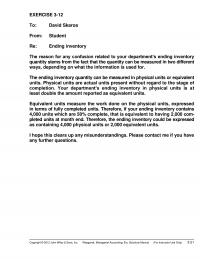

EXERCISE 3-12 To: David Skaros From: Student Re: Ending inventory The reason for any confusion related to your department’s ending inventory quantity stems from the fact that the quantity can be measured in two different ways, depending on what the […]

978-1118096895 Chapter 3 Part 2

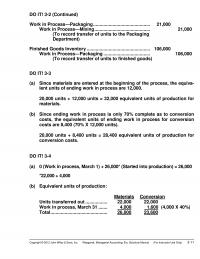

DO IT! 3-2 (Continued) Work in Process—Packaging …………………………………….. 21,000 Work in Process—Mixing ……………………………………. 21,000 (To record transfer of units to the Packaging Department) Finished Goods Inventory …………………………………………. 106,000 Work in Process—Packaging ……………………………… 106,000 (To record transfer of units to finished […]

978-1118096895 Chapter 3 Part 1

CHAPTER 3 Process Costing ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems * 1. Understand who uses process cost systems. 1, 2, 20 1 1 * 2. Explain the similarities and differences between […]

978-1118096895 Chapter 2 Part 5

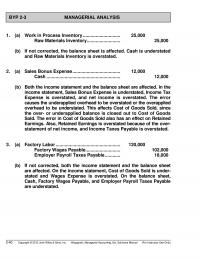

BYP 2-3 MANAGERIAL ANALYSIS 1. (a) Work in Process Inventory ……………………….. 25,000 Raw Materials Inventory…………………….. 25,000 (b) If not corrected, the balance sheet is affected. Cash is understated and Raw Materials Inventory is overstated. 2. (a) Sales Bonus Expense ………………………………. […]

978-1118096895 Chapter 2 Part 4

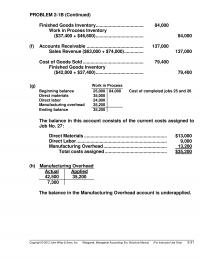

PROBLEM 2-1B (Continued) Finished Goods Inventory ………………………………. 84,000 Work in Process Inventory ($37,400 + $46,600) ………………………………. 84,000 (f) Accounts Receivable …………………………………….. 137,000 Sales Revenue ($63,000 + $74,000) …………… 137,000 Cost of Goods Sold ……………………………………….. 79,400 Finished Goods Inventory ($42,000 + […]

978-1118096895 Chapter 2 Part 3

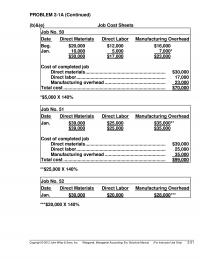

PROBLEM 2-1A (Continued) (b)&(e) Job Cost Sheets Job No. 50 Date Direct Materials Direct Labor Manufacturing Overhead Beg. Jan. $20,000 10,000 $30,000 $12,000 5,000 $17,000 *$16,000* * 7,000* *$23,000* Cost of completed job Direct materials …………………………………………………….. $30,000 Direct labor …………………………………………………………… […]

978-1118096895 Chapter 2 Part 2

SOLUTIONS TO EXERCISES EXERCISE 2-1 (a) Factory Labor …………………………………………………. 80,000 Factory Wages Payable ……………………………. 66,000 Employer Payroll Taxes Payable ………………. 8,000 Employer Fringe Benefits Payable ……………. 6,000 (b) Work in Process Inventory ($80,000 X 85%) ……… 68,000 Manufacturing Overhead …………………………………. […]

978-1118096895 Chapter 2 Part 1

CHAPTER 2 Job Order Costing ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Explain the characteristics and purposes of cost accounting. 1, 2, 3, 4 2. Describe the flow of costs in […]

978-1118096895 Chapter 14 Part 5

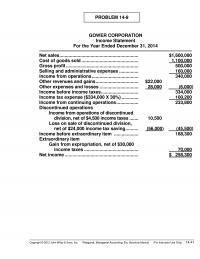

PROBLEM 14-9 GOWER CORPORATION Income Statement For the Year Ended December 31, 2014 Net sales ……………………………………………………. $1,600,000 Cost of goods sold …………………………………….. 1,100,000 Gross profit ……………………………………………….. 500,000 Selling and administrative expenses …………… 160,000 Income from operations ……………………………… 340,000 Other revenues […]

978-1118096895 Chapter 14 Part 4

PROBLEM 14-3 (a) 2013 2014 (1) Profit margin. $32,000 $640,000 = 5.0% $42,000 $700,000 = 6.0% (2) Asset turnover. $640,000 $533,000 + $600,000 2 = 1.1 times $700,000 $600,000 + $640,000 2 […]

978-1118096895 Chapter 14 Part 3

Copyright © 2012 John Wiley & Sons, Inc. Weygandt, Managerial Accounting, 6/e, Solutions Manual (For Instructor Use Only) 14–21 EXERCISE 14-4 (a) HENDI CORPORATION Condensed Income Statements For the Years Ended December 31 Increase or (Decrease) During 2013 2014 2013 […]

978-1118096895 Chapter 14 Part 2

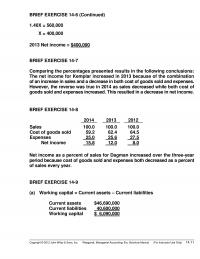

BRIEF EXERCISE 14-6 (Continued) 1.40X = 560,000 X = 400,000 2013 Net income = $400,000 BRIEF EXERCISE 14-7 Comparing the percentages presented results in the following conclusions: The net income for Kemplar increased in 2013 because of the combination of […]

978-1118096895 Chapter 14 Part 1

CHAPTER 14 Financial Statement Analysis ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises Problems 1. Discuss the need for comparative analysis. 1, 2, 3, 5 1 2. Identify the tools of financial statement analysis. 2, 3, 5, […]

978-1118096895 Chapter 13 Part 6

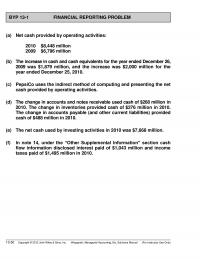

BYP 13-1 FINANCIAL REPORTING PROBLEM (a) Net cash provided by operating activities: 2010 $8,448 million 2009 $6,796 million (b) The increase in cash and cash equivalents for the year ended December 26, 2009 was $1,879 million, and the increase was […]

978-1118096895 Chapter 13 Part 5

PROBLEM 13-5B ANNE DROID INC. Partial Statement of Cash Flows For the Year Ended December 31, 2014 Cash flows from operating activities Net income …………………………………………………. $115,000 Adjustments to reconcile net income to net cash provided by operating activities: Decrease in […]

978-1118096895 Chapter 13 Part 4

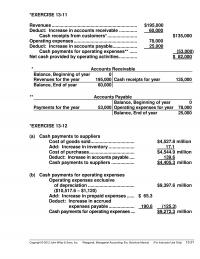

*PROBLEM 13-8A (Continued) (2) Cash payments to suppliers Cost of goods sold ……………………………………….. $175,000 Add: Increase in inventory ……………………………. 10,000 Cost of purchases ………………………………………… 185,000 Deduct: Increase in accounts payable …………… 14,000 Cash payments to suppliers ………………………….. $171,000 (3) Cash […]

978-1118096895 Chapter 13 Part 3

*EXERCISE 13-11 Revenues ………………………………………………………… $195,000) Deduct: Increase in accounts receivable ………….. 60,000 Cash receipts from customers* ………………….. $135,000 Operating expenses …………………………………………. 78,000) Deduct: Increase in accounts payable ………………. 25,000 Cash payments for operating expenses** …… (53,000) Net cash provided by […]

978-1118096895 Chapter 13 Part 2

*BRIEF EXERCISE 13-14 + Decrease in income taxes payable Cash payment for income taxes = Income tax expense – Increase in income taxes payable $112,000,000 = $360,000,000 – $248,000,000* *$525,000,000 – $277,000,000 = $248,000,000 (Increase in income taxes payable) *BRIEF […]

978-1118096895 Chapter 13 Part 1

CHAPTER 13 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems *1. Indicate the usefulness of the statement of cash flows. 1, 2, 6, 15 *2. Distinguish among operating, investing, […]

978-1118096895 Chapter 12 Part 5

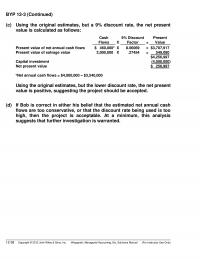

BYP 12-3 (Continued) (c) Using the original estimates, but a 9% discount rate, the net present value is calculated as follows: Cash Flows X 9% Discount Factor = Present Value Present value of net annual cash flows Present value of […]

978-1118096895 Chapter 12 Part 4

PROBLEM 12-3B (Continued) (3) Internal rate of return on Option B is 12%, as calculated below: Cash Flows X 12% Discount Factor = Present Value Present value of net annual cash inflows Present value of cost to rebuild Present value […]

978-1118096895 Chapter 12 Part 3

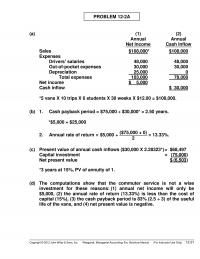

Copyright © 2012 John Wiley & Sons, Inc. Weygandt, Managerial Accounting, 6/e, Solutions Manual (For Instructor Use Only) 12–21 PROBLEM 12-2A (a) (1) Annual Net Income (2) Annual Cash Inflow Sales Expenses Drivers’ salaries Out-of-pocket expenses Depreciation Total expenses Net […]

978-1118096895 Chapter 12 Part 2

DO IT! 12-4 Revenues ………………………………………………………….. $80,000 Less: Expenses (excluding depreciation) ……………….. $40,000 Depreciation ($120,000/4 years) …………………….. 30,000 70,000 Annual net income …………………………………………….. $ 10,000 Average investment = ($120,000 + 0)/2 = $60,000. Annual rate of return = $10,000/$60,000 = 16.7%. […]

978-1118096895 Chapter 12 Part 1

CHAPTER 12 Planning for Capital Investments ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Discuss capital budgeting evaluation, and explain inputs used in capital budgeting. 1 2. Describe the cash payback technique. […]

978-1118096895 Chapter 11 Part 7

BYP 11-4 REAL-WORLD FOCUS (a) Glassmaster is using standard costs because management states that a factor that contributed to improved margins (profit) was a favorable materials price variance. (b) The materials price variance experienced should not lead to changes in […]