Archives

978-0078025815 Chapter 1 Solution Manual

Chapter 01 – Introduction to Accounting and Financial Reporting for Governmental and Not-for-Profit Organizations 1-1 INSTRUCTOR’S MANUAL TO ACCOMPANY ESSENTIAL OF ACCOUNTING FOR GOVERNMENTAL AND NOT–FOR-PROFIT ORGANIZATIONS: TWELFTH EDITION PREPARED BY: MARY LORETTA MANKTELOW MARILLA S. MELCHER JAMES MADISON UNIVERSITY […]

978-0078025815 Chapter 10 Solution Manual Part 1

Chapter 10 – Accounting for Private Not-for-Profit 10-1 CHAPTER 10 ACCOUNTING FOR PRIVATE NOT–FOR-PROFIT 10-1. ANSWERS WILL VARY DEPENDING ON STATEMENTS OBTAINED. 10-2. A. THE FINANCIAL REPORTS REQUIRED BY THE FASB FOR NONPROFIT ORGANIZATIONS ARE (1) STATEMENT OF FINANCIAL POSITION, […]

978-0078025815 Chapter 10 Solution Manual Part 2

Chapter 10 – Accounting for Private Not-for-Profit 10-12. THE GRANT WOOD ARTS ASSOCIATION GENERAL JOURNAL – UNRESTRICTED DEBITS CREDITS 1. CASH CONTRIBUTIONS-UNRESTRICTED CONTRIBUTIONS-TEMPORARILY RESTRICTED CONTRIBUTIONS-PERMANENTLY RESTRICTED 3,900,000 1,950,000 950,000 1,000,000 2. CASH ADMISSIONS CHARGES-UNRESTRICTED INTEREST INCOME-UNRESTRICTED TUITION REVENUE-UNRESTRICTED NOTE PAYABLE […]

978-0078025815 Chapter 11 Solution Manual Part 1

Chapter 11 – College and University Accounting – Private Institutions 11-1 CHAPTER 11 College and University Accounting – Private Institutions 11-1. ANSWERS WILL VARY DEPENDING ON STATEMENTS OBTAINED. 11-2. A. PUBLIC (GOVERNMENT–OWNED) COLLEGES AND UNIVERSITIES. 1. GASB 2. STATEMENT OF […]

978-0078025815 Chapter 11 Solution Manual Part 2

Chapter 11 – College and University Accounting – Private Institutions 11–13 11-8 (B CONTINUED). LEE COLLEGE STATEMENT OF CHANGES IN NET ASSETS YEAR ENDED JUNE 30, 2015 TOTAL UNRESTRICTED REVENUES $ 16,265,000 NET ASSETS RELEASED FROM RESTRICTION 1,800,000 TOTAL UNRESTRICTED […]

978-0078025815 Chapter 12 Solution Manual

Chapter 12 – Accounting for Hospitals and Other Health Care Providers 12-1 CHAPTER 12 Accounting for Hospitals and Other Health Care Providers 12-1. a. CHARITY CARE: CHARITY CARE OCCURS WHEN A HOSPITAL OR OTHER HEALTH CARE ORGANIZATION PROVIDES CARE TO […]

978-0078025815 Chapter 13 Problem Solution

CONTINUOUS PROBLEM – CHAPTER 13 RATIO FORMULA CALCULATIONS CITY OF MONROE 1) FINANCIAL POSITION (GOVERNMENT– WIDE, GOVERNMENTAL ACTIVITIES) Unrestricted Net Position: Total Expenses: Governmental Activities 1,808,110 16,193,360 11.2% 2) FINANCIAL POSITION (GENERAL FUND) Unassigned Fund Balance Total Expenditures + Other […]

978-0078025815 Chapter 13 Solution Manual

Chapter 13 – Auditing, Tax Exempt Organizations, and Evaluating Performance CHAPTER 13 Auditing, Tax Exempt Organizations, and Evaluating Performance 13-1. THE SOLUTION TO THIS AND THE FIRST EXERCISE OF CHAPTERS 1 THROUGH 8 WILL VARY FROM STUDENT TO STUDENT, ASSUMING […]

978-0078025815 Chapter 14 Solution Manual

Chapter 14 – Financial Reporting by the Federal Government 13-1 CHAPTER 14 Financial Reporting by the Federal Government 14-1. BASIC FINANCIAL STATEMENTS OF A FEDERAL AGENCY INCLUDE: o BALANCE SHEET, 14-2. BASIC FINANCIAL STATEMENTS OF THE U.S. GOVERNMENT INCLUDE: o […]

978-0078025815 Chapter 2 Solution Manual

Chapter 02 – Overview of Financial Reporting for State and Local Governments 2-1 CHAPTER 2 Overview of Financial Reporting for State and Local Governments 2-1. THE SOLUTION TO THIS AND THE FIRST EXERCISE OF CHAPTERS 1 AND 3 THROUGH 9 […]

978-0078025815 Chapter 3 Solution Manual

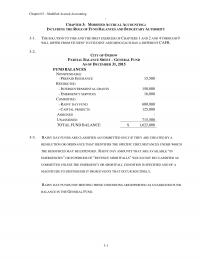

Chapter 03 – Modified Accrual Accounting 3-1 ` CHAPTER 3: MODIFIED ACCRUAL ACCOUNTING: INCLUDING THE ROLE OF FUND BALANCES AND BUDGETARY AUTHORITY 3-1. THE SOLUTION TO THIS AND THE FIRST EXERCISE OF CHAPTERS 1 AND 2 AND 4 THROUGH 9 […]

978-0078025815 Chapter 4 Problem Solution

City of Monroe – General Fund Journal Entries reference Account Titles Debits Credits 3-C Estimated Revenues Control 11,250,000 Appropriations Control 9,300,000 Estimated Other Financing Uses Control 1,700,000 Budgetary Fund Balance 250,000 4-C 1 Encumbrances Control 17,000 Budgetary Fund Balance – […]

978-0078025815 Chapter 4 Solution Manual Part 1

Chapter 04 – Accounting for the General and Special Revenue Funds CHAPTER 4 Accounting for the General and Special Revenue Funds 4-1. THE SOLUTION TO THIS AND THE FIRST EXERCISE OF CHAPTERS 1 THROUGH 9 WILL DIFFER FROM STUDENT TO […]

978-0078025815 Chapter 4 Solution Manual Part 2

Chapter 04 – Accounting for the General and Special Revenue Funds 4-12 4-9 (B) NEWPORT CITY 911 CALL CENTER SPECIAL REVENUE FUND STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCE FOR THE YEAR ENDED DECEMBER 31, 2015 REVENUES: PHONE […]

978-0078025815 Chapter 4 Special Revenue Fund Problem Solution

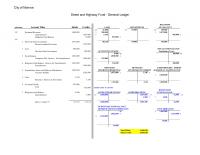

City of Monroe Street and Highway Fund – General Ledger DUE FROM reference Account Titles Debits Credits CASH INVESTMENTS STATE GOV’T bb 21,000 bb 59,000 bb 109,000 3-C Estimated Revenues 1,068,000 2 985,000 11,072,000 Appropriations 1,047,000 55,120 985,000 2 Budgetary […]

978-0078025815 Chapter 5 Other Governmental Funds Problem Solution

City of Monroe – City Jail Construction Fund CITY JAIL CAPITAL PROJECTS FUND CONTRACTS PAYABLE reference Account Titles Debits Credits CASH ACCOUNTS PAYABLE RETAINED PERCENTAGE 14,200,000 200,000 11,282,500 867,500 8 5-C-1 91,320,000 116,000 3 11 1,282,500 12 67,500 1 Cash […]

978-0078025815 Chapter 5 Solution Manual Part 1

Accounting for Other Governmental Funds 5-18 5-1. THE SOLUTION TO THIS AND THE FIRST EXERCISE OF CHAPTERS 1 THROUGH 8 WILL DIFFER FROM STUDENT TO STUDENT, ASSUMING EACH HAS A DIFFERENT CAFR. 5-2. IN DETERMINING THE APPROPRIATE FUND TO RECORD […]

978-0078025815 Chapter 5 Solution Manual Part 2

Accounting for Other Governmental Funds 5-30 5-12 (A). CITY OF SHARPESBURG LIBRARY BOOK PERMANENT FUND GENERAL JOURNAL DEBITS CREDITS 1. CASH REVENUES-ADDITION TO PERMANENT ENDOWMENTS 950,000 950,000 2. INVESTMENTS-BONDS CASH 950,000 950,000 3. CASH REVENUES-INVESTMENT INCOME-INTEREST 21,375 21,375 4. EXPENDITURES-LIBRARY […]

978-0078025815 Chapter 6 Problem Solution

City of Monroe Stores Services Internal Service Fund STORES AND SERVICES INTERNAL SERVICE FUND INVENTORY OF DUE FROM reference Account Titles Debits Credits CASH SUPPLIES OTHER FUNDS LAND bb 31,000 bb 27,500 bb 27,000 bb bb 18,000 6-C-1 1No journal […]

978-0078025815 Chapter 6 Solution Manual Part 1

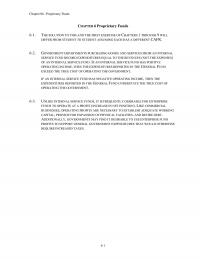

Chapter 06 – Proprietary Funds 6-1 CHAPTER 6 Proprietary Funds 6-1. THE SOLUTION TO THIS AND THE FIRST EXERCISE OF CHAPTERS 1 THROUGH 9 WILL 6-2. GOVERNMENT DEPARTMENTS PURCHASING GOODS AND SERVICES FROM AN INTERNAL SERVICE FUND RECORD EXPENDITURES EQUAL […]

978-0078025815 Chapter 6 Solution Manual Part 2

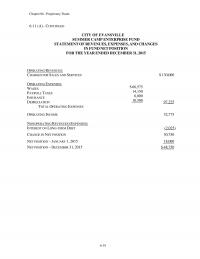

Chapter 06 – Proprietary Funds 6-11 (A) – CONTINUED CITY OF EVANSVILLE SUMMER CAMP ENTERPRISE FUND STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN FUND NET POSITION FOR THE YEAR ENDED DECEMBER 31, 2015 OPERATING REVENUES: CHARGES FOR SALES AND SERVICES […]

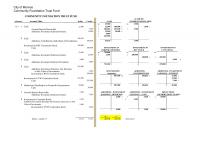

978-0078025815 Chapter 7 Problem Solution

City of Monroe Community Foundation Trust Fund COMMUNITY FOUNDATION TRUST FUND ACCRUED reference Account Titles Debits Credits CASH INTEREST RECEIVABLE bb 49,500 bb 7,500 7-C-1 1Cash 22,500 122,500 200,000 27,500 1 Accrued Interest Receivable 7,500 2206,026 203,500 5 7 7,500 […]

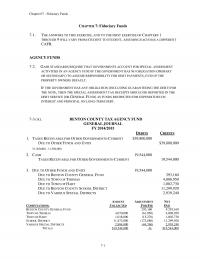

978-0078025815 Chapter 7 Solution Manual Part 1

Chapter 07 – Fiduciary Funds 7-1 7-1. THE ANSWERS TO THIS EXERCISE, AND TO THE FIRST EXERCISE OF CHAPTERS 1 THROUGH 9 WILL VARY FROM STUDENT TO STUDENT, ASSUMING EACH HAS A DIFFERENT CAFR. AGENCY FUNDS 7-2 . GASB STANDARDS […]

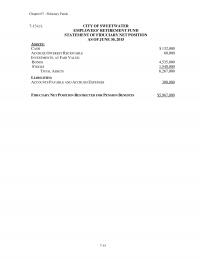

978-0078025815 Chapter 7 Solution Manual Part 2

Chapter 07 – Fiduciary Funds 7-13 (C). CITY OF SWEETWATER EMPLOYEES’ RETIREMENT FUND STATEMENT OF FIDUCIARY NET POSITION AS OF JUNE 30, 2015 ASSETS: CASH ACCRUED INTEREST RECEIVABLE INVESTMENTS, AT FAIR VALUE: BONDS STOCKS TOTAL ASSETS $ 132,000 60,000 4,535,000 […]

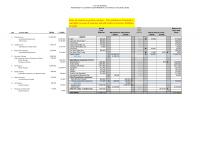

978-0078025815 Chapter 8 Problem Solution

CITY OF MONROE WORKSHEET TO CONVERT GOVERNMENTAL ACTIVITIES TO ACCRUAL BASIS Refr. Account Titles Debits Credits Gov’tal Fund Balances Adjustments & Eliminations Govern- mental Funds Adjusted Internal Service Funds Balances for Gov’t-wide Stmts Debits Credits Debits Credits ACapital Assets 65,900,000 […]

978-0078025815 Chapter 8 Solution Manual

Chapter 8 Government-Wide Statements, Capital Assets, Long-Term Debt 8-1 CHAPTER 8: Government-Wide Statements, Capital Assets, Long-Term Debt 8-1. THE SOLUTION TO THIS AND THE FIRST EXERCISE OF CHAPTERS 1 THROUGH 8 WILL DIFFER FROM STUDENT TO STUDENT ASSUMING EACH HAS […]

978-0078025815 Chapter 9 Solution Manual

Chapter 09 – Accounting for Special-Purpose Entities, Including Public Colleges and Universities 9-1 CHAPTER 9 Accounting for Special-Purpose Entities, Including Public Colleges and Universities 9-1. THE SOLUTION TO THIS PROBLEM WILL DIFFER FROM STUDENT TO STUDENT, ASSUMING EACH HAS A […]

978-0078025815 Exercise 10 Excel

AWG EDUCATIONAL FOUNDATION – a private not-for-profit journal entries and General ledger PLEDGES ACCRUED INTEREST CASH RECEIVABLE RECEIVABLE SUPPLIES Association of Women in Government bb 22,900 bb 27,232 bb 700 bb 400 Educational Foundation 2,200 1 5 1,362 700 3 […]

978-0078025815 Exercise 11 Excel

financial statements Unrestricted Temporarily Restricted Permanently Restricted Total Revenues Student Tuition and Fees 1,508,000$ 1,508,000$ State Appropriations 700,000 700,000 Contributions to Endowment 105,700$ 105,700 Federal Grants 175,000$ 175,000 Investment Income 66,000 66,000 Net assets released from restriction: – Satisfaction of […]

978-0078025815 Exercise 12 Excel

Exercise 12-9 General Ledger Journal Entries debits credits CASH PATIENT ALLOWANCE FOR 1 Patient Accounts Receivable 21,130,000 bb 830,000 ACCOUNTS RECEIVABLE UNCOLLECTABLE ACCOUNTS SUPPLIES CONTRIBUTIONS RECEIVABLE Unrestricted-Patient Service Revenue 21,130,000 1 17,600,000 1,600,000 9 bb 3,250,000 650,000 bb bb 130,000 […]

978-0078025815 Exercise 3 Excel

CITY OF Grafton Schedule of Revenues, Expenditures and Changes in Fund Balance – Budget and Actual: General Fund For The Year Ended December 31, 2015 Budgeted Amounts REVENUES Original Final Actual Amounts Budgetary Basis Variance with Final Budget Property Taxes […]

978-0078025815 Exercise 4 Excel

State Government – Special Revenue Fund CASH LICENSE FEES RECEIVABLE SUPPLIES Fish and Game Fund Journal Entries bb 200,000 bb 125,000 bb 9,000 December 31, 2015 31,150,000 303,000 7125,000 3 6 287,500 4272,000 305,000 9 3 128,000 283,650 12 Item […]

978-0078025815 Exercise 5 Excel

JOURNAL ENTRIES State Government Capital Project Fund Journal Entries December 31, 2015 Account Title Debits Credits 1 Encumbrances 1,700,000 Budgetary Fund Balance – Reserve for encumbrances 1,700,000 2 Cash 25,412,000 Taxes receivable 2,550,000 5 Contracts payable 28,818,000 Cash 28,818,000 Fuel […]

978-0078025815 Exercise 6 Excel

Rural County – journal entries and General ledger Special Revenue fund CAPITAL ASSETS CASH FEES RECEIVABLE SUPPLIES (NET OF ACCL DEPR) Rural County bb 85,000 Special Revenue Fund Journal Entries 385,250 37,300 December 31, 2015 89,900 3 6 2,400 7500 […]

978-0078025815 Exercise 7 Excel

Moose County – journal entries and General ledger Permanent fund INVESTMENTS IN INVESTMENTS IN ACCRUED INTEREST CASH CORPORATE EQUITIES CORPORATE BONDS RECEIVABLE Moose County Permanent Fund Journal Entries 2180,000 12,700,000 13,000,000 112,000 December 31, 2015 3168,000 150,000 5 5 190,000 […]

978-0078025815 Exercise 8 Excel

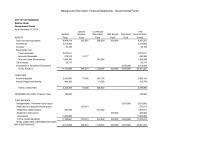

Background Information: Financial Statements – Governmental Funds CITY OF COTTONWOOD Balance Sheet Governmental Funds As of December 31, 2015 General Special Revenue Courthouse Renovation Debt Service Permanent Total Governmental ASSETS Fund Fund Fund Fund Fund Funds Cash and cash equivalents […]

978-0078025815 Exercise 9 Excel

Exercise 9–9 Cherokee Library District Type journal entries to convert to the accrual basis in the space below and post them to the financial statements on the next two tabs. debits credits a Capital Assets 19,500,000 Accumulated Depreciation 6,330,000 Net […]

978-0078025815 Financial Statement Practice Set Province of Europa

1 GOVERNMENTAL ACCOUNTING PRACTICE SET Part A due: Part B due: Introduction The date is December 31, 2091. You have just risen from a three month cryogenic sleep during harvests per Earth year. All banking is performed on Earth through […]

978-0078025815 Financial Statement Template Enterprise Fund

ENTERPRISE FUND – GENERAL LEDGER Journal Entries debits credits DUE FROM 3 Feb. 1 Cash 300,000 CASH OTHER FUNDS SUPPLIES ACCOUNTS RECEIVABLE Transfer in – capital contribution 300,000 bb – bb – bb – bb – To record contribution from […]

978-0078025815 Financial Statement Template Governmental Type Funds

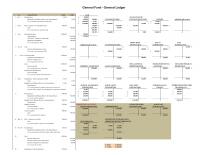

General Fund – General Ledger # date Journal Entries debits credits CASH 1 Jan. 1 Encumbrances 11,806 bb 18,000 ALLOWANCE FOR Budgetary Fund Balance Reserve for Encumbrances 11,806 TAXES RECEIVABLE UNCOLLECTIBLE TAXES SUPPLIES additional debit account To re-establish outstanding encumbrances […]

978-0078025815 Financial Statement Template Govt Wide

Worksheet to convert Governmental fund basis information to accrual basis #Journal Entries debits credits (enter as negatives) Gov’tal Fund Balances Adjustments & Eliminations Balances for Gov’t-wide Stmts type accounts to be debited here Debits Credits type accounts to be credited […]

978-0078025815 Journal Entries and Statement Memo

_______________________________________________________________________________________________ School of Accounting MSC 0203 Harrisonburg, VA 22807 Phone (540) 568-3071 Fax (540) 568-3017 TO: Adopters of Essentials 11th Edition FROM: Paul Copley SUBJECT: Practice Set The Twelfth Edition provides a practice set that is a middle ground between […]

978-0078025815 Journal Entries and Statement Solution Enterprise Fund

ENTERPRISE FUND – GENERAL LEDGER Journal Entries debits credits DUE FROM 3 Feb. 1 Cash 300,000 CASH OTHER FUNDS SUPPLIES ACCOUNTS RECEIVABLE Transfer in – capital contribution 300,000 bb – bb – bb – bb – To record contribution from […]

978-0078025815 Journal Entries and Statement Solution Governmental Type Funds

General Fund – General Ledger # date Journal Entries debits credits CASH 1 Jan. 1 Encumbrances 11,806 bb 18,000 ALLOWANCE FOR Budgetary Fund Balance Reserve for Encumbrances 11,806 5450,000 300,000 3TAXES RECEIVABLE UNCOLLECTIBLE TAXES SUPPLIES additional debit account To re-establish […]

978-0078025815 Journal Entries and Statement Solution Govt Wide

Worksheet to convert Governmental fund basis information to accrual basis Journal Entries debits credits (enter as negatives) Gov’tal Fund Balances Adjustments & Eliminations Balances for Gov’t-wide Stmts 1 Capital Assets 1,875,000 Debits Credits Bonds Payalbe 1,875,000 DEBITS: to record beginning […]

AC 169

1) The single audit requirements apply only to state and local governments. Private not-for-profits do not have to comply with these requirements, even if they receive federal grants. 2) For most state and local governments, the budget, when adopted according […]

AC 340 Quiz 1

1) A fire protection district is anexample of specialpurpose local government. 2) The residual classification for governmental funds other than the General Fund is Assigned. Answer: True 3) When closing the General Fund and Special Revenue Funds of a state […]

AC 609

1) The Proprietary Fund Statement of Revenues, Expenses, and Changes in Fund Net Position must include a performance indicator, such as operating income. 2) If a private not-for-profit fails to comply with donor restriction on contributions received, the organization must […]

AC 744 Quiz

1) The program expense ratio is calculated as Program service expenses / Total expenses. 2) FASB sets the reporting standards for private not-for-for profits. Answer: True 3) Governments must capitalize infrastructure assets in the government-wide statements Answer: True 4) Capital […]

ACC 227 Test 2

1) Budgetary comparison schedules are not required for proprietary funds. 2) The GASB Concept Statement on Service Efforts and Accomplishments Reporting requires state and local governments to include inputs of nonmonetary resources in their financial reporting. Answer: False 3) General […]

ACC 266 Test

1) In addition to the government-wide statements, governments are required to prepare fund financial statements for governmental, proprietary and fiduciary funds. 2) Unexpended Appropriations Balance may be interpreted as how much a government may continue to spend and remain within […]

Acc 357

1) Examples of budgetary accounts include Estimated Revenues, Appropriations, and Estimated Other Financing Uses. 2) The Governmental Accounting Standards Board sets financial reporting standards for all units of government: federal, state, and local. Answer: False 3) According to the rules […]

ACC 393 Midterm 2

1) Capital projects funds are always included in the Budgetary Comparison Schedule. 2) Allotmentsare made at the agency level and assign portions of the appropriation to subunits or programs. Answer: True 3) To apply for tax-exempt status, an organization must […]

ACC 436 Quiz 3

1) An internal service fund is required whenever an activity is funded by fees or charges from other government departments. 2) Unless use of an agency fund is mandated by law, by GASB standards, or by decision of the governing […]

ACC 798 Quiz 3

1) According to the rules for accounting for colleges and universities under the jurisdiction of the FASB, expenses are reported by function, either in the statements or in the notes. 2) A Statement of Functional Expenses is not required for […]

Acc 841 Homework

1) The current and long-term portions of General Long-term Debt are normally reported in a debt service fund. 2) Investment Trust Funds account for only the external portion of investment pools. Answer: True 3) Private colleges and universities use the […]

Acc 855 Test 2

1) Employers with defined contribution plans will report a pension liability if the required contribution has not been fully paid by year end. 2) Fiduciary funds are reported only in the fund-basis financial statements. Answer: True 3) An annuity serial […]

Acc 875 Quiz 3

1) Revenue for reimbursement grants may be recognized before expenditures take place as long as the grant has been awarded. 2) The Fiduciary Funds are included in the Government-Wide Financial Statements. Answer: False 3) There are no expenses in modified […]

Accounting 284

1) Assuming an auditee is not considered low-risk, the auditor is required to express an opinion on compliance on major programs, which must add up to 90 percent of federal funds expended by the auditee. 2) Governments and other nonprofits […]

Accounting 679 Midterm 1

1) Business activities fund statements must be changed to the accrual basis from the modified accrual basis when preparing government-wide financial statements. 2) When preparing the government-wide statements, an entry is required to record depreciation expense on general capital assets […]

Acct 197 Quiz 1

1) Government-wide statements are to be prepared using the current financial resources measurement focus and modified accrual basis of accounting. 2) FASB requires that the reconciliation of income and cash flows from operations starts with operating income. Answer: False 3) […]

ACCT 273 Quiz 1

1) In the General Fund, revenues are recognized when measurable and earned. 2) The most numerous and important enterprise services rendered by local governments are public utilities. Answer: True 3) A fund represents part of the activities of an organization […]

Acct 371 Final

1) Country clubs and labor unions are not included in the category other not-for-profit organizations because they provide benefit to their members only and not to the general public. 2) Both governmental owned and private health care providers use the […]

ACCT 486 Midterm 1

1) According to GASB 34, restricted Net Position does not include those that are the results of constraints imposed by creditors, grantors, contributors, or laws or regulations of other governments. 2) When preparing fund basis financial statements, any funds not […]

Acct 526 1 Fiduciary funds include

1) Fiduciary funds include agency, pension trust, investment trust, and permanent funds. 2) Escheat property, often collected by the state, is to be reported either in a private-purpose trust fund or in the fund to which the property ultimately reverts. […]

ACCT 528 Quiz 3

1) Unrelated Business Income Tax is an excise tax, applied to the gross receipts of a business activity. Therefore allocations of expenses incurred in generating the income are irrelevant. 2) The Statement of Custodial Activity is not required of every […]

ACCT 604 Test 1

1) Tax-exempt organizations are required to file Form 990 by the 15th day of the 9th month following the organizations taxable year. 2) Service Efforts and Accomplishments Reporting includes measures of service inputs, outputs and outcomes. Answer: True[/cpmembership] 3) Special-purpose […]

Acct 660 Quiz 3

1) Universities treat athletic scholarships as a reduction in revenue. 2) The Comprehensive Annual Financial Report (CAFR) contains four major sections: introductory, financial, supplementary, and statistical. Answer: False 3) Private-purpose Trust Funds benefit individuals, private organizations, or other governments. Answer: […]

ACCT 712

1) Inflows from self-supporting university operations, known as auxiliary enterprises, are unrestricted. 2) Supporting expenses are included in the numerator of the program expense ratio. Answer: False 3) Public higher education institutions that report as special-purpose entities engaged in business-type […]

ACCT 745 Quiz 1

1) When converting from governmental fund financial statements to the governmental activities column of the government-wide statements, the proceeds from the sale of capital assets which were listed as an other financing source are eliminated and the gain or loss […]

ACCT 762 Quiz 1

1) The Financial Accounting Standards Board and the Governmental Accounting Standards Board are parallel bodies under the oversight of the Financial Accounting Foundation. 2) General-purpose governments are those that offer more than one type of basic governmental service, while special-purpose […]

ACCT 836 1 Present and potential

1) Present and potential donors are the primary users of private not-for-profit financial statements. 2) GASB standards for property tax revenue recognition under the modified accrual basis of accounting provide that revenue is permitted to be recorded if the expected […]

Acct 860 Test

1) The government-wide financial statements present the government as a whole, including component units and including fiduciary activities. 2) Special-purpose governments generally provide a limited set of services or programs. Answer: True 3) A non exchange transaction is one where […]

ACT 172 Quiz 2

1) Proprietary funds do not record capital assets, depreciation on those capital assets, and long-term debt. 2) The Budgetary Comparison Schedule requires a column for the original budget, a column for the final revised budget, and a column for actual […]

ACT 401 Quiz 2

1) Governmental attestation engagements must comply with the Government Auditing Standards but are exempt from compliance with the 2) General long-term debt, to be paid out of resources of the government’s taxing power, is reported in both the governmental fund […]

ACT 635

1) An investment trust fund is used to account for the internal portion of a multi-government investment pool, when the reporting government is trustee. 2) Long term liabilities of an enterprise fund are reported in the proprietary fund statement and […]

ACT 824 Quiz 2

1) Churches must file a Form 990 . 2) All donated services are recognized as revenue. Answer: False 3) The introductory and statistical sections of a CAFR are required to be audited. Answer: False 4) Contributions of assets other than […]

ACT 836

1) Typically, budgetary authority that is not obligated by a federal agency before the end of the fiscal year rolls over and is available for the following fiscal year. 2) For hospitals, contractual adjustments to 3rd party payers, such as […]

MET MG 136 Homework

1) The FASB requires private not-for-profit organizations to report net assets (the excess of assets over liabilities) separated by unrestricted, temporarily restricted and permanently restricted. 2) Special-purpose governments that are engaged in both governmental and business-type activities are required to […]

MET MG 188

1) The three major sections of a CAFR are the Introductory, Financial, and Statistical sections. 2) The FASAB was established to recommend accounting and financial reporting standards for the federal government. Answer: True 3) Governmental Auditing Standards identifies four categories […]

MET MG 226 Midterm

1) With respect to private colleges and universities, why are quasi-endowments not classified as permanently restricted net assets while True endowments are? 2) State and local governments may use twelve different fund types. Answer: False 3) The difference between assets […]

MET MG 397 Quiz 3

1) Special-purpose governments engaged in business type activities only are required to prepare both proprietary fund and government-wide financial statements. 2) The Single Audit Actis intended to provide assurance to the federal government that federal funds are protected through a […]

SMG AC 196 Quiz 3

1) Proprietary funds record the net pension liability as a fund liability. 2) Unmatured principal installments and accrued interest which is due shortly after year end are required to be reported as liabilities in the debt service fund at year […]

SMG AC 449 Test 2

1) Unexpended intergovernmental grants and taxes dedicated to capital improvements in a capital projects fund are likely to be classified as Restricted Fund Balance 2) Financial statements prepared for private colleges and universities present net assets as: unrestricted, restricted, or […]

SMG AC 695 Quiz 2

1) The term fiduciary funds include agency, pension trust, investment trust, and private purpose trust funds. 2) The required financial statements for agency funds includea Statement of Fiduciary Net Position, and a Statement of Changes in Fiduciary Net Position. Answer: […]

SMG AC 803 Homework

1) A Charitable lead trust is a type of split-interest agreement. 2) NACUBO guidelines treat estimates of uncollectible accounts as reductions in revenue. Answer: True 3) Positive fund balances of capital projects funds are classified as nonspendable, restricted, committed, or […]

SMG AC 833 Quiz 1

1) In a governmental audit the auditor is required to report directly to appropriate officials in addition to the board or audit committee. 2) An asset may be considered impaired if either the decline in the service utility is unexpected […]

SMG AC 847

1) The 2) According to the rules for accounting for colleges and universities under the jurisdiction of the FASB, depreciation is recorded. When reporting by function, depreciation is allocated to functional categories. Answer: True 3) NACUBO guidelines require both revenues […]