1) Country clubs and labor unions are not included in the category other not-for-profit

organizations because they provide benefit to their members only and not to the general

public.

2) Both governmental owned and private health care providers use the modified accrual

basis of accounting and the economic resources measurement focus.

3) According to the rules for accounting for colleges and universities under the

jurisdiction of the FASB, if both unrestricted and restricted resources are available for a

restricted purpose, the FASB requires that the institution recognize the use of restricted

resources first.

4) Private not-for-profit organizations should have little to no profit.

5) Special revenue funds are used when it is desirable to provide separate reporting of

resources that are assigned to expenditure for purposes other than debt service or capital

projects.

6) In the General Fund, revenues are recognized when earned and available

7) Debt service coverage can only be directly measured from proprietary fund

statements.

8) Blending of financial information is done only when component units and the

primary government are so intertwined that they are essentially the same.

9) GASB Statement No. 34 states that general capital assets should not be reported as

assets in governmental funds but should be reported in the governmental activities

column of the government-wide Statement of Net Position.

10) Both commercial and private sector not-for-profit hospitals and health care

providers follow FASB Statements 116 and 117 .

11) The four classes of non exchange transactions include all of the following except:

A) Imposed non exchange revenues

B) Derived tax revenues

C) Voluntary non exchange transactions

D) Sales of Services

12) Donors to private not-for-profit entities are primarily concerned with which of the

following performance measures?

A)Return on Investment

B) Program Expense Ratio

C) Change in Net Assets

D) Ending Unrestricted Net Assets

13) Which of the following would notbe considered a split-interest agreement,

according to the Not-for-Profit Guide?

A)Charitable remainder trusts

B)Charitable gift annuities

C)Permanent income-sharing agreements

D)Pooled (life) income funds

14) With respect to government-wide statement, which of the following statements is

correct?

A)GASB requires a reconciliation from proprietary fund financial statements to the

government-wide statements business-activities columns from modified accrual

accounting to accrual accounting

B)General capital assets should not be reported as assets in governmental funds but

should be reported in the governmental activities column of the government-wide

Statement of Net Position

C) In addition to the fund basis statement, GASB Statement 34 requires

government-wide statements that are prepared on the modified accrual basis using the

economic resources measurement focus

D) Fiduciary activities are reported in the government-wide statements in a separate

column

15) Which of the following events will result in a journal entry being recorded in both

the budgetary and proprietary accounts of a federal agency?

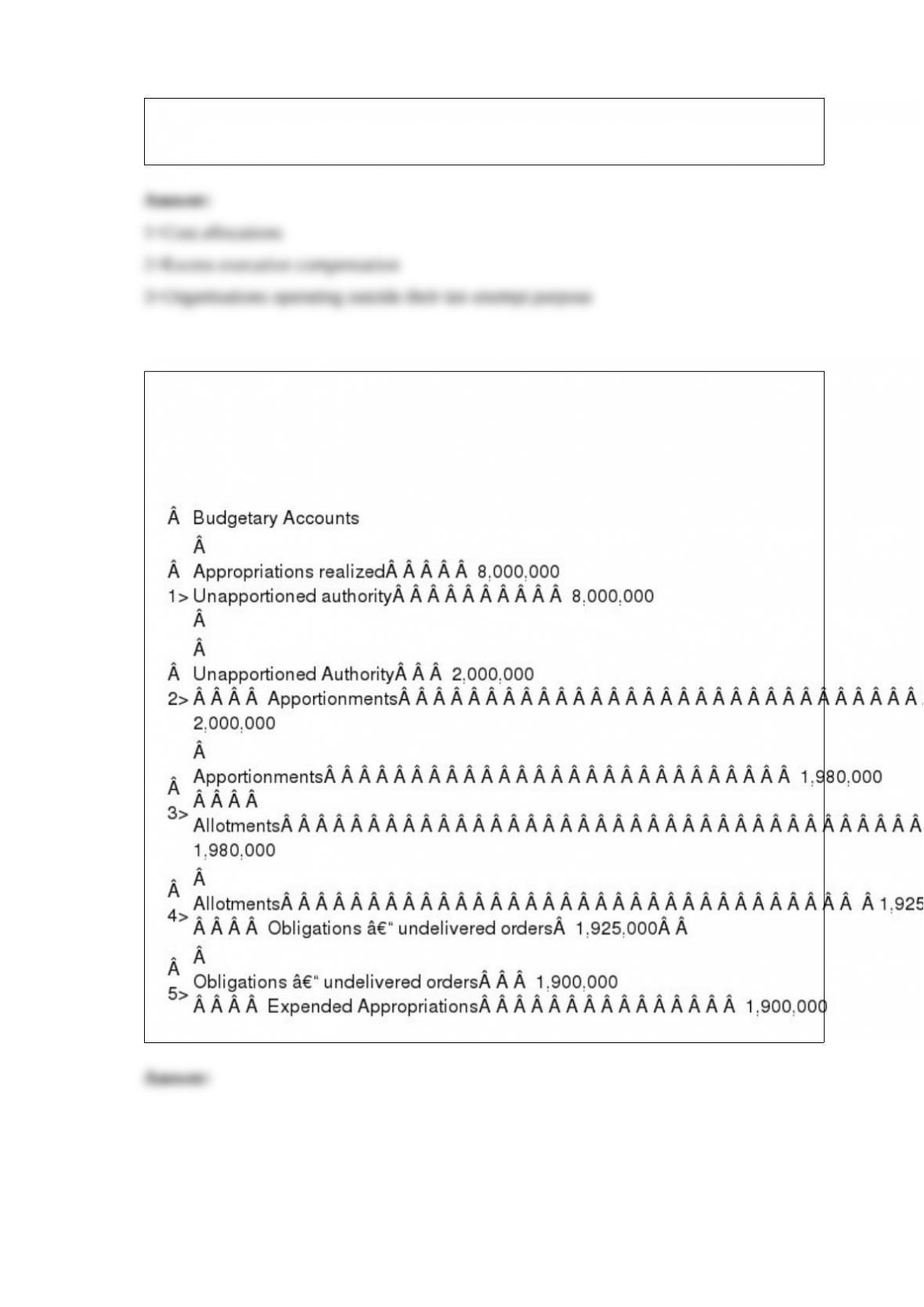

A)OMB establishes the amount of the total appropriation that the agency may expend in

the first quarter

B)Goods or services are received and approved for payment

C)Both (a) and (b)

D) Neither (a) nor (b)

16) Which of the following is (are) accurate regarding a federal agencys Statement of

Net Costs?

A)Net costs reported on the Statement of Net Costs may differ from those appearing in

the Statement of Changes in Net Position, since the latter are measured on the

budgetary basis

B)The Statement of Net Costs provides greater detail about the cost of the Agencys

programs, but agrees in total net cost reported on the Statement of Changes in Net

Position

C)Both (a) and (b) above

D)Neither (a) nor (b) above

17) The General Fund of the City of Bangor purchased water from its Water Utility

Fund in the amount of $20,000. The General Fund would debit:

A)Water Expense

B)Other Financing Uses-Transfers Out

C)Expenditures Control

D)None of the above; no entries would be made

18) Norton County operated a landfill, and accounted for it as an enterprise fund. The

closure and post-closure care costs are estimated to be $20,000,000. It is estimated that

the capacity of the landfill is 5 million tons of waste and that waste will be accepted for

10 years. During 2015, 750,000 tons of waste was accepted by the landfill. The charge

for closure and post-closure care costs for 2015 would be:

A)$ 750,000

B)$2,000,000

C) $3,000,000

D)Impossible to determine from the information given

19) Capital project funds record the proceeds of debt issued as:

A)Other Financing Sources

B)Revenues

C) Expenses

D)Liabilities

20) Where in the CAFR would one find the long-term liability for revenue bonds (paid

from the revenues of an enterprise fund)?

A)The proprietary funds Statement of Net Position only

B)The government-wide Statement of Net Position only

C)The government-wide Statement of Net Position and the RSI Schedule of Bonds

Payable

D)The government-wide Statement of Net Position and the proprietary funds Statement

of Net Position

21) When a government is the sponsor of a multi-government investment pool, the

government should report the external portion of those trust assets in a(n):

A)Pension Trust Fund

B)Investment Trust Fund

C) Private-Purpose Trust Fund

D) Agency Fund

22) The Museum of Creative Arts had the following expenses: $5,000 of membership

development expense, $3,000 of Fund-raising expense, $3,000 of Instructional Classes

expense, and $1,500 of general and administrative expense. What is the program

expense ratio (rounded)?

A)24%

B)39%

C)43%

D)70%

23) Investments in a private-purpose trust fund should generally be reported using:

A) Cost Basis

B) Fair Market Value

C) Equity Method

D) None of the above

24) In order to compute the operating ratio-enterprise funds, one would look in the

CAFR in which of the following sections?

A)In the government-wide Statement of Net Position

B)In the proprietary funds Statement of Net Position

C)In the proprietary funds Statement of Revenues, Expenses, and Changes in Fund Net

Position

D)In the proprietary funds Statement of Cash Flows

25) Which of the following is True regarding revenue recognition for property taxes,

when reporting in the government-wide statements?

A)Assets are recognized when an enforceable legal claim has arisen or when resources

are received, whichever is first

B)Revenues are recognized when measurable and available; that is, when collected

during the current period or no more than 60 days after the end of the current period

C)Both of the above are True

D)Neither of the above is True

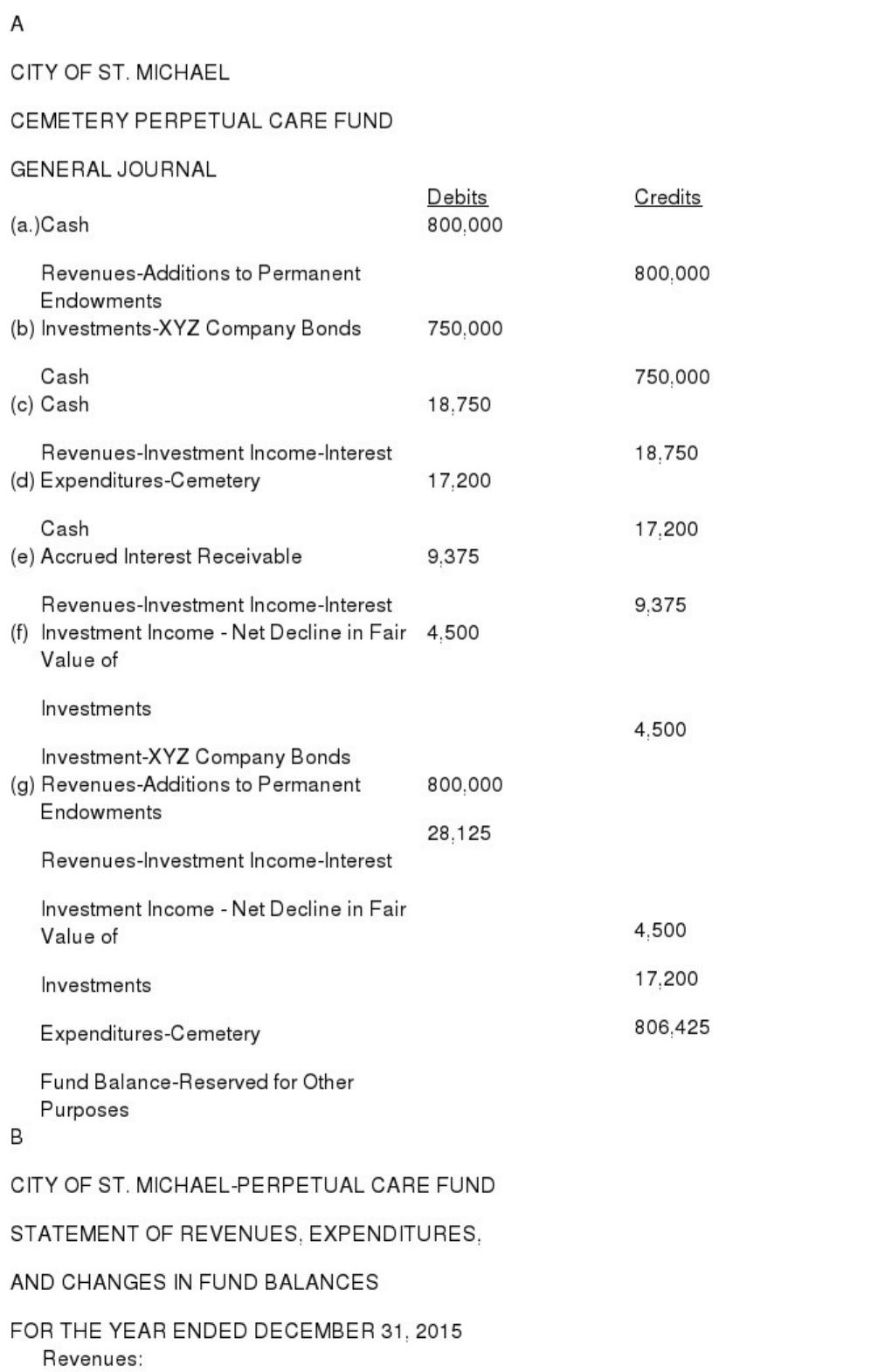

26) The City of St. Michael received a gift of $800,000 from a local resident on April 1,

2015 and signed an agreement that the funds would be invested permanently and that

the income would be used to maintain the city cemetery. The following transactions

took place during the year ended December 31, 2015 .

(a)The gift was recorded on April 1 .

(b)On April 1, 2015, XYZ Company bonds were purchased in the amount of $750,000,

at par. The bonds carry an annual interest rate of 5 percent, payable semiannually on

October 1 and April 1 .

(c)On October 1, the semiannual interest was received.

(d)From October 1 through December 1, payments were made totaling $17,200 to a

lawn service.

(e)On December 31, an accrual was made for interest.

(f)Also, on December 31, a reading of the financial press indicated that XYZ bonds had

a fair value of $745,500, exclusive of accrued interest.

(g)The books were closed.

Required:

A.Record the transactions on the books of the Cemetery Perpetual Care Fund.

B.Prepare a separate Statement of Revenues, Expenditures, and Changes in Fund

Balances for the Cemetery Perpetual Care Fund for the Year Ended December 31,

2015 .

C.Prepare the Balance Sheet for the Cemetery Perpetual Care Fund for the year ended

December 31, 2015

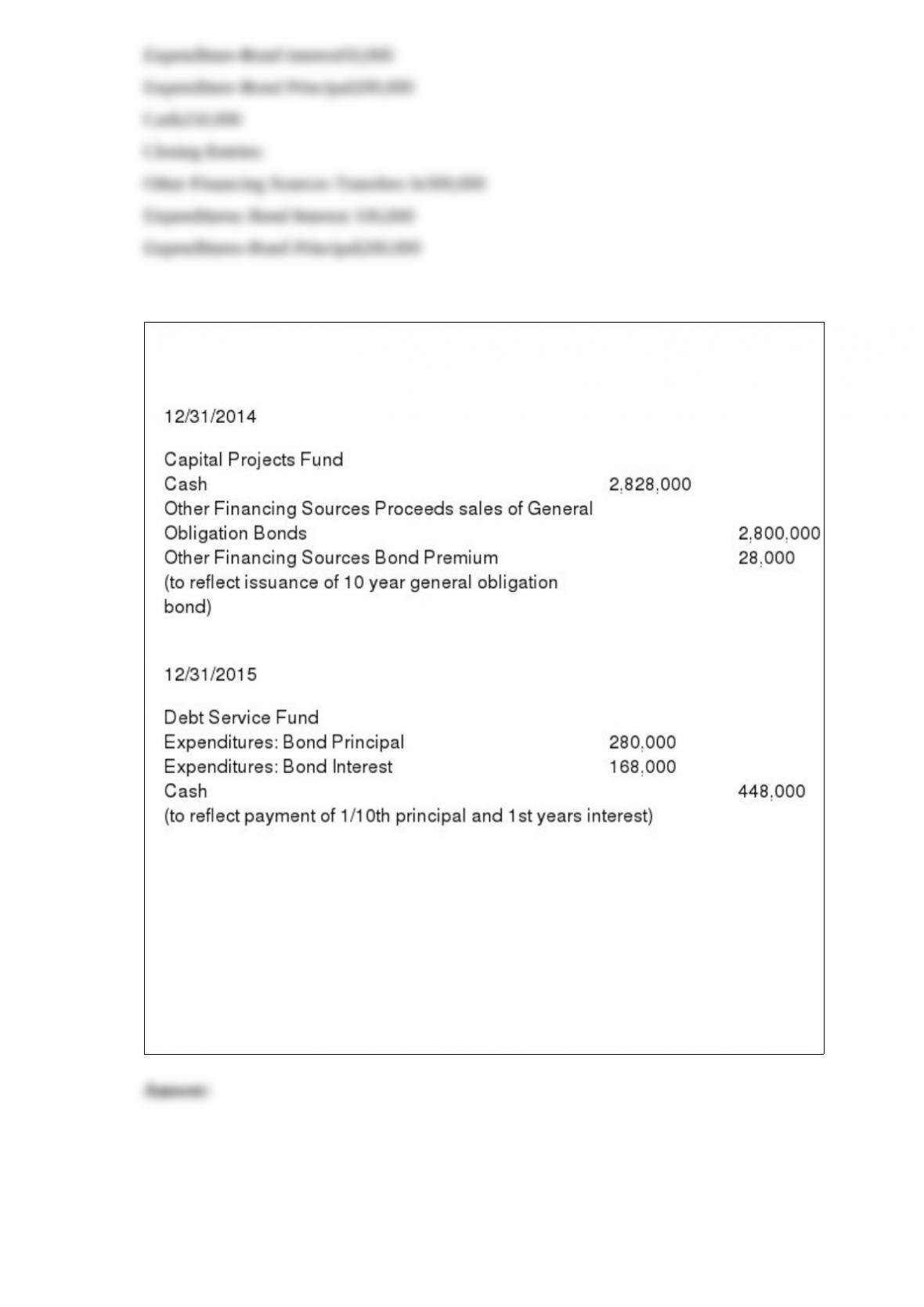

27) The following entries were in the governmental funds.

Required:

Part A.What is the worksheet entry required to adjust beginning (or Position) in the

12/31/2015 government-wide financial statements for long term debt?

Part B.What are the worksheet entries to adjust for current year activity in long-term

debt for the year ended 12/31/2015? Assume interest for the year is due on 12/31 and

the bond premium is amortized on the straight line basis.

28) When a private college or university has a foundation, and that foundation receives

contributions specifically directed for the benefit of the college or university,

A)The college or university records no revenue until monies are received from the

foundation

B)The college or university must recognize its interest in the contribution as an asset

and revenue at the same time as the foundation

C)At the time of the contribution to the foundation, the college or university records an

increase in net assets and unearned revenue. When the money is received the unearned

revenue is reduced and revenue is recorded

D)None of the above

29) Which of the following is True regarding the Single Audit Act and its amendments?

A)A risk-based approach is used

B)An opinion is required on compliance of all programs

C)Both A and B above

D)Neither A nor B above

30) Which of the following is True regarding GASB’s definition of the financial

reporting entity?

A)The financial reporting entity might include a primary government, component units,

joint ventures, or a jointly governed organization

B)Primary governments may be general-purpose governments (such as states, cities,

and counties) or special-purpose governments that have separately elected governing

bodies, are legally separate and are fiscally independent of other state or local

governments

C)Blending is used to incorporate component units when those component units are, in

substance, part of the primary government

D)All of the above are True

31) Which of the following is True regarding the Single Audit Act and its amendments?

A)An auditor is expected to express an opinion on major programs, which are chosen

based on size

B)An auditor is required to select all Type A programs as major programs

C)Both A and B above

D)Neither A nor B above

32) When recording property taxes, the estimated uncollectible amount of property

taxes is:

A)Recognized as an expenditure

B)Recognized as a reduction of revenue

C)Not recognized

D) None of the above

33) A donor gave $60,000 to a nongovernmental, not-for-profit charity with instructions

that the funds be transferred to Sam Smith, an individual who lost his home in a fire.

The not-for-profit would:

A)Record the $60,000 cash and credit a liability

B)Record the $60,000 cash and credit temporarily restricted revenue

C)Do either (a) or (b), depending upon the policy of the not-for-profit

D)Not record the transaction, because the money is going directly to the intended

recipient

34) The Revenues Control account of the General Fund is debited when:

A)The budget is recorded at the beginning of the year

B)Uncollectible taxes receivable accounts are written off

C)Property taxes are collected

D)None of the above

35) Which of the following is True regarding fiduciary funds?

A)Fiduciary funds are not included in the government-wide financial statements

B)Fiduciary funds include agency, pension (and other employee benefit) trust,

private-purpose trust, and investment trust funds

C)Both of the above

D)Neither of the above

36) Which of the following would not be a non exchange transaction for a state

government?

A)Sales of lottery tickets

B)Property taxes

C)Fines and forfeits

D)Income taxes

37) The ______ Fund accounts for all resources other than those required to be

accounted for in other funds

A)Agency

B)Enterprise

C) General

D)Special revenue

38) Investments by private not-for-profit organizations in equity securities should be

carried at

A) Historical cost

B) Fair Market Value

C) Lower of cost or Market

D) None of the above

39) The Governmental Accounting Standards Board has been given authority to

establish accounting and financial reporting standards for:

A)all governmental units and agencies.

B)federal, state, and local governments and governmentally related utilities, authorities,

hospitals, and colleges and universities

C)state and local governmental entities, and governmentally related utilities, authorities,

hospitals, and colleges and universities

D)all governmental units and all not-for-profit organizations

40) Which of the following is not correct regarding Government Trust Accounting?

A)If a trust is to benefit the government or its citizenry, it should be accounted for in a

special revenue or permanent fund

B)If a trust is to benefit individuals, private organizations, or other governments, it

should be accounted for in a private-purpose trust fund

C)The journal entry to establish a permanent fund would include a credit to Fund

Balance Nonspendable

D)Trust funds accounted for in a permanent fund useaccrual accounting

41) A private not-for-profit organization received a gift of $640,000 with purpose

restrictions in 2014 . In 2015 funds were expended for the purpose outlined in the gift,

however, it was not possible to determine whether the restricted funds or unrestricted

funds were used. The presumption should be:

A)The restricted funds would have been used first

B)The unrestricted funds would have been used first

C)The restricted funds and unrestricted funds would have been used equally

D)The restricted funds and unrestricted funds would have been used, based on a

weighted average of the amounts

42) Which of the following is True regarding the governmental fund financial

statements?

A)The governmental fund financial statements include the Balance Sheet and the

Statement of Revenues, Expenditures, and Changes in Fund Balances

B)The governmental fund financial statements are prepared using the current financial

resources measurement focus and the modified accrual basis of accounting

C)Both of the above

D)Neither of the above

43) Short-term loans which are backed by the taxing power of the governmental unit

and used to meet working capital requirements are called:

A) Appropriation loan

B) Inter-fund loans

C) Other financing sources

D) Tax anticipation notes

44) Which of the following is True regarding the final appropriations budget?

A) Can be changed at any time by the accounting department

B) Can be exceeded by actual appropriations

C) Is legal and binding

D) None of the above

45) Which of the following statements is not required for pension trust funds?

A)Statement of Fiduciary Net Position

B)Statement of Changes in Fiduciary Net Position

C)Statement of Fiduciary Cash Flows

D)None of the above; all three statements should be prepared for pension-trust funds

46) Which of the following is not correct with respect to mergers under the rules

established by FASB Statement No. 164, Not-for-Profit Entities: Mergers and

Acquisitions?

A)If the combination qualifies as a merger, it will be accounted for using the carryover

method

B)Goodwill is recognized on long term assets only

C)Assets and liabilities are transferred from both existing entities to the new entity at

book value

D)The entity resulting from the merger is a new reporting entity, with no activity before

the date of the merger

47) Which of the following is one of the principal organizations that formed the Federal

Accounting Standards Advisory Board?

A)Department of Treasury

B)Congressional Budget Office

C)American Institute of CPAs

D)All of the above

48) On April 1, 2015, the City of Southern Ponds issued $3,500,000 in 4% general

obligation, tax supported bonds at 101 for the purpose of constructing a new police

station. The premium was transferred to a debt service fund. A total of $3,490,000 was

used to construct the police station, which was completed before December 31, 2015,

the end of the fiscal year. The remaining funds were transferred to the debt service fund.

The bonds were dated April 1, 2015, and paid interest on October 1 and April 1 . The

first of 20 equal annual principal payments of $175,000 is due April 1, 2016 .

In addition to reporting a $3,500,000 liability and a $35,000 bond premium in the

government-wide Statement of Net Position, how would the bond sale be reported?

A)As a $3,500,000 liability in the government-wide Statement of Net Position and as a

$3,500,000 other financing source in the debt service fund

B)As a $3,535,000 liability in the government-wide Statement of Net Position, as a

liability of $ 3,535,000 in the capital projects fund, and as another financing source of

$3,535,000 in the capital projects fund

C)A $3,535,000 other financing source in the capital projects fund, a $35,000 other

financing use in the capital projects fund, and a $35,000 other financing source in the

debt service fund

D)The $3,500,000 liability in the government-wide Statement of Net Position and the

$35,000 would also be recorded as a bond premium in the Statement of Net Position

49) Under GASB Statement 34, capital assets:

A)must be reported in government-wide statements but are not reported in any of the

fund financial statements

B)must be reported in government-wide statements and in proprietary fund financial

statements

C)are not to be reported in either government-wide or fund financial statements

D)are to be reported but not depreciated in government-wide and fund financial

statements

50) To qualify as a collection, a donated or purchased item must meet all of the

following conditions except:

A) Held for public exhibition, education, or research to further public service

B) Protected, kept unencumbered, cared for, and preserved

C) Subject to an organizational policy that requires the proceeds from sales of

collection items to be used to acquire other collectibles

D) All of the above conditions must be met

51) Distinguish between the Encumbrances Control account and the Budgetary Fund

Balance — Reserve for Encumbrances account

52) Identify three items often found in Required Supplementary Information.

53) Describe the accounting required for risk management activities of governmental

units when the government is self-insured.

54) The IRS announced that it considers tax-exempt organizations to be one of its four

highest enforcement priorities. What are the three areas of concern for the IRS?

55) Assume a federal agency prepared the following journal entries during the first

quarter of the year. Prepare a schedule showing the status of the appropriation at the

end of the first quarter.

56) Write yes or no in each box to indicate whether each property applies to the

following funds:

57) Contrast the economic resources measurement focus and the current financial

resources measurement focus with regard to the accounting treatment of capital assets.