1) Business activities fund statements must be changed to the accrual basis from the

modified accrual basis when preparing government-wide financial statements.

2) When preparing the government-wide statements, an entry is required to record

depreciation expense on general capital assets

3) When preparing the government-wide statements, worksheet entries are booked to

provide the trial balance amounts used to prepare the financial statements.

4) A Special Revenue Fund may not have a positive Unassigned Fund Balance

5) Conditional promises to give are recognized as revenue or support when the promise

is made net of estimated uncollectible receivables.

6) When establishing funds, governments should attempt to minimize the number of

special revenue and other funds, instead using functional classification to record

transaction detail.

7) When converting from the enterprise funds Statement of Net Position to the

government-wide Statement of Net Position (government-wide statements), it is not

necessary to add fixed assets and to deduct long-term debt.

8) The basic financial statements of a state or local governmental unit include the

MD&A, government-wide statements, fund statements, and the notes.

9) With respect to fund basis financial statements, a government may only designate a

fund to be a major fund if it meets the size thresholds established by GASB.

10) Governments must have as many funds as necessary to fulfill legal requirements

and sound financial administration but must have at a minimum a General Fund.

11) A Charitable gift annuity is a type of split-interest agreement.

12) Governmental fund financial statements are prepared using the current financial

resource measurement focus.

13) Inter fund services provided and used are recognized directly as Revenues and

Expenditures.

14) When a contributor and a government agree that the principle and/or income of trust

assets is for the benefit of individuals, organizations, or other governments, an agency

trust fund has been formed.

15) Fixed assets may be recorded by a private not-for-profit as temporarily restricted or

unrestricted, depending on the policy of the organization.

16) Enterprise funds are reported in the fund-basis statements only.

17) Which of the following would be considered a program revenue in the Statement of

Activities of a local government?

A)A grant from the state to construct utility plant

B)A motor fuel tax, restricted for road repairs

C)Both of the above

D)Neither of the above

18) Managements Discussion and Analysis (MD&A) in The Comprehensive Annual

Financial Report (CAFR) is part of the Financial Section.

19) Which of the following is False regarding government-wide financial statements?

A) Government-wide financial statements are prepared using the accrual method of

accounting

B) General capital assets are required to be reported on the government-wide balance

sheet

C) GASB requires a reconciliation from fund financial statements to government-wide

financial statements

D) Worksheet entries are required to change the enterprise fund financial statements to

the accrual basis of accounting

20) Assume a government is determined to be a special-purpose government engaged in

business-type activities only. Which of the following financial statements would be

required?

A)Balance Sheet, Statement of Revenues, Expenditures, and Changes in fund Balances

B)Statement of Net Position, Statement of Activities, Statement of Cash Flows

C)Statement of Net Position, Statement of Revenues, Expenses, and Changes in Net

Position, Statement of Cash Flows

D)Statement of Net Position and Statement of Activities

21) Which of the following is responsible for preparing the federal governments

consolidated financial statements?

A)Government Accountability Office

B)Congressional Budget Office

C)Office of Management and Budget

D) Department of Treasury

22) The Single Audit Act intends that auditors conducting regular financial audits of

state and local governments and not-for-profits organizations provide assurance to the

federal government that:

A)Federal funds have been expended in accordance with laws and regulations

B)Federal funds are protected through a system of internal controls and sound financial

management practices

C)Both A and B above

D)Neither A nor B above

23) Which of the following is True regarding the government-wide Statement of

Activities?

A)Fiduciary activities are not reported

B)Discretely presented component units are not reported

C)Both of the above

D)Neither of the above

24) The reconciliations required to be presented on the face of the governmental fund

financial statements or in separate schedule immediately after the fund financial

statements include:

A) Reconciliation from the governmental fund Balance Sheet to the Statement of Net

Position

B) Reconciliation from the governmental fund Statement of Revenues, Expenditures,

and Changes in Fund Balances to the Statement of Activities

C) Both A & B

D) No reconciliations are required to be submitted

25) Which of the following is True with respect to special assessment levies?

A)If the government is not liable for the special assessment debt directly or through

guarantee, the special assessment is accounted for in an agency fund

B)Taxpayers may opt out of a service-type special assessment if they agree to not use

the service funded by the assessment

C)Service-type special assessments may not be accounted for in the General or special

revenue fund

D)Construction-type special assessments are accumulated until there is enough money

to finance the construction project

26) Which of the following is True regarding capital projects funds?

A)Capital projects funds are considered to be governmental funds

B)Capital projects funds use the economic resources measurement focus and accrual

basis of accounting

C)Encumbrance accounting is not used

D)Fixed assets are depreciated in capital projects funds

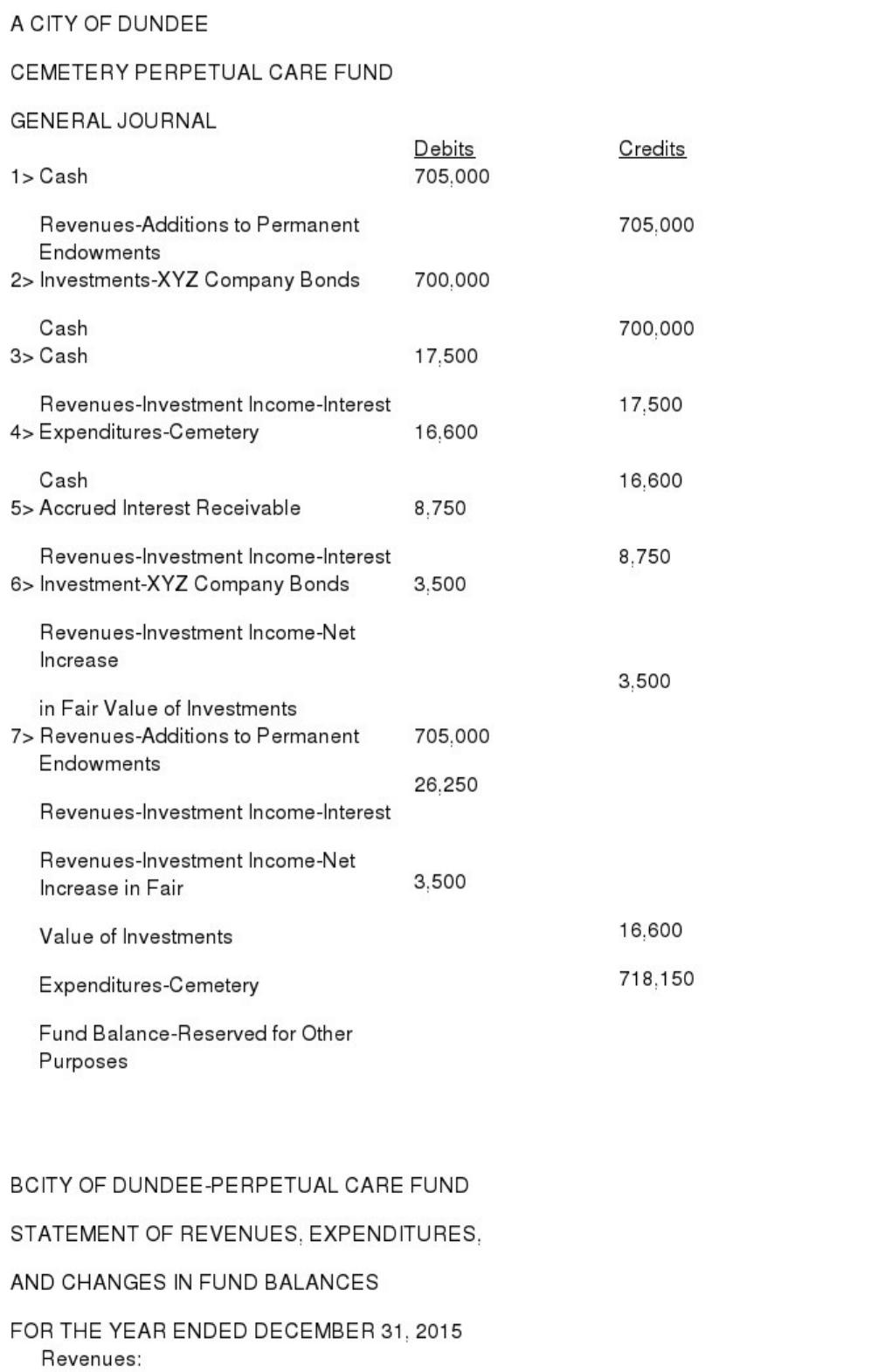

27) The City of Dundee received a gift of $705,000 from a local resident on April 1,

2015 and signed an agreement that the funds would be invested permanently and that

the income would be used to maintain the city cemetery. The following transactions

took place during the year ended December 31, 2015 .

(a)The gift was recorded on April 1 .

(b)On April 1, 2015, XYZ Company bonds were purchased in the amount of $700,000,

at par. The bonds carry an annual interest rate of 5 percent, payable semiannually on

October 1 and April 1 .

(c)On October 1, the semiannual interest was received.

(d)From October 1 through December 1, payments were made totaling $16,600 to a

lawn service company.

(e)On December 31, an accrual was made for interest.

(f)Also, on December 31, a reading of the financial press indicated that XYZ bonds had

a fair value of $ 703,500, exclusive of accrued interest.

(g)The books were closed.

Required:

A.Record the transactions on the books of the Cemetery Perpetual Care Fund.

B.Prepare a separate Statement of Revenues, Expenditures, and Changes in Fund

Balances for the Cemetery Perpetual Care Fund for the Year Ended December 31,

2015 .

28) Where in the basic financial statements, in most cases, would one find internal

service activities reported?

A)In the proprietary funds statements and in the business-type activities column of the

government-wide statements

B)In the governmental funds statements and in the governmental activities column of

the government-wide statements

C)In the governmental funds statements and in the business-type activities column of

the government-wide statements

D)In the proprietary funds statements and in the governmental activities column of the

government-wide statements

29) Which of the following would not be an adjustment for long-term debt when

preparing government-wide financial statements?

A)Changing Other Financing Sources – Proceeds of Bonds to Bonds Payable

B)Changing Expenditures Bonds Principle to Bonds Payable

C)Recording the cash received from a debt issue

D)Amortizing bond premiums

30) If a government decides to account for its risk management activities in a single

fund, it must use:

A)An Internal Service Fund

B)A Fiduciary Fund

C)ASpecial Revenue Fund

D)Either the General Fund or an Internal Service fund

31) Revenue bonds sold by a water utility fund, upon sale, would be recorded in an

enterprise fund as:

A)Other Financing SourcesProceeds of Bonds

B)A liability

C)A direct addition to Net Position

D)Nonoperating RevenuesProceeds of Bonds

32) GASB requires that educational institutions who engage in business-type activities

and issue debt account for the debt by:

A)Recording the debt service as an expenditure as it becomes due

B)Recording the interest as an expense when it is due and payable

C)Recording the principal net of any premium or discount when the debt is issued and

expense the interest as it is paid

D)Recording the interest expense on the accrual basis, including amortizing the

premium or discount, if applicable

33) How should the following revenues be reported by a private college?

$15,000 for the improvement of a study lounge,

$5,600 in unrestricted contributions,

$600 unrestricted investment income on endowment investments,

$11,600 sales of services by auxiliary enterprises.

UnrestrictedRestricted

A)32,800 0

B) 17,80015,000

C) 17,20015,600

D) 5,60027,200

34) Which type of pension plan is required to pay out a certain sum, generally based on

a percentage of salary upon retirement and the number of years of service?

A)Defined Benefit

B)Defined Contribution

C)Contributory

D)Noncontributory

35) Which of the following is True regarding fiduciary funds?

A)When a government provides employees a defined benefit pension plan,the

government is required to present a ten year Schedule of Changes in Net Pension

Liability and Related Ratios as required supplementary information

B)Governmental type funds report a net pension liability representing the unfunded

pension obligation

C)Both of the above

D)Neither of the above

36) The FASB has the authority to set accounting standards for all of the following

organizations except:

A)Public colleges

B)Private colleges

C)For profit proprietary schools

D)Educational foundations established to support a private college or university

37) Which of the following statements is correct with respect to GASB Statement No.

53 which establishes reporting requirements for governments entering into derivative

instruments?

A)Changes in the value of hedge derivatives are deferred and reported in the Statement

of Net Position

B)If a derivative is an investment derivative, the changes in the value of the derivative

are deferred and reported in the Statement of Net Position

C)Statement No. 53 does not apply to proprietary funds

D)Statement No. 53 applies to government financial statements prepared using the

modified accrual basis of accounting

38) Which of the following is True regarding the government-wide Statement of Net

Position?

A)The government-wide Statement of Net Position reflects capital assets, net of

accumulated depreciation, for both governmental and business-type activities

B)The government-wide Statement of Net Position must be prepared in a classified

format; that is, both assets and liabilities must be separated between current and

long-term categories

C)The government-wide Statement of Net Position includes all resources entrusted to

the government; including governmental, proprietary, and fiduciary

D)A reporting entity (primary government plus component units) total column is

required

39) The fund basis statements for governmental funds are presented using the

A) Economic Resources Measurement focus and the Accrual Basis of Accounting

B)Current Financial Resources Measurement focus and the Modified Accrual Basis of

Accounting

C)Current Financial Resources Measurement focus and the Accrual Basis of

Accounting

D) Economic Resources Measurement focus and the Modified Accrual Basis of

Accounting

40) The NACUBO Financial Accounting and Reporting Manual treats estimates of

uncollectible student accounts as:

A) Bad debt expense

B) Reduction in revenue

C) Other financing uses

D) None of the above

41) Which of the following groups would not be considered a component unit of a

special-purpose government, for the purposes of applying GASB Statement 39:

Determining Whether Certain Organizations Are Component Units?

A)General governments

B)Booster clubs

C)Museums

D)Health care entities

42) Which of the following is not a fiduciary fund?

A) Agency

B) Permanent

C) Pension trust

D) Private-purpose trust

43) Which of the following fund types is present in every general-purpose government?

A) Permanent

B) Special revenue

C) General

D) Capital projects

44) If the receivable for a student is $9,000 and the student pays only $1,000 as the

result of receiving a work study appointment from the school, what would be the

appropriate debits?

A) Debit Cash and Debit Discount on Revenue

B) Debit Cash and Debit Expense

C) Debit Cash and Debit accounts receivable

D) Debit Cash

45) Budgetary Fund Balance — Reserve for Encumbrances (current year) in excess of a

balance of Encumbrances Control indicates:

A)An excess of Vouchers Payable over Encumbrances Control

B)An excess of purchase orders released over invoices received

C)An excess of invoices received over purchase orders released

D)A recording error

46) What basis of accounting would the Enterprise Fund use?

A) Accrual

B) Modified Accrual

C) Cash

D) Expended Accrual

47) What is the correct debit or credit for the following scenario: A contract was issued

for the major part of work to be done by a private contractor in the amount of

$1,200,000 for a new County court house?

A) Debit: Budgetary Fund Balance — Reserve for Encumbrances

B) Debit: Construction expenditures

C) Credit: Cash

D) Debit: Encumbrances