1) Churches must file a Form 990 .

2) All donated services are recognized as revenue.

3) The introductory and statistical sections of a CAFR are required to be audited.

4) Contributions of assets other than cash to a private not-for-profit are recorded at the

donors basis

5) Patient service revenue for a hospital does not include charges for charity care.

6) When converting from fund financial statements to government-wide statements, it is

necessary to eliminate transfers that are between the categories of governmental

activities and business-type activities.

7) Agency funds report the excess of assets over liabilities as Net Position.

8) GASB requires a reconciliation between the amount shown as GAAP expenditures in

the basic financial statements and the amount shown in the budgetary comparison

schedule.

9) Special-purpose governments that are engaged in more than one governmental

activity are required to use the full reporting model including MD&A,

government-wide and fund-basis statements, notes to the financial statements and RSI.

10) A tax-exempt organization must pay income taxes on income generated from trade

or business activities unrelated to the entitys tax-exempt purposes.

11) Contributions to be paid in future periods should be recorded at present value.

12) When preparing government-wide statements, depreciation expense must be

eliminated.

13) According to GASB standards relating to Budgetary Accounting, an annual budget

should be adopted by every governmental unit.

14) A special item is a significant transaction that is unusual or infrequent, but within

the control of management.

15) Internal Service funds are reported in the fund-basis statements only.

16) City and county governments are not typically classified as special purpose

governments.

17) Which of the following statements is False?

A)With respect to fund basis financial statements, a government may designate any

fund to be a major fund if reporting that fund separately would be useful

B)When preparing fund basis financial statements, any funds not reported separately

are reported by function

C)When preparing fund basis financial statements, any funds not reported separately

are aggregated and reported in a single column under the label non-major funds

D)In addition to the government-wide statements, governments are required to prepare

fund financial statements for governmental, proprietary and fiduciary funds

18) Which of the following is True regarding modified accrual accounting?

A)Modified accrual accounting requires that all expenditures be recognized on the cash

basis

B)Revenues are recognized in the period in which they become available and

measurable, and expenditures are recognized at the time a liability is incurred,except for

principal and interest on long-term debt

C)Modified accrual accounting is required for all fund financial statements

D)All of the above

19) Which of the following is not True regarding the Statement of Activities for

nongovernmental, not-for-profit organizations?

A)FASB requires that the change in net assets be reported for each of the net asset

classes

B)Expenses are reported as unrestricted, temporarily restricted or permanently

restricted

C) Expenses are reported as decreases in unrestricted net assets

D)Organization-wide totals must be provided

20) Which of the following is True about the combining financial statements?

A) They are used whenever a non-major column is used in one of the fund financial

statements

B) The total column in the combining statements is not always the same as the

non-major funds column in the basic financial statements

C) Both of the above

D) Neither of the above

21) A donor gave a gift of $40,000 cash to a private college in 2014 to support basic

psychology research. The funds were expended in 2015 . The private college would

recognize the $40,000 as:

A)Revenue in 2014 increasing temporarily restricted net assets; recognize the expense

in 2015, and reclassify the resources from temporarily restricted net assets to

unrestricted net assets in 2015

B)Deferred revenue in 2014 and as revenue in 2015, increasing temporarily restricted

net assets. The expense would be recognized also in 2015, and the resources would be

reclassified from temporarily restricted net assets to unrestricted net assets in 2015

C) Deferred revenue in 2014 and as revenue in 2015, increasing unrestricted net assets.

The expense would be recognized in 2015

D)Either (b) or (c), depending upon the policy of the private college

22) GASB provides which method(s) for including component unit financial

information with that of the primary government?

A) Discrete Presentation

B) Blending

C) A and B

D) None of the above

23) Tuition and fees for the Northern University was assessed at $22,000,000.

Scholarship allowances, for which no services are required, were $1,600,000 and

graduate assistantships, for which services are required, were $1,000,000.

What is the journal entry to record tuition revenue?

A) Accounts receivable 20,400,000

Operating Revenue-Student Tuition & Fees20,400,000

B) Accounts Receivable22,000,000

Operating Revenue-Student Tuition & Fees22,000,000

C) Accounts Receivable19,400,000

Operating Revenue-Student Tuition & Fees19,400,000

D) Accounts Receivable21,000,000

Operating Revenue-Student Tuition & Fees21,000,000

24) Service Efforts and Accomplishments reporting is relevant because:

A)SEA reporting provides more complete information about a government entity’s

performance than can be provided by the basic financial statements

B)The GASB requires supplemental reporting of service efforts and accomplishments

C)Enterprise fund statements do not do a good job of measuring efficiency or

effectiveness

D)All of the above

25) Which of the following occurs when uncollectible delinquent taxes are written off?

(Ignore interest and penalties)

A)Delinquent Tax Receivable is increased

B) Accounts receivable goes down and the Estimated Uncollectible Taxes Account is

increased

C)Net receivables remain unchanged

D) Uncollectible Delinquent Tax Expense is increased

26) Which of the following is True regarding the financial reporting entity of a state or

local government?

A)Only a primary government is reported in the government-wide statements

B)A school district could never be a primary government

C)Many component units are discretely presented, rather than blended

D)All of the above are True

27) The Township of Thomasvilles General Fund has the following net resources at

year end:

$77,000 of prepaid insurance

$375,000 rainy day fund approved by the township governing board with specific

conditions for its use

$2,500 of supplies inventory

$61,000 state grant for snow removal

$150,000 contractual obligations for the purchase of equipment

$200,000 to be used to fund government operations in the future

Outstanding encumbrance of $80,000 for the purchase of furniture & fixtures (assume

no contractual obligation)

What would be the total Restricted fund balance?

A)$ 61,000

B)$150,000

C)$200,000

D)$375,000

28) Which of the following is one of the criteria to determine if a governmental fund is

considered to be a major fund?

A)Total assets, liabilities, revenues or expenditures of the individual governmental fund

constitutes 10 percent of the governmental funds category

B) Total assets, liabilities, revenues or expenditures/expenses are 5 percent of the total

of the governmental and enterprise category. Other funds may be designated major

funds at the discretion of management

C)Both A and B are required

D)Either A or B will qualify a fund to be a major fund

29) Which of the following is True regarding the financial statements for

special-purpose entities?

A)Special-purpose entities that are engaged only in one governmental activity may

combine government-wide and governmental fund statements

B)Special-purpose entities that are engaged in fiduciary activities only prepare the

statements required for fiduciary funds (Statement of Fiduciary Net Position, Statement

of Changes in Fiduciary Net Position)

C)Both of the above

D)Neither of the above

30) The legal authorization for the administrators of the governmental unit to incur

liabilities during the budget period for purposes specified in the appropriations statute

or ordinance and not to exceed the amount specified for each purpose is a (an):

A)Appropriation

B)Encumbrance

C) Other financing source/use

D)Expenditure

31) Which of the following is(are) accurate regarding a federal agencys Statement of

Budgetary Resources?

A)The statement reports the status of budgetary resources at year end

B)Outlays are measured using the budgetary basis of accounting

C)Both (a) and (b)

D)Neither (a) nor (b)

32) Private sector, not-for-profit health care organizations have a category of assets

called Assets Whose Use is Limited. That category refers to:

A)Assets that have been restricted by donor action

B)Unrestricted assets that have been limited by individuals or entities other than

contributors (such as by bond covenants)

C)Both (a) and (b) above

D)Neither (a) nor (b) above

33) Assume a federal agency receives supplies that had been previously ordered that

will be used to support a federal program. The journal entries at the agency level to

record this event will include:

A)a credit to a liability account such asAccounts Payable

B)a debit to the account Unexpended Appropriations

C)Both (a) and (b)

D)Neither (a) nor (b)

34) If an auditee is not considered low-risk, what percent of federal funds expended are

auditors required to express an opinion on?

A)25%

B)50%

C)70%

D)100%

35) Which of the following is (are) True regarding the Chief Financial Officers Act?

A)The Act created the position of chief financial officer within federal agencies

B)The Act called for audits of the financial statements of federal agencies

C)Both (a) and (b) above

D)Neither (a) nor (b) above

36) The following information was available for the General Fund of the City of

Thomasville for the Year Ended December 31, 2015:

(a)Revenues for the year included property taxes in the amount of $6,612,000, fines and

forfeits in the amount of $ 700,000, and miscellaneous in the amount of$400,000.

(b)Expenditures from current appropriations included: general government, $4,847,000;

public safety, $1,924,000; culture and recreation, 812,000.

(c)In addition to (b) above, expenditures related to prior year appropriations

(encumbered last year) amounted to $40,000 (public safety). Encumbrances issued this

year but not filled amounted to $60,000 (general government).

(d)A transfer was made from the General Fund to a debt service fund in the amount of

$500,000. A transfer was made from an enterprise fund to the General Fund in the

amount of$450,000.

(e)A sale of park land was made during the year, which was considered infrequent but

not unusual and under the control of management. The proceeds amounted to $126,000,

and the land had a basis of $90,000 reported in the government-wide Statement of Net

Position the year before.

(f)Beginning balances included Fund Balance in the amount of $222,000.

Required: Prepare a Statement of Revenues, Expenditures, and Changes in Fund

Balances for the General Fund for the City of Thomasville for the Year Ended

December 31, 2015 .

37) A fund that exists when a government is the trustee for a defined benefit pension

plan, or a defined contribution pension plan is a(n):

A)Agency fund

B)Private-Purpose Trust Fund

C)Investment Trust Fund

D)Pension Trust Fund

38) During the fiscal year ended December 31, 2015, the City of Johnstown issued 6%

general obligation serial bonds in the amount of $2,000,000 at 102 ($2,040,000) and

used $1,980,000 of the proceeds to construct a fire station. The $40,000 premium was

transferred to a debt service fund. The $20,000 left in the capital projects fund at the

end of the project was later transferred to the debt service fund. The bonds were dated

April 1, 2015 and paid interest on October 1 and April 1 . The first of 10 equal annual

principal payments was due on April 1, 2016 .

How would the government account for the transfer of the unused bond proceeds?

A)As a revenue in the debt service fund and as an expenditure in the capital projects

fund

B)As an other financing source in the capital projects fund and as an other financing use

in the debt service fund

C)As an other financing source in the debt service fund and as an other financing use in

the capital projects fund

D) As a special item in both the debt service and capital project funds

39) A performance indicator is required in the Statement of Operations for health care

entities. Which of the following must be reported below that performance indicator?

A)Other revenue, such as parking lot or cafeteria revenue

B)Net assets released from restrictions for operating purposes

C)Both (a) and (b) above

D)Neither (a) nor (b) above

40) When should unconditional pledges be recorded as revenue?

A) Never

B) When money is received

C) When the pledge is made

D) When full collection is assured

41) Which of the following organizations does not follow the

A)Political parties

B)Voluntary health and welfare organizations

C)City libraries

D)Private foundations

42) Debt service expenditures for interest are:

A) Accrued

B) Recorded when due but may be accrued at year end if the debt service due date is

less than 30 days after year end

C) Recorded when due but may be accrued at year end if the debt service due date is

less than 60 days after year

D)Reported only in the government-wide statements

43) The GASB sets accounting standards for all of the following except:

A)State and local governments

B)Component units owned or controlled by governments

C)Governmentally related not-for-profit universities

D)Nongovernmental not-for-profit hospital

44) What are the reporting options for the Statement of Financial Position of institutions

of higher education as outlined by the NACUBO Financial Accounting and Reporting

Manual for Higher Education?

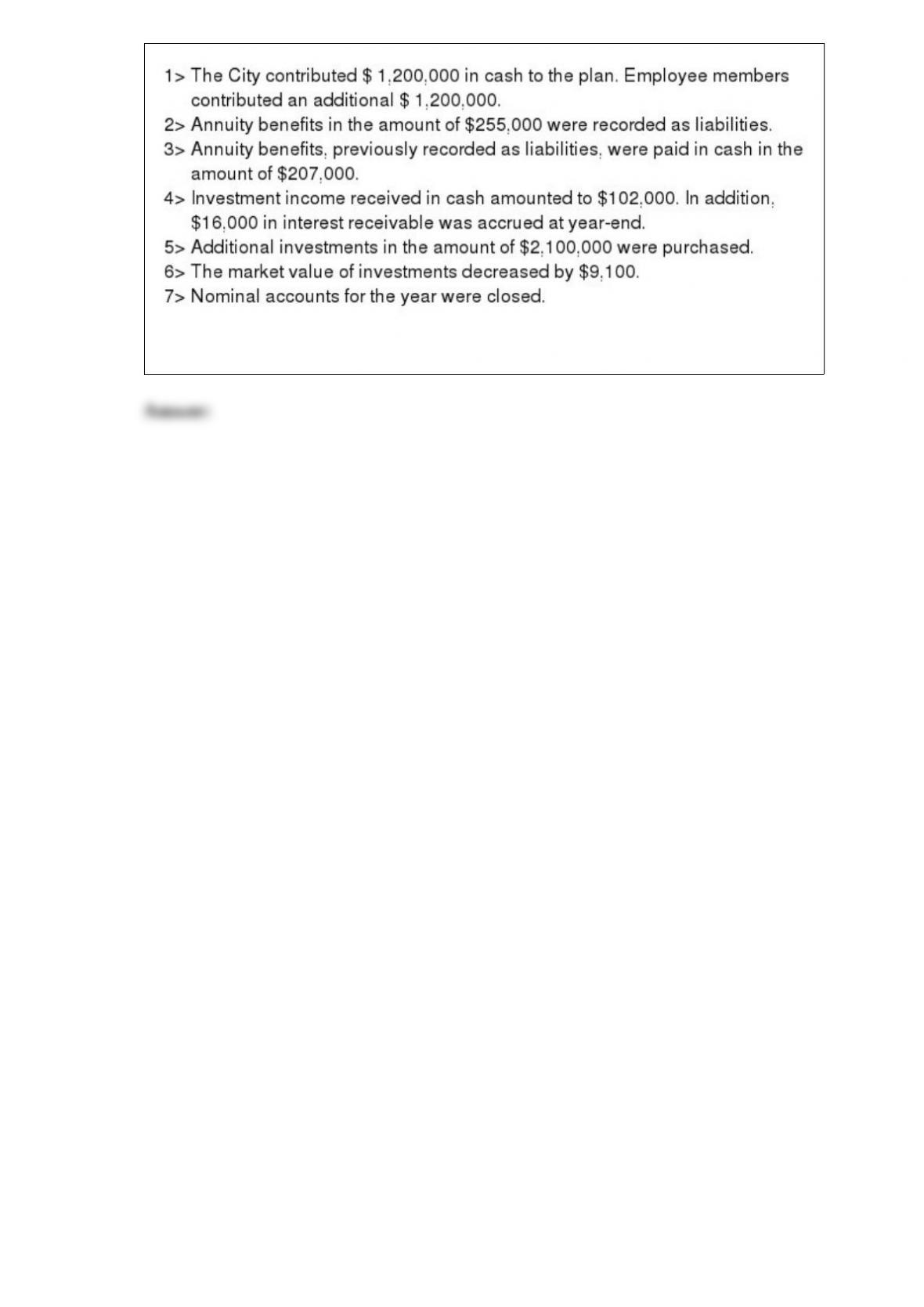

45) The City of Richmond maintains a Public Employee Retirement Trust Fund for its

public safety employees. During the year ended June 30, 2015, the following

transactions occurred:

Required: Prepare journal entries for the above transactions on the books of the City of

Richmond Public Safety Employee Retirement Trust Fund.

46) Why is Service Efforts and Accomplishments reporting especially important for

governmental and not-for-profit entities?

47) What are the required statements and schedules for a pension trust fund and in what

part of the CAFR are the schedules reported?

48) When might it be appropriate for a not-for-profit organization to report a surplus

(increase in net assets)?

49) What is the difference between an extraordinary and special item?

50) With regard to the government-wide statements, distinguish between program

revenues and general revenues. List three examples of each. What is the difference in

reporting between program revenues and general revenues?

51) Ballard University, a private not-for-profit, billed four students for tuition and fees

each in the amount of $ 8,000 each for fall semester. The University estimates 25% of

tuition and fees will prove to be uncollectible. The University collected $ 10,000 as

follows:

Required: Prepare the journal entries to record the billing and subsequent collection or

write-off for the transactions listed above.

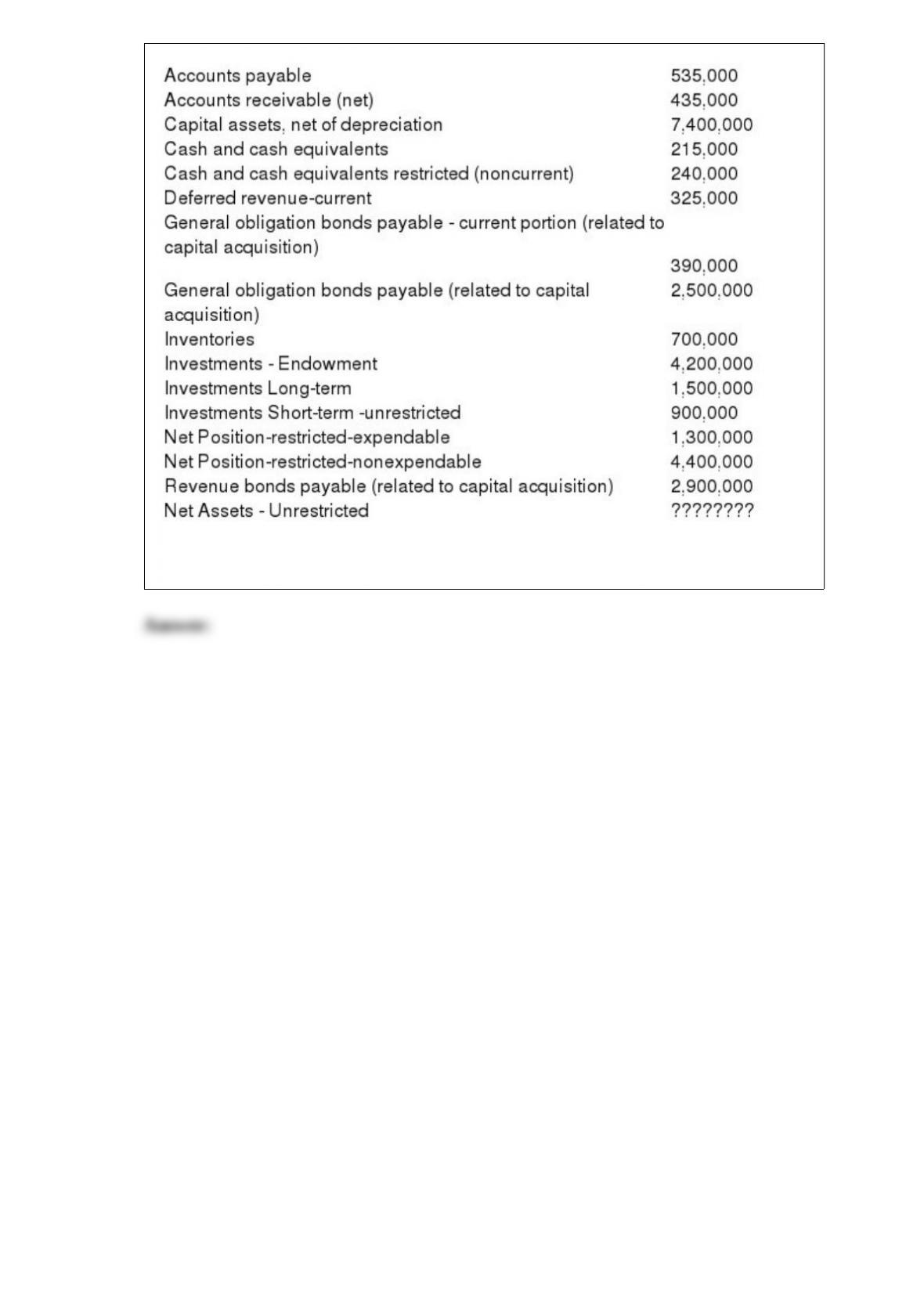

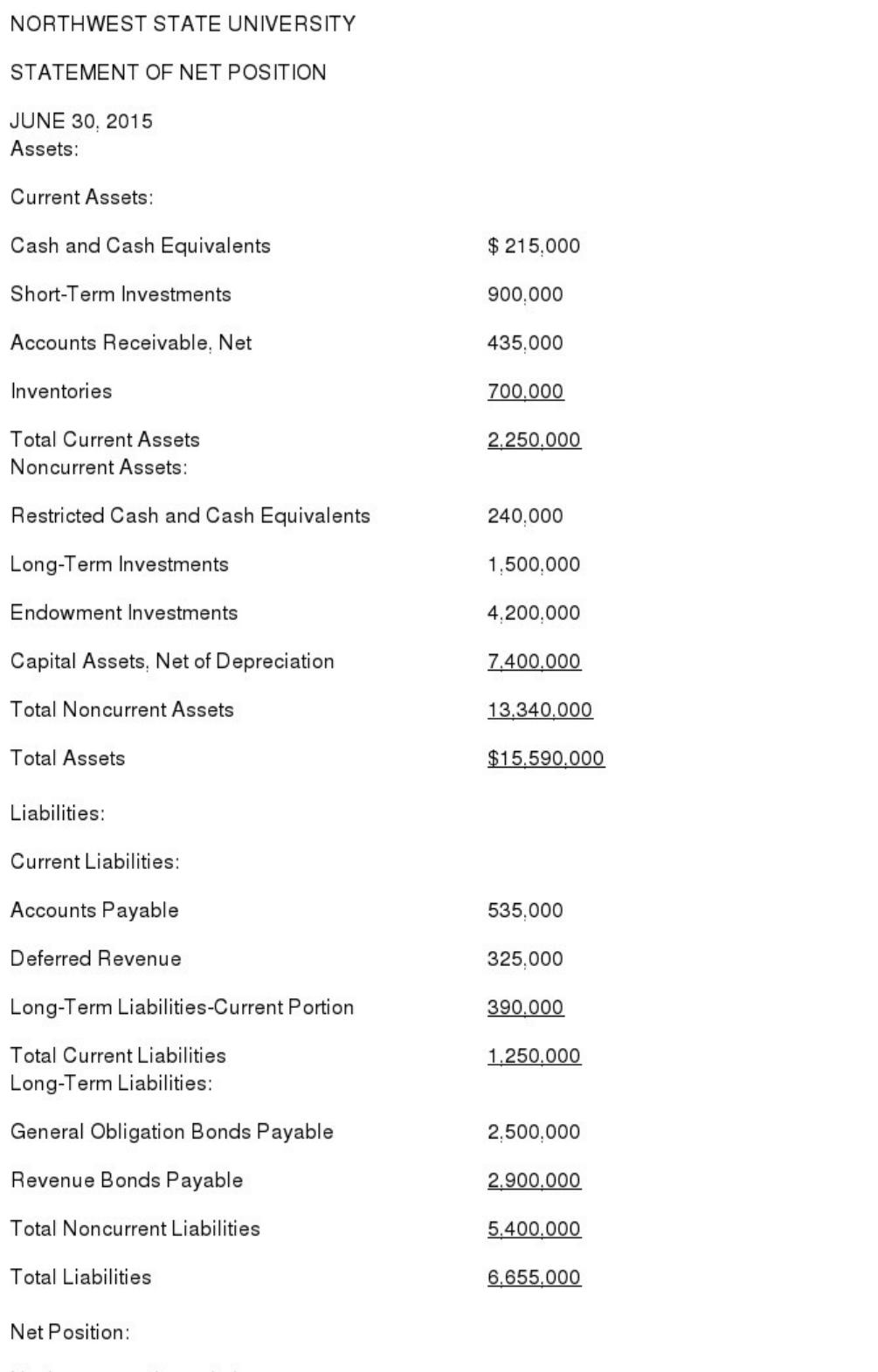

52) Northwest State University had the following account balances as of June 30,

2015 . Debits are not distinguished from credits, so assume all accounts have a normal

balance (i.e. cash is a debit and accounts payable a credit)

Required: Prepare, in good form, a Statement of Net Position for Northwest State

University as of June 30, 2015 .

53) What is the distinction between discounts and expenses for private colleges and

universities?