1) The government-wide financial statements present the government as a whole,

including component units and including fiduciary activities.

2) Special-purpose governments generally provide a limited set of services or programs.

3) A non exchange transaction is one where a government receives resources without

giving equal value in return.

4) Funds that are restricted for a certain number of years and then released are

considered to be quasi-endowments and are classified as temporarily restricted fundsby

private colleges and universities.

5) Tax-exempt organizations are required to disclose the compensation of its officers,

directors, trustees, highest paid employees and independent contractors in the Form 990

.

6) Private not-for-profit organizations record depreciation expense.

7) The excess of assets over liabilities of proprietary funds is termed Net Position.

8) Long term debt serviced from proprietary funds is reportedonly in

thegovernment-wide Statement of Net Position.

9) $200,000 to be used to fund government operations in the future from the General

Fund is an example of an unassigned fund balance.

10) Depreciation on capital assets is included as an expense in the Statement of

Activities in the governmental fund statements.

11) According to the rules for accounting for colleges and universities under the

jurisdiction of the FASB, contributed services should be recognized when the services

create or enhance nonfinancial assets or require specialized skills, are provided by an

individual possessing those skills, and would typically be purchased if not provided by

donation.

12) GASB requires that the budgetary basis of accounting for the General Fund used in

the Budget-Actual Comparison Schedule be on the same modified accrual basis as the

governmental fund Statement of Revenues, Expenditures and Changes in Fund Balance.

13) If a tax-exempt organization is found by the IRS to have paid unreasonable benefits,

the individual must pay a tax penalty of 25% of the excess benefit and the individuals

who approved the benefits must pay a 10% penalty.

14) When using the modified approach to record infrastructure, expenditures to widen a

2-lane road to 4-lanes would be charged to an expense, in lieu of depreciation.

15) A non-expendable trust which benefits a government or its citizenry and which

stipulates that earnings only (not principal) may be used for its prescribed purpose

would be reported in a Special Revenue Fund.

16) According to the rules for accounting for colleges and universities under the

jurisdiction of the FASB, investments in stock with determinable fair values and all debt

securities are reported at market value.

17) The General Fund of the City of Lexington approved a tax levy for the calendar

year 2015 in the amount of $2,000,000. Of that amount, $30,000 is expected to be

uncollectible. During 2015, $1,750,000 was collected. During 2016, $100,000 was

collected during the first 30 days, $50,000 was collected during days 31-60, and

$70,000 was collected during the days 61-90 . During the post-audit, you discovered

that the City showed $2,000,000 in revenues. How much revenue should the City

recognize in 2015 from this tax levy?

A)$ 1,850,000

B)$ 1,900,000

C)$ 1,920,000

D)$ 2,000,000

18) Which of the following is True regarding the Balance Sheet of a federal agency?

A)The balance sheet is prepared using the economic resource measurement focus and

accrual accounting

B)Assetsare measured on the modified accrual basis

C)The difference between assets and liabilities is termed Net Assets

D)Assets are separated between current and noncurrent

19) Revenue bonds sold by a water utility fund, upon sale, would be recorded:

A)In an enterprise fund as Other Financing Source

B)In the general long-term debt accounts as a liability

C)In an enterprise fund as a liability

D)In an enterprise fund as an addition to Net Position

20) GASB requires which of the following to be reported separately after other

financing sources and uses in the Statement of Revenues, Expenditures, and Changes in

Fund Balance?

A)Special items

B)Extraordinary items

C)Inter fund transfers

D) A and B

21) Which of the Fiduciary Funds listed below is used to account for the assets held by

a government acting as an agent for one or more other governmental units?

A)Private-purpose Trust Fund

B)Permanent Fund

C)Pension Fund

D)Agency Fund

22) Which of the following is True regarding revenue recognition for health care

organizations?

A)Patient service revenues are reported net of contractual adjustments

B)Revenues do not include charity care

C)Revenues may include fees for parking, cafeteria sales, and gift shops

D)All of the above are True

23) Lisa informed her church that she had named the church in her will and later

provided a written copy of the will to the church. At what point should the church

record the contribution?

A)At the time when the church was informed of her will

B)At the time the church receives a written copy of the will

C)At the date the probate court declares the will valid following her death

D)At Lisas death

24) The equity section of the balance sheet for investor-owned colleges and universities

includes which of the following designations?

A) Unrestricted Net Assets, Temporarily Restricted Net Assets, and Permanently

Restricted Net Assets

B) Paid in Capital and Retained Earnings

C) Net Investment in Capital Assets, net of related Debt; Restricted Net position; and

Unrestricted Net position

D) None of the above

25) Which of the following is True regarding component units?

A)Component units may be reported discretely in the government-wide statements or

may be blended as a fund in the fund financial statements (and thus also included in the

government-wide financial statements)

B)Component units could include towns, school districts, counties, and municipalities

C)Both of the above

D)Neither of the above

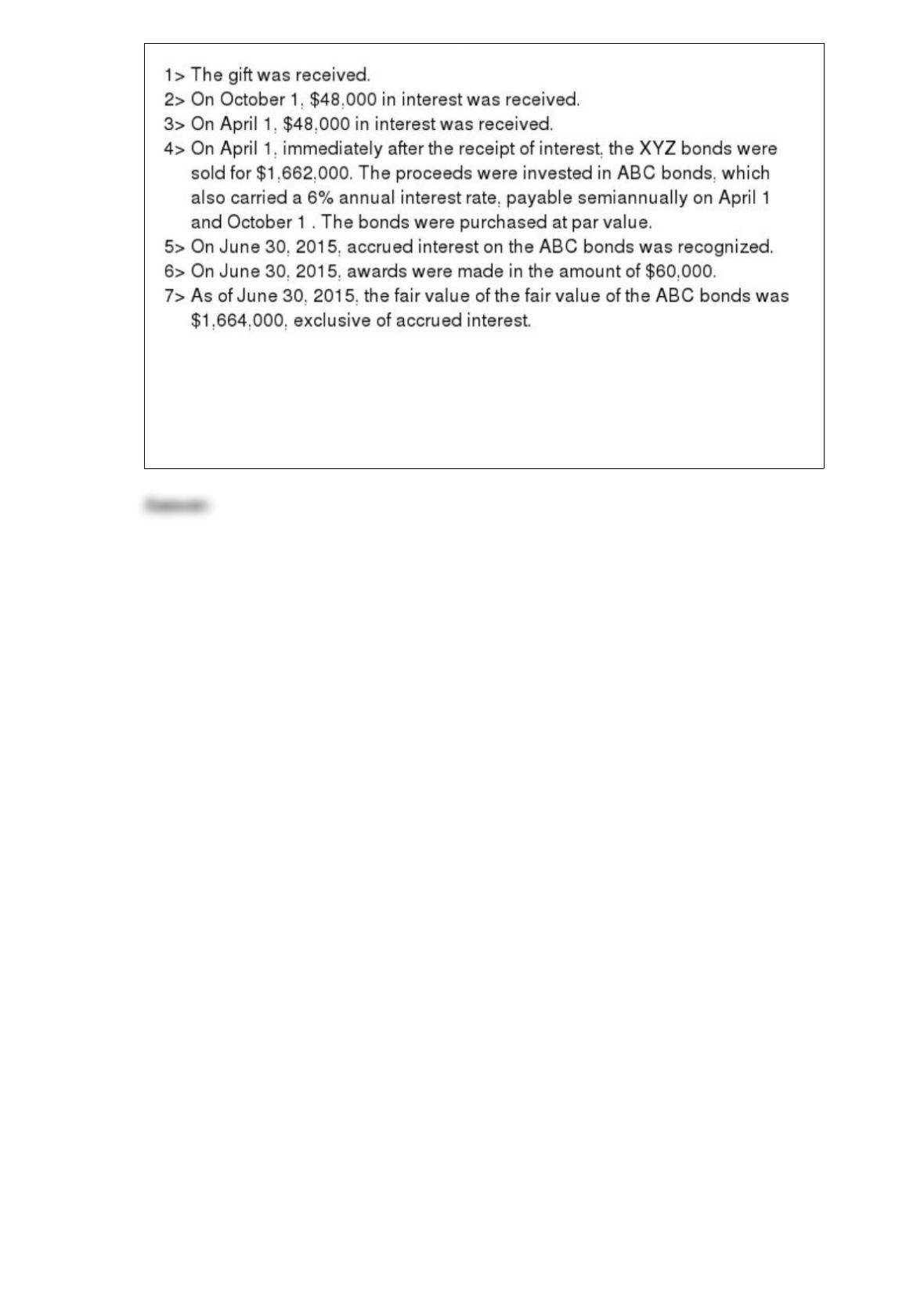

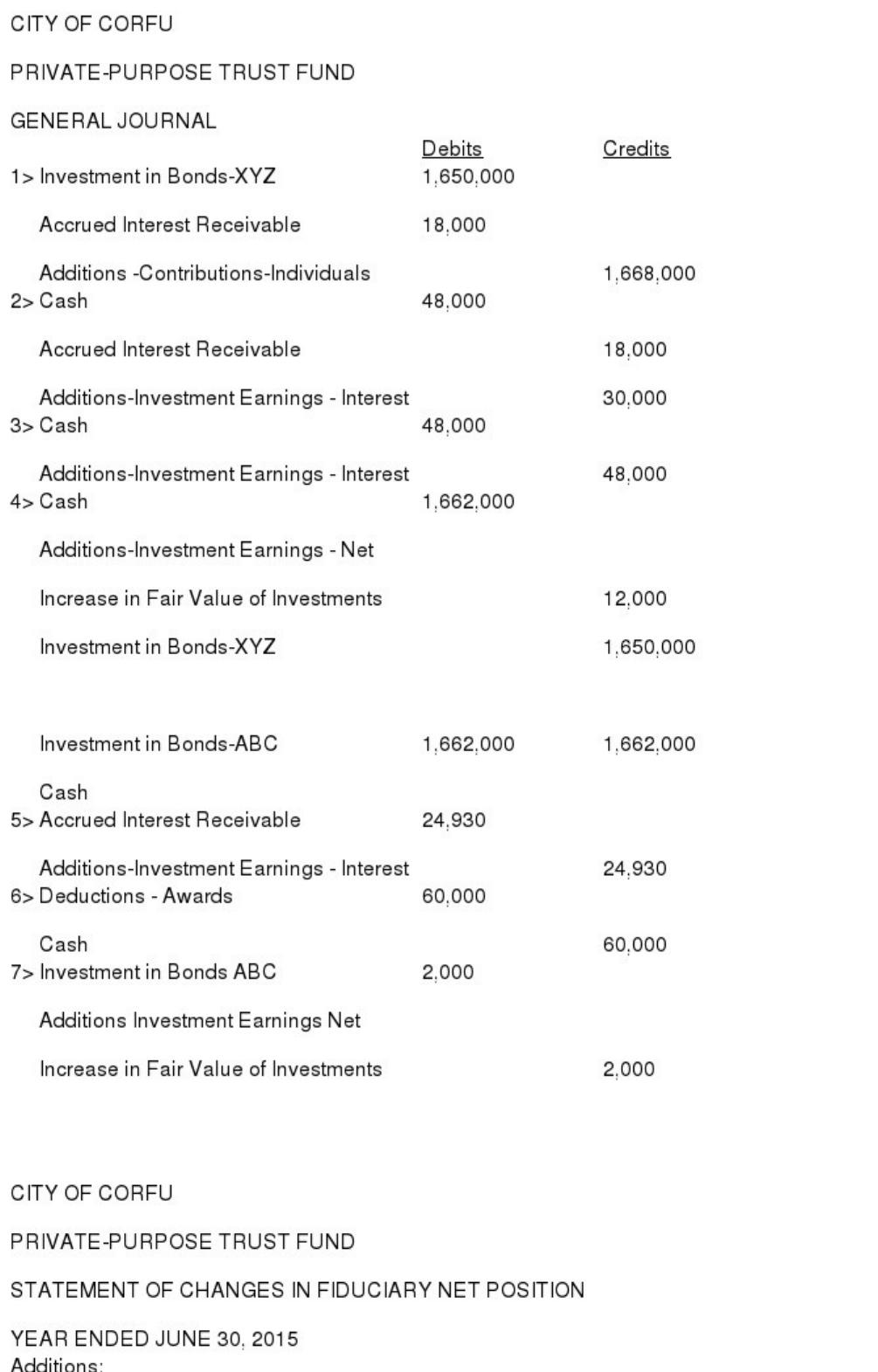

26) On July 1, 2014, the City of Corfu received a gift of debt securities of XYZ

Company with a nominal (par) value of $1,600,000. Income is to be used to make

awards for civic achievements. As of the date of the gift, the securities had a market

value of $1,668,000. Included in this amount is accrued interest of $18,000. The bonds

carried an annual interest rate of 6%, payable semiannually on April 1 and October 1 .

During the fiscal year ended June 30, 2015, the following transactions took place:

Required:

A.Record the above transactions on the books of the City of Corfu Private-Purpose

Trust Fund.

B.Prepare a Statement of Changes in Fiduciary Net Position for the City of Corfu

Private-Purpose Trust Fund for the year ended June 30, 2015 .

27) The ___________ is the governments official annual report prepared and published

as a matter of public record.

A) comprehensive annual financial report

B) governmental annual financial report

C) independent auditors report

D) complete audited financial report

28) Which of the following is True regarding the proprietary fund financial statements?

A)Statements include the Statement of Net Position, Statement of Revenues, Expenses,

and Changes in Fund Net Position, and Statement of Cash Flows

B)Normally, a reconciliation is required between the proprietary fund financial

statements and the business-type activities column in the government-wide financial

statements

C)The Statement of Net Position reflects equity as contributed equity and retained

earnings

D)The Statement of Cash Flows may be prepared using either the direct or indirect

methods

29) Which of the following is not likely to be recorded in a special revenue fund?

A)Phone fees restricted to supporting the emergency 911 access system

B)Hotel taxes restricted to promoting tourism

C)Sales taxes restricted to courthouse additions

D)State motor fuel tax restricted to road maintenance

30) The city of Canandaiguareceives proceeds from the sale of land, the transaction is

considered to be a special item. The proceeds are:

A)Reported separately after other financing sources and uses

B)Reported as a revenue

C) Reported as an item that changes the Fund Balance

D)Not recorded but the gain on the sale is

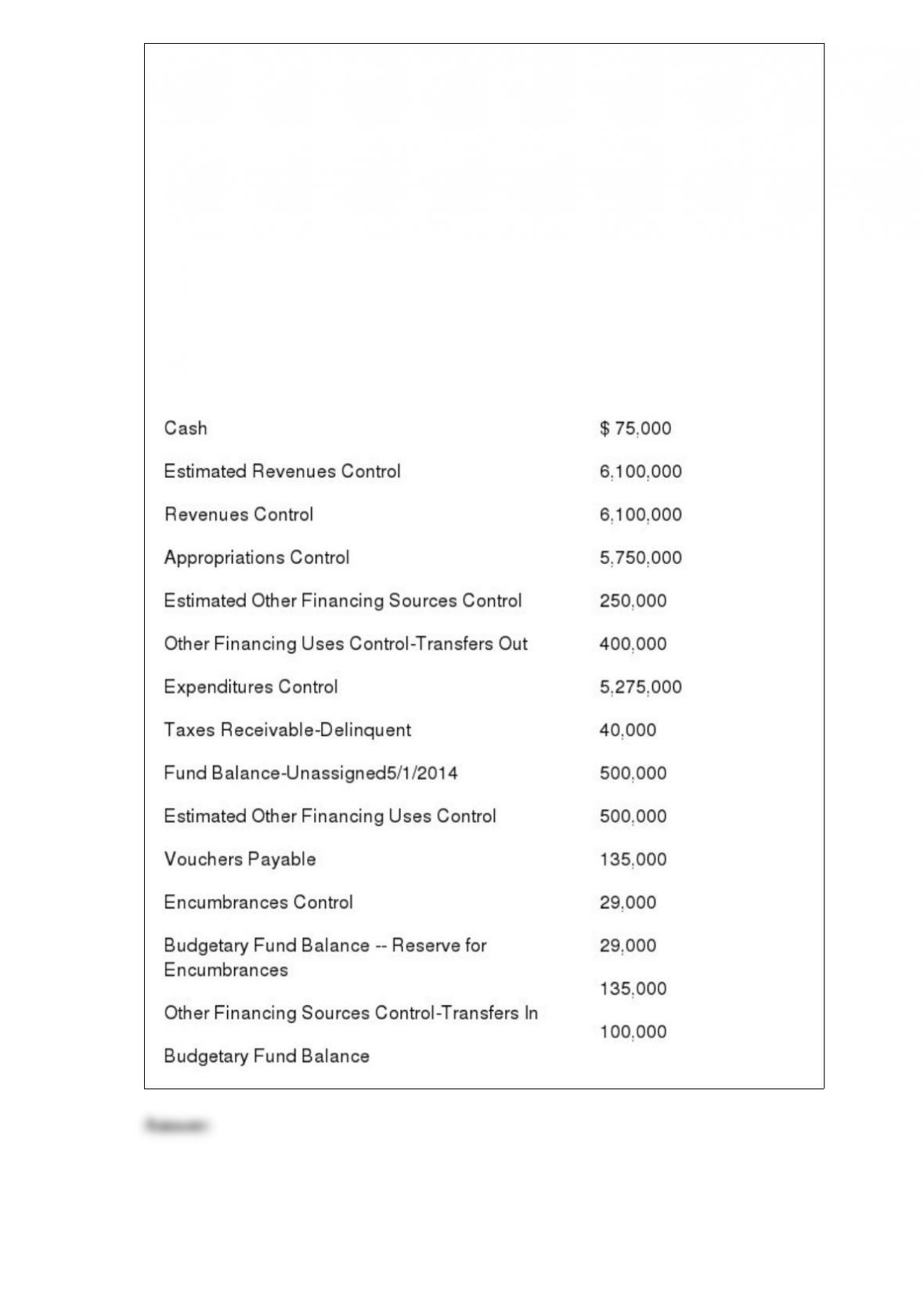

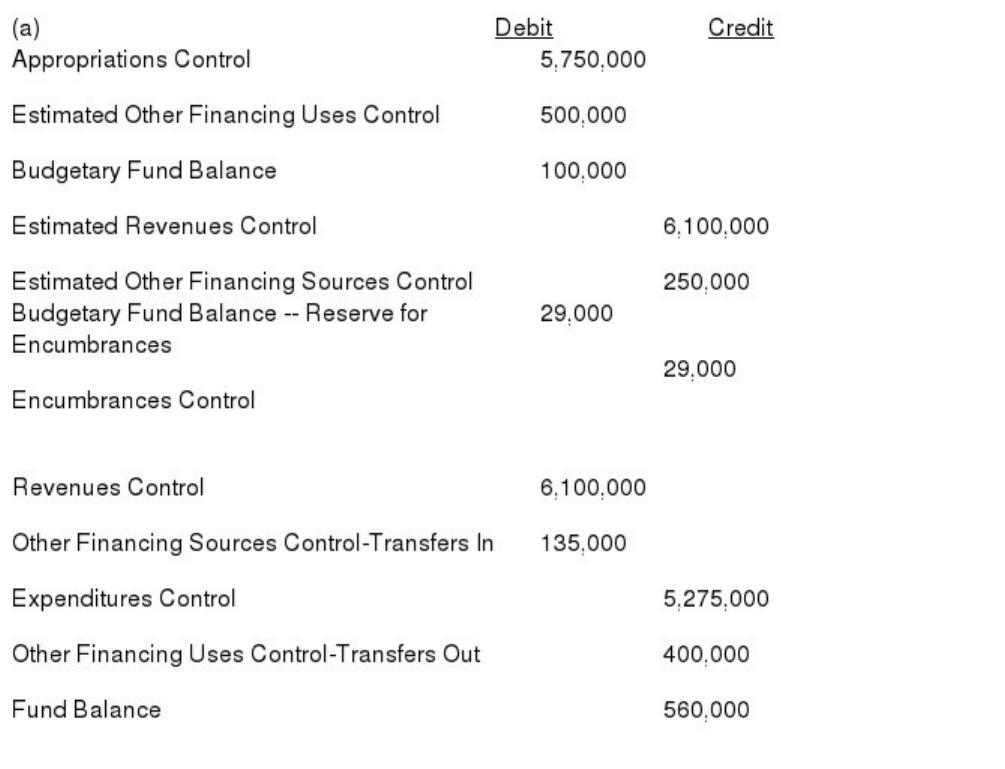

31) The City of Morganville had the following pre-closing account balances in its

General Fund as of April 30, 2015 . Debits and credits are not separated; each account

had its normal balance. Among the expenditures recorded this year is an amount

expended on supplies ordered at the end of the previous year. Assume that

encumbrances do not lapse and that the City failed to make the journal entry(s)

necessary to re-establish the encumbrance in the current year.

Required:

(a)Prepare all entries necessary to close the General Fund of the City of Morganville.

(b)Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for

the General Fund for the City of Morganville for the Year Ended April 30, 2015 . End

with the ending fund balance. This is the GAAP operating statement.

32) Which of the following organizations wouldnotbe subject to the accounting and

reporting requirements of FASB Statements 116 (Accounting for Contributions) and

117 (Financial Reporting for Not-for-Profit Organizations)?

A)The City of Hannibal Missouri

B)St. Jude Childrens Hospital

C)Live Arts Theater

D)Girl Scouts

33) Which of the following is part of the treatment of multi-year pledges as required by

FASB Statement No. 116?

A)The donation is recorded as a receivable at the present value of the future collections

but revenue is not recorded until the pledge is received

B)At the end of each accounting period, the difference between the balance in the

receivable account and the new present value is deducted from the amount of the

amount received from the donor which is recorded as income

C)At the end of each accounting period, the difference between the balance in the

receivable account and the new present value is recorded as contribution revenue and

the receivable is increased

D)Pledge receivable is recorded for the total amount to be received and revenue is

recorded each year as monies are received by the organization

34) The NACUBO Financial Accounting and Reporting Manual treats estimates of

uncollectible student accounts as:

A)A reduction in tuition and fee revenue

B)Bad debt expense

C)Either bad debt expense or a reduction in tuition and fee revenue as long as the policy

is consistently applied

D)None of the above; colleges and universities must use the direct write off method

35) A transaction in which a government receives resources without directly giving

equal value in exchange is known as a(n):

A) Equity Transaction

B) Fair Exchange.

C) Non-exchange Transaction

D) Not Fair Market Exchange transaction

36) The journal entry to record the prior years deferred Inflows: property taxes (those

expected to be collected more than 60 daysbeyond year-end) as revenue in the current

year would include:

A)A debit to Revenues Control

B)A debit to Deferred Inflows: Revenues

C)A credit to Revenues Control

D)B and C would both be included in the journal entry

37) The City of Smithfield levied property taxes in and for 2015 in the amount of $300

million. It is estimated that 1% will be uncollectible. During 2015, $280 million was

collected, and $12 million was collected during the next 60 days. Smithfield recognizes

the maximum possible property taxes in its governmental funds. The adjustment, when

moving from the governmental funds changes in fund balances to the governmental

activities change in Net Position would be:

A)$2 million increase

B)$2 million decrease

C)$5 million increase

D)$5 million decrease

38) Which of the following General Fund accounts would be closed at year end?

A) Due from State Government

B)Special Items Proceeds from Sale of Land

C)Taxes Receivable Delinquent

D) Deferred Inflows Property Taxes

39) Identify the primary financial reporting body for each of the following forms of

college or university

A.Private not-for-profit

B.For Profit – Investor owned

C.Public government owned

40) Which of the following is notcorrect with respect to the reporting of expenses for a

private not-for-profit?

A)Expenses can be reported in the unrestricted net asset class or restricted net asset

class, as appropriate

B)Expenses are reported by function in the Statement of Activities or in the notes

C)The FASB describes functions as either program or supporting

D)Major program classifications should be shown in the Statement of Activities or in

the notes

41) Which of the following is True regarding pension (and other employee benefit)

trust funds?

A)The actuarially computed Net Pension Liability is reported in the Statement of

Fiduciary Net Position

B)While full accrual accounting is used, the terms additions and deductions are used in

the Statement of Changes in Fiduciary Net Position in lieu of revenues and expenses

C)Both of the above

D)Neither of the above

42) A public college had tuition and fees of $21,000,000. Scholarships, for which no

services were required, amounted to $2,500,000. Graduate assistantships, for which

services were required, amounted to $1,600,000. The amount to be reported by the

public college as net tuition and fees would be:

A)$21,000,000

B)$19,400,000

C)$18,500,000

D)$16,900,000

43) Which of the following is(are) accurate regarding a federal agencys Statement of

Changes in Net Position?

A)The statement starts with the beginning of year balances in the net position accounts

and reconciles these to the ending balances appearing on the agencys Balance Sheet

B)The statement does not report Appropriations Received since this is a budgetary

account and does not affect net position

C)Both (a) and (b) above

D)Neither (a) nor (b) above

44) Which of the following statements regarding serial bonds is False?

A)The principal on serial bonds is paid over the term of the bonds

B)The assets of a debt service fund may include Cash with Fiscal Agent

C)If the first payment is delayed for more than a year with equal payments thereafter,

the bonds are deferred serial bonds

D)The principal repayment on an annuity serial bonds decreases each year as the

outstanding balancedecreases

45) Which of the following funds require a Statement of Cash Flows?

A) Governmental funds

B)Proprietary funds

C)Fiduciary Funds

D)Governmental and Fiduciary Funds

46) Governmental funds include:

A)Special revenue funds

B)Internal service funds

C)Debt service funds

D)A and C

47) Which of the following would not be considered a special-purpose government for

financial reporting purposes?

A)A public school system

B)An art museum

C)A public hospital

D)A county board of supervisors

48) Revenues in governmental fund accounting

A) include taxes, fees, resources provided by other governments, and interfund transfers

B)are recognized when earned

C)are recognized in the fiscal year they are available for expenditure

D) none of the above describes revenues in governmental accounting

49) Reciprocal inter fund activity:

A)Does not include inter fund loans

B)Is the internal counterpart to exchange transactions

C)Includes inter fund transfers

D)None of the above

50) Which of the following factors, if present, would indicate that a transaction is not a

contribution?

A)The resource provider received value in exchange

B)The resource provider entered into the transaction voluntarily

C)The transfer of assets was unconditional

D)The organization has discretion in the use of the assets received

51) Care Foundation is a voluntary health and welfare organization funded by

contributions from the general public. Care sold equipment for $30,000 which cost

$40,000 and had a book value of $25,000 at the time of sale. In recording the sale, Care

should:

A)Record temporarily restricted revenue of $ 30,000

B)Record a gain of $ 5,000

C)Record a loss of $10,000

D)None of the above

52) Identify the standard setting body for private not-for-profit organizations and the

basis of accounting that should be used.

A) GASB & Accrual

B) GASB & Modified Accrual

C) FASB & Accrual

D) FASB & Modified Accrual

53) A donor pledged $500,000 to a not-for-profit hospital in 2014 to conduct medical

research, conditional on the hospital raising $500,000 from other donors. The other

donors met the condition in 2015. The donor transferred the funds to the hospital in

2015 . In which year would the revenue be recognized?

A)2014

B)2015

C)Half in 2014 and half in 2015

D)None of the above; the hospital would only recognize revenue when the amounts had

been expended according to the donor’s wishes

54) A)Governmental Accounting Standards Board

B)Financial Accounting Standards Board

C)Hospital Financial Management Association

D)American Institute of Certified Public Accountants

55) The General Fund of the City of X passed a budget, providing for $2,000,000 in

anticipated revenues and $1,990,000 in anticipated expenditures. The journal entry(s)to

record the budget would result in a:

A)credit to Appropriations Control in the amount of $1,990,000

B)debit to Estimated Revenues Control in the amount of $2,000,000

C)credit to Budgetary Fund Balance in the amount of $10,000

D)all of the above

56) At year-end, the balance of Expenditures, Revenues and Other Financing Sources

and Uses accounts are closed to:

A) Budgetary Fund Balance

B) Expenses

C)Fund Balance

D)Expenditure Control

57) What are major programs with respect to the Single Audit Act of 1984 and

amendment of 1996? Distinguish between Type A and Type B programs.

58) What is the purpose of the Unrelated Business Income Tax?

59) What is the treatment of multi-year pledges as required by FASB Statement No.

116?

60) Special-purpose governments that are engaged in both governmental and

business-type activities or in more than one governmental activity are required to

include which items in its financial reporting?

61) Identify (in order of occurrence) the steps in the federal budgetary authority

process.

62) Assume a federal agency has the following events:

1>Receives a warrant from the Treasury notifying the agency of appropriations of

$12,000,000.

2>OMB apportions 1/4th of the appropriation for the first quarter of the year.

3>The Director of the agency allots $ 2,850,000 to program units.

4>Program units place orders $ 2,790,000.

5>Supplies ($ 490,000) and services ($ 2,291,000) are received and paid during the first

quarter. Supplies of $ 417,000 were used in the quarter.

Required: Prepare any necessary journal entries to reflect the events described above.

Identify whether the entry is budgetary or proprietary.

63) Distinguish between an exchange transaction and a contribution. How is the

accounting different for these two events?

64) Describe the different types of governmental audit and attestation engagements.

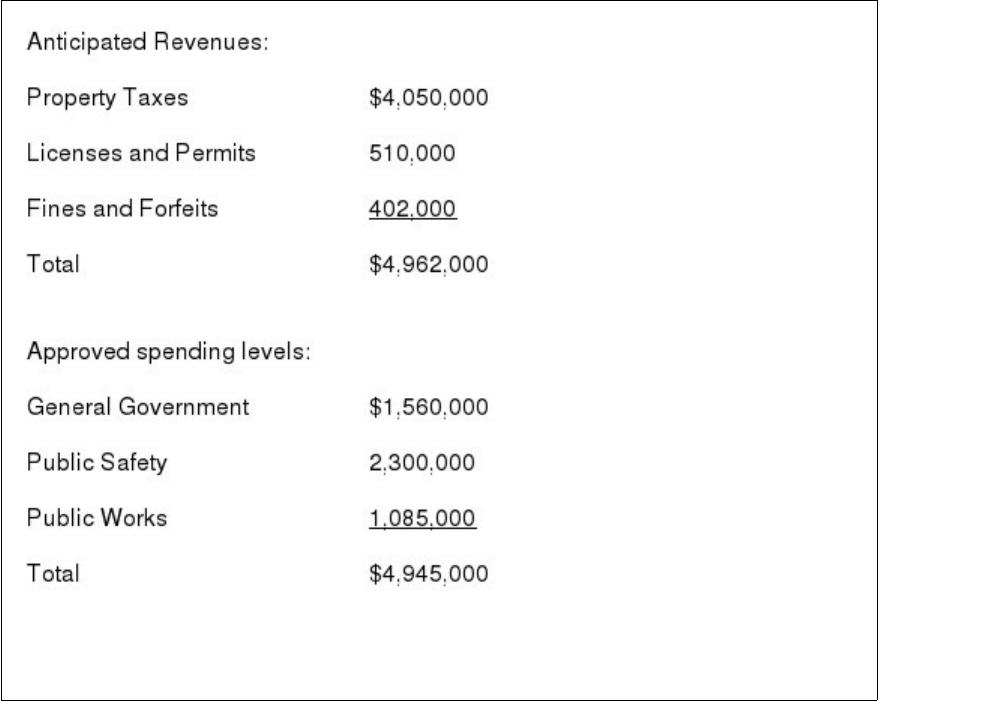

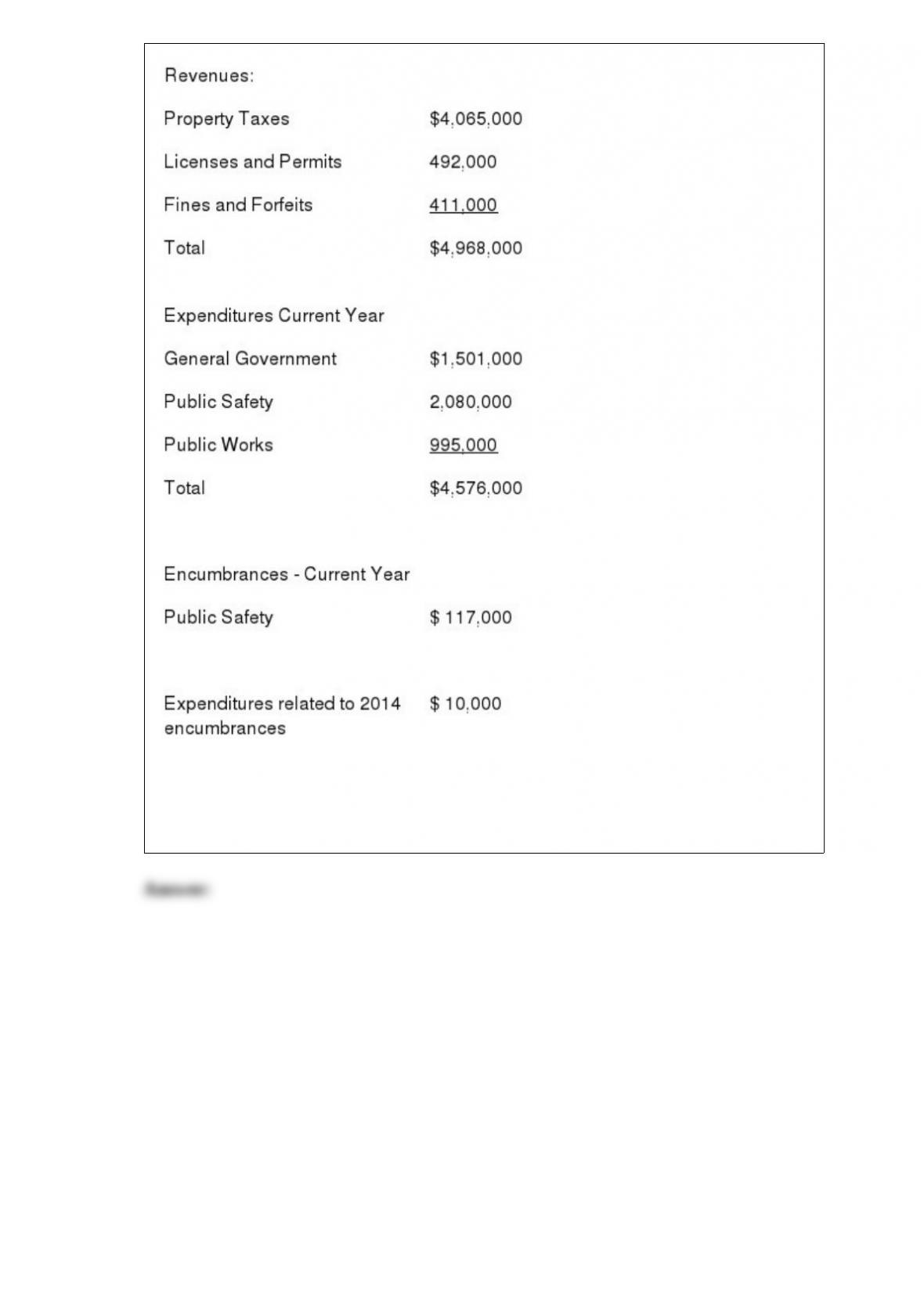

65) The City of Fairport adopted the following budget for fiscal year 2015:

In addition, the City reported the following actual amounts for the same fiscal year.

Required: Prepare a budgetary comparison schedule for the City for the year ended

December 31,2015 assuming the fund balance of the General Fund(budgetary basis)

was $627,000 at January 1, 2015 . No “original budget” column is required. Include a

“variance” column.