1) An investment trust fund is used to account for the internal portion of a

multi-government investment pool, when the reporting government is trustee.

2) Long term liabilities of an enterprise fund are reported in the proprietary fund

statement and in government-wide statements.

3) The GASB Concept Statement on Service Efforts and Accomplishments Reporting

encourages state and local governments to include inputs of nonmonetary resources in

their financial reporting.

4) The journal entry to record a purchase order in the General Fund would be a debit to

encumbrances control account and credit Accounts Payable

5) Comparison of the legally approved budget with actual results of the General Fund is

not part of required supplementary information in the CAFR.

6) The

7) Fiduciary Fund activities report in terms of Additions and Deductions.

8) Proprietary Funds use the accrual basis of accounting.

9) Service Efforts and Accomplishments Reporting is mandatory for government

organizations.

10) Expenditures, encumbrances, and budgetary accounts are used by private

not-for-profit organizations.

11) The cash flow statements of private health care organizations, both not-for-profit

and for-profit, may use only the indirect method.

12) Capital assets constructed by an internal service fund are recorded in a capital

projects fund.

13) Health care organizations that are privately owned and operated to provide a return

to investors follow which standards:

A) GASB

B) FASB, including standards specifically for not-for-profits

C) FASB, excluding standards specifically for not-for-profits

D) None of the above

14) The Township of Thomasvilles General Fund has the following net resources at

year end:

$77,000 of prepaid insurance

$375,000 rainy day fund approved by the township governing board with specific

conditions for its use

$2,500 of supplies inventory

$61,000 state grant for snow removal

$150,000 contractual obligations for the purchase of equipment

$200,000 to be used to fund government operations in the future

Outstanding encumbrance of $80,000 for the purchase of furniture & fixtures (assume

no contractual obligation)

What would be the total Assigned fund balance?

A)$ 61,000

B)$ 77,000

C)$ 80,000

D)$150,000

15) Which of the following is True regarding Government-wide financial statements?

A) Prior year data must be presented

B) A Statement of Cash Flows is not required for Government-wide statements

C) Depreciation may only be reported as a charge in total to the general government

D) Fiduciary activities are only reported if they qualify as a major fund

16) A governmental fund Statement of Revenues, Expenditures, and Changes in Fund

Balances reported expenditures of $30 million, including capital outlay expenditures of

$9 million. Capital assets for that government cost $90 million, including land of $10

million. Depreciable assets are amortized over 20 years, on average. The reconciliation

from governmental changes in fund balances to governmental activities changes in

would reflect a(an):

A)Decrease of $1 million

B)Increase of $l million

C)Increase of $5 million

D)Decrease of $4 million

17) Which of the following would not be correct with respect to accounting for colleges

and universities under the jurisdiction of the FASB?

A)If both unrestricted and restricted resources are available for a restricted purpose, the

FASB requires that the institution recognize the use of unrestricted resources first

B)Accrual accounting is used. Revenues and expenses are reported at gross amounts

and gains and losses are reported net

C)Expenses are reported by function, either in the statements or in the notes

D)If an institution decides not to capitalize museum and other inexhaustible collections,

note disclosures are required regarding the collections

18) Premiums generated from the issuance of bonds for a capital projects fund are

generally:

A)Transferred to the General Fund

B)Retained in the capital projects fund

C)Transferred to the debt service fund

D) None of the above

19) The term special item is defined as:

A)Unusual or infrequent but within managements control

B)Frequent and unusual but within managements control

C) Frequent and unusual and not within managements control

D) Unusual or infrequent and not within managements control

20) Which of the following is notTrue regarding accounting and financial reporting for

private not-for-profit hospitals?

A)Expenses may be unrestricted or temporarily restricted depending on donor intent

B)Fund accounting is not required

C)The Statement of Cash Flows may use either the direct or indirect method

D)Net assets are classified as Unrestricted, Temporarily Restricted or Permanently

Restricted

21) Which of the following is not an example of a special-purpose government?

A)Village government

B)Tollway authority

C)Library district

D)Fire protection districts

22) Which of the following would not need to be addressed/adjusted in compiling the

government-wide statements?

A)Principal repayment on proprietary fund bonds

B)Issuance of general obligation bonds

C) Inter fund transfers among governmental funds

D) Interest accrual on general obligation bonds

23) Where in the basic financial statements would one find fiduciary activities reported?

A)In the fiduciary funds statements and in the governmental activities column of the

government-wide statements

B)In the fiduciary funds statements and in the business like activities column of the

government-wide statements

C)In the fiduciary funds statements only

D)In the government-wide statements only

24) A county treasurer maintains an investment pool in which several different towns in

the county hold investments. Where should the towns investments be recorded?

A)Investment Trust Fund

B)Agency Fund

C)Private-purpose Trust Fund

D)None of the above

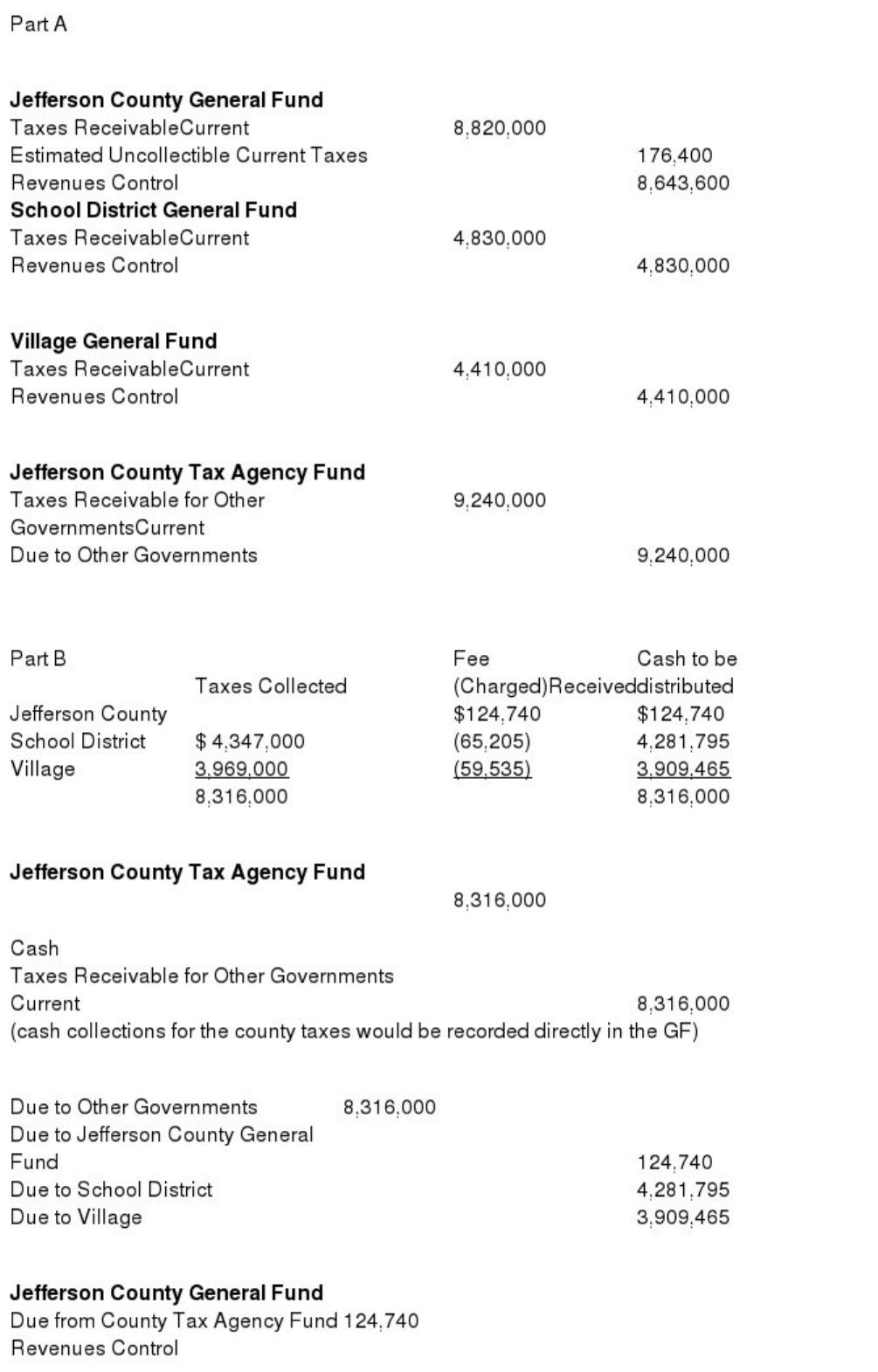

25) Jefferson County maintains a tax agency fund for use by the County Treasurer to

record receivables, collections, and disbursements of all property tax collections to all

units of government in the county. In the year 2015, the following taxes were levied:

1>$8,820,000 in property taxes were levied for the General Fund, of which 2% are

deemed to be uncollectible.

2>$4,830,000 in property taxes werelevied for the school district.

3>$4,410,000 in property taxes were levied for a village in the county.

Required:

A.Prepare the journal entries for each unit and the Agency Fund to record these levies.

B.The agency fund then collected 90% of the levy for each fund. The Jefferson County

General Fund charges 1.5% of collections as a fee for maintaining the agency fund.

Prepare the journal entries for each unit and the Agency Fund to record these

collections and fees.

26) Which of the following could be recognized as contributed services revenue by a

not-for-profit hospital?

A)A high school student class volunteered to answer the telephone during the Friday

night midnight shift

B)An architect developed building plans for a new outpatient clinic

C)Both (a) and (b) above

D)Neither (a) nor (b) above

27) When converting fund financial records to government-wide financial statements,

worksheet entries are made to eliminate all of the following accounts except:

A)Interest Payable

B) Bond Proceeds

C)Debt Service Expenditure – Principal

D)Capital Expenditures

28) Which of the following is correct with respect to Internal Service Funds?

A)Internal service funds use modified accrual accounting and the current financial

resourcesmeasurement focus

B)Net position is to be reported in two categories: assigned and unassigned

C)Internal service funds account for long-term debt but not capital assets

D)All of the above are False statements

29) Student scholarships for which no service was required were applied to student

accounts in the amount of $5,000. What is the journal entry to record this event?

A)Debit: Tuition discount-Unrestricted-Student aid $5,000 Credit: Accounts Receivable

$5,000

B) Debit: Scholarship Expense $5,000 Credit: Accounts Receivable $5,000

C) Debit: Tuition waiver $5,000 Credit: Loan to student $5,000

D) None of the above

30) Sales taxes, income taxes, and motor fuel taxes are examples of which class of non

exchange transactions?

A) Imposed non exchange transactions

B) Derived tax revenues

C) Government-mandated non exchange transactions

D) Voluntary non exchange transactions

31) Which of the following is not a reconciliation required by GASB?

A) From governmental fund balance sheet to the Government-wide Statement of

Net Position

B) From governmental fund Statement of Revenues, Expenditures, and Changes

in Fund Balances to the Government-wide Statement of Activities

C) From enterprise fund balance sheet to the Government-wide Statement of Net

Assets

D) None of the above, all these reconciliations are required

32) On October 1, 2014, the City of Mizner issued $4,000,000 in 4%, general obligation

bonds at 101 for the purpose of constructing an addition to City Hall. The premium was

transferred to a debt service fund. A total of $3,975,000 was used to construct the

addition, which was completed prior to June 30, 2015 . The remaining funds were

transferred to the debt service fund. The bonds were dated October 1, 2014, and paid

interest on April 1 and October 1 . The first of 20 annual principal payments of

$200,000 is due October 1, 2015 . The fiscal year for Mizner is July 1- June 30 .

How would the government account for the unused bond proceeds?

A)As a revenue in the debt service fund and as an expenditure in the capital projects

fund

B)As another financing source in the capital projects fund and as another financing use

in the debt service fund

C)As another financing source in the government-wide Statement of Activities

D)As another financing source in the debt service fund and as another financing use in

the capital projects fund

33) According to GASB 34, Enterprise funds must be used when:

A)Debt is backed solely by fees and charges

B)A legal requirement exists that the cost of providing services for an activity, including

capital costs, be recovered through fees or charges

C)A government has a policy to establish fees and charges to cover the cost of

providing services for an activity

D) Any of the above apply

34) Public sector audits differ from those of commercial businesses in which of the

following ways?

A)The auditor is not required to be independent

B)The auditor reports to outside agencies as well as management of the organization

C)The auditor does not use sampling

D)All of the above

35) Which of the following should appear within the equity (net position) section of a

federal agency balance sheet?

A)Net Position Unexpended Appropriations

B)Fund Balance with Treasury

C)Both (a) and (b) above

D)Neither (a) nor (b) above

36) A government had the following transfers reported in its governmental funds

Statement of Revenues, Expenditures, and Changes in Fund Balances: (1) a transfer

from the General Fund to a debt service fund in the amount of $l, 100,000; (2) a transfer

from the General Fund to an internal service fund in the amount of $1,300,000; and (3)

a transfer from the General Fund to a special revenue fund in the amount of $500,000.

The amount that would be shown as a transfer out in the governmental activities

column in the Statement of Activities would be:

A)$0

B)$1,300,000

C)$1,600,000

D)$2,400,000

37) Which of the following serial bonds has the first scheduled installment delayed for a

period of more than 1 year after the date of the issue?

A)Annuity Serial Bonds

B) Regular Serial Bonds

C) Irregular Serial Bonds

D) Deferred Serial Bonds

38) If taxes and/or special assessments are levied by the General Fund, and then are

subsequently transferred to the debt service fund, they are:

A)Recorded as revenues of the debt service fund

B)Included as transfers out in the General Fund but are not as revenue in that fund

C)Included in the revenues of the General Fund and are also reported by the General

Fund as transfers out to the debt service fund

D)Recorded as an expense and voucher payable by theGeneral Fundand are recorded as

a revenue and receivable by the debt service fund

39) Cash provided by the General Fund for a capital project would be recorded in a

capital projects fund as a (an):

A)Revenue

B)Other Financing Use

C)Direct addition to Fund Balance

D)Other Financing Source Transfer In

40) Which of the following is True regarding fiduciary fund statements?

A)Fiduciary fund statements include the Statement of Fiduciary Net Position and the

Statement of Changes in Fiduciary Net Position

B)Fiduciary fund statements are prepared using the current financial resources

measurement focus and modified accrual basis of accounting

C)Both of the above

D)Neither of the above

41) Which organization promulgates Statements of Federal Financial

AccountingStandards?

A)The American Institute of Certified Public Accountants

B)The Federal Accounting Standards Advisory Board

C)The U.S. Office of Management and Budget

D)The U.S. Government Accountability Office

42) Which of the following is not an objective of federal financial reporting?

A) Budgetary Integrity

B)Increase Taxpayer Awareness

C) Stewardship

D)Operating Performance

43) GASB No. 53 establishes reporting requirements for governments entering into

derivative instruments. What is the treatment of hedging vs. investment derivatives?

44) What are the four objectives that should be followed with respect to federal

financial reporting according to SFFAC #1 as issued by the FASAB?

45) What is a bond refunding and why do governments refund bonds?

46) On January 1,2015, the Town of Walton issued $ 5,000,000 of 4% tax supported

bonds. The bonds are dated January 1, 2015 with interest payment dates of June 30 and

December 31 . The first of 10 annual principal payments is due on December 31, 2015 .

The bonds were sold at a $48,000 premium that was transferred to the Debt Service

Fund from the capital projects fund to be used to fund the first payment. Cash sufficient

to cover interest and principal payments for the year less the premium is transferred

from the General Fund on June 1st.

Required: Record any and all entries to be made by the Debt Service Fund for the bond

issued for the year 2015 (including closing entries)

47) The Village of Lake Georges General Fund has the following net resources at

December 31, 2015

$5,000 of prepaid insurance

$ 25,000 of property taxes receivable currently due and expected to be collected within

60 days

$300,000 rainy day fund approved by the township governing board

$82,500 of supplies inventory

$33,000 government grant for city park maintenance

$10,000 contractual obligations for the purchase of park fixtures

$200,000 to be used to fund government operations in the future

Required: Prepare the fund balance section of the Balance Sheet

48) What are the fund-basis financial statements for each of the following fund

categories?

Fiduciary

Proprietary

Governmental

49) What are the four classes of nonexchange revenues?

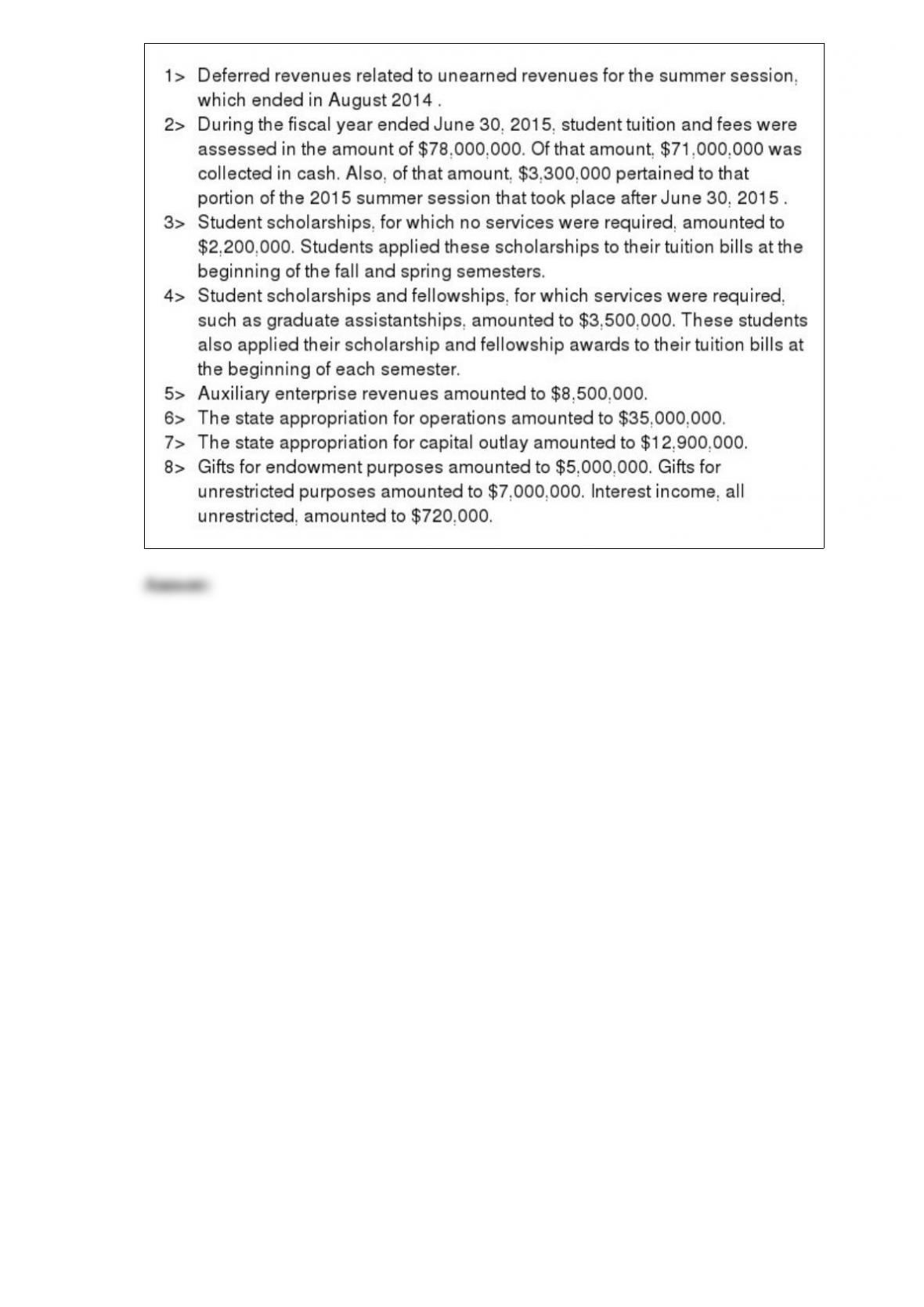

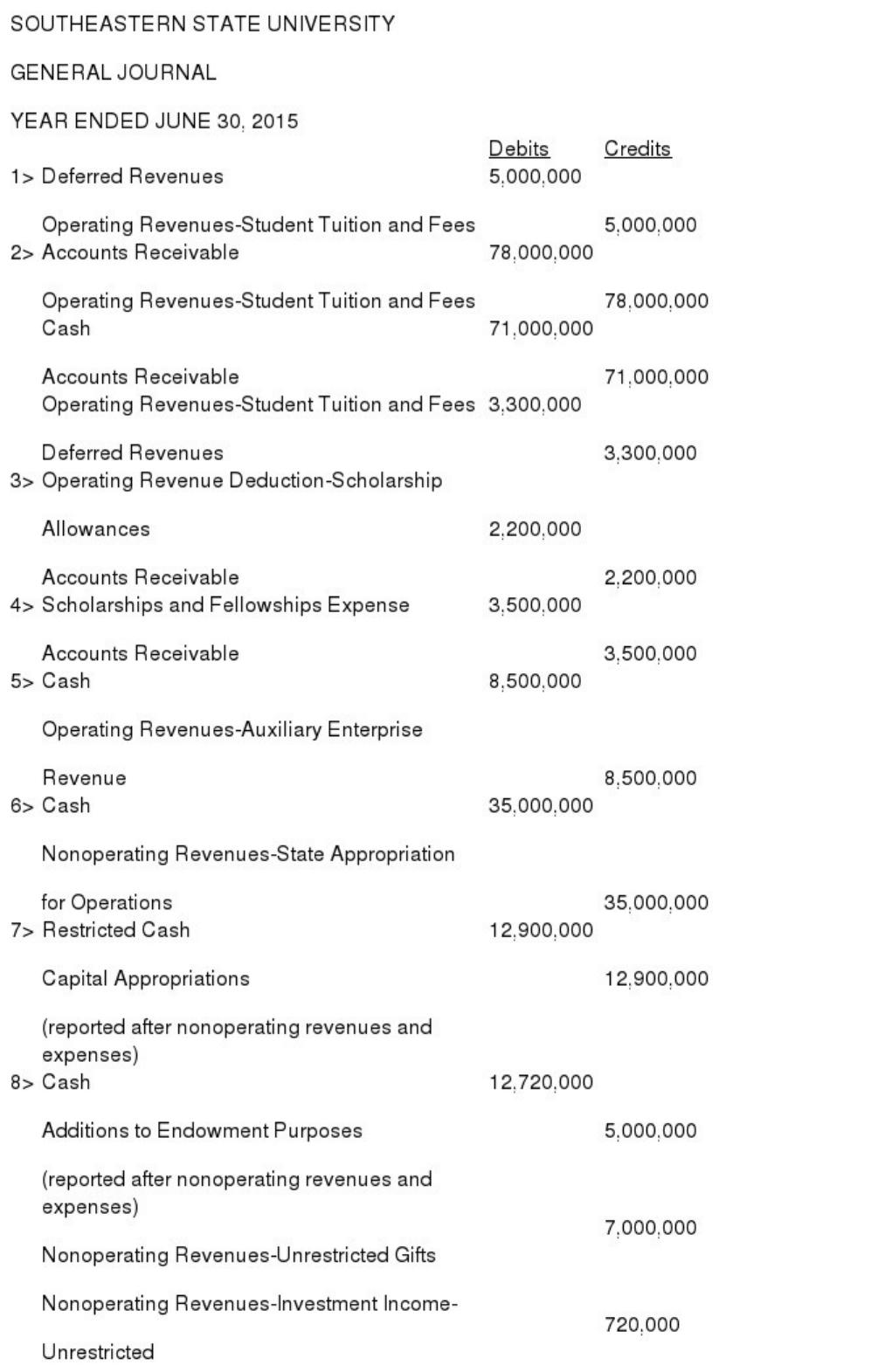

50) Southeastern State University has chosen to report as a public university reporting

as a special-purpose entity engaged only in business-type activities. Deferred Revenues

were reported as of July 1, 2014 in the amount of $5,000,000. Record the following

transactions related to revenue recognition for the year ended June 30, 2015 . Include in

the account titles the proper revenue classification (operating revenues, nonoperating

revenues, etc.):