1) According to the rules for accounting for colleges and universities under the

jurisdiction of the FASB, expenses are reported by function, either in the statements or

in the notes.

2) A Statement of Functional Expenses is not required for private voluntary health and

welfare organizations.

3) While the principal users of corporate audit reports are investors and creditors, the

main user of Single Audit reports is the federal government.

4) The program expense ratio for a not-for-profit organization will improve if the

organization shifts costs from fund-raising to administrative expenses.

5) Assuming an auditee is considered low-risk, the auditor is required to express an

opinion on compliance on major programs, which must add up to 25 percent of federal

funds expended by the auditee.

6) The Statement of Functional expenses presents a matrix of expenses classified by

function (various programs, fund-raising, etc.) and by object or natural classification

(salaries, supplies, travel, etc.).

7) Pension expenditures for governmental type funds are equal to the amounts paid to

the pension fund for current year service plus any accruals for amounts to be paid from

current financial resources.

8) The categories on the Statement of Changes in Fiduciary Net Position are Additions

and Deductions.

9) Capital assets are not reported in governmental funds.

10) Internal investment pools, which account for investments of the reporting entity, are

to be reported within the funds providing the resources, when preparing financial

statements.

11) The Governmental Accounting Standards Board considers the financial reporting

entity to include the primary government, but not its component units.

12) Unexpended intergovernmental grants and taxes dedicated to capital improvements

in a capital projects fund are likely to be classified as Committed Fund Balance

13) Rainy day funds are classified as restricted if they are created by a resolution or

ordinance that identifies the specific circumstances under which the resources may be

expended.

14) Fiduciary funds of a governmental unit use the current financial resources

measurement focus and modified accrual basis of accounting

15) Government owned hospitals follow FASB Statements 116 and 117 .

16) Public colleges and universities are (primarily) subject to financial reporting

standards issued by:

A) FASB

B) GASB

C)

D) None of the above

17) Which of the following statements regarding employer reporting of pension trust

funds is not correct?

A) Contributions by the governmental funds are recorded as expenditures in the

General Fund

B) The net pension liabilities are reported in the government-wide statements

C) The net pension liabilities of proprietary fund employees are reported in the

proprietary fund-basis statements

D) Governmental funds report net pension liabilities of governmental fund employees

as a fund liability

18) Which of the following events will result in a journal entry being recorded in both

the budgetary and proprietary accounts of a federal agency?

A)Treasury notifies the agency that Congress passed legislation (signed by the

President) granting budgetary authority to fund its activities

B)The agency places orders for goods or services

C)Both (a) and (b)

D)Neither (a) nor (b)

19) As of December 31, 2014, The Halifax Fishing Museum had unrestricted cash of

$52,000, building and land with a net book value of $145,000, and permanently

restricted collections totaling $ 105,000. There were no liabilities. The Museum has two

programs: Operation of a Fishing Museum and Educational Programs. During the year

ended December 31, 2015 the Museum incurred the following transactions:

(1)Cash contributions to the Museum included (a) unrestricted $ 512,000, (b) restricted

for educational programs $ 37,000 and (c) restricted by the donor for endowment

purposes $100,000.

(2)Additional unrestricted cash receipts included $ 29,000 in fees from individuals and

organizations using the Museum building as a meeting facility. Included in this is $

3,000 for a meeting to be held in January 2014 .

(3)Incurred cash expenses:

(4)Purchased land for future expansion to the adjoining lot in the amount of $ 35,000.

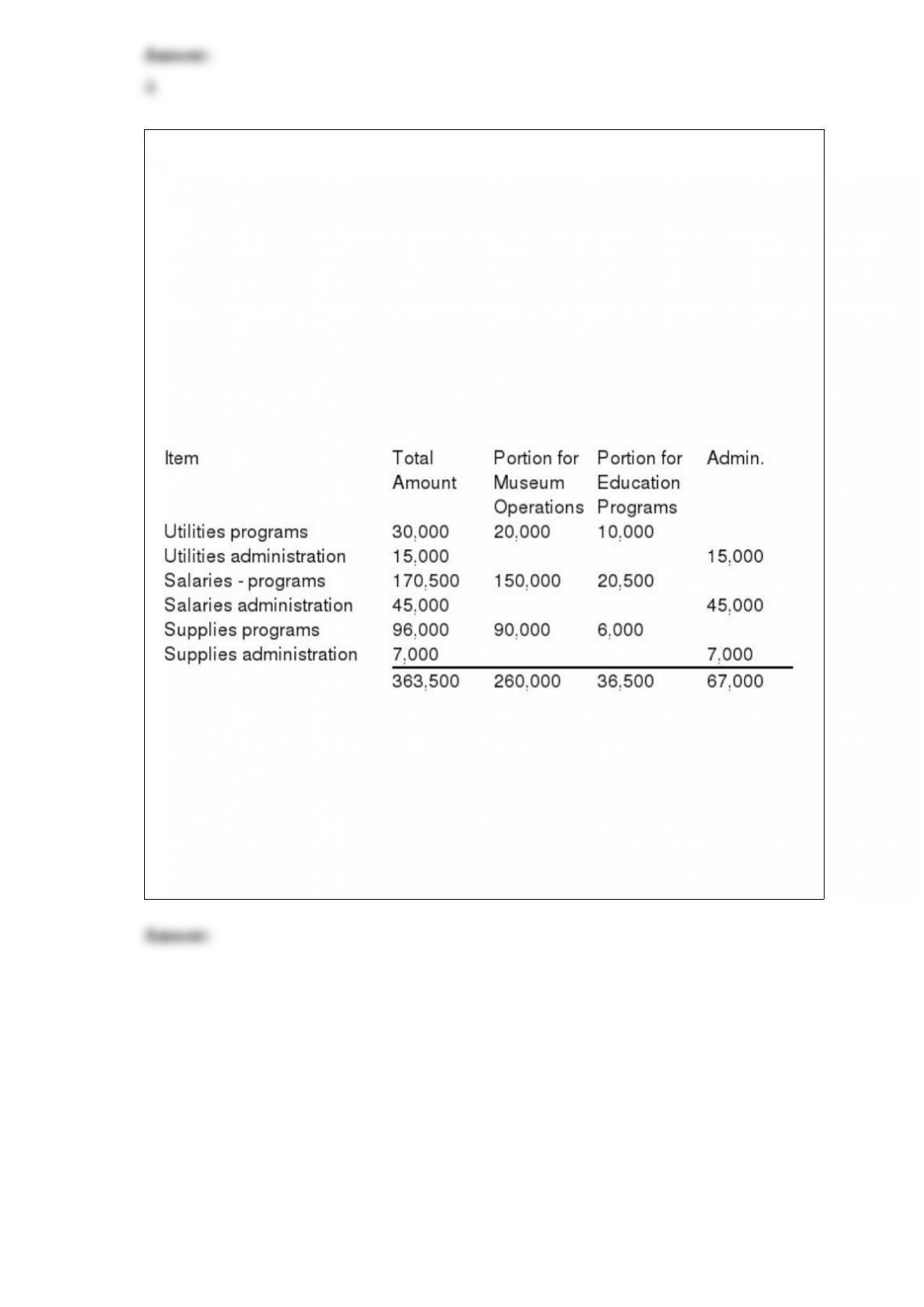

(5)Depreciation on the Museum building amounted to $ 55,000 and is allocated on the

basis of square feet: $ 40,000 to Museum operations, $ 5,000 to Education Programs,

and $ 10,000 to administration.

(6)Outstanding purchase orders for administrative supplies at 12-31-2015 totaled

$2,000.

Required: Prepare a Statement of Activities and Changes in Net Assets for the Museum

for the year ended 12-31-2015 .

20) With respect to budgetary reporting by governments, which of the following is not

True?

A)While GASB standards guide the format of the comparison, it does not require

governments to maintain budgetary accounts

B)The basis of accounting used to report the Actual column in the budgetary

comparison schedule is prepared according to legal requirements for budget

preparation; even if it is a departure from GASB standards

C)Budgetary accounts are required to appear in the general purpose financial statements

D)GASB standards require governments to present a comparison of budgeted and

actual results for the General Fund and special revenue funds with legally adopted

budgets

21) In addition to a Statement of Financial Position and a Statement of Activities, a

private college or university is required to present:

A)A Statement of Functional Expense

B)A Statement of Cash Flows

C)Both (a) and (b)

D)Neither (a) nor (b)

22) The statistical section typically presents ____ years of information in each table or

schedule.

A) 3

B) 5

C)10

D) 12

23) Which of the following is False regarding revenues of health care organizations:

A) Patient service revenues are to be reported net of estimated contractual adjustments

in the operating statement

B) Operating Revenues are often classified as net patient service revenue and other

revenue

C) Patient service revenue includes charge for charity care

D)Revenues are measured on the accrual basis

24) Which of the following is not True regarding the Statement of Cash Flows for

proprietary funds?

A) Four categories of cash flows are used

B) Interest and dividends received are recorded as investing activities

C) The direct method is required for reporting cash flows from operations

D) At the bottom of the statement, net income is reconciled to cash flows from

operations

25) Which of the following is True regarding the reporting of investments by state and

local governmental units?

A)Investments, for which a determinable fair value can be obtained, are to be reported

at fair value

B)Realized and unrealized gains and losses are to be combined in the relevant operating

statement (for example, the Statement of Changes in Fiduciary Net Position)

C)Both of the above

D)Neither of the above

26) GASB Statement No. 52 requires endowments with investment real estate to report

those assets at:

A)Historical cost

B)Fair market value

C)Historical cost net of related debt

D)Market value net of related debt

27) Clinton County maintains an investment trust fund for the investments of

governments within its borders. All the investments had determinable fair values.

Which of the following is True regarding investment trust funds and investments in

general?

A)Clinton County would report the investments of the other governments at fair value

in the investment trust funds

B)Clinton County would report its own investments at fair value in the investment trust

funds

C)Both of the above

D)Neither of the above

28) Which of the following is not required for a special-purpose local government

engaged in only fiduciary type activities?

A)Statement of Fiduciary Net position

B)Statement of Fiduciary Cash Flows

C)Notes to the Financial Statements

D)Required Supplementary Information other than MD&A

29) Which of the following results in a decrease in fund balance on a governmental

funds Balance Sheet?

A) Expenditures

B)Transfers Received

C) Encumbrance

D)Both A and B

30) The following treatment is correct with regards to payments that are partially

exchange transactions and partially contributions:

A) Reported only as an exchange transaction

B) Reported only as a contributions

C) Reported as either an exchange transaction or contribution, depending on

managements judgment

D) The two parts should be separately accounted for

31) According to

A) Transfers among affiliated organizations

B) Receipt of temporarily or permanently restricted contributions

C)Transactions with the owners, other than in exchange for services

D)All of the above should be excluded

32) The difference between the amount of debt limit calculated as prescribed by law

and the net amount of outstanding indebtedness subject to limitation, is known as:

A) Debt Limit

B) Debt Margin

C) Long-Term Debt

D) General Long-Term Debt

33) When preparing government-wide financial statements, the modified accrual basis

governmental funds are adjusted for which of the following events?

A)Capital asset related events

B)Long-term debt related events

C)Internal service fund activities

D)All of the above

34) Which of the following is a prohibited activity for a Tax-exempt Organization?

A)Make a Profit

B)File a tax return

C)Give money away

D)Make financial contributions to a political candidate

35) Where should a government report special assessment debt that the government is

not liable for in any way?

A)Capital projects fund

B)Debt service fund

C)Government-wide statements (not in a fund)

D)None of the above

36) Which of the following is not True regarding enterprise funds?

A)Enterprise funds record long-term debt directly in the fund accounts

B)Enterprise funds record capital assets directly in the fund accounts

C)Enterprise funds report a Statement of Cash Flows

D)The difference between assets and liabilities of enterprise funds is termed Fund

Balance

37) The Expenditures control account in the General Fund is debited when:

A)Supplies are ordered

B)The budget is recorded

C)The books are closed at the end of the year

D)Equipment previously ordered is received

38) Which of the following is a required statement for a private college?

A)Statement of Changes in Fund Balance

B)Statement of Revenues and Expenditures

C)Budgetary Comparison Statement

D)None of the above is a required statement

39) Which of the following is True regarding the proprietary fund financial statements?

A)The proprietary fund financial statements include the Statement of Net Position, the

Statement of Revenues, Expenses, and Changes in Fund Net Position, and the

Statement of Cash Flows

B)The proprietary fund financial statements are prepared using the economic resources

measurement focus and the accrual basis of accounting

C)Both of the above

D)Neither of the above

40) Which of the following is not a type of governmental audit?

A)Attestation engagements

B)Consulting engagements

C)Financial audits

D)Performance audits

41) Which of the following isnot True regarding the Statement of Revenues, Expenses

and Changes in Net Position for a public college reporting as a special purpose entity

engaged in business type activities only?

A)The accrual basis of accounting is used to measure revenues and expenses

B)Encumbrances are recorded at the time purchase orders are issued

C)Depreciation expense is recorded

D)All of the above are True

42) What is the maximum threshold for a tax-exempt organizationto file a form 990-N

(electronic postcard) for tax years after 2011?

A)A charity with gross receipts of <$25,000

B)A charity with gross receipts of < $50,000

C)A charity with gross receipts of < $500,000

D)A charity with gross receipts of < $500,000 and total assets of < 2.5 $million

43) The following balances exist at year end within the governmental activities of a

government unit:

Transfers In:145,000

Transfers Out:115,000

When compiling the government-wide financial statements, the journal entry to

eliminate the transfer activity will include:

A)A debit of $115,000 to Transfers Out

B)A debit of $30,000 to Transfers In

C)A debit of $115,000 to Transfers In

D)None of the above

44) The difference between accounting for private not-for-profit hospitals and

government- owned hospitals is:

A)Government owned hospitals do not have to prepare a Statement of Cash Flows

B)Government owned hospitals do not have to record depreciation

C)The equity accounts have different titles and definitions

D)All of the above

45) The following items were included in the City of Wilson’s General Fund

expenditures for the year ended June 30, 2015:

How much should be classified as capital assets in Wilson’s General Fund balance sheet

at June 30, 2015?

A)$ -0-

B)$3,000

C)$ 9,000

D)$12,000

46) What would be the appropriate journal entry to adjust to the accrual basis of

accounting for depreciation on general capital assets related to prior years?

A) Debit Depreciation expense, Credit Accumulated Depreciation

B) Debit Net Position, Credit Accumulated Depreciation

C) Debit Accumulated Depreciation, Credit Net Position

D) Debit Machinery, Credit Accumulated Depreciation

47) When accounting for defined benefit pensions, the net pension liability for

employees of governmental activities is:

A)Reported in the government-wide statements

B)Reported in the governmental fund-basis statements

C)Both A and B

D)Neither A nor B

48) Which of the following is True regarding internal service funds?

A)Internal service funds provide services primarily to external users on a user charge

basis

B)Internal service funds normally record the annual budget in the accounts

C)Internal service funds’ capital assets are not accounted for in the accounts

D)Internal service funds use full accrual accounting

49) What is the correct journal entry for a Tax Agency Fund to record tax levies of other

governments certified to it?

A) Taxes Receivable – Current

Revenues Control

B) Taxes Receivable – Current

Due from Other Governments

C) Taxes Receivable

Transfer Out

D) Taxes Receivable for Other Governments

Due to Other Governments

50) Governmental fund financial statements are to be prepared on the

A) Accrual basis of accounting

B) Cash basis of accounting

C) Modified accrual basis of accounting

D) Tax basis of accounting

51) What are the criteria outlined in GASB Statement 39: Determining Whether Certain

Organizations Are Component Unitsfor requiring public college foundations to be

reported as discretely presented components in the colleges financial reports?

52) Identify the three basic fund categories, the funds that make up each of them, and

the categorys basis of accounting.

53) FASB Statement 136 Transfer of Assets to a Not-for-Profit Organization or

Charitable Trust that Raises or Holds Contributions for Others provides guidance on

how intermediary recipient organizations should record receipt of resources held for

others. Briefly describe the issue and how such transfers should be recorded.

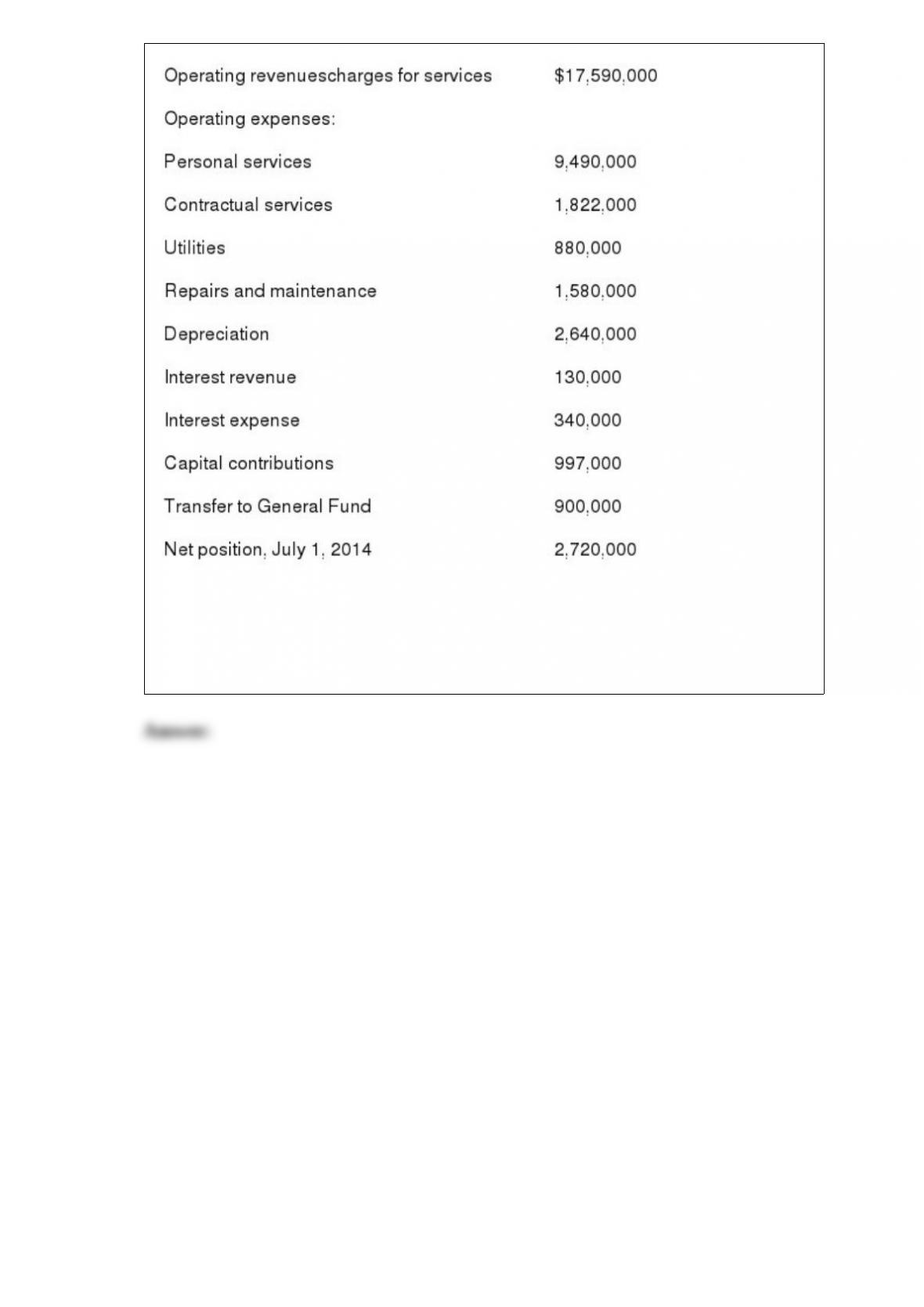

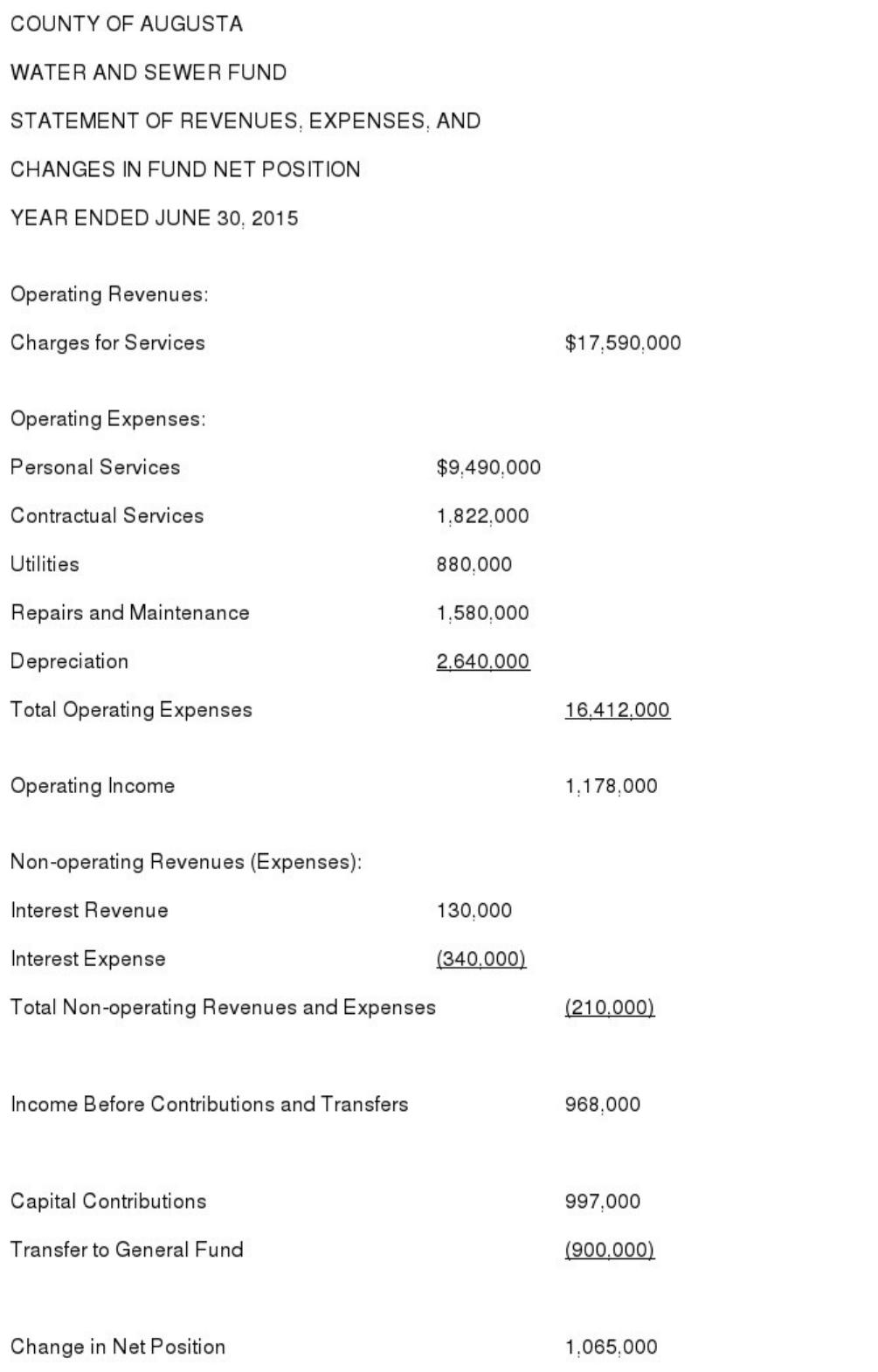

54) The following water and sewer information is available for the preparation of the

financial statements for the County of Augusta for the year ended June 30, 2015:

Required: From the information given above, prepare, in good form, a Water and Sewer

Fund column for the proprietary fund Statement of Revenues, Expenses, and Changes

in Fund Net Position for the County of Augusta for the Year Ended June 30, 2015 .

55) What conditions must be satisfied in order to use the modified approach for

recording infrastructure?

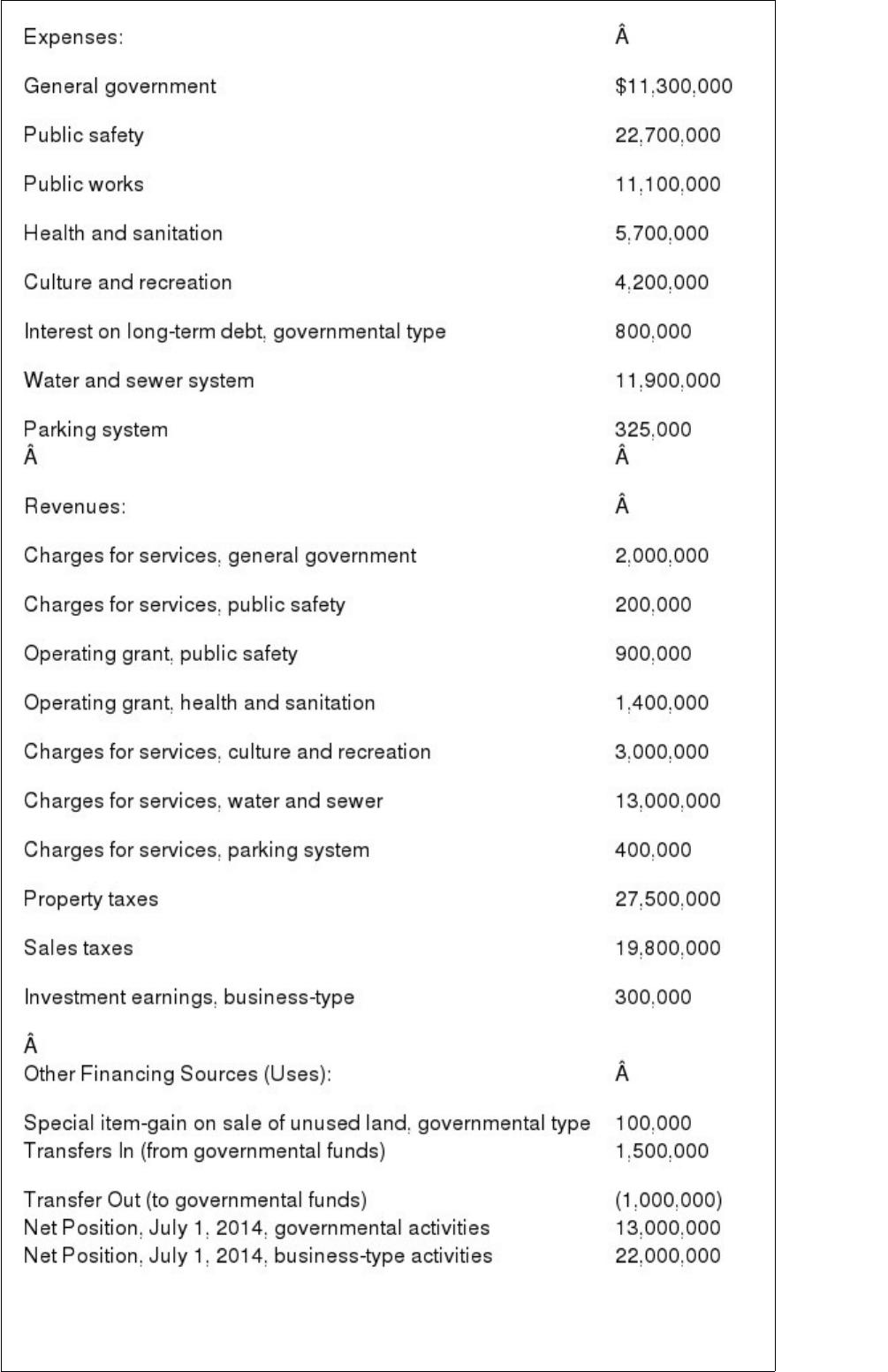

56) The following information is available for the preparation of the government-wide

financial statements for the City of Fishersville for the year ended June 30, 2015:

Required: From the information given above, prepare, in good form, a Statement of

Activities for the City of Fishersville for the year ended June 30, 2015 . Fishersville has

no component units.

57) Define and give an example of each of the following categories of Fund Balance

outlined in GASB Statement No. 54:

Non spendable

Restricted

Committed

Assigned

Unassigned

58) List the five categories outlined in GASB Statement 44 to be included in the

statistical section of the CAFR.

59) What is the objective of the single audit process?