1) The program expense ratio is calculated as Program service expenses / Total

expenses.

2) FASB sets the reporting standards for private not-for-for profits.

3) Governments must capitalize infrastructure assets in the government-wide statements

4) Capital assets acquired through proprietary funds are reported in both the Statement

of Net Position of those funds and the government-wide Statement of Net Position.

5) A County could be either a general-purpose or a special purpose government.

6) GASB specifically requires interest during construction in governments funds to be

capitalized in the government-wide statements.

7) The term, Fund Balance, is used to indicate the residual net position of a proprietary

fund.

8) Special revenue funds are used when it is desirable to provide separate reporting of

resources that are restricted or committed to expenditure for purposes other than debt

service or capital projects.

9) FASB statement 116 requires contributions to be recorded as revenue when the

contributed money is actually received.

10) Agency fund assets belong to the party or parties for which the government acts as

agent.

11) The statistical section of the CAFR contains the combining schedules of non-major

funds.

12) Fund-basis financial statements prepared for proprietary funds include the

Statement of Net Position, Statement of Revenues, Expenses, and Changes in Fund Net

Position, and the Statement of Cash Flows.

13) Real estate property taxes are an example of derived tax revenue.

14) The Accrual Basis and Economic Resource Measurement Focus are used for

Private-Purpose, Investment Trust and Pension Funds.

15) A charitable remainder trust and a charitable gift annuity both require a formal trust

agreement.

16) Investments of permanent funds should be reported at fair value, if determinable,

and unrealized gains reported along with realized gains as Investment Income-Net

Increase in Fair Value of Investments.

17) Which of the following is True regarding the Single Audit Act and its amendments?

A)All governmental entities with expenditures of federal funds in excess of $500,000

must have a single audit, if more than one program exists

B)An audit must be designed to cover 25 percent of federal funds expended, unless the

organization is deemed to be low risk

C)Both A and B above

D)Neither A nor B above

18) Which of the following is True regarding the government-wide Statement of Net

Position?

A)Discretely presented component units are included in a separate column (or columns)

B)Net Position is displayed in three categories: net investment in capital assets,

reserved, and unreserved

C)Both of the above

D)Neither of the above

19) A hospital reported the following uncollectible amounts:

$ 10,000 for services rendered to homeless individuals with no intention of collection.

$ 30,000 for services rendered with the expectation of collection, but which proved to

be uncollectible.

What amount should be reported in revenues and provision for bad debt for these

items?

A)Revenues: $ 40,000; Provision for Bad Debt: 40,000

B)Revenues: $ 40,000; Provision for Bad Debt: 30,000

C)Revenues: $ 30,000; Provision for Bad Debt: 30,000

D)Revenues: $ 0; Provision for Bad Debt: 0

20) Proprietary funds:

A)Are required to present budget-actual statements in the fund statements

B)Are required to present a reconciliation between the Statement of Revenues,

Expenses, and Changes in Fund Net Position and the Cash Flow Statement

C)Are not required to accrue interest due more than 30 days after the end of the fiscal

year

D)Are required to present a Statement of Revenues and Expenses and Balance sheet

21) Which of the following fund types uses modified accrual accounting?

A)Enterprise

B) Internal Service

C) Investment Trust

D)Special Revenue

22) In a governmental audit the auditor:

A)Is required to report directly to appropriate officials in addition to the board or audit

committee

B)Is only required to report to the board or audit committee

C)Is only required to report directly to the appropriate officials

D) None of the above

23) Which of the following is True regarding the Single Audit Act and its amendments?

A)Major programs selected for audit must equal 50 percent or more of federal

expenditures, unless the organization is deemed to be low risk

B)Separate reports are filed with every federal agency from which the audited

organization receives funds

C)Both A and B above

D)Neither A nor B above

24) A special assessment tax is

A)Assessed against all property ownersfollowing a referendum in which voters

approved the special project being constructed

B)Assessed only against certain property owners who are deemed to benefit from the

service or project being paid for by the proceeds of the special assessment levy

C)A waiver of property taxes for businesses willing to locate within a governments

jurisdiction

D) None of the above

25) Which of the following statement(s) are not included in the proprietary funds for a

government entity:

A) Statement of Revenues, Expenditures, and Changes in Fund Balances

B) Statement of Cash Flows

C)Statement of Net Position

D) All of the above are included

26) Which of the following would not be True regarding internal service funds?

A)Internal service funds use the economic resources measurement focus and accrual

basis of accounting

B)Examples of internal service funds would include self-insurance funds, motor pool

funds, and print shop funds

C)In the basic financial statements, internal service funds are reported in the proprietary

funds financial statements

D)None of the above; all are True

27) Wages that have been earned by the employees of a governmental unit, but not paid

at year-end, should be recorded in the General Fund by a debit to which of the

following accounts?

A)Appropriations

B)Encumbrances

C)Expenses

D)Expenditures

28) Which of the following is True regarding accounting and financial reporting for

private colleges and universities?

A)Expenses may be unrestricted or temporarily restricted depending on donor intent

B)The Statement of Cash Flows must use the direct method

C)A Statement of Unrestricted Revenues, Expenses and Other Changes in Unrestricted

Net Assets and a Statement of Changes in Net Assets may be presented instead of a

Statement of Activities

D)None of the above are True

29) Which of the following statements is True regarding accounting and financial

reporting for public colleges and universities?

A)Public colleges and universities may choose to report in the same manner as private

colleges and universities, using FASB standards

B)Public colleges and universities may choose to report as special-purpose entities

C)Both A and B are True

D)Neither A nor B is True

30) Which of the following statements is True regarding estimated closure costs for

municipal solid waste landfills, assuming that it is operating as an enterprise fund?

A) The estimated closure costs are expensed fully at the time of the estimate

B) A portion of those future estimated costs is to be charged as an expense and a

liability recorded based on a units-of-production method

C) Modified accrual principles apply and the amount expensed is limited to amounts

expected to be paid during the year and within 60 days of year end

D) None of the above is True

31) With respect to public colleges engaged in business-type activities, which of the

following is not correct?

A)GASB requirements for business-type activities of public colleges requires accrual

account for debt, include accrual of interest and amortization of debt discount and

premium

B)Most public college foundations are required to be reported as discretely presented

component units in the colleges financial report

C)Only amounts that are to paid by students and third-party payers can be shown as

tuition and fee revenue net of any scholarship discounts and allowances

D)All of the above are correct

32) GASB requires which of the following (if applicable) to be included in the Notes to

Financial Statements?

A) Outstanding encumbrances

B) The definition of cash and cash equivalents used in the statement of cash flows

for proprietary funds

C) Interfund receivables and payables

D) All of the above

33) Form 990, Return of Organization Exempt From Income Tax, requires all of the

following except:

A)Statement of Program Accomplishments

B)Governance, Management and Disclosures

C)Statement of Cash Flows

D)Compensation Schedules

34) Which of the following statements is not True with respect to GASB Statement No.

54 regarding restricted fund balances?

A)Restricted funds are those that are subject to constraints imposed by external parties

or by law

B)Restricted fund balance can result from legally enforceable requirements that

resources be used only for specific purpose

C)Restricted funds are the result of a self-imposed constraint by a government upon

itself

D)All of the above are correct

35) When accounting for health care organizations, services provided for charity care

are:

A)Recorded as revenues but the costs are expensed as normal

B)Must be disclosed in the notes to the financial statements

C) Not recorded as revenues and the costs are not expensed

D) None of the above

36) Which of the following would be a financial audit (or a part of a financial audit)

under the Government Auditing Standards?

A)An audit expressing an opinion on the basic financial statements of a state or local

government audit

B)An examination to determine whether purchasing procedures are appropriately

designed to assure program supplies meet standards

C)Both A and B above

D)Neither A nor B above

37) A budgetary comparison schedule is required for?

A) The General Fund

B) Each special revenue fund that has a legally adopted annual budget

C) Enterprise funds

D) (A) and (B) only

38) The City of Greystone maintains its books so as to prepare fund accounting

statements and prepares worksheet adjustments in order to prepare government-wide

statements. You are to prepare, in journal form, worksheet adjustments for each of the

following situations:

A.The City levied property taxes for the current fiscal year in the amount of

$8,000,000. At year-end, $720,000 of the taxes had not been collected. It was estimated

that $330,000 of that amount would be collected during the 60 days after the end of the

fiscal year and that $250,000 would be collected after that time and the balance would

be uncollectible. The City had recognized the maximum of property taxes allowable

under modified accrual accounting.

B.$179,000 of property taxes had been deferred at the end of the previous year and was

recognized under modified accrual as revenue in the current year.

C.In addition to the expenditures allowed under modified accrual accounting, the city

computed that an additional $72,000 should be accrued for compensated absences.

D.In the Statement of Revenues, Expenditures, and Changes in Fund Balances, General

Fund transfers out included $400,000 to a debt service fund and $270,000 to a special

revenue fund. General Fund transfers in included $1,000,000 from an enterprise fund.

39) Which of the following is False regarding the cash flow statements of a proprietary

fund?

A)A reconciliation is required between the Statement of Revenues, Expenses, and

Changes in Fund Net Position and the cash flows from operating activities section of

the Cash Flow Statement

B)Interest payments are reported as increases in cash flows from either capital and

related financing or noncapital financing activities, whichever is appropriate

C)Purchases of equipment would be reported in the investing section

D)None of the above these are all True

40) When a liability is incurred as authorized by an appropriation, the appropriation is

said to be:

A) Encumbered

B) Appropriated

C)Expensed

D)Expended

41) Contractual allowances for amounts billed to 3rd parties are treated as:

A)Contractual allowance expense

B)A contra-revenue

C)A bad debt expense

D) An other financing use

42) With respect to Permanent Funds, which of the following is not True?

A)The principal is classified as Nonspendable Fund balance

B)Permanent Funds are created when resources are provided by private donation

C)Earnings in excess of expenditures must be added to principal corpus

D)Permanent Funds use the current financial resources measurement focus

43) Which of the following is True with respect to the General Fund

A) The General Fund is considered to be a major fund if the combined total of assets,

liabilities, revenues and expenses exceeds 10% of the total of all governmental funds

B)The General Fund is considered to be a major fund when preparing fund basis

financial statements if it bears a financial benefit or burden to the primary government

C)The General Fund is always considered to be a major fund when preparing fund basis

financial statements

D)The General Fund is not reported as part of the CAFR

44) With the exception of collections, fixed assets may be recorded by a private

not-for-profit as:

A)Temporarily restricted

B)Unrestricted

C) Permanently restricted

D)Either A or B

45) Montgomery County operates a landfill as an enterprise fund. The closure and

post-closure care costs are estimated to be $25 million. It is estimated that the capacity

of the landfill is 12 million tons of waste and that waste will be accepted for 5 years.

During 2015, 3 million tons of waste was accepted. The charge for closure and

post-closure care costs for 2015 would be:

A)$ 6.25million

B)$ 5.8 million

C)$5 million

D) $2.4 million

46) The Water Utility (an enterprise fund) has just sent out a purchase order to a vendor

for some new equipment. Which of the following would be included in the journal entry

to record this event?

A) A credit to Accounts Payable

B) A debit to Encumbrances

C) A debit to Expenditures

D) None of the above

47) Which of the following steps in the budgetary authority process occurs when a

federal agency issues a purchase order?

A)Apportionment

B)Appropriation

C)Allotment

D)Obligation

48) When closing out the General Fund and Special Revenue Funds of a state or local

governmental unit, the balance of the operating statement are closed to:

A)Budgetary Fund Balance Reserved for Encumbrances

B)Appropriations Control

C) Other Financing Sources Transfer Out

D)Fund Balance

49) Under NACUBO guidelines, the current period provision for uncollectible accounts

should be reported as:

A)Bad debt expense

B)Decreases in Temporarily Restricted Net Assets

C)Reductions in revenue

D)Transfers

50) To apply for tax-exempt status, a non-profit organization must file:

A)IRS Form 501(c)(3)

B)IRS Form 990

C)IRS Form 1023

D)None of the above

51) An encumbrance in a capital project fund is created

A) When the project is paid for in full

B) When the work on the project begins

C) When the work on the project is finished

D) When a contract is signed or issued

52) The GASB is under the oversight of:

A) GAO

B) FASAB

C) FAF

D) FASB

53) In 2014, a private college received a grant of $100,000 with purpose restrictions. In

2015 funds were expended for the purpose outlined in the gift; however, it was not

possible to determine whether the restricted funds or unrestricted funds were used. The

presumption should be:

A)The restricted funds would have been used first

B)The unrestricted funds would have been used first

C)The restricted funds and unrestricted funds would have been used equally

D)The restricted funds and unrestricted funds would have been used, based on a

weighted average of the amounts

54) The General Fund is always considered to be a major fund. When are other

governmental funds considered major?

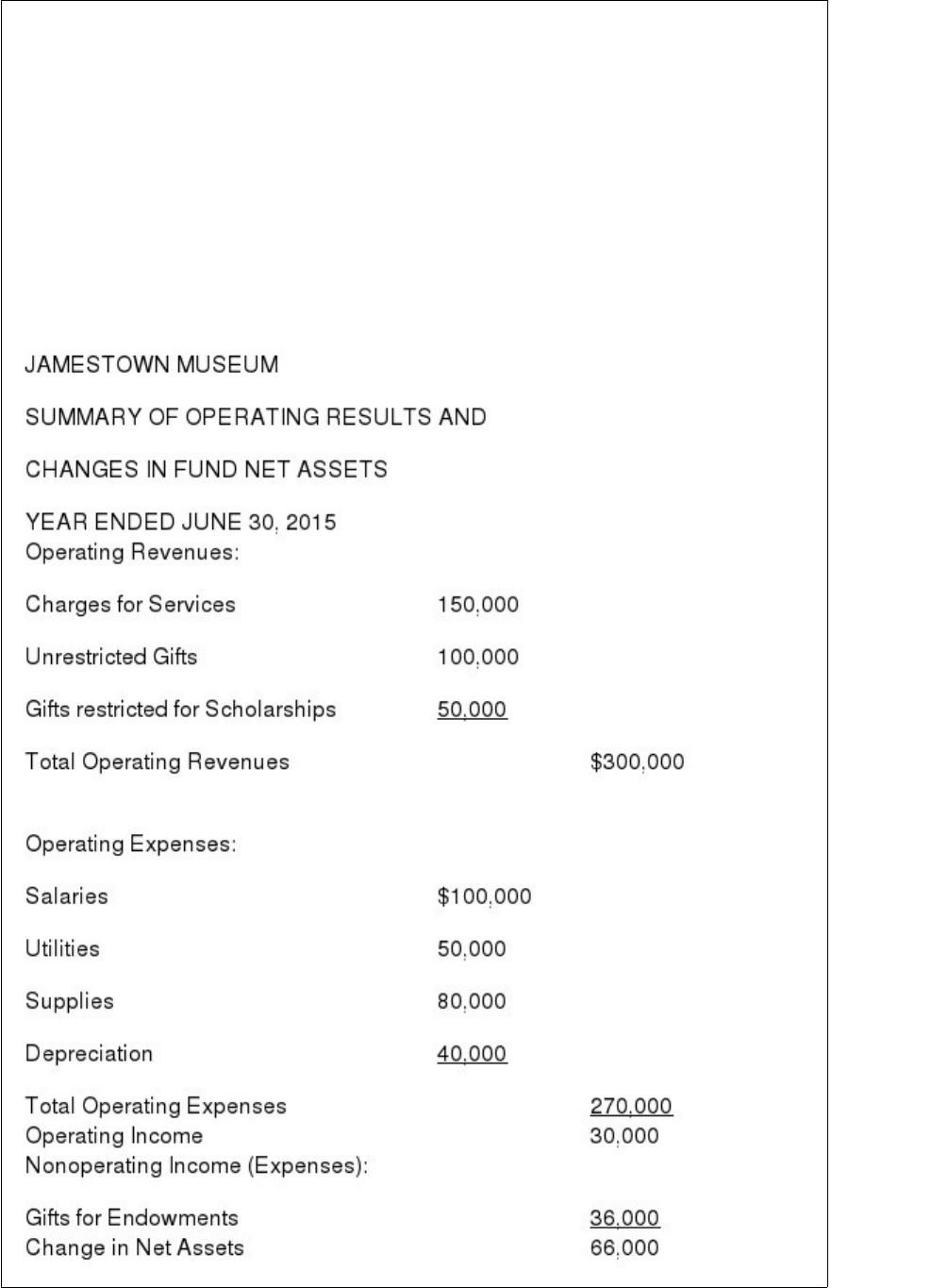

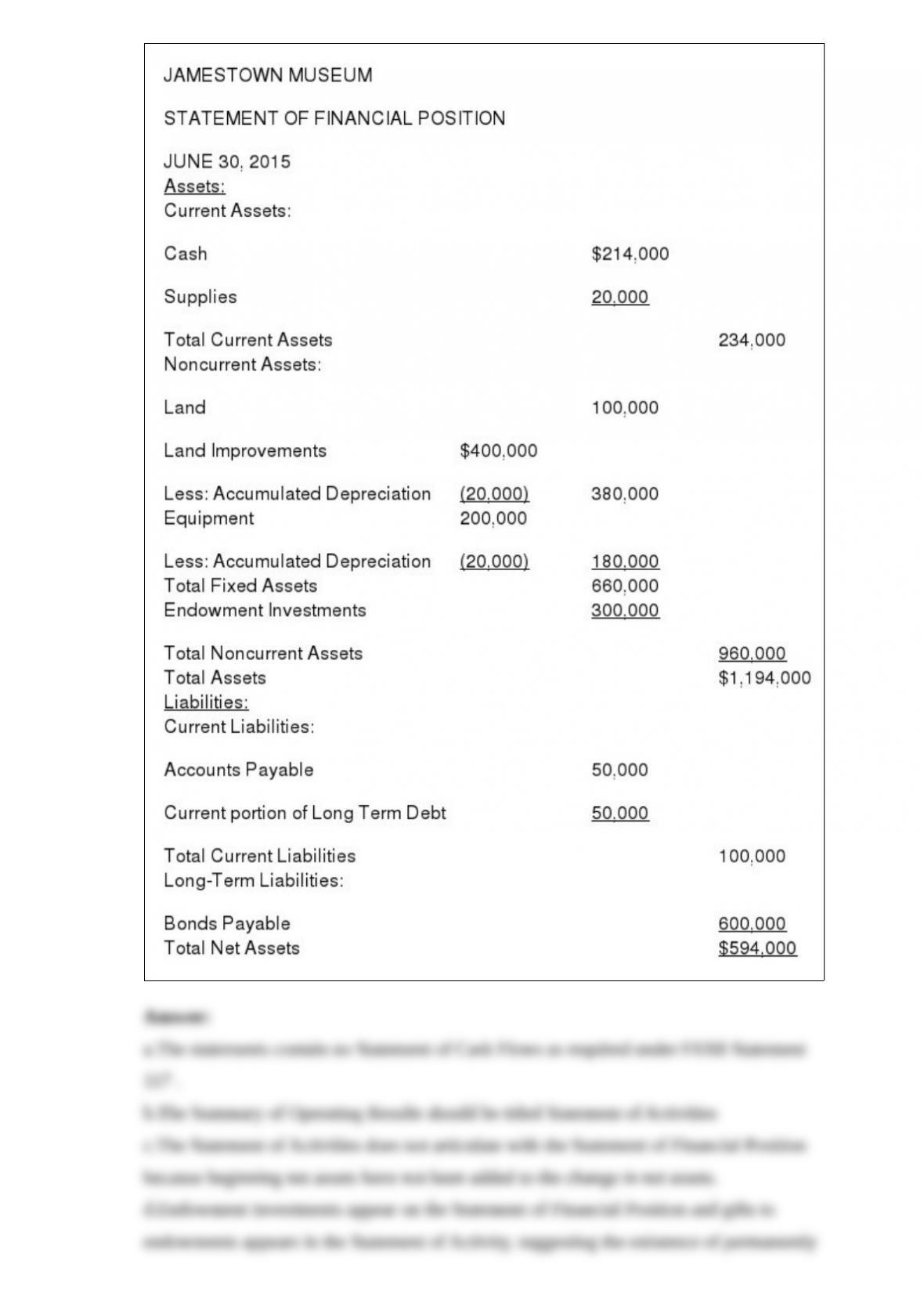

55) Below are the complete set of published financial statements taken from the annual

report of the Jamestown Museum. The statements do not comply with generally

accepted accounting principles for private not-for-profits in a number of ways. Review

these statements and describe instances in which the statements fail to comply with

accepted accounting standards. You must be able to justify your assertions – for example

you cannot say they failed to capitalize leases if there is no evidence they have a

qualifying lease.

Example: (1) The financial statements contain no note disclosures. The notes are an

integral part of the financial statements and many individual disclosures are required

under FASB standards.

56) What is the difference between an exchange and a non exchange transaction?

57) With regard to the government-wide statements, list the required statements.

58) Provide the definition of the following terms as outlined by GASB Concepts

Statement No. 4, Elements of Financial Statements:

Assets

Liabilities

Net position

Inflows of resources

Outflows of resources

59) Contrast the purpose of Private-purpose Trust Funds and Permanent Funds.

60) When preparing government-wide financial statements, the modified accrual based

governments funds are adjusted. List 4 events involving capital assets that are likely to

require adjustments.

61) The City of Smithville was awarded a federal grant on May 1, 2015 in the amount

of $2,400,000 for the purpose of conducting a summer youth employment program.

This was a reimbursement-type grant. On August 31, $5,475,000 of expenditures was

recorded, and cash was paid out. On October 15 the $5,475,000 was received from the

federal government. Record necessary entries as of July 1, August 31, September 30

and October 15 .

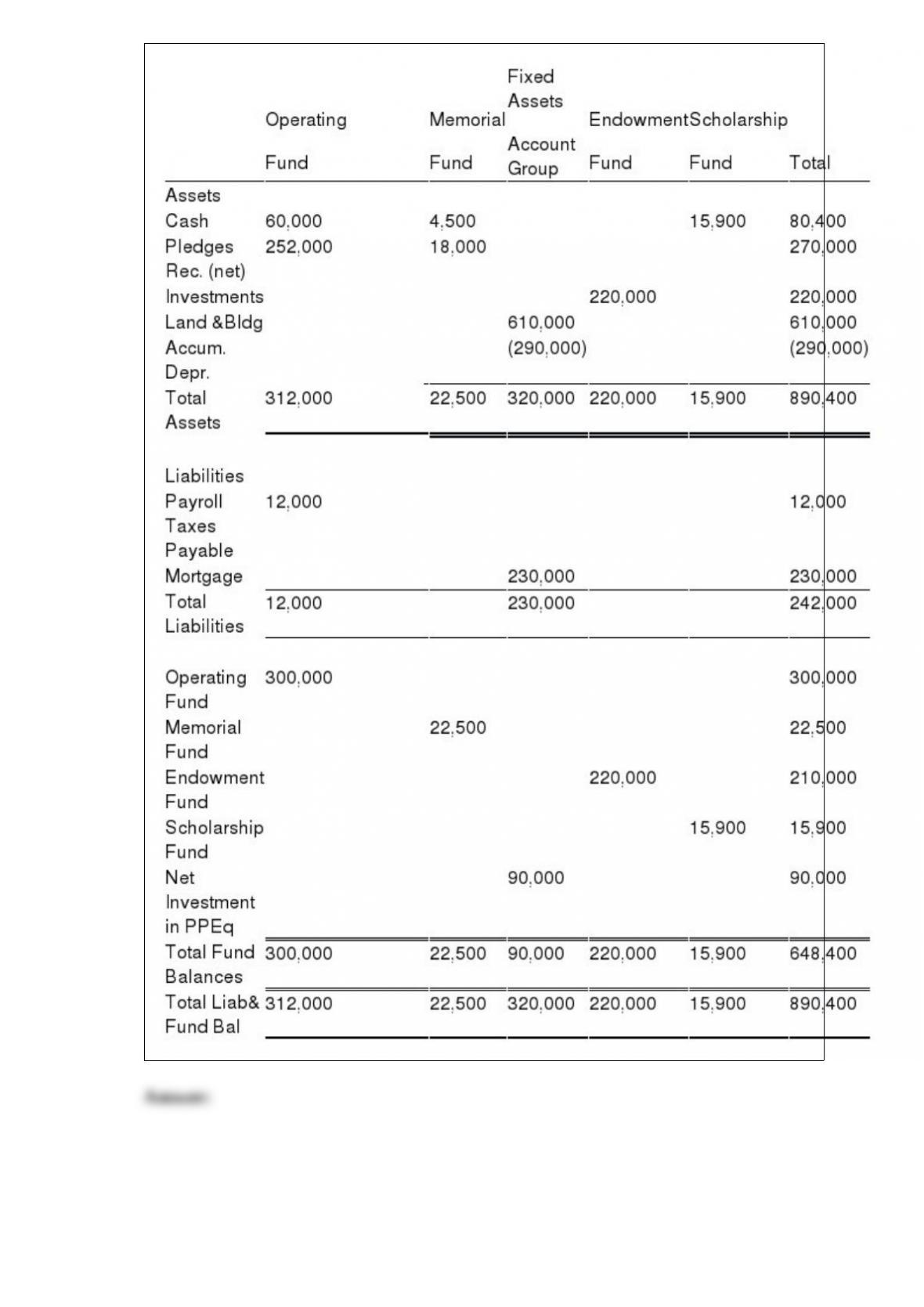

62) Union Seminary uses the fund basis of accounting for internal record keeping.

Presented below is the fully adjusted 12/31/2015 balance sheet for Union, prepared

using funds and account groups. The following are fund descriptions:

Operating Fund – the fund used for transactions not falling within the definition of other

funds. There are no restrictions on these resources.

Memorial Fund – Used to account for resources donated from outside parties for

specific capital additions

Endowment Fund – Assets received from an outside donor for permanent investment,

only the earnings may be expended.

Scholarship Fund – Cash set aside by the Seminary’s governing board for use as

scholarships and student aid.

Fixed Assets Account Group – A record of the Seminary’s fixed assets and long-term

debt.

Required: Prepare a Statement of Financial Position following the guidelines provided

in FASB Statements 116 and 117 for private not-for-profits and assuming Union does

not classify plant assets as temporarily restricted.