1) The

2) According to the rules for accounting for colleges and universities under the

jurisdiction of the FASB, depreciation is recorded. When reporting by function,

depreciation is allocated to functional categories.

3) NACUBO guidelines require both revenues and expenses for split summer sessions

to be apportioned to the two fiscal years.

4) Notes to the financial statements must distinguish between the primary government

and discretely presented component units.

5) According to FASB standards relating to Budgetary Accounting, the accounting

system should provide the basis for appropriate budgetary control.

6) Under the modified accrual basis, property taxes are recognized in the period in

which cash is received, regardless of when the taxes were levied.

7) When using modified accrual accounting, revenues should be recognized when

measurable and available to finance expenditures of the current period.

8) An enterprise fund should be used when the government has a policy to establish fees

to cover the costs of providing services for an activity.

9) Only governmental fund statements include separate columns for discretely

presented component units.

10) Differences between actual and estimated contractual adjustments are treated as

changes in accounting estimates.

11) Governments offering postemployment benefits to their retired employees must

present two financial statements related to their plans: the Statement of FiduciaryNet

Position and the Statement of Changes in FiduciaryNet Position, as well as additional

required supplementary information.

12) The four categories on the Statement of Cash Flows for a proprietary fund are

operating, non-capital financing activities, capital and related financing activities, and

investing activities.

13) Governmental fund financial statements are to be prepared on the accrual basis of

accounting.

14) The Township of Thomasvilles General Fund has the following net resources at

year end:

$77,000 of prepaid insurance

$375,000 rainy day fund approved by the township governing board with specific

conditions for its use

$2,500 of supplies inventory

$61,000 state grant for snow removal

$150,000 contractual obligations for the purchase of equipment

$200,000 to be used to fund government operations in the future

Outstanding encumbrance of $80,000 for the purchase of furniture & fixtures (assume

no contractual obligation)

What would be the total Committed fund balance?

A)$375,000

B)$290,000

C)$525,000

D)$455,000

15) The FASAB has the authority to establish accounting and financial reporting

standards for:

A)State and local governments

B)Investor owned business

C)Federal government

D)Public not-for-profits

16) Estimated Revenues are $4,600,000, and Appropriations are $4,000,000, the journal

entry for the budget includes a:

A) Debit to Budgetary Fund balance for 600,000

B) Debit to Encumbrances for 600,000

C) Credit to Budgetary Fund balance for 600,000

D) Credit to Budgetary Fund Balance — Reserve for Encumbrances for 600,000

17) A government reported an other financing source in the amount of $750,000, related

to the sale of land in its governmental funds Statement of Revenues, Expenditures, and

Changes in Fund Balances. The land had a cost of $300,000. The adjustment in the

reconciliation, when moving from the governmental Funds Statement of Revenues,

Expenditures, and Changes in Fund Balances to the change in net position for

governmental activities in the Statement of Activities would be a(an):

A)Increase of $450,000

B)Decrease of $450,000

C)Decrease of $300,000

D)Increase of $300,000

18) Investments of internal investment pools are to be reported in:

A)The funds providing the resources for the investments

B)An investment trust fund

C)An agency fund

D)Either A and B

19) Which of the following is not one of the major sections of the Comprehensive

Annual Financial Report (CAFR)?

A)Budgetary

B)Financial

C)Introductory

D)Statistical

20) Which of the following funds typically record budgets?

A) General Funds, special revenue funds, capital projects, debt service, and permanent

B) Only General Funds

C) General Funds and permanent funds

D) General Funds and special revenue funds

21) A private foundation made a multi-year pledge to a private college on December 31,

2014, the last day of the fiscal year. The pledge was to pay $15,000 per year each year

for five years, beginning on December 31, 2015 . The discount rate is 6%. The present

value of five payments of $15,000 is $63,185. The present value of four payments of

$15,000 is $51,977. No purpose or plant restrictions were involved.

The private college would:

A)Record contribution revenue of $3,792 in 2014

B)Record contribution revenue of $3,792 in 2015

C)Record interest revenue of $3,792 in 2014

D) Record interest revenue of $3,792 in 2015

22) Which of the following is True regarding the proprietary funds statements?

A)Major enterprise and internal service funds are reported in separate columns; a

column is presented for all non-major enterprise and internal service funds (combined),

and a total column is presented

B)Financial statements include a Statement of Net Position, Statement of Revenues,

Expenses, and Changes in Fund Net Position, and Statement of Cash Flows

C)Both of the above

D)Neither of the above

23) A fund that is used to account for assets held by a government temporarily acting as

agent for one or more other governments units or for individuals or private

organizations is a(n):

A)Agency fund

B)Private-Purpose Trust Fund

C)Investment Trust Fund

D)Pension Trust Fund

24) Fiduciary Funds are not included in the Government-wide Financial Statements

because:

A) These Funds use the modified accrual basis of accounting

B) The resources are not available to the reporting unit

C) The government doesnt keep track of these types of funds

D) These funds do not have a material effect on the financial statements

25) Inter fund Transfers are flows of cash or other assets that:

A)Require repayment

B) Are an exchange between funds of equal value

C)Do not require repayment

D)Are taxable

26) Which of the following statements is correct with respect to GASB Statement No.

54 regarding committed funds?

A)Committed funds are those that are designated as committed through ordinance or

resolution by the governments highest level of authority

B) These constraints are easily changed by administrators

C)This is constraint is imposed by law and may not be changed without amendment of

the law

D)Committed funds may be redesignated to uncommitted in the event of a budget

shortfall

27) A government reported expenditures for infrastructure as follows: $18 million for

improvements and additions; $20 million to extend the life of existing infrastructure;

$17 million for general repairs. The cost of its infrastructure, excluding land, is $750

million, and the infrastructure has an estimated life of 50 years, on average. Which of

the following would be the reported expense (in millions) under each of the following

options?

A)Depreciation Approach: $15; Modified Approach: $37

B)Depreciation Approach: $15; Modified Approach: $32

C)Depreciation Approach: $32; Modified Approach: $37

D)Depreciation Approach: $32; Modified Approach: $32

28) Which of the following is an inter fund transaction?

A)Inter fund services provided and used

B)Inter fund transfers

C)Inter fund loans

D)All of the above are inter fund transactions

29) A private college received a $2,000,000 gift from a donor. The colleges governing

board voted to use the $2,000,000 to establish an endowment, with the intent to keep

the principal intact forever. The income from the endowment was to be used to fund

research in the biology department. How should the college classify the $2,000,000

gift?

A)Unrestricted

B)Temporarily restricted

C)Permanently restricted

D)Either temporarily or permanently restricted

30) Which of the following would be accounted for as a permanent fund?

A)A gift of $65,000 to a school district, to be invested permanently, with the proceeds

to be awarded as college scholarships to graduating seniors

B)A gift of $65,000 to a school district, to be used for landscaping improvements

C)A gift of $65,000 to a city to be invested permanently, with the proceeds to be used to

buy books for the city library

D)Both A and C

31) Which of the following conditions would exempt income-producing activities from

the Unrelated Business Income Tax (UBIT)?

A)Majority of labor is performed by paid employees

B)The business sells donated merchandise

C)The business is carried on regularly but is unrelated to the organizations tax-exempt

purpose

D)The business is operated for a profit

32) Proprietary funds utilize what basis of accounting?

A)Modified accrual

B)Accrual

C)Cash

D)Budgetary

33) Which of the following statements is not correct?

A) Transactions between funds of the same government may not be assumed to be arms

length in nature

B)Most inter fund transactions are eliminated in the government-wide statements

C)Inter fund reimbursements are classified as other financing sources or uses

D)Inter fund transfers are classified as other financing sources or uses

34) Which of the following is True regarding the governmental fund financial

statements?

A)The governmental fund financial statements include the Balance Sheet, and the

Statement of Revenues, Expenditures, and Changes in Fund Balances

B)The governmental fund financial statements are prepared on the current financial

resources measurement focus and modified accrual basis of accounting

C)The governmental fund Balance Sheet reflects the difference of assets minus

liabilities as Fund Balance

D)All of the above are True

35) The following transactions occurred in the General Fund of SmythCounty. Prepare

the journal entry(s) as instructed for each. Assume each item is independent of each

other.

A.The total estimated revenue budget for 2015 is $11,000,000 and the total

appropriations for 2015 are $9,500,000. Total planned transfer to debt service funds for

2015 is $800,000. Record the budget (without subsidiary ledger detail)

B.SmythCounty was able to get a Tax Anticipation Note that was secured by the

countys power to tax. The county borrowed $500,000 and planned to repay the loan as

tax collections begin to exceed current disbursements for the year. Upon repayment of

the loan the county must pay $12,600 in interest. Record the Note payable and the later

repayment of the note payable

C.Property taxes of $ 7,000,000 were levied for SmythCounty. Assume that 1.5 percent

of these taxes are estimated to be uncollectible due to local economic conditions.

Record the entry when the tax is levied

D.During 2015 the billing staff inappropriately had duplicate bills for the same

properties in the amount of $23,000. Record the entry to correct this error.

E.Upon examining the revenues and expenditures to date, the governing board decided

to amend the budget. The revenue budget needs to be decreased by $85,000 and the

appropriations should be increased by $65,000. Record the amendments to the budget

when legally approved

F.A review of the Tax Receivable subsidiary ledger indicates the following:

$20,000 would be received 120 days after year-end

$45,000 would be received 90 days after year-end

$22,000 would be received 60 days after year-end

$21,000 would be received 30 days after year-end

Record the property taxes to be deferred that is required by the GASB

G.The treasurer of Smyth County approved the write-off of delinquent taxes from 2015

totaling $10,200 and related interest and penalties of $750. – Record the write-off of

uncollectible delinquent taxes

36) Which fund is used when a contributor specifies that the income of trust assets be

used for the benefit of the general citizenry?

A) Private-purpose trust fund

B) Agency fund

C)Investment trust fund

D) Permanent fund

37) DukesMedicalCenter performed charity care at a cost of $5,000 and a standard

charge of $11,000. How much should Dukes recognize as revenue?

A) $11,000

B) $ 6,000

C) $5,000

D) $ 0

38) Which of the following would generally be included in the Statement of Net

Position of an Enterprise Fund?

Reserve for Encumbrances Revenue Bonds Payable

A) No No

B) No Yes

C) Yes No

D) Yes Yes

39) Which of the following is True regarding the financial statements of a private

sector not-for-profit hospital?

A)Revenues are measured using the accrual basis of accounting

B)Changes in net assets must be shown by net asset classification

C)The Statement of Cash Flows uses a three-category format

D)All of the above are True

40) Supporting activities as classified in the Statement of Activities, normally include

A) Management and general

B) Fund-raising

C) Membership development

D) All of the above

41) Which of the following is True regarding the government-wide Statement of

Activities?

A)The government-wide Statement of Activities may reflect expenses either by

function (general government, public safety, etc.) or by object or natural classification

(salaries, supplies, etc.)

B)The government-wide Statement of Activities reflects taxes as general revenues

C)The government-wide Statement of Activities is prepared using the modified accrual

basis of accounting for governmental activities and using the accrual basis of

accounting for business-type activities

D)Indirect program expenses may not be allocated to the other functional areas

42) Under GASB rules for the financial reporting entity:

A)Component units must be reported in columns (discrete presentation) separate from

the funds of a primary government

B)Counties are component units of the State Government

C)Blended and discretely presented component units are to be reported in

government-wide financial statements but not in fund financial statements

D)Component units are included if the primary government is financially accountable

for their operations

43) A donor gave $ 1,000,000 to a private not-for-profit organization to be held in

endowment. In addition, the governing board permanently designated $ 500,000 to the

endowment. In the Statement of Financial Position, how should these amounts be

classified?

A)Permanently Restricted: $1,500,000; Unrestricted: $ – 0 –

B)Permanently Restricted: $1,000,000; Unrestricted: $ 500,000

C)Permanently Restricted: $ 500,000; Unrestricted: $1,000,000

D)Permanently Restricted: $ – 0; Unrestricted: $1,500,000

44) Which of the following is considered a source of general revenue in the

Government-wide Statement of Activities?

A) Charges for Services

B)Operating Grants

C)Sales Tax

D) None of the Above

45) Which of the following is a governmental audit that is concerned with examining,

reviewing, or performing agreed upon procedures on a subject matter of an assertion

and reporting on the results?

A)Financial Audit

B)Attestation Engagement

C)Performance Audits

D)Nonaudit Services

46) When taxes and/or special assessments are levied specifically for payment of

interest and principal on long-term debt, those taxes are recognized:

A) As revenues in the General Fund with transfers made to the debt service funds for

payments

B) As Other Financing Sources in the debt service fund

C) As revenues in the capital projects fund with transfers made to the debt service funds

for payments

D) As revenues in the debt service fund

47) Which of the following is True regarding the reporting of Budget-Actual

Comparisons?

A)A Budget-Actual Comparison Schedule is required for the General Fund and all

major special revenue funds that have a legally adopted annual budget

B)A Budget-Actual Comparison Statement may be prepared in lieu of the Schedule

C)Both (A) and (B) are True

D)Neither (A) nor (B) is True

48) Contrast revenue recognition under the accrual and modified accrual bases of

accounting.

49) List the fund financial statements required by GASB Statement 34 for proprietary

type funds.

50) What are the required parts of the annual financial reports for special-purpose

governments engaged only in fiduciary-type activities?

51) What are the required parts of the annual financial report for special-purpose local

governments engaged only in business-type activities?

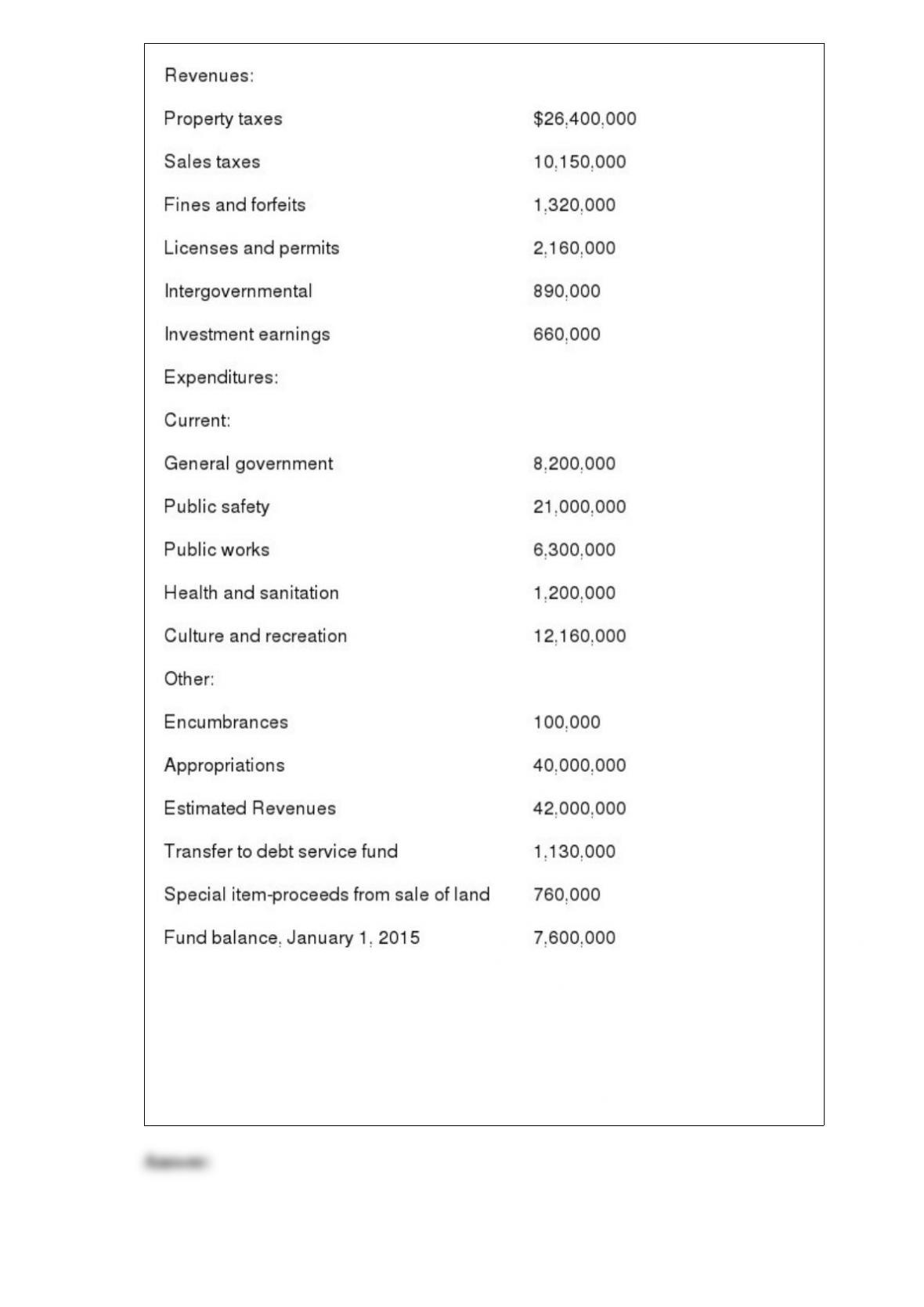

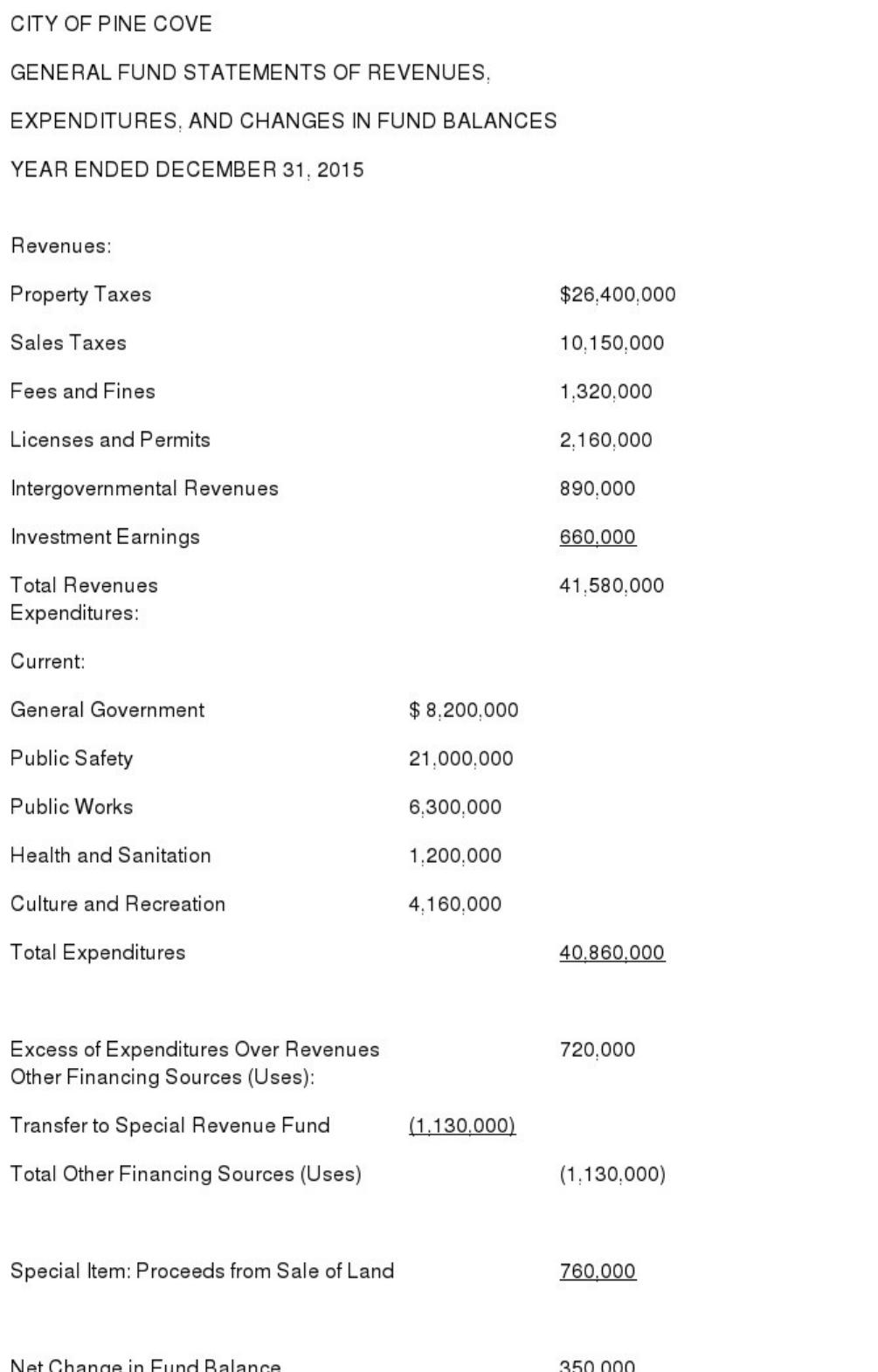

52) The following General Fund information is available for the preparation of the

financial statements for the City of Pine Cove for the year ended December 31, 2015 .

Required: From the information given above, prepare, in good form, a General Fund

Statement of Revenues, Expenditures, and Changes in Fund Balances for the City of

Pine Cove for the Year Ended December 31, 2015 .

53) The Village of Naples has $19,000 of purchase orders outstanding at the end of

2014 which will be honored. The goods and supplies were received during the second

week of January, 2015 . The invoice amounted to $18,800

What are the journal entries necessary to re-establish the encumbrance and record

receipt of the supplies?

54) According to FASB Statement No. 116, Appendix D, how are not-for-profit

organizations distinguished from a business?

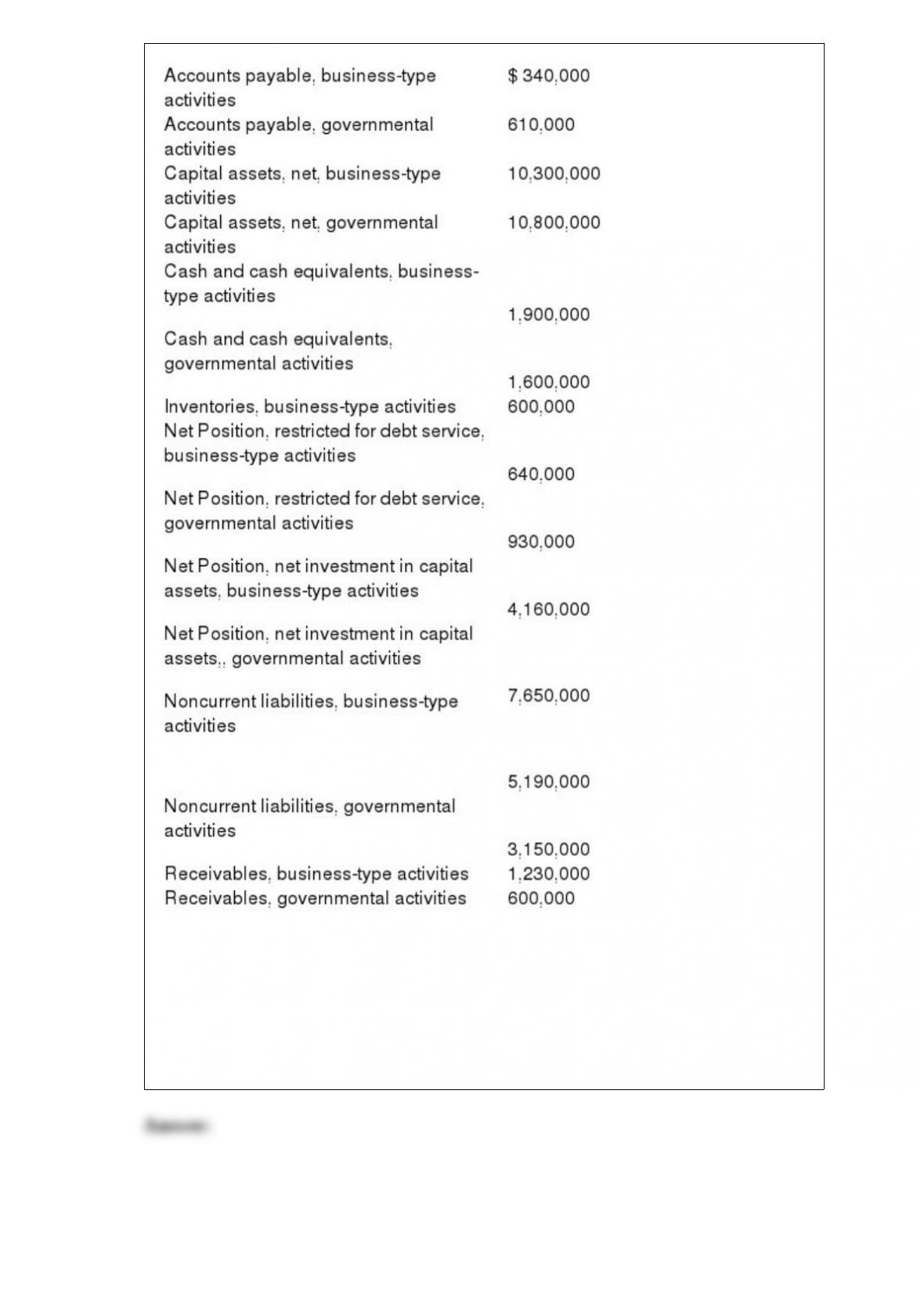

55) The following information is available for the preparation of the government-wide

financial statements of the City of Aurora as of June 30, 2015:

Assume all long-term liabilities were incurred in the acquisition of capital assets.

Required: From the information given above, prepare, in good form, a Statement of Net

Position for the City of Aurora as of June 30, 2015. Include the unrestricted net

position, which is to be computed from the information presented above. Include a total

column. Aurora has no component units.

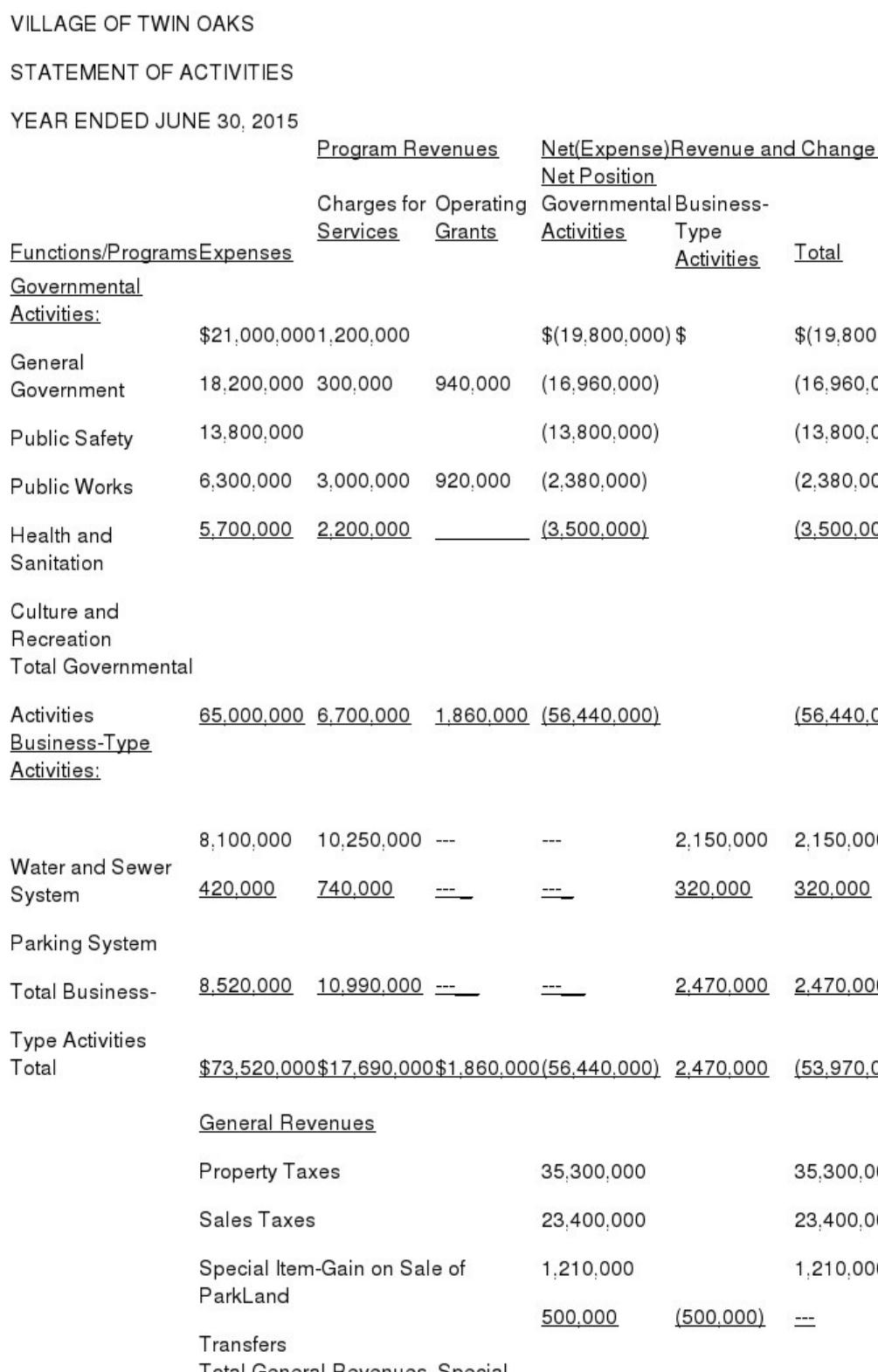

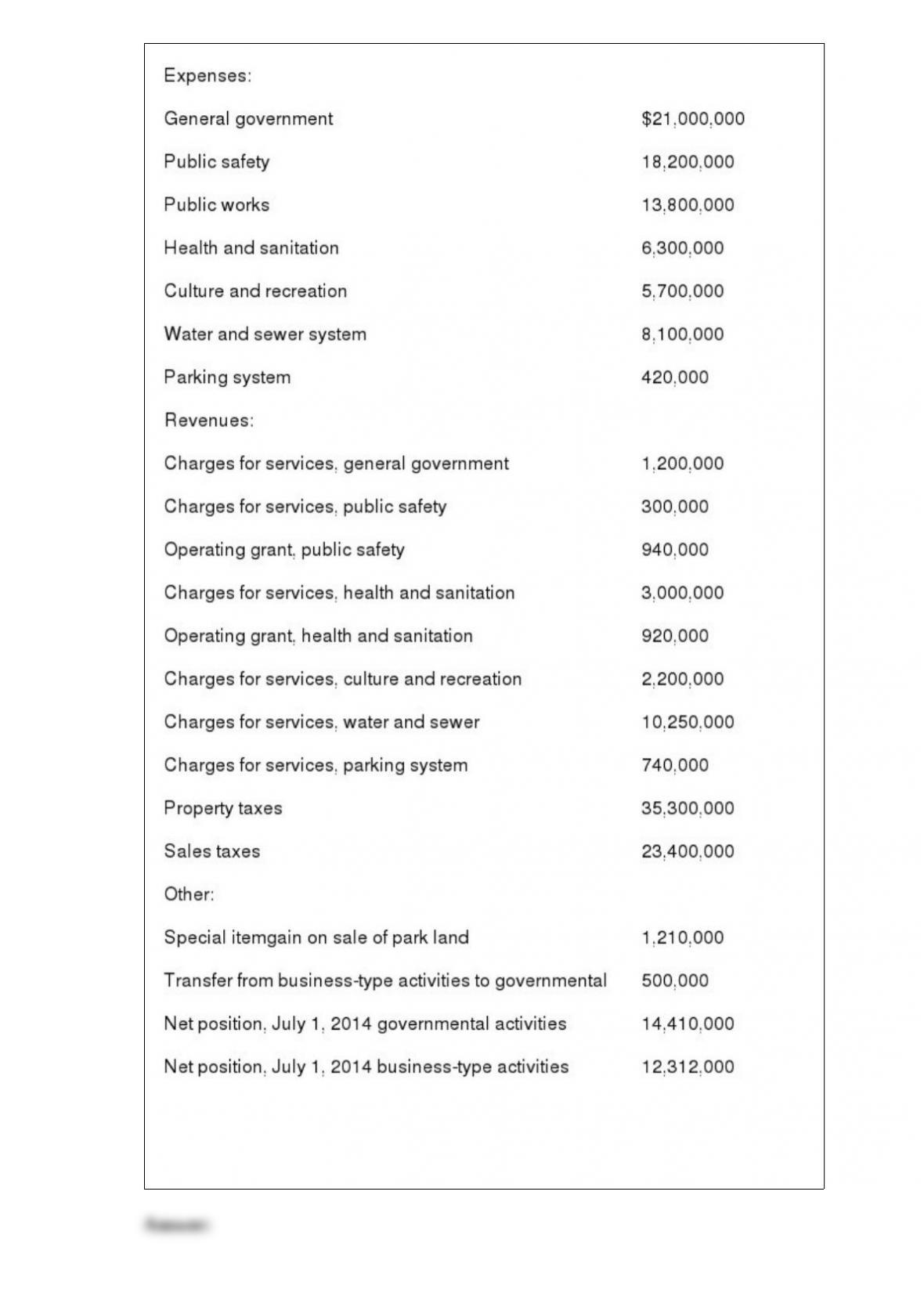

56) The following information is available for the preparation of the government-wide

financial statements for the Village of Twin Oaks for the year ended June 30, 2015:

Required: From the information given above, prepare, in good form, a Statement of

Activities for the Village of Twin Oaks for the Year Ended June 30, 2015 .