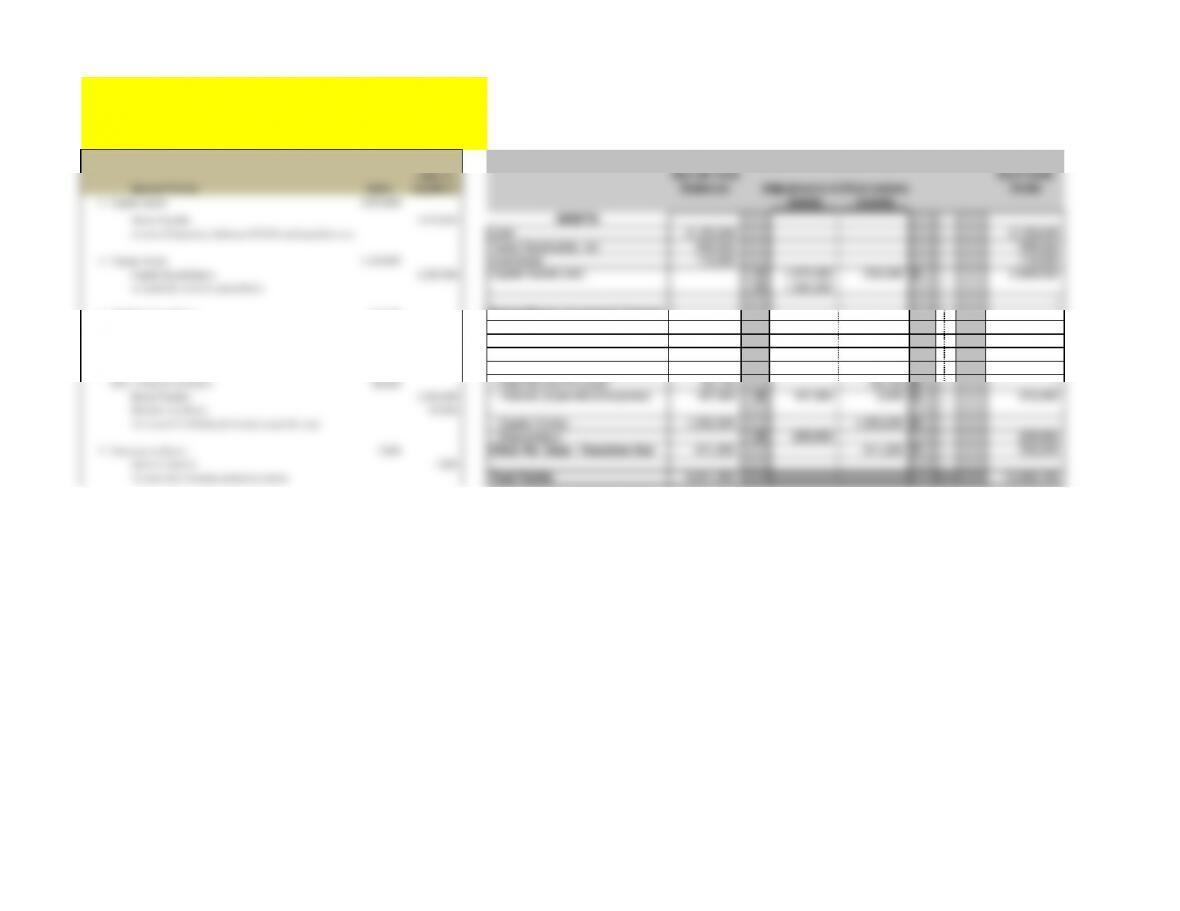

Worksheet to convert Governmental fund basis information to accrual basis

Journal Entries debits

credits

(enter as

negatives)

Gov’tal Fund

Balances

Adjustments & Eliminations

Balances for

Gov’t-wide

Stmts

1 Capital Assets 1,875,000

Debits Credits

Bonds Payalbe 1,875,000 DEBITS:

to record beginning balances LT debt and capital assets Cash 2,123,249 2,123,249

Taxes Receivable, net 559,000 559,000

2 Capital Assets 1,250,000

Inventories 116,000 116,000

Capital Expenditures 1,250,000 Capital Assets (net) 11,875,000 235,500 32,889,500

to capitalize current expenditures 21,250,000

–

3 Depreciation expense 235,500

Expenditures (expenses) Current

Accumulated depreciation 235,500 General Govt. Operations 1,490,501 1,490,501

current year depreciation Public Safety 1,495,000 1,495,000

Education 1,115,000 1,115,000

4 OFS – Proceeds of Bonds 2,500,000

Other Expenditures (expenses)

OFS – Premium on Bonds 80,000 – Debt Service Principal 93,750 93,750 8–

Bonds Payable 2,500,000 – Interest (expenditure/expense) 187,500 6187,500 3,000 5372,000

Premium on Bonds 80,000

To record LT liability for bonds issued this year

– Capital Outlay 1,250,000 1,250,000 2–

– Depreciation 3235,500 235,500

5 Premium on Bonds 3,000

Other Fin. Uses – Transfers Out 911,250 611,250 7300,000

Interest Expense 3,000

To amortize 9 months of bond premium

Total Debits 9,341,250 10,695,750

Enter all amounts as positive numbers. The worksheet is

formatted to add debits to assets & expenses and add credits

to revenues, liabilities & equity

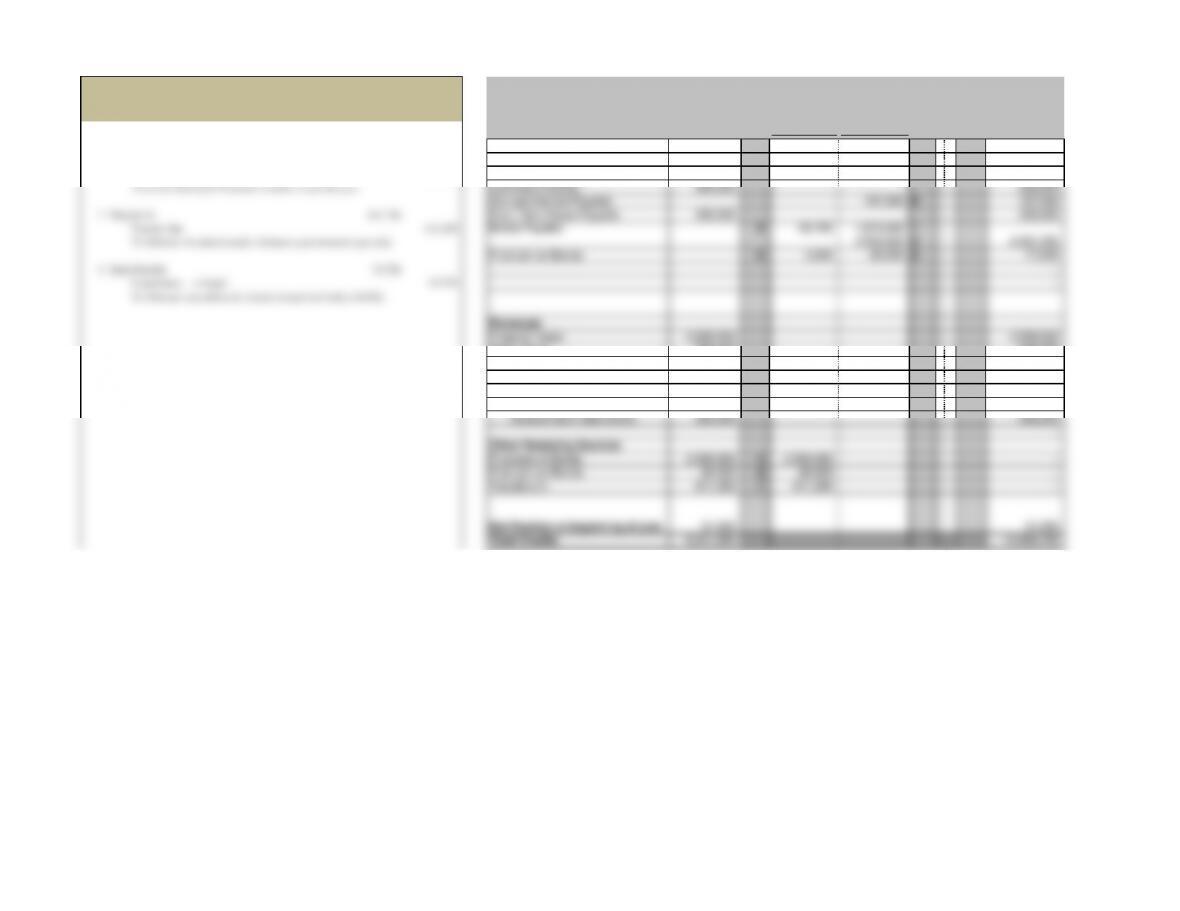

Worksheet to convert Governmental fund basis information to accrual basis

Journal Entries debits

credits

(enter as

negatives)

Gov’tal Fund

Balances

Adjustments & Eliminations

Balances for

Gov’t-wide

Stmts

1 Capital Assets 1,875,000

Debits Credits

CREDITS:

6 Interest Expense 187,500

Accounts Payable 35,000 35,000

Accrued interest payable 187,500 Due to Other Funds 115,000 115,000

To accrue interest for 9 months on bonds issued this year Contracts Payable 400,000 400,000

Accrued Interest Payable 187,500 6187,500

7 Transfer In 611,250

Short Term Notes Payable 300,000 300,000

Transfer Out 611,250 Bonds Payable 893,750 1,875,000 1

To eliminate interfund transfers (between governmental type only) 2,500,000 44,281,250

Premium on Bonds 53,000 80,000 477,000

8 Bond Payable 93,750

–

Expenditures – principal 93,750 –

To eliminate expenditure for bond principal and reduce liability

Revenues

Property Taxes 3,589,000 3,589,000

Sales Taxes 838,000 838,000

Interest –

Fees, Licenses & Permits 312,000 312,000

Miscellaneous 80,000 80,000

Intergovernmental Grant for –

General Gov’t Operations 450,000 450,000

–

Other Financing Sources

Proceeds of Bonds 2,500,000 42,500,000 –

Premium on Bonds 80,000 480,000 –

Transfers In 611,250 7611,250 –

Net Position at beginning of year 31,000 31,000

Total Credits 9,341,250 10,695,750

Journal Entries debits

credits

(enter as

negatives)

Gov’tal Fund

Balances

Adjustments & Eliminations

Balances for

Gov’t-wide

Stmts

1 Capital Assets 1,875,000

Debits Credits

column totals for JE’s 6,836,000 6,836,000

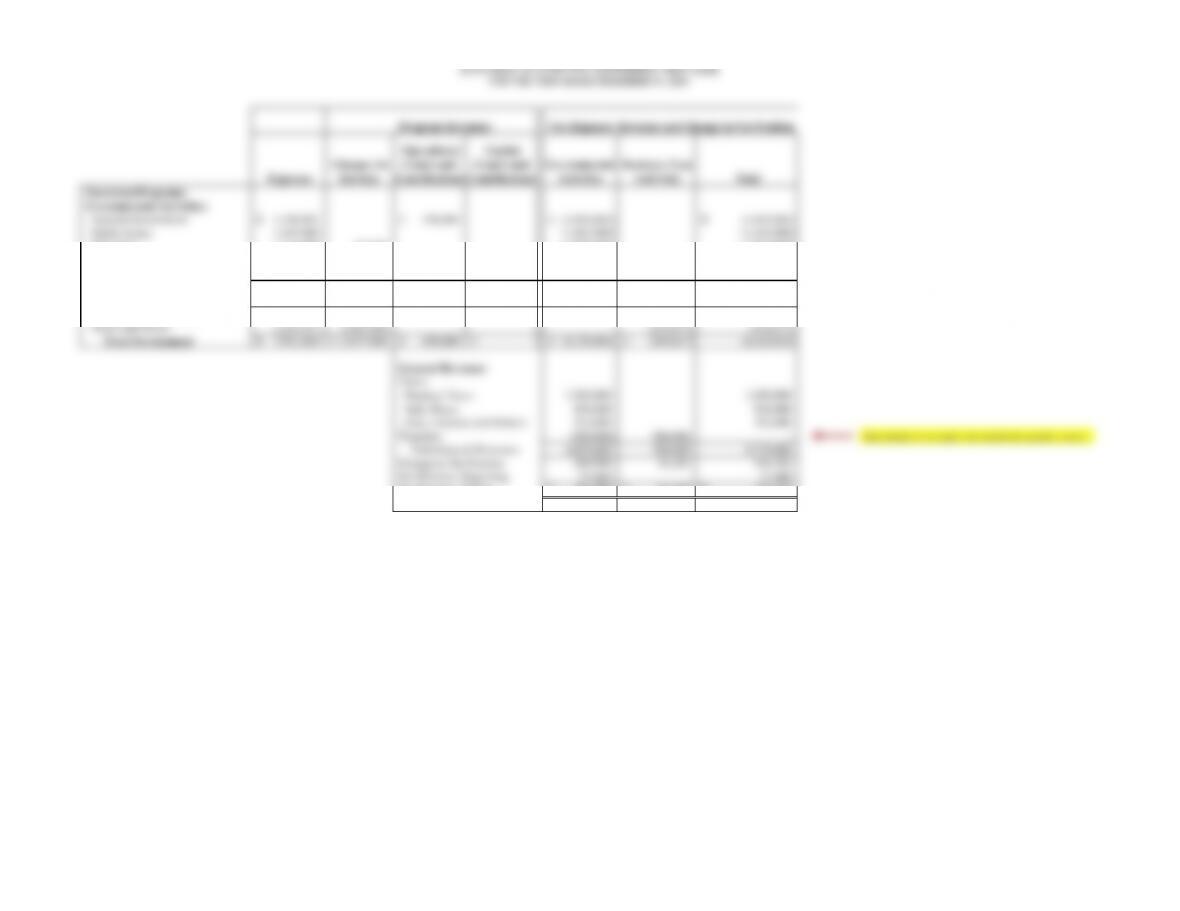

PROVINCE OF EUROPA

STATEMENT OF ACTIVITIES GOVERNMENT-WIDE BASIS

FOR THE YEAR ENDED DECEMBER 31, 2091

PROVINCE OF EUROPA

STATEMENT OF NET POSITION

AS OF DECEMBER 31, 2091

Governmental

Activities

Business-Type

Activities

Total

Assets

Cash 2,123,249$ 69,500$ 2,192,749$

Accounts Receivable (Net) 272,600 272,600

Taxes Receivable (Net) 559,000 559,000

Internal Balances Current (115,000) 115,000 – Enter payables to other funds as negative, receivables as positve amounts

Inventories 116,000 14,000 130,000

Capital Assets, Net of Accumulated Depreciation 2,889,500 1,895,583 4,785,083

Total Assets 5,572,749$ 2,366,683$ 7,939,432$

Liabilities

Accounts Payable 35,000 55,000 90,000

Contracts Payable 400,000 232,500 632,500

Accrued Interest Payable 187,500 125,000 312,500

Short Term Notes Payable 300,000 650,000 950,000

General Obligation Bonds Payable 4,281,250 1,250,000 5,531,250

Premium on Bonds Sold 77,000 77,000

Total Liabilities 5,280,750 2,312,500 7,593,250

Net Position

Net Investment in Capital Assets (1,468,750) 645,583 (823,167)

Unrestricted 1,760,749 (591,400) 1,169,349

Total Net Position 291,999$ 54,183$ 346,182$

Page 5