1) The single audit requirements apply only to state and local governments. Private

not-for-profits do not have to comply with these requirements, even if they receive

federal grants.

2) For most state and local governments, the budget, when adopted according to

procedures specified by state laws, is not binding upon the administrators of a

governmental unit.

3) The category other financing sources includes transfers from other funds, but not

bond issue proceeds.

4) GASB requires that general fixed assets acquired through General, special revenue or

capital projects funds be included in the government-wide financial statements.

5) The Balance Sheet and the Statement of Revenues, Expenditures, and Changes in

Fund Balances are required for Proprietary funds.

6) When preparing the Statement of Cash Flows for a private not-for-profit

organization, the direct method or indirect method may be used.

7) Governments should report the net pension liability in the governmental fund basis

statements even if it is not expected to be paid from current financial resources.

8) Private not-for-profits use the modified accrual basis and do not record fixed assets

or long-term debt.

9) Budgets are typically recorded for Debt Service Funds.

10) Because debt service and permanent funds use modified accrual accounting, these

funds would typically record encumbrances.

11) The City of Thomasville maintains its books so as to prepare fund accounting

statements and prepares worksheet adjustments in order to prepare government-wide

financial statements. Required: You are to prepare, in journal form, worksheet

adjustments for each of the following situations.

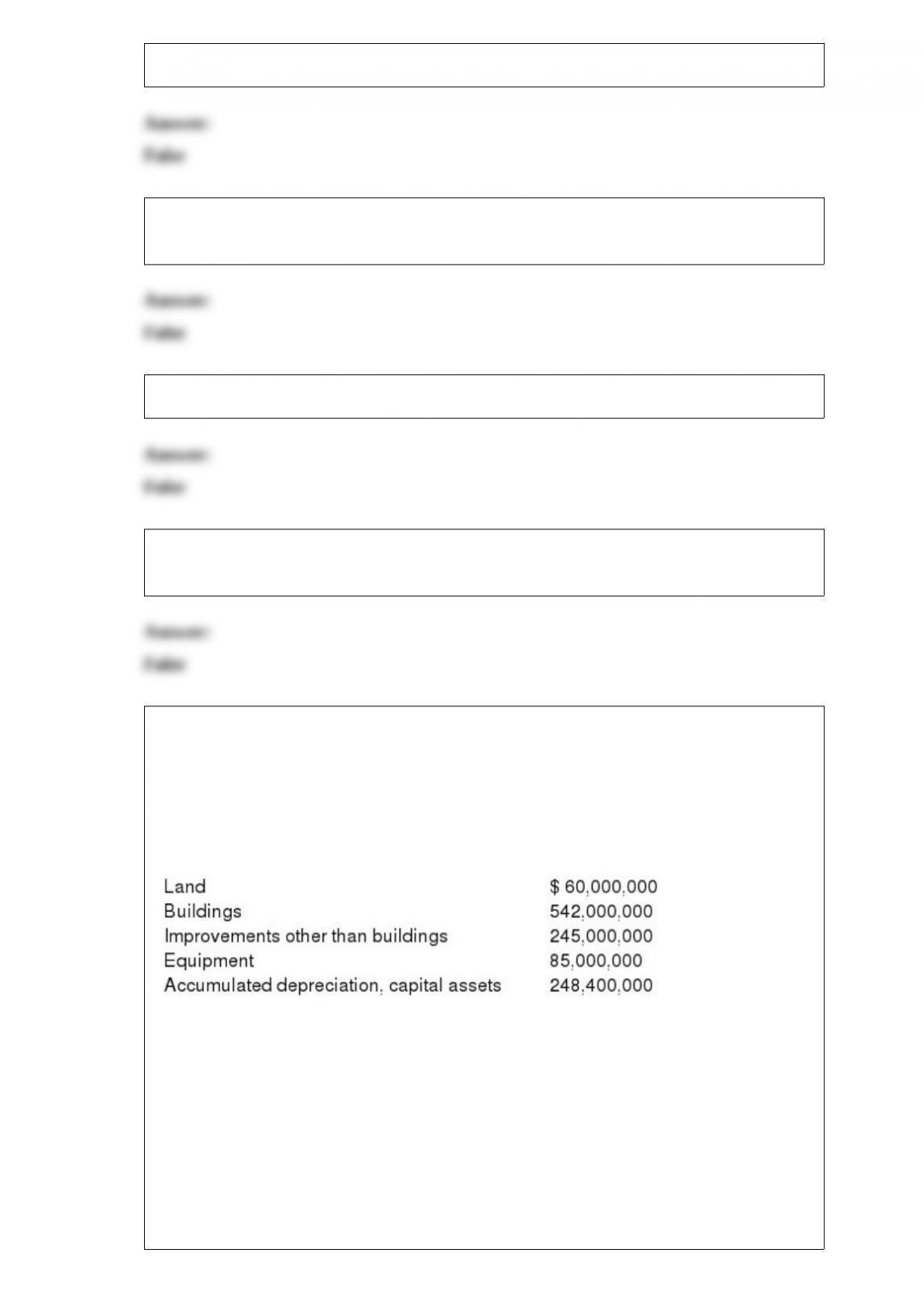

A.General fixed assets, as of the beginning of the year, which had not been recorded,

were as follows:

B.During the year, expenditures for capital outlays amounted to $14,250,000. Of that

amount, $11,900,000 was for buildings; $1,950,000 was for improvements other than

buildings, $ 10,000 was capitalized interest and the remainder was for land.

C.The capital outlay expenditures outlined in (B) were completed at the end of the year

(no depreciation until next year). For purposes of financial statement presentation, all

capital assets are depreciated using the straight-line method, with no estimated salvage

value. Estimated lives are as follows: buildings, 50 years; improvements other than

buildings, 20 years; equipment, 10 years.

D.Equipment with a cost of $ 90,000 and accumulated depreciation at the time of sale

of $60,000 was sold for $25,000.

12) With respect to the preparation of fund basis financial statements, governmental

funds other than the General Fund are considered to be major when which of the

following conditions exist?

A)With respect to fund basis financial statements, governmental funds are considered to

be a major fund when total assets, liabilities, revenues, or expenditures of that

individual governmental fund constitutes 10% of the total for the governmental fund

category

B)With respect to fund basis financial statements, governmental funds are considered to

be a major fund when total assets, liabilities, revenues, or expenditures of that

individual governmental or enterprise fund are 5% of the total of the governmental and

enterprise categories, combined

C)Both A and B are required for a governmental fund to be a major fund

D)Either A or B would fulfill the requirements

13) Which of the following are the governmental funds?

A)General, special revenue, debt service, capital projects, private purpose

B)General, special revenue, debt service, capital projects, permanent

C)General, special revenue, debt service, capital projects, internal service

D)None of the above

14) Which of the following is True regarding accounting for investments of permanent

funds?

A)Gains and losses on investments would not be reported in the Governmental Funds

Statement of Revenues, Expenditures, and Changes in Fund Balances but are reported

in the government-wide Statement of Activities

B)Investments with determinable fair values must be reported at fair value

C)Both of the above are True

D)Neither of the above is True

15) Under which fund type would you debit expenditure when land is acquired?

A) Proprietary

B) Governmental

C) Both of the above

D) None of the above

16) Which of the following statements is True of a special-purpose government?

A)Special-purpose governments that are engaged in more than one governmental-type

activities can combine the fund and government-wide financial statements

B)Special-purpose governments that are engaged in a single governmental-type

activitymay combine the fund and government-wide financial statements

C)Special-purpose governments engaged in only one business-type activity have to

prepare government-wide financial statements

D)Special-purpose governments must be stand-alone local governments

17) Internal service funds are most commonly reported in which section of the

Government-wide financial statements?

A) Governmental Activities

B) Business-type Activities

C)Component Unit

D) None of the above

18) An endowment to support scholarships would most likely be accounted for in which

of the following fund types?

A) Agency Fund

B) Investment Trust Fund

C) Private-Purpose Trust Fund

D) None of the Above

19) Which organization promulgates the Government Auditing Standards?

A)The American Institute of Certified Public Accountants

B)The U.S. Office of Management and Budget

C)The U.S. Government Accountability Office

D)The U.S. Congressional Budget Office

20) A private university billed $20,000,000 in tuition and fees during an academic year.

Graduate assistantships, for which services were required, were awarded in the amount

of $1,200,000. Scholarships, for which no services were required, were awarded in the

amount of $1,400,000. Provision for bad debt was estimated to be $2,000,000. The net

tuition and fees that would be reported in the Statement of Activities would be:

A)$18,000,000

B)$16,800,000

C)$16,600,000

D)$15,400,000

21) Which of the following would be accounted for as a permanent fund?

A)An intergovernmental grant of $500,000 to a city to be used for low income housing

B)A gift of $500,000 to a city, to be invested permanently, with the proceeds to be

distributed as scholarships

C)A gift of $500,000 to a city, to be invested permanently, with the proceeds to be used

to maintain the city cemetery

D)A gift of $500,000 to a city to be used for a new caretakers residence at the local

cemetery

22) A city government sells police cars no longer in use. No restrictions have been

placed on the proceeds. Which fund should account for the receipt?

A)General fund

B)Capital projects fund

C)Enterprise fund

D)Debt service fund

23) Which of the following would be found in an Enterprise Fund Financial Statement?

A) Expenditure Supplies

B) Reserve for Encumbrance

C) Appropriations

D) Depreciation Expense

24) Governmental funds use the:

A)economic resources measurement focus and accrual basis of accounting

B)current financial resources measurement focus and accrual basis of accounting

C)economic resources measurement focus and modified accrual basis of accounting

D) current financial resources measurement focus and modified accrual basis of

accounting

25) Which of the following is True concerning tax-exempt organizations with unrelated

business income?

A)They may deduct the first $1,000 of unrelated business income

B)They must include income from donated merchandise

C)They must include investment income in computing their tax liability

D)None of the above

26) The modified approach for infrastructure requires schedules and disclosures to be

included in which part of the CAFR?

A) Notes to the Financial Statements

B)Other Supplementary Information

C) Required Supplementary Information

D) Proprietary Fund Statements

27) Which of the following results in an encumbrance?

A)Place a purchase order

B)Receive goods previously ordered

C)Receive an invoice on goods previously received

D)Payment of an invoice previously received

28) Which of the following is an example of a special-purpose government?

A)Park district

B)Village government

C)Township government

D)City government

29) Which of the following activities give rise to Unrelated Business Income Tax?

A)Investment income arising from investment of unrestricted funds

B)Business operated for the convenience of employees and patients

C)Sale of donated merchandise

D)None of the above

30) An employee enrolls in a pension plan that will pay out 3% of the employees

average salary for the last 3 years for each year of service that the employee worked.

What type of pension plan does the employee have?

A)Defined Contribution Plan

B)Normal Payout Plan

C)Defined Benefit Plan

D)None of the above

31) The program expense ratio is calculated as follows:

A)Total expenses / Program service expenses

B)Program service expenses + supporting service expenses / Total expenses

C)Program service expenses / Total expenses

D)Total expenses / (Program service expenses + supporting service expenses)

32) The term fiduciary funds applies to:

A)enterprise and internal service funds

B)pension, investment trust and enterprise funds

C)enterprise, internal service, and private-purpose trust funds

D)none of the above answers are correct

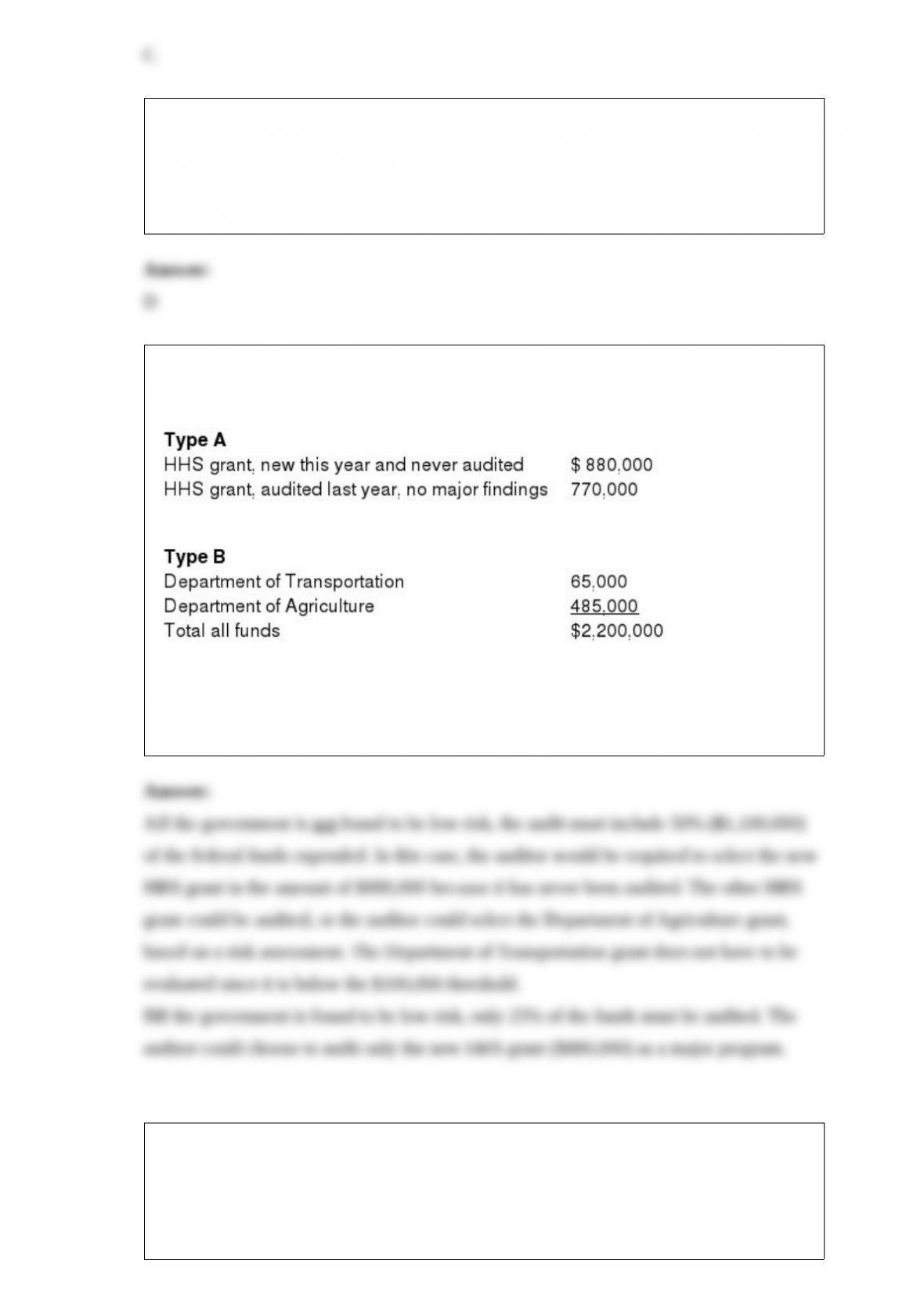

33) A local government has four federal grants. Expenditures during the year ended

June 30, 2015, are below:

A.Which grants would the auditor be required to audit, assuming the government is not

found to be low risk?

B.Which grants would the auditor be required to audit, assuming the government is

found to be low risk?

34) A local government recorded the sale of a capital asset at a gain by recording a debit

to cash and credit to proceeds of sale of capital asset. What is the worksheet entry when

preparing the government-wide statements?

A)Debit to Proceeds of sale of capital asset and credit to Gain on sale of capital asset

B)Debit to Cash and credit to capital asset (net) and credit to Gain on sale of capital

asset

C)Debit to Proceeds of sale of capital asset and credit to capital asset (net) and Gain on

sale of capital asset

D)None of the above

35) The Town of Little River expects to collect $90,000 in sales tax from the state

government within 30 days of the end of fiscal year 2015 for retail sales taking place in

fiscal year 2015 . What entry, if any, would Little River make at the end of 2015?

A)Taxes receivable current90,000

Deferred Inflows90,000

B)Taxes receivable deferred90,000

Revenues control90,000

C)Taxes receivable current90,000

Due from state government90,000

D)Due from state government90,000

Revenues control90,000

36) Which of the following is not True of a Statement of Activities prepared for a

private not-for-profit organization?

A)Expenses are shown only as decreases in unrestricted net assets

B)Reclassifications for expiration of time restrictions are shown in the revenues and

support section

C)Unrealized gains (losses) on investments are shown only as increases (decreases) in

unrestricted net assets

D)Expenses are classified by function within the categories of Program Services and

Supporting Services either in the Statement or the notes

37) A local government was awarded a federal grant in the amount of $950,000 to

provide for a summer youth employment program for young people. The grant was a

reimbursement grant, and a notification of the grant award was received on Apri1 30,

2015 . The local government expended the resources as follows:

June 2015: $400,000;

July2015: $300,000;

August 2015: $250,000.

The federal government sent the funds in the month following the expenditure. The

local government would recognize revenues for the fiscal year ended June 30, 2015 in

which amount?

A)$ -0-

B)$400,000

C)$700,000

D)$950,000

38) During the fiscal year ended December 31, 2015, the City of Johnstown issued 6%

general obligation serial bonds in the amount of $2,000,000 at 102 ($2,040,000) and

used $1,980,000 of the proceeds to construct a fire station. The $40,000 premium was

transferred to a debt service fund. The $20,000 left in the capital projects fund at the

end of the project was later transferred to the debt service fund. The bonds were dated

April 1, 2015 and paid interest on October 1 and April 1 . The first of 10 equal annual

principal payments was due on April 1, 2016 .

The amount of capital outlay expenditures reported by the capital projects fund would

be:

A)$1,980,000

B)$2,000,000

C)$2,040,000

D)$3,000,000

39) The ______ Funds are used when resources are provided primarily through the use

of sales and service charges to parties external to the government and it is the intent of

the government to measure revenues, expenses and changes in net position.

A) Agency

B) Enterprise

C) General

D) Special revenue

40) A governmental funds Statement of Revenues, Expenditures, and Changes in Fund

Balances reported expenditures for capital outlay in the amount of $5,000,000. Capital

assets for that government cost $110,000,000, including $20,000,000 in land.

Depreciable assets are amortized over 20 years, on average. The reconciliation from the

governmental funds changes in fund balances to the governmental activities change in

Net Position would reflect a(an):

A)Increase of $250,000

B)Decrease of $250,000

C)Increase of $500,000

D)Decrease of $500,000

41) If the receivable for a student is $8,000 and the student pays only $500 as the result

of receiving an athletic scholarship from the school, what would be the appropriate

debits

A) Debit Cash

B) Debit Cash and Debit Expense

C) Debit Expense

D) Debit Cash and Debit Tuition Discount on Accounts Receivable

42) Which of the following is True regarding the government-wide statements?

A)The governmental activities portion of the government-wide statements is prepared

using the current financial resources measurement focus and modified accrual basis of

accounting

B)The government-wide statements include a Statement of Net Position and a

Statement of Activities

C)Both of the above

D)Neither of the above

43) Which of the following is True regarding the recording of long term debt in an

enterprise fund?

A)When revenue bonds are sold at par, Cash is debited and Bonds Payable is credited

B)The bonds would be reported in both an enterprise fund and in the government-wide

statements

C)Both of the above

D)Neither of the above

44) Depending upon the circumstances, in practice public colleges and report as special

purpose entities engaged in:

A)Business-type activities only

B)Both governmental and business-type activities

C)Governmental activities only

D)Any one of the above

45) When a purchase order is issued under a Capital Projects fund, how should the

transaction be recorded?

A)Debit Expenditures and credit Budgetary Fund Balance — Reserve for Encumbrances

B)Debit EncumbrancesControl and credit Budgetary Fund Balance — Reserve for

Encumbrances

C)Debit Expenditures and credit Vouchers payable

D)Debit Encumbrances Control and credit Vouchers payable

46) Which of the following is True regarding the government-wide statements?

A)Balances from enterprise funds statements are entered in the business-type activities

sections of the government-wide statements without adjustment

B)Government-wide statements eliminate inter fund transactions, within columns

C)Both of the above

D)Neither of the above

47) Which of the following is not a distinguishing characteristic of a private

not-for-profit organization according to FASB Statement No. 116?

A)Operating purposes other than to provide goods or services at a profit

B)Absence of ownership interests like those of business enterprises

C)Commonly financed through voluntary contributions

D)Operate for the direct benefit of members

48) Which of the following steps in the budgetary authority process occurs when the

Office of Management and Budget establishes the quarterly amount available to a

federal agency for spending?

A)Apportionment

B)Appropriation

C)Allotment

D)Obligation

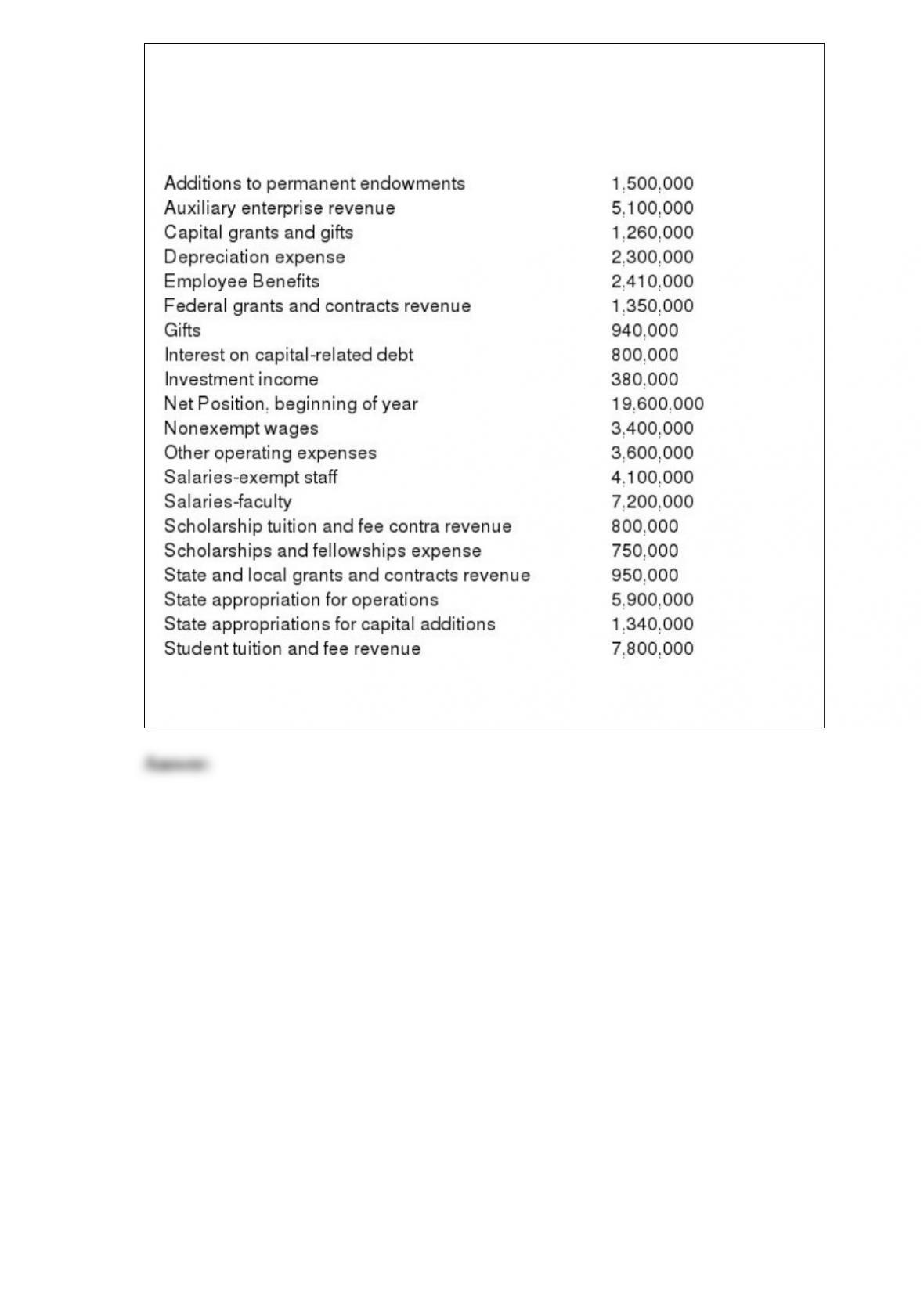

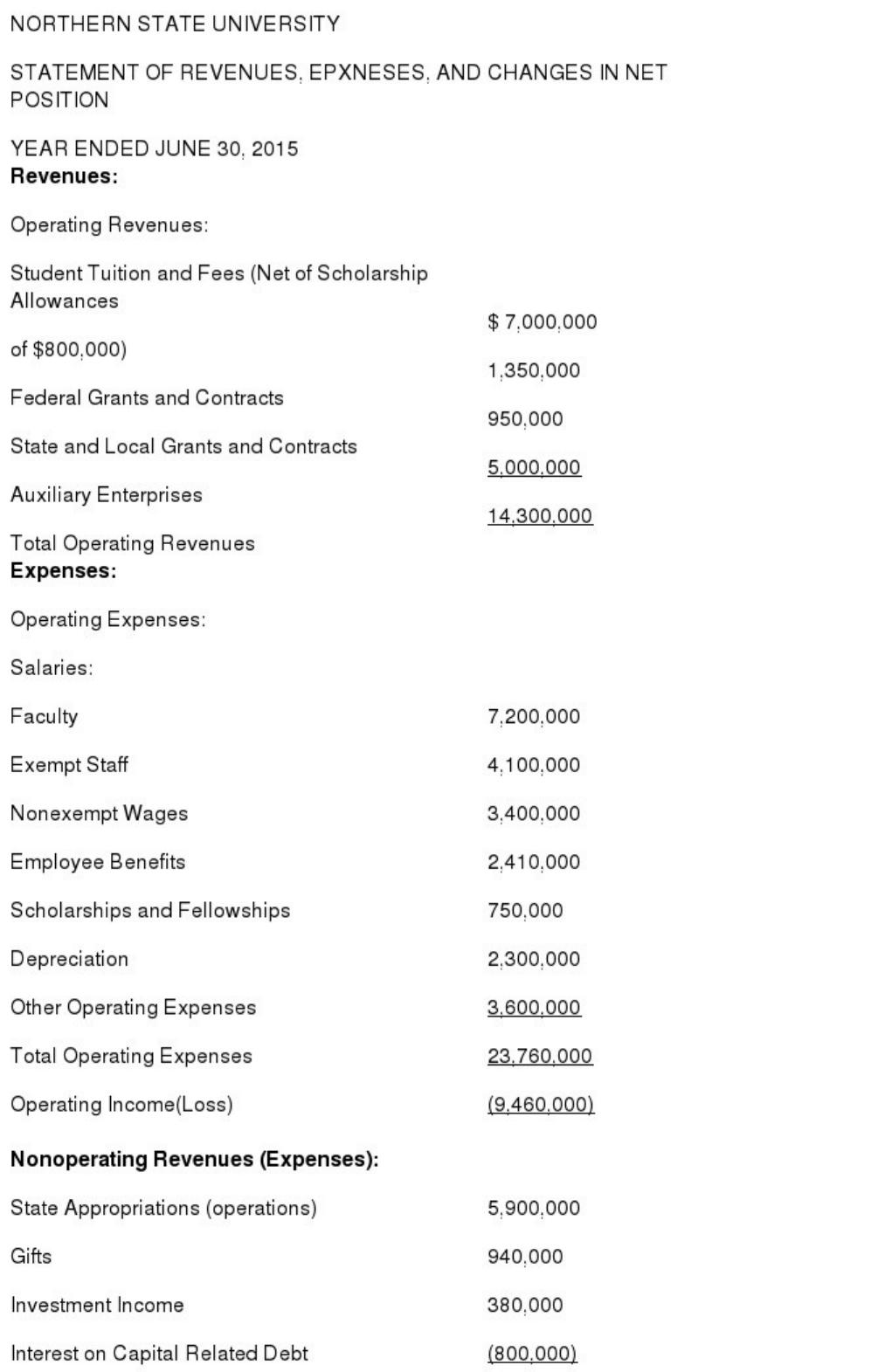

49) Northern State University had the following account balances for the year ended

and as of June 30, 2015. Debits are not distinguished from credits, so assume all

accounts have a normal balance.

Required: Prepare, in good form, a Statement of Revenues, Expenses, and Changes in

Net Position for Northern State University for the year ended June 30, 2015 .

50) List and describe the three major sections of the Comprehensive Annual Financial

Report and indicate briefly what is in each.

51) Describe the types of audit opinions that may be issued on a governmental or

not-for-profit financial report.

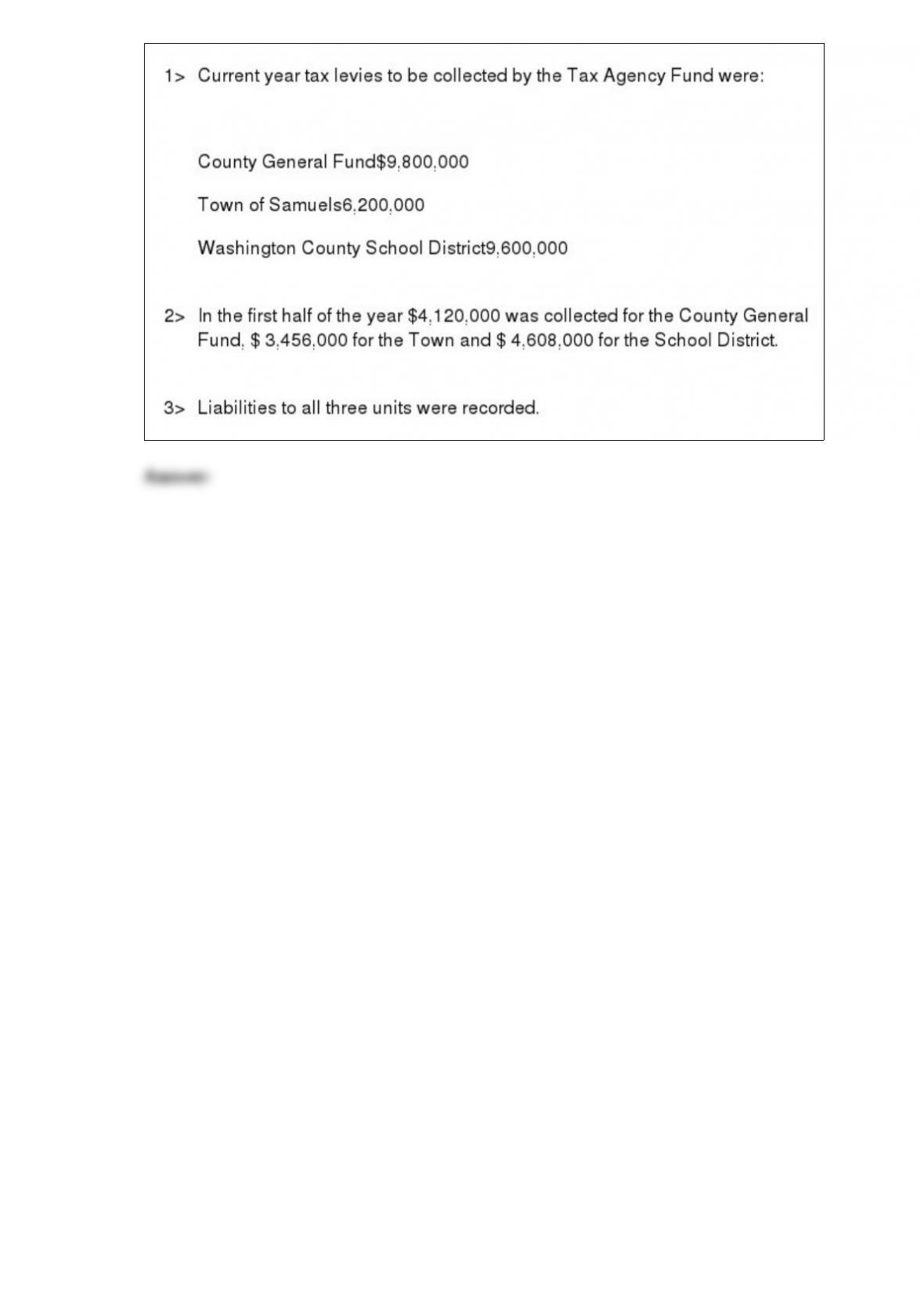

52) Washington County assumed the responsibility of collecting property taxes for all

governments within its boundaries. In order to reimburse the county for expenditures

for administering the Tax Agency Fund, the Tax Agency Fund is to deduct 1.5 percent

from the collections from the city and school district. The total amount deducted is to be

added to the collections for the county and remitted to the County General Fund. You

are to record the following transactions in the accounts of the Washington County Tax

Agency Fund.

53) In its Statement of Financial Accounting Concepts #4, the FASB identifies the

information needs of the users of non-business financial statements. These include

providing information that is useful to present and potential resource providers in which

four evaluation areas?

54) What are the revenue and expenditure recognition criteria under modified accrual

accounting? Include in your answer specifically the recognition of property tax revenue.

55) List and explain the five ethical concepts outlined by the Yellow Book.

56) Under GASB Statement 34, enterprise funds must be used under which

circumstances?

57) On 9/1/2015Birmingham County sold bonds at par value in the amount of

$12,000,000 to finance construction of a new library. On 10/10/2015 Hills County

entered into a contract with a private contractor to build a new library building in the

amount of $11,000,000. On 12/1/2015, when the contract was half finished, the

contractor submitted a bill for $5,500,000. The bill was paid on 12/15/2015 less Hills’

standard 5% retention to assure any construction deficiencies are corrected. Hills

County operates on a Dec. 31 fiscal year.

Required: Prepare the journal entries required in the Capital Projects Fund for the above

transactions.

58) List and define the five classifications of governmental funds.