1) Special-purpose governments engaged in business type activities only are required to

prepare both proprietary fund and government-wide financial statements.

2) The Single Audit Actis intended to provide assurance to the federal government that

federal funds are protected through a system of internal controls and sound financial

management practices.

3) Private, Not-for-Profit Colleges and Universities must have Statement of Financial

Position, Statement of Activities, Statement of Cash Flows, and Notes to the Financial

Statements included in their financial report.

4) According to GASB Statement 34, governmental activities are generally financed

through taxes, intergovernmental revenues and other nonexchangerevenues.

5) Capital project funds exist for the duration of the project for which it is created and

are then closed.

6) The purpose of the Unrelated Business Income Tax is to eliminate advantages that

tax-exempt organizations have over commercial enterprises providing goods or services

for sale.

7) Private colleges and universities are required to report net assets within the

categories of unrestricted, temporarily restricted and permanently restricted.

8) Prior-year data are required to be presented on government-wide statements

9) Budgets are typically not recorded for Special Revenue Funds.

10) Entities which are determined to be component units of state and local

governmental units must be discretely presented in the financial statements.

11) Net Assets must be presented separately in the Statement of Activities for the three

classes (unrestricted, temporarily restricted, and permanently restricted).

12) Fiduciary fund statements are prepared using the current financial resources

measurement focus and modified accrual basis of accounting.

13) Centralized purchasing, computer services, and janitorial services are examples of

activities that are commonly reported in:

A) Enterprise funds

B) Capital project funds

C) Debt service funds

D) Internal service funds

14) The two types of proprietary funds include:

A)Enterprise funds and capital projects funds

B)Enterprise funds and internal service funds

C)Internal service funds and capital project funds

D)Agency funds and enterprise funds

15) Which of the following is True regarding the Comprehensive Annual Financial

Report (CAFR)?

A)The CAFR has three main sections: introductory, financial, and statistical

B)Required Supplementary Information includes a Budgetary Comparison Schedule for

the General Fund and all major special revenue funds that have a legally adopted annual

budget (unless a statement is prepared)

C)Both of the above

D)Neither of the above

16) Indicate the financial reporting rules for each of the following special-purpose

entities (which category of special-purpose entity), and indicate the financial statements

that would be required:

a.A township that assesses property for taxation, provides road maintenance, and

provides welfare assistance.

b.A fire protection district that engages in protection of property in unincorporated areas

from fires.

c.An independent tollway authority, not the component unit of any other government.

d.An independent statewide pension plan.

e.A public college.

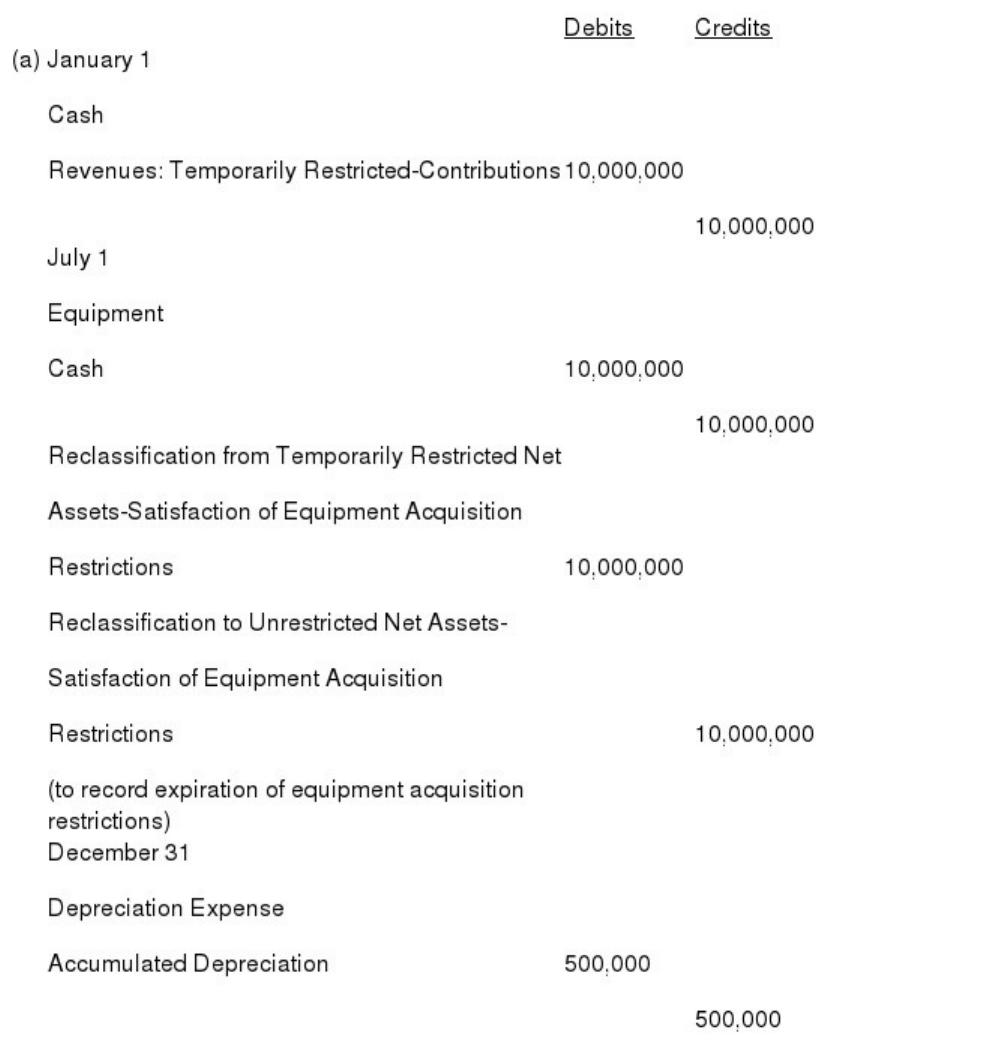

17) On January 1, 2015, Antioch College, a private not-for-profit college, received

$10,000,000 in cash to purchase an electron microscope. The microscope was delivered

on July 1, 2015 and payment was made. The microscope is expected to last 10 years

and has no salvage value at the end of that time. The fiscal year end is December 31 .

a.Record the journal entries required on January 1, July 1, and December 31, 2015 to

record the receipt of the cash, the purchase of equipment, and one-half year’s

depreciation, assuming the plant assets are recorded as unrestricted assets at the time of

purchase.

b.Record the journal entries required on January 1, July 1, and December 31, 2015 to

record the receipt of the cash, the purchase of equipment, and one-half year’s

depreciation, assuming the plant assets are recorded as temporarily restricted assets at

the time of purchase.

18) Which of the following is True regarding the Budgetary Comparison Schedule?

A)The Budgetary Comparison Schedule compares the actual results to the original

budget, but display of variances is optional

B)The Budgetary Comparison Schedule is considered part of the basic financial

statements

C)The Budgetary Comparison Schedule must be prepared for the General Fund and

each major special revenue fund that has a legally adopted budget

D)Both (A) and (C) are True

19) A private foundation made a multi-year pledge to a private college on December 31,

2014, the last day of the fiscal year. The pledge was to pay $15,000 per year each year

for five years, beginning on December 31, 2015 . The discount rate is 6%. The present

value of five payments of $15,000 is $63,185. The present value of four payments of

$15,000 is $51,977. No purpose or plant restrictions were involved.

The private college would:

A)Record contribution revenue in the amount of $15,000 in each of the years 2015,

2015, 2015, 2015 and 2016

B) Record contribution revenue in the amount of $63,185 in 2014

C)Record contribution revenue in the amount of $51,977 in 2015

D)None of the above

20) Which of the following use current financial resources measurement focus?

A) Fiduciary fund statements

B)Governmental fund statements

C)Proprietary fund statements

D)Internal Service fund statements

21) Which of the following situations would be unlikely toresult in the recognition of an

asset impairment?

A)A city warehouse is damaged by fire

B)Recently purchased city-owned voting booths are rendered obsolete by a federal law

requiring a new technology

C)Ridership on city buses declines

D)Construction on a municipal sports complex stops when the citys major league

baseball team moves to another city

22) When converting to government-wide financial statements, the entry to record the

amortization of the premium on a bond would:

A) Debit the Premium on bonds payable and a credit premium expense

B)Debit the Bond Payable and a credit Premium on bonds payable

C)Debit the Premium on bonds payable and a credit interest expense

D) There is no entry. You do not amortize the premium

23) James McHughes gave the following to the City of Carnesville in order to establish

a private-purpose trust:

oLand cost, $400,000; fair market value as of the date of the gift, $500,000.

oSecurities cost, $1,600,000; fair market value as of the date of the gift, $1,800,000.

The amount to be recorded as additions for gifts by the private-purpose trust fund

would be:

A)$2,000,000

B)$2,100,000

C)$2,200,000

D)$2,300,000

24) Churchville County is trustee for a multi-government investment pool and has

established an investment trust fund. Included in the investment trust fund, for

management purposes, are investments in the amount of $15 million from the County’s

General Fund, $3 million from the County’s special revenue funds, and $112 million

from other governments. Which of the following would be True?

A)The County would report $18 million in an investment trust fund

B)The County would report the entire $130 million in an investment trust fund

C)The County would report the $112 million in an investment trust fund, the $15

million in its General Fund, and the $3 million in special revenue funds

D)The County would report the $112 million in an investment trust fund and the$18

million in a permanent fund

25) With respect to public colleges and universities, state appropriations for operating

purposes are shown as:

A)Non-operating revenue

B)Operating revenue

C)Non-expendable endowments

D)None of the above

26) Currently, a single audit is required for organizations receiving what amount of

federal funds?

A)> $100,000

B)> $300,000

C)> $500,000

D)> $700,000

27) A donor made an unconditional pledge in 2014 of $ 50,000 to a private

not-for-profit organization with the intent to pay the cash in 2015 for unrestricted use in

2015 . The organization should:

A)Record the pledge receivable and deferred revenue in 2014

B)Record the pledge as temporarily restricted revenue in 2014 and reclassify it to

unrestricted in 2015

C)Record the pledge as unrestricted revenue in 2014

D)Record the pledge as temporarily restricted revenue in 2014 and reclassify it to

unrestricted in 2015, but only in an amount equivalent to the amount that is spent in

2015

28) Which of the following is not required to convert from the modified accrual basis to

the accrual basis in preparing the government-wide statements?

A)Record general capital assets

B)Change expenditures for debt service principal to reduction of liabilities

C)Make adjustments to revenues deferred under the 60 day rule

D)Accrue interest on enterprise fund bonds

29) Which of the following is True regarding Service Efforts and Accomplishments

Reporting?

A)SEA reporting utilizes both financial and non-financial performance measures

B)GASB standards require the reporting of service efforts and accomplishments for

public school systems

C)Service efforts and accomplishments reporting is commonly covered by the auditors

opinion

D)All of the above

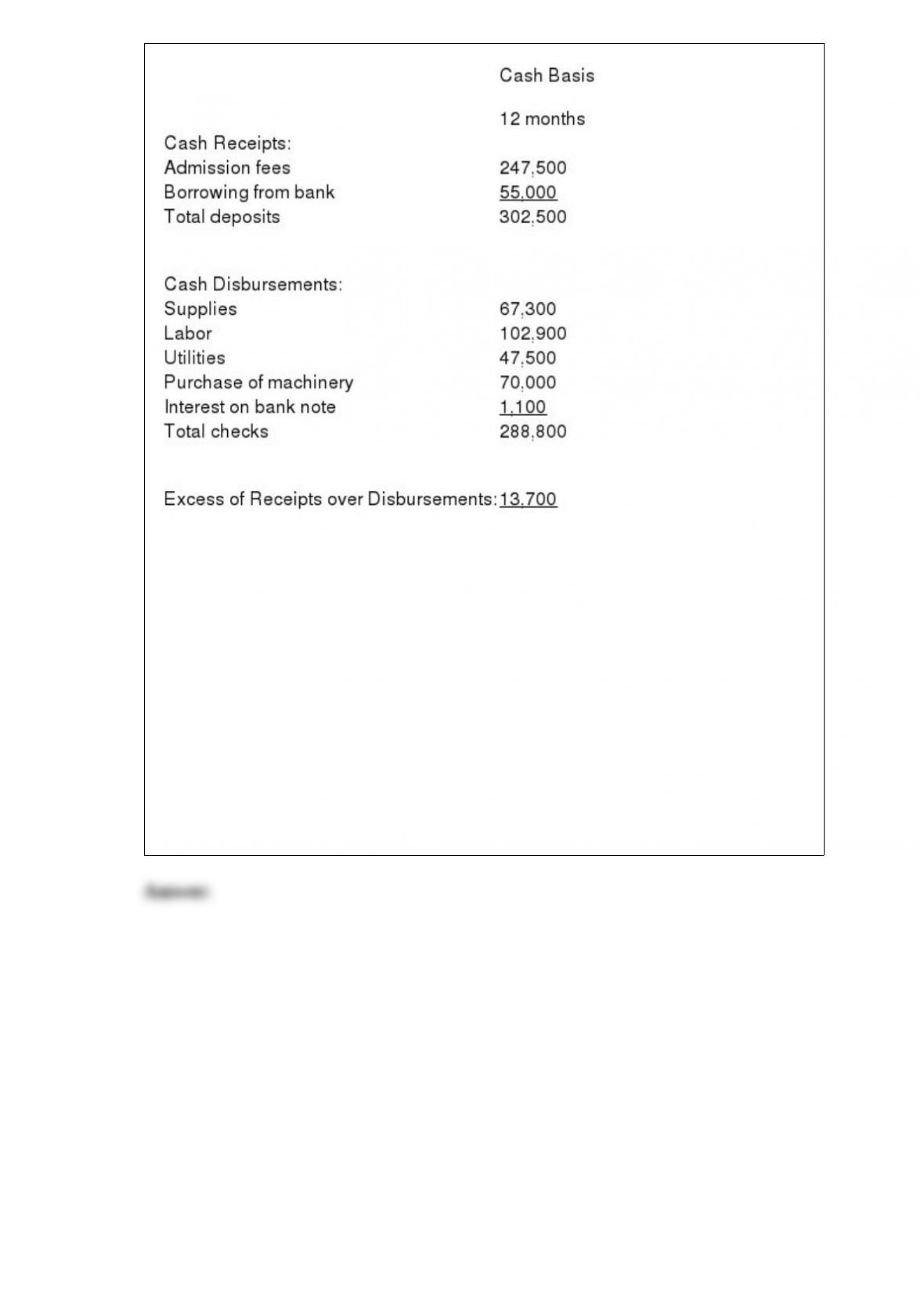

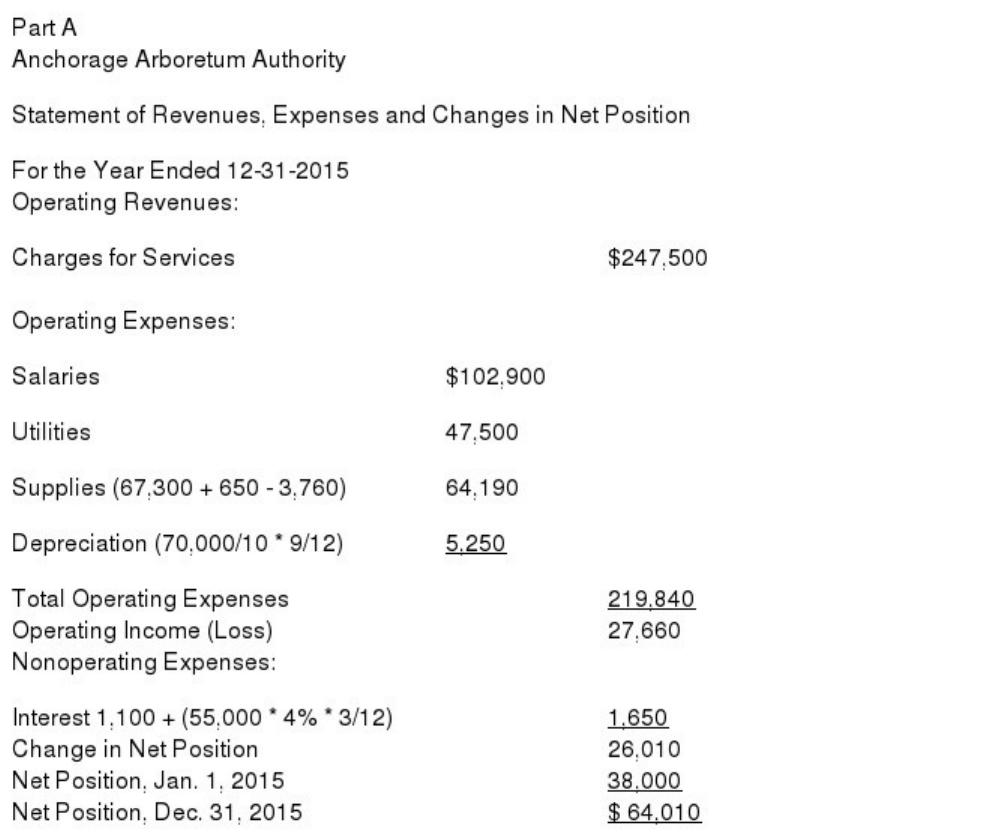

30) The following Statement of Cash Receipts and Disbursements was prepared by the

bookkeeper of The Anchorage Arboretum Authority. The Arboretum Authority is a

component unit of the City of Anchorage and must be included in the City’s financial

statements. It began operations on January 1, 2015 with no outstanding liabilities or

commitments and only 2 assets:(1) $15,000 cash and (2) land that it had paid $ 23,000

to acquire.

The loan from the bank is dated April 1 and is for a five year period. Interest (4%

annual rate) is paid on Oct. 1 and April 1 of each year, beginning October 1, 2015 .

The machinery was purchased on April 1 with the proceeds provided by the bank loan

and has an estimated useful life of 10 years. (straight-line basis)

Supplies on hand amounted to $ 3,760 at December 31, 2015 . These included $650 of

fertilizer that was received on December 29 and paid in January 2015 . All other bills

and salaries related to 2015 had been paid by close of business on December 31 .

Required:

Part A.Prepare a Statement of Revenues, Expenses and Changes in Net Position for the

year ended 12-31-09 for the Arboretum assuming the City plans to account for its

activities on the accrual basis.

Part B.Prepare a Statement of Revenues, Expenditures and Changes in Fund Balance

for the year ended 12-31-09 for the Arboretum assuming the City plans to account for

its activities on the modified accrual basis.

31) St. Davids is a not-for-profit business-oriented hospital. What is the journal entry

for the following transaction: During the month, gross patient service revenue

amounted to $93,000 of which $82,000 was received in cash. Contractual adjustments

to third-party payers amounted to $10,000 (actual, not estimated).

A)Cash82,000

Patient Accounts Receivable11,000

Operating Revenues Unrestricted – Patient Service Revenue93,000

Contractual Adjustments Unrestricted10,000

Patient Accounts receivable10,000

B)Cash82,000

Patient Accounts Receivable11,000

Operating Revenues Patient Service Revenue, Restricted93,000

Bad Debts Expense Restricted10,000

Patient Accounts receivable10,000

C)Cash82,000

Patient Accounts Receivable11,000

Operating Revenues Unrestricted – Patient Service Revenue93,000

Operating Revenues-Unrestricted patient Service Revenue10,000

Patient Accounts receivable10,000

D)Cash82,000

Patient Accounts Receivable 1,000

Operating Revenues Unrestricted – Patient Service Revenue83,000

32) Assume a government is a special-purpose entity engaged in fiduciary activities

only. Which of the following financial statements would be required?

A)Statement of Fiduciary Net Position and Statement of Changes in Fiduciary Net

Position

B)Statement of Net Position and Statement of Activities

C)Statement of Net Position, Statement of Activities, Statement of Fiduciary Net

Position, Statement of Changes in Fiduciary Net Position

D)Statement of Fiduciary Net Position, Statement of Changes in Fiduciary Net Position,

and Statement of Cash Flows

33) An unrestricted balance sheet category used in health care reporting to show

limitations on the use of assets due to bond covenant restrictions and governing board

plans for future use is called:

A)Permanently restricted net assets

B)Temporarily restricted net assets

C)Assets whose use is limited

D) Unrestricted net assets

34) Which of the following is True regarding the reporting of general capital assets by

state and local governments?

A)Capital assets are reported in the government-wide Statement of Net Position

B)Capital assets are reported in the governmental funds Balance Sheet

C)Both of the above

D)Neither of the above

35) In a budgetary entry, if Appropriations Control exceeds Estimated Revenues

Control, the excess would be:

A)debited to Budgetary Fund Balance

B)credited to Budgetary Fund Balance

C)credited to Fund Balance-Unassigned

D) credited to Fund Balance-Reserved for Encumbrances

36) Care Foundation is a voluntary health and welfare organization funded by

contributions from the general public. In its Statement of Activities, the annual

provision for depreciation should:

A)Not be included

B)Be included as an element of support

C)Be included as an element of changes in fund balances

D)Be included as an element of expense

37) Which of the following fund(s) should be used if resources are provided by a donor

with the stipulation that they be used for the benefit of the citizenry?

A) Special revenue fund

B) Permanent fund

C) Private purpose fund

D) Either A or B, depending upon whether the principal must be maintained

38) An example of expenditure classification by object would be:

A) Current

B)Public safety

C)Police department

D)Salaries

39) A membership pass to the YMCA (a private not-for-profit organization) includes

unlimited rights to all facilities and a health magazine subscription. Non-members do

not possess these rights. How must the YMCA account for membership dues?

A) The dues are a non-exchange transaction, so it should report all dues in the year

received

B) The dues are a non-exchange transaction, so it should report dues on a pro-rata basis

determined by the length of the individual memberships

C) The dues are an exchange transaction, so it should report dues on a pro-rata basis

determined by the length of the individual memberships

D) The dues are an exchange transaction, so it should report all dues in the year

received

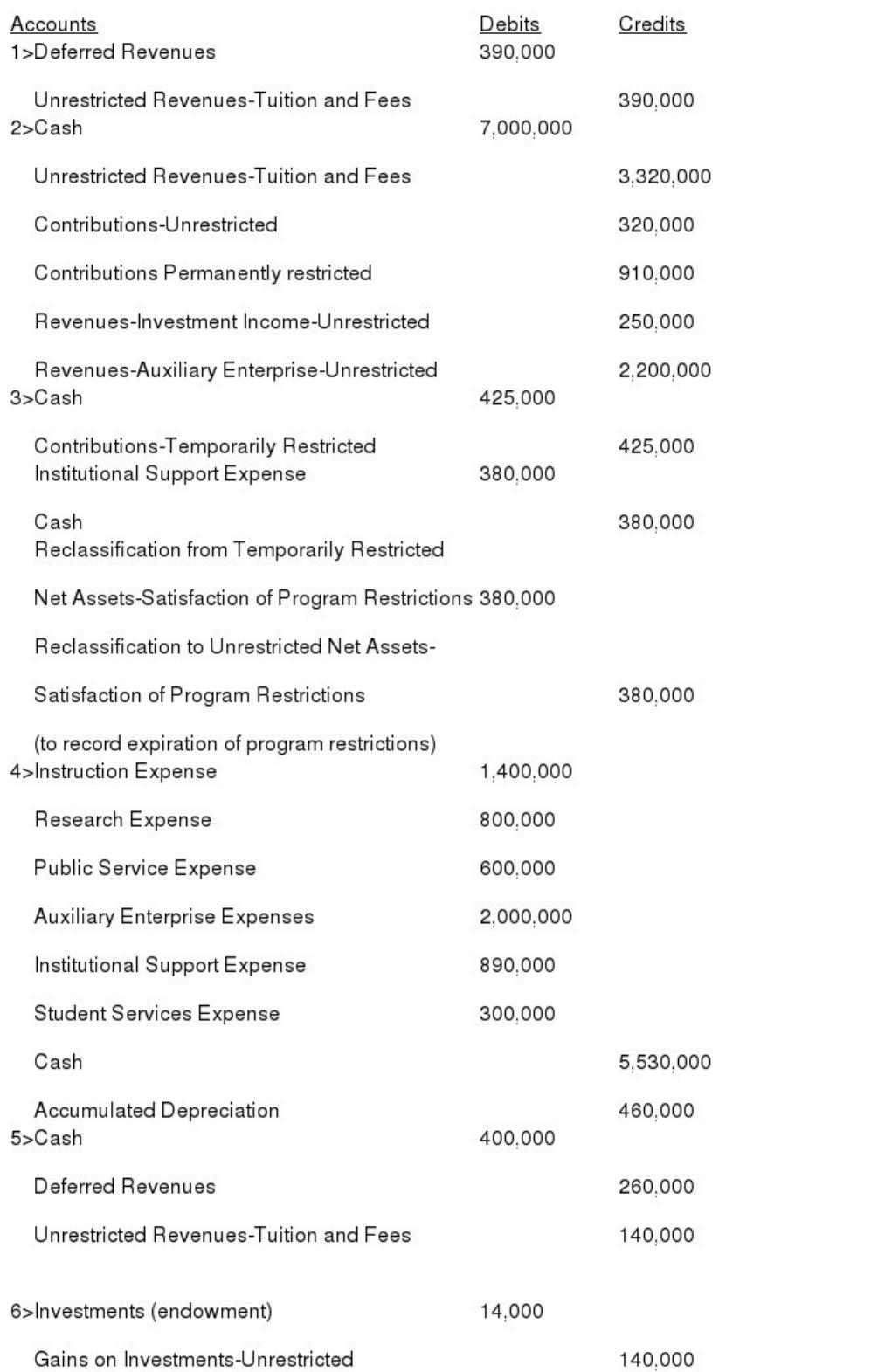

40) Ethan Allen University is a private university following FASB standards for

reporting. The following transactions took place during the year ended June 30, 2015 .

(1)EAU had received $600,000 in tuition in June 2015 for the summer session that runs

from June 16 to August 14, 2014 and had deferred $ 390,000 (65%) at June 30, 2014 .

(2)EAU received in cash tuition of $3,320,000; unrestricted contributions of $320,000;

contributions permanently restricted by donor agreement for the endowment of $

910,000, unrestricted interest income on endowments of $250,000; and auxiliary

enterprise revenue of $2,200,000.

(3)Contributions for student scholarships were received in the amount of $425,000.

$380,000 was awarded to students during the year. Students receiving these

scholarships are required to work 10 hours a week (institutional support).

(4)Expenses amounted to $1,400,000 for instruction, $800,000 for research, $600,000

for public service, $2,000,000 for auxiliary enterprises, $300,000 for student services,

and $890,000 for institutional support. Included in these amounts is $460,000 of

depreciation. All other expenses ($ 5,530,000) were paid in cash. Plant assets are

classified as unrestricted.

(5)EAU received $400,000 in tuition in mid June 2015 for the summer session ending

in mid-August2015 . (65% relates to the next fiscal year)

(6)At year-end, endowment investments were determined to have a fair value of

$14,000 in excess of their recorded amounts. No restrictions apply to this income.

Required:

(a)Prepare journal entries to record these events including closing entries.

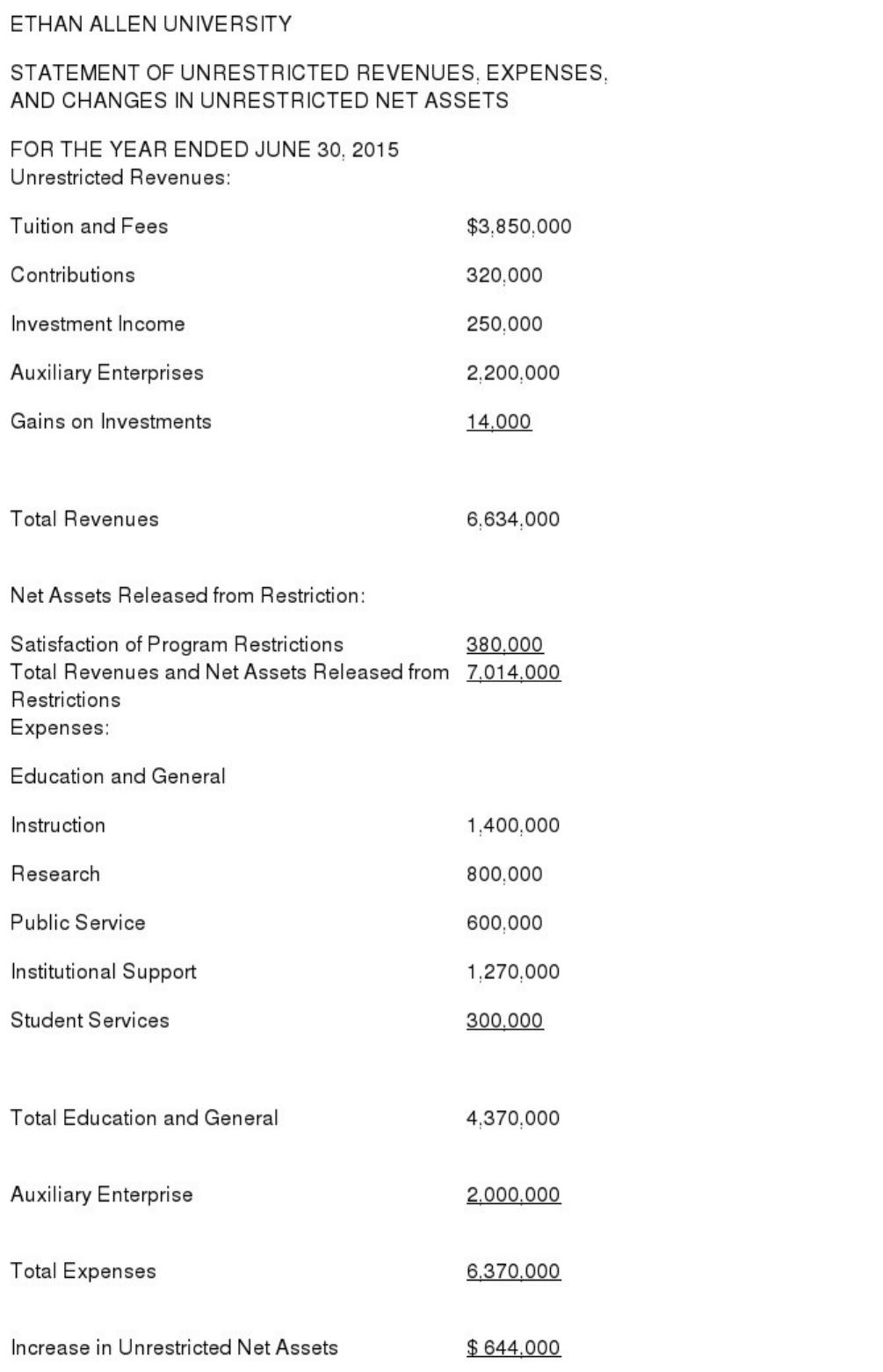

(b)Prepare a Statement of Unrestricted Revenues, Expenses and Other Changes in

Unrestricted Net Assets.

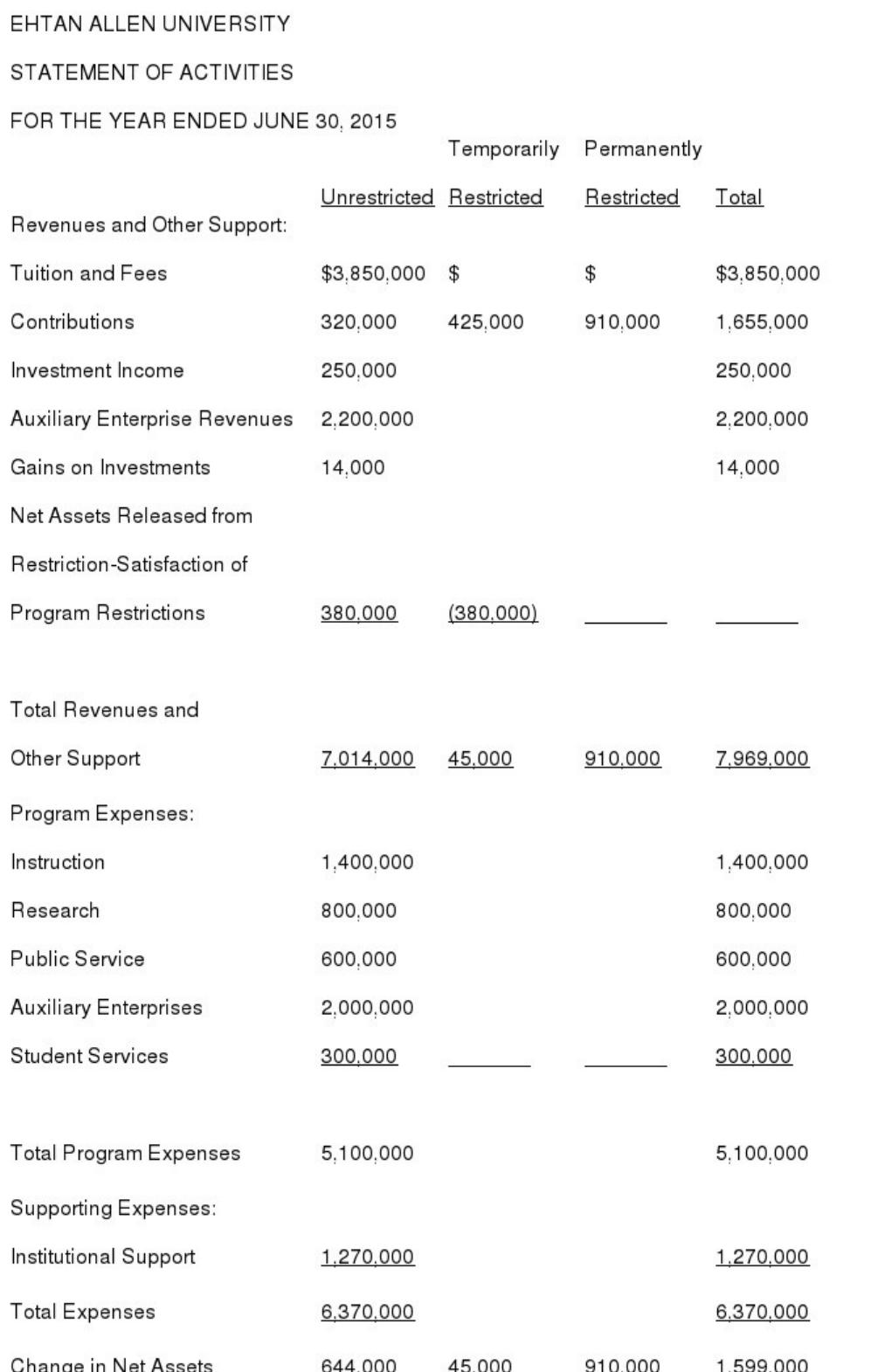

(c)Prepare a Statement of Activities for the year ending June 30, 2015, assuming the

June 30, 2014 balances in net assets are: $1,020,000 unrestricted, $30,000 temporarily

restricted, and $8,000,000 permanently restricted.

41) Expenditures are generally recorded and fund liabilities are recognized

A)When goods and services are received, but only if resources are available in the fund

B)When invoices are paid

C)When purchase orders are issued, regardless of whether or not resources are available

in the fund

D)When goods and services are received, regardless of whether or not resources are

available in the fund

42) Inter fund services purchased by the General Fund are recognized as:

A) Transfers Out

B)Decreases in Fund Balance

C)Expenditures

D)None of the above