Archives: Solution Manual

Accounting Chapter 21 The real estate broker’s fee should be capitalized

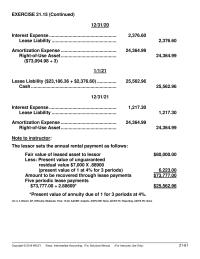

EXERCISE 21.15 (Continued) 12/31/20 Interest Expense ……………………………………………. 2,376.60 Lease Liability ………………………………………….. 2,376.60 Amortization Expense ……………………………………. 24,364.99 Right-of–Use Asset ……………………………………. 24,364.99 ($73,094.98 ÷ 3) 1/1/21 Lease Liability ($23,186.36 + $2,376.60) …………… 25,562.96 Cash ………………………………………………………… 25,562.96 12/31/21 Interest Expense ……………………………………………. 1,217.30 Lease […]

Accounting Chapter 21 as they do not transfer a separate good

EXERCISE 21.4 (Continued) Schedule 1 KIMBERLY-CLARK CORP. Lease Amortization Schedule (partial) (Lessee) Date Annual Lease Payment Interest (8%) on Liability Reduction of Lease Liability Lease Liability 12/31/19 $521,934 12/31/19 $71,830 $ 0 $71,830 450,104 12/31/20 71,830 36,008 35,822 414,282 12/31/21 […]

Accounting Chapter 21 Note that this is expensed along with the amortization

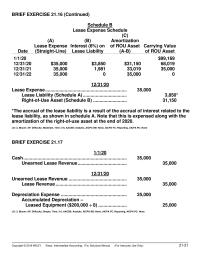

BRIEF EXERCISE 21.16 (Continued) Schedule B Lease Expense Schedule Date (A) Lease Expense (Straight-Line) (B) Interest (6%) on Lease Liability (C) Amortization of ROU Asset (A–B) Carrying Value of ROU Asset 1/1/20 $99,169 12/31/20 $35,000 $3,850 $31,150 68,019 12/31/21 35,000 […]

Accounting Chapter 21 The Lease Contains Bargain purchase Option The Lease

CHAPTER 21 Accounting for Leases ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Rationale for leasing. 1, 2, 3 2. Concepts, classification, and measurement of leases. 4, 5, 6, 7, 8, 10, 11, […]

Accounting Chapter 20 Amortization of any prior service cost or credit

CE20.3 According to FASB ASC 715-30–35-4 (Defined-Benefit Plans – Pension – Components of Net Periodic Cost): All of the following components shall be included in the net pension cost recognized for a period by an employer sponsoring a defined-benefit pension […]

Accounting Chapter 20 Us Employees And Certain Employees International Locations

Copyright © 2019 WILEY Kieso, Intermediate Accounting, 17/e, Solutions Manual (For Instructor Use Only) 20–79 CA 20.5 1. This situation can exist because companies vary as to which assumption they are using when interest rates are disclosed. In the implicit […]

Accounting Chapter 20 This case is quite thought-provoking and should stimulate

PROBLEM 20.7 Copyright © 2019 WILEY Kieso, Intermediate Accounting, 17/e, Solutions Manual (For Instructor Use Only) 20-59 HANSON CORP. Pension Worksheet—2020 General Journal Entries Memo Record Items Annual Pension Expense Cash OCI—Prior Service Cost OCI— Gain/Loss Pension Asset/Liability Projected Benefit […]

Accounting Chapter 20 Pension expense for 2020 consisted only of the service

*EXERCISE 20.23 (15–20 minutes) 20–40 Copyright © 2019 WILEY Kieso, Intermediate Accounting, 17/e, Solutions Manual (For Instructor Use Only) ENGLEHART CO. Postretirement Benefit Worksheet—2020 General Journal Entries Memo Record Items Annual Postretirement Expense Cash OCI—Prior Service Cost Postretirement Asset/Liability APBO […]

Accounting Chapter 20 the pension worksheet on the next page could be

EXERCISE 20.8 (20–25 minutes) Corridor and Minimum Loss Amortization Year Projected Benefit Obligation (a) Plan Assets 10% Corridor Accumulated OCI (G/L) (a) Minimum Amortization of Loss 2019 $2,000,000 $1,900,000 $200,000 $ 0 $ 0 2020 2,400,000 2,500,000 250,000 280,000 3,000(b) […]

Accounting Chapter 20 Postretirement benefit expense computation

CHAPTER 20 Accounting for Pensions and Postretirement Benefits ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Basic definitions and concepts related to pension plans. 1, 2, 3, 4, 5, 6, 7, 8, 9, […]

Accounting Chapter 19 Significant Expenses Implement Tax planning Strategy Any Significant

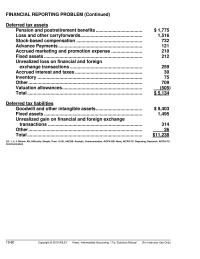

FINANCIAL REPORTING PROBLEM (Continued) Deferred tax assets Pension and postretirement benefits ……………………………… $ 1,775 Loss and other carryforwards………………………………………… 1,516 Stock-based compensation …………………………………………… 732 Advance Payments ……………………………………………………….. 121 Accrued marketing and promotion expense …………………… 210 Fixed assets …………………………………………………………………. 212 Unrealized loss […]

Accounting Chapter 19 Rents Are Taxed The Year They Are

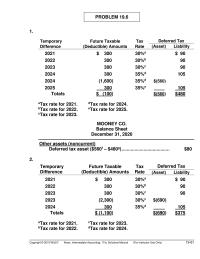

PROBLEM 19.6 1. Temporary Difference Future Taxable (Deductible) Amounts Tax Rate Deferred Tax (Asset) Liability 2021 $ 300 30%a $ 90 2022 300 30%b 90 2023 300 30%c 90 2024 300 35%d 105 2024 (1,600) 35%d $(560) 2025 300 35%e […]

Accounting Chapter 19 Pretax Financial Income Nondeductible Expense Subtotal Taxable

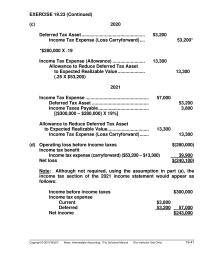

EXERCISE 19.23 (Continued) (c) 2020 Deferred Tax Asset …………………………………………. 53,200 Income Tax Expense (Loss Carryforward) …. 53,200* *$280,000 X .19 Income Tax Expense (Allowance) ……………………. 13,300 Allowance to Reduce Deferred Tax Asset to Expected Realizable Value ………………… 13,300 (.25 X […]

Accounting Chapter 19 Temporary Difference Installment Sales Warranty Costs Totals

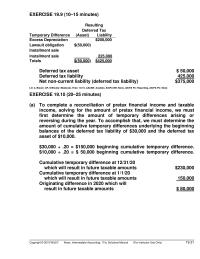

EXERCISE 19.9 (10–15 minutes) Resulting Deferred Tax Temporary Difference (Asset) Liability Excess Depreciation $200,000 Lawsuit obligation $(50,000) Installment sale Installment sale 225,000 Totals $(50,000) $425,000 Deferred tax asset $ 50,000 Deferred tax liability 425,000 Net non-current liability (deferred tax liability) […]

Accounting Chapter 19 Such Positions Give Rise Tax Benefits Either

CHAPTER 19 Accounting for Income Taxes ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Reconcile pretax financial income with taxable income. 1, 14 1, 2, 3, 4, 5, 10, 16, 18, 19 1, […]

Accounting Chapter 18 Progress billings would be accounted for by

*CA 18.9 (a) Widjaja Company should recognize revenue as it performs the work on the contract (the percentage-of-completion method) because it meets the criteria for revenue recognition over time. (b) Progress billings would be accounted for by increasing accounts receivable […]

Accounting Chapter 18 therefore the task would not need to be

PROBLEM 18.11 (Continued) 2022 Costs to date (12/31/22)……………………..………….. $2,100,000 Estimated costs to complete …………………………. 0 2,100,000 Contract price ………..…………………………………….. 1,900,000 Total loss………..……………………..…………………….. $ 200,000 Total loss………………………………………………….….. Less: Loss recognized in 2021 ……………………… $180,000 $ 200,000 Gross profit recognized in 2020…….……… […]

Accounting Chapter 18 Since the services in the extended period

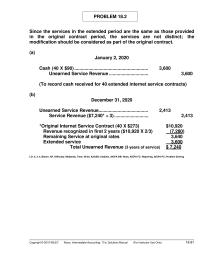

Since the services in the extended period are the same as those provided in the original contract period, the services are not distinct; the modification should be considered as part of the original contract. (a) January 2, 2020 Cash (40 […]

Accounting Chapter 18 Celic recognizes warranty expenses associated

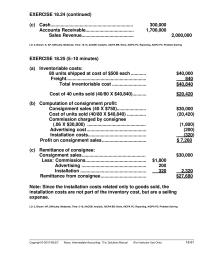

EXERCISE 18.24 (continued) (c) Cash…………………………….…………………………. 300,000 Accounts Receivable.………………………………. 1,700,000 Sales Revenue..………………………….…….. 2,000,000 LO: 3, Bloom: K, AP, Difficulty: Moderate, Time: 10-15, AACSB: Analytic, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Problem Solving EXERCISE 18.25 (5–10 minutes) (a) Inventoriable costs: […]

Accounting Chapter 18 The separate performance obligations are the oven

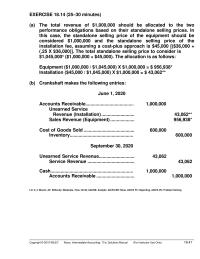

EXERCISE 18.14 (25–30 minutes) (a) The total revenue of $1,000,000 should be allocated to the two performance obligations based on their standalone selling prices. In this case, the standalone selling price of the equipment should be considered $1,000,000 and the […]

Accounting Chapter 18 This Statement True One The Difficulties The

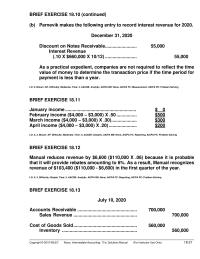

BRIEF EXERCISE 18.10 (continued) (b) Parnevik makes the following entry to record interest revenue for 2020. December 31, 2020 Discount on Notes Receivable……………………. 55,000 Interest Revenue (.10 X $660,000 X 10/12) ……………………. 55,000 As a practical expedient, companies are not […]

Accounting Chapter 18 The Seller Cannot Have The Ability Use

CHAPTER 18 Revenue Recognition ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Current Environment; 5-Step Model. 1, 2, 3, 4, 5, 6 8 1, 2, 3 2. Contracts. 7 1, 2, 3, 4 […]

Accounting Chapter 17 Continued Classification Financial Liabilities And Equity

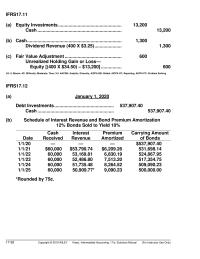

IFRS17.11 (a) Equity Investments …………………………………………. 13,200 Cash ……………………………………………………….. 13,200 (b) Cash ………………………………………………………………. 1,300 Dividend Revenue (400 X $3.25) ………………… 1,300 (c) Fair Value Adjustment …………………………………….. 600 Unrealized Holding Gain or Loss— Equity [(400 X $34.50) – $13,200] ……………. 600 LO: […]

Accounting Chapter 17 Similarly Amounts Recognized Accrued Receivables Shall Not

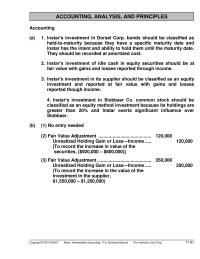

Copyright © 2019 WILEY Kieso, Intermediate Accounting, 17/e, Solutions Manual (For Instructor Use Only) 17–81 ACCOUNTING, ANALYSIS, AND PRINCIPLES Accounting (a) 1. Instar’s investment in Dorsel Corp. bonds should be classified as held-to-maturity because they have a specific maturity date […]

Accounting Chapter 17 No entry necessary at the date of the swap

Copyright © 2019 WILEY Kieso, Intermediate Accounting, 17/e, Solutions Manual (For Instructor Use Only) 17–61 *PROBLEM 17.14 (a) January 7, 2020 Put Option ……………………………………………………… 360 Cash ………………………………………………………… 360 (b) March 31, 2020 Put Option ……………………………………………………… 2,000 Unrealized Holding Gain or […]

Accounting Chapter 17 Some students may debit Interest Receivable at date

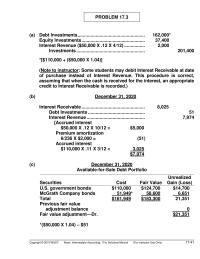

PROBLEM 17.3 (a) Debt Investments ……………………………………………. 162,000* Equity Investments …………………………………………. 37,400 Interest Revenue ($50,000 X .12 X 4/12) ……………. 2,000 Investments …………………………………………….. 201,400 *[$110,000 + ($50,000 X 1.04)] (Note to instructor: Some students may debit Interest Receivable at date of […]

Accounting Chapter 17 Amount reclassified from accumulated other

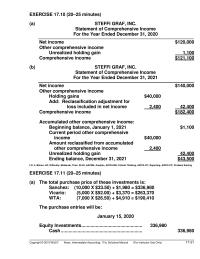

EXERCISE 17.10 (20–25 minutes) (a) STEFFI GRAF, INC. Statement of Comprehensive Income For the Year Ended December 31, 2020 _____________________________________________________________ Net income $120,000 Other comprehensive income Unrealized holding gain 1,100 Comprehensive income $121,100 (b) STEFFI GRAF, INC. Statement of Comprehensive […]

Accounting Chapter 17 Journal entries for fair value and equity

CHAPTER 17 Investments ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Debt securities. 1, 2, 3, 13 1 6 (a) Held-to-maturity. 4, 5, 7, 8, 10, 13, 21 1, 3 2, 3, 5 […]

Accounting Chapter 16 A reconciliation of the numerators and the denominators

CE16-3 According to FASB ASC 260-10–50-1 (Earnings Per Share—Disclosure): For each period for which an income statement is presented, an entity shall disclose all of the following: (a) A reconciliation of the numerators and the denominators of the basic and […]

Accounting Chapter 16 Income tax laws impose no restrictions on the exercise

CA 16.3 (Continued) 3. Income tax laws impose no restrictions on the exercise price of warrants issued to purchasers of a company’s bonds. The exercise price may be above, equal to, or below the current market price of the company’s […]

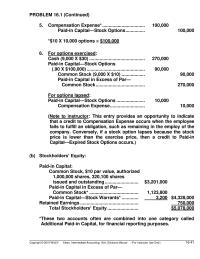

Accounting Chapter 16 This entry provides an opportunity to indicate that

PROBLEM 16.1 (Continued) 5. Compensation Expense* …………………………… 100,000 Paid-in Capital—Stock Options …………… 100,000 *$10 X 10,000 options = $100,000 6. For options exercised: Cash (9,000 X $30) ……………………………………. 270,000 Paid-in Capital—Stock Options (.90 X $100,000) ……………………………………… 90,000 Common Stock (9,000 […]

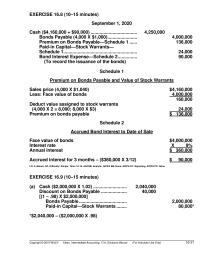

Accounting Chapter 16 Premium on Bonds Payable and Value of Stock

EXERCISE 16.8 (10–15 minutes) September 1, 2020 Cash ($4,160,000 + $90,000) ……………………………… 4,250,000 Bonds Payable (4,000 X $1,000) ………………….. 4,000,000 Premium on Bonds Payable—Schedule 1 …… 136,000 Paid-in Capital—Stock Warrants— Schedule 1 ………………………………………………… 24,000 Bond Interest Expense—Schedule 2 …………… 90,000 […]

Accounting Chapter 16 The Holders These Securities Can Expect Participate

CHAPTER 16 Dilutive Securities and Earnings Per Share ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Convertible debt and preferred stock. 1, 2, 3, 4, 5, 6, 7 1, 2, 3 1, 2, […]

Accounting Chapter 16 Accumulated Depreciation Equipment John Wiley Amp

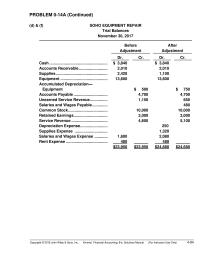

PROBLEM 0-14A (Continued) (d) & (f) SOHO EQUIPMENT REPAIR Trial Balances November 30, 2017 Before Adjustment After Adjustment Dr. Cr. Dr. Cr. Accumulated Depreciation— Equipment Accounts Payable …………………………. Unearned Service Revenue ……………. Salaries and Wages Payable ………….. Common Stock ……………………………… […]

Accounting Chapter 16 Cash received with respect to fees and dues

PROBLEM 0-8A (Continued) (d) PAMPER ME SALON INC. Trial Balance May 31, 2017 Debit Credit Unearned service revenue ……………………………………….. Common stock ……………………………………………………….. Retained earnings …………………………………………………… Service revenue ………………………………………………………. Salaries and wages expense ……………………………………. Rent expense ………………………………………………………….. Supplies expense ……………………………………………………. Advertising […]

Accounting Chapter 16 Assets, Dividends, and Expenses have debit balances

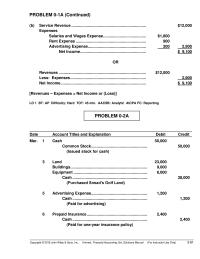

PROBLEM 0-1A (Continued) (b) Service Revenue ………………………………………………………….. $12,000 Expenses Salaries and Wages Expense ………………………………… $1,800 Rent Expense ………………………………………………………. 900 Advertising Expense …………………………………………….. 200 2,900 Net Income …………………………………………………… $ 9,100 OR Revenues ……………………………………………………………………. $12,000 Less: Expenses …………………………………………………………… 2,900 Net Income …………………………………………………………………… […]

Accounting Chapter 16 Stockholders Equity And Expenses The Opposite

EXERCISE 0-21 (a) Revenue recognition principle. (b) Periodicity assumption. (c) No violation. (d) Going concern assumption. (e) Historical cost principle. (f) Economic entity assumption. LO 5 BT: C Difficulty: Medium TOT: 10 min. AACSB: None AICPA FC: Reporting EXERCISE 0-22 […]

Accounting Chapter 16 Maintenance and Repairs Expense Accounts Payable

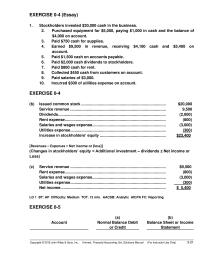

EXERCISE 0-4 (Essay) 1. Stockholders invested $20,000 cash in the business. 2. Purchased equipment for $5,000, paying $1,000 in cash and the balance of $4,000 on account. 3. Paid $750 cash for supplies. 4. Earned $9,500 in revenue, receiving $4,100 […]

Accounting Chapter 16 Increase in assets and increase in liabilities

CHAPTER 0 Accounting Cycle Review SOLUTIONS TO BRIEF EXERCISES BRIEF EXERCISE 0-1 Assets Liabilities Stockholders’ Equity (b) (c) + – NE NE + – LO 1 BT: C Difficulty: Easy TOT: 2 min. AACSB: None AICPA FC: Reporting (a) + […]

Accounting Chapter 15 One measure of solvency is the ratio of debt

COMPARATIVE ANALYSIS CASE (Continued) During 2017, PepsiCo earned a higher return on its stockholders’ equity. (g) Payout ratios for 2017. Coca-Cola, $5,350 = 75.37% $7,098 PepsiCo, $3,730 = 62.74% $5,946 – $1 LO: 4, Bloom: AN, Difficulty: Moderate, Time: 20-25, […]

Accounting Chapter 15 Generally Investments Owners Cause Increase Assets Addition

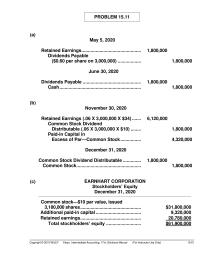

PROBLEM 15.11 (a) May 5, 2020 Retained Earnings ………………………………………. 1,800,000 Dividends Payable ($0.60 per share on 3,000,000) ……………… 1,800,000 June 30, 2020 Dividends Payable ……………………………………… 1,800,000 Cash ……………………………………………………… 1,800,000 (b) November 30, 2020 Retained Earnings (.06 X 3,000,000 X $34) […]

Accounting Chapter 15 including a note to the financial statements setting

Time and Purpose of Problems (Continued) Problem 15.10 (Time 35–45 minutes) Purpose—to provide the student with an understanding of the differences between a stock dividend and a stock split. Acting as a financial advisor to the Board of Directors, the […]

Accounting Chapter 15 No entry simply a memorandum note indicating

EXERCISE 15.5 (10–15 minutes) (a) Fair Value of Common (500 X $165) $ 82,500 Fair Value of Preferred (100 X $230) 23,000 $105,500 Allocated to Common: $82,500/$105,500 X $100,000 $ 78,199 Allocated to Preferred: $23,000/$105,500 X $100,000 21,801 Total allocation […]

Accounting Chapter 15 Preferred stock commonly has preference to dividends

CHAPTER 15 Stockholders’ Equity ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Stockholders’ rights; corporate form. 1, 2, 3 1 2. Stockholders’ equity. 4, 5, 6, 16 3 7, 9, 10, 16, 17, […]

Accounting Chapter 14 That Presumption However Must Not Permit The

FINANCIAL REPORTING PROBLEM (Continued) Inventory turnover = Cost of goods sold Average inventory = $32,535 $4,624 + $4,716 2 = 6.97 times (6.79 in 2016) Current cash debt coverage = Net cash provided by operating activities Average current liabilities = […]

Accounting Chapter 14 One method of amortization is the straight-line

PROBLEM 14.9 12/31/19 (a) Machinery ………………………………………………………. 182,485.20 Discount on Notes Payable ………………………….. 27,514.80 Cash ………………………………………………………. 50,000.00 Notes Payable ………………………….. 160,000.00 [To record machinery at the present value of the note plus the immediate cash payment: PV of $40,000 annuity @ […]

Accounting Chapter 14 The Loss Reported Ordinary Loss Note Loss

Copyright © 2019 WILEY Kieso, Intermediate Accounting, 17/e, Solutions Manual (For Instructor Use Only) 14–41 *EXERCISE 14.27 (Continued) December 31, 2021 (see schedule) Cash ……………………………………………………………………… 11,000 Allowance for Doubtful Accounts ………………………….. 12,277 Interest Revenue ……………………………………………. 23,277 December 31, 2022 (see […]

Accounting Chapter 14 Fallen’s creditworthiness has improved during

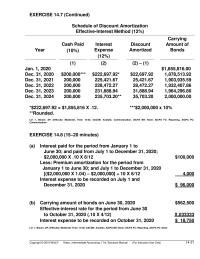

EXERCISE 14.7 (Continued) Schedule of Discount Amortization Effective-Interest Method (12%) Year Cash Paid (10%) Interest Expense (12%) Discount Amortized Carrying Amount of Bonds (1) (2) (2) – (1) Jan. 1, 2020 $1,855,816.00 Dec. 31, 2020 $200,000*** $222,697.92 * $22,697.92 1,878,513.92 […]

Accounting Chapter 14 Entries for redemption and issuance of bonds

CHAPTER 14 Long-Term Liabilities ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Long-term liability; classification; definitions. 1, 14 1, 2 10, 11 1, 2 2. Issuance of bonds; types of bonds. 2, 3, […]

Accounting Chapter 13 Yes The Debt Should Included Current Liabilities

CE13.1 Master Glossary (a) An asset retirement is an obligation associated with the retirement of a tangible long-lived asset. (b) Current liabilities is used principally to designate obligations whose liquidation is reasonably expected to require the use of existing resources […]