Archives: Solution Manual

Accounting Chapter 1 Homework Accounts Sony Withdrawals Revenues Expenses Payable

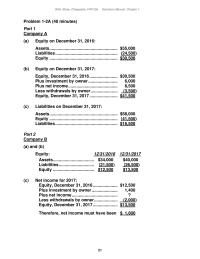

21 Problem 1-2A (40 minutes) Part 1 Company A (a) Equity on December 31, 2016: Assets …………………………………………………. $55,000 Liabilities …………………………………………….. (24,500) Equity …………………………………………………. $30,500 (b) Equity on December 31, 2017: Equity, December 31, 2016 …………………… $30,500 Plus investment by owner […]

Accounting Chapter 1 Homework Accounting professionals offer many services including auditing

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 1 Chapter 1 Accounting in Business QUESTIONS 1. The purpose of accounting is to provide decision makers with relevant and reliable information to help them make better decisions. Examples include information for […]

Accounting Chapter 1 Homework Corporation Business That Separate Legal Entity

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition 1-1 CHAPTER 1 ACCOUNTING IN BUSINESS Related Assignment Materials Student Learning Objectives Questions Quick Studies* Exercises* Problems* Beyond the Numbers Conceptual objectives opportunities in accounting. 8, 9, 10, 11, 12, 23 […]

Accounting Chapter 21 Homework Investing Activities Sale Building Purchase Investment Purchase

Student Name: Class: Dec. 31 Changes Dec. 31 2015 Debits Credits 2016 30 12 42 3 2 5 12 3 9 30 30 – 100 60 160 200 50 250 100 26 126 90 35 80 135 575 715 Notes […]

Accounting Chapter 21 Homework Mr Lowell Had Just Hung The Phone

RETAINED EARNINGS The stock dividend caused a $13 million reduction of retained earnings. Net income increased retained earnings by $12 million. The net reduction of $1 million accounted for by these two entries leaves unexplained $5 million […]

Accounting Chapter 21 Homework Depreciation expense and the loss on sale of land are not cash outflows

(decrease) (decrease) 1 600 0 0 600 Cash (paid to suppliers of goods) 600 2 600 18 0 618 Inventory 18 Cash (paid to suppliers of goods) 618 3 600 0 558 558 5. Summary Entry Cost of goods sold […]

Accounting Chapter 20 Homework Calculation of annual depreciation after the change:

Student Name: Class: Debit Credit Requirement 2: 2016 2015 (210,000) (159,600) 315,000$ 239,400$ Correct! Correct! 3.15$ 2.39$ Correct! Correct! Income tax expense Net income Earnings per common share Earnings per share: 525,000$ 399,000$ Problem 20-01 McGraw-Hill/Irwin Instructor Requirement 1: CECIL-BOOKER […]

Accounting Chapter 20 Homework Estimated Remaining Life Years New

Bearing reports the change prospectively; previous financial statements are not revised. Instead, the company simply employs the straight-line method from then on. The undepreciated cost remaining at the time of the change would be depreciated straight-line over the remaining useful […]

Accounting Chapter 19 Homework Share Millions Except Per Share Amounts 2014

Student Name: Class: 2$ Debit Credit 40 «- Correct! 16 16 «- Correct! Tax expense Paid-in capital – stock options Deferred tax asset 40 «- Correct! 16 16 «- Correct! 320 80 40 360 «- Correct! 64 32 32 «- […]

Accounting Chapter 19 Homework Eps Subsequent Years For Comparative Purposes Net

$25.50 fair value per share x 12 million shares granted = $306 million fair value of award ($ in millions) Compensation expense ($306 million ÷ 3 years) .. 102 Paid-in capital – restricted stock …………….. 102 x 12 million shares […]

Accounting Chapter 18 Homework Common Stock Par Authorized 5000000 Shares Issued

Student Name: Class: Debit Credit 150,000 «- Correct! 1,650,000 1,650,000 1,650,000 «- Correct! 1,400,000 200,000 1,200,000 «- Correct! 1,400,000 200,000 1,600,000 «- Correct! Common stock Paid-in capital – excess of par Cash Retained Earnings Cash Cash November 9, 2018 Retired […]

Accounting Chapter 18 Homework Paidin Capital Reacquired Shares Retained Earnings

Common stock (60 million shares x $1 par) ……………… 60 Paid-in capital – excess of par (difference) ………………. 540 February 14 Legal expenses (1 million shares x $10 per share) …………. 10 Common stock (1 million shares x $1 par) […]

Accounting Chapter 17 Homework PV of retirement annuity at end of 2041

Student Name: Class: 19,200$ 174,872$ 32,220$ Correct! 270,000$ 68,040$ 619,702$ 122,174$ Correct! 122,174$ (108,743) 13,431$ (7,612) 5,819$ PV of retirement annuity at end of 2016 Pension benefit at end of 2016 Less: Interest cost Service cost Projected benefit obligation Requirement […]

Accounting Chapter 17 Homework Now Requires Companies Record Obligation

ATTRIBUTION Jessica Farrow was hired by Global Communications at age 22 at the beginning of 2005 and is expected to retire at the end of 2044 at age 61. The retirement period is estimated to be 20 years. Global’s employees […]

Accounting Chapter 17 Homework The Gain And Loss Becomes Part The

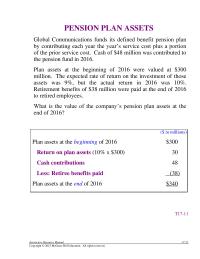

PENSION PLAN ASSETS Global Communications funds its defined benefit pension plan by contributing each year the year’s service cost plus a portion of the prior service cost. Cash of $48 million was contributed to the pension fund in 2016. Plan […]

Accounting Chapter 17 Homework Service Cost And Net Interest Cost income Are

C CH HA AP PT TE ER R 1 17 7 P Pe en ns si io on ns s a an nd d O Ot th he er r P Po os st tr re et ti ir re […]

Accounting Chapter 17 Homework After the two amortization amounts are

Problem 17–16 (continued) Requirement 5 To record gains and losses ($ in millions) Loss—OCI ($5 loss on change of PBO assumption) 5 PBO …………………………………………….. 5 Plan assets ………………………………………… 12 Gain—OCI ($36 actual return on assets exceeds $24 gain expected) 12 […]

Accounting Chapter 17 Homework Plan Assets Expected Return Plan Assets

Problem 17–7 Requirement 1 ($ in 000s) Net gain (previous gains exceeded previous losses) $170 10% of $1,400 ($1,400 is greater than $1,100) 140 Excess at the beginning of the year $ 30 Average remaining service period years ÷ 15 […]

Accounting Chapter 17 Homework They Are Instead Reported The Statement Comprehensive

Exercise 17–22 (concluded) Requirement 2 ($ in millions) Service cost 72 DBO (2016 service cost) 60 DBO (past service cost) 12 Net interest cost (7.5% x [$360 – 240]) 9 Plan assets (7.5% x $240: interest income) 18 DBO (7.5% […]

Accounting Chapter 17 Homework Balance Jan 2016 Service Cost Interest Cost

Exercise 17–4 Requirement 1 ($ in millions) Pension expense (total) …………………………………………… 14 Plan assets (expected return on assets) ………………………….. 4 PBO ($10 service cost + $6 interest cost) …………………….. 16 Amortization of net loss—OCI (current amortization)* .. 2 Requirement 2 […]

Accounting Chapter 17 Homework Items The Statement Comprehensive Income And

Chapter 17 Pensions and Other Postretirement Benefits QUESTIONS FOR REVIEW OF KEY TOPICS Question 17–1 Pension plans are arrangements designed to provide income to individuals during their retirement years. Funds are set aside during an employee’s working years so that […]

Accounting Chapter 17 Homework The Present Value The Retirement

Interest cost 36 Expected return on the plan assets ($27 actual, less $3 gain) (24) Pension expense $72 PBO 72 Plan assets 60 Cash (given) 60 PBO 27 Plan assets (given) 27 Alternate Exercises and Problems 17–1 Chapter 17 Pensions […]

Accounting Chapter 16 Homework Journal entry at the end of 2016

Student Name: Class: 2016 2017 2018 2019 60,000$ 80,000$ 70,000$ 70,000$ (39,600) (52,800) (18,000) (9,600) Cumulative Temporary 2016 2017 2018 2019 Difference (39,600) (52,800) (18,000) (9,600) (9,600) (22,800) 12,000 20,400 –$ «- Correct! (22,800) 12,000 20,400 9,600$ «- Correct! 12,000 […]

Accounting Chapter 16 Homework What Might Contribute RadioShack’s Need Record Valuation

1-32 Intermediate Accounting, 8/e Dealing with Uncertainty GAAP allows companies to recognize in the financial statements the tax benefit of a position it takes only if it is “more likely than not” (greater than 50% chance) to be sustained if […]

Accounting Chapter 16 Homework The Enacted Tax Rate 40 Each Year

TEMPORARY AND PERMANENT DIFFERENCES Kent Land Management reported pretax income in 2016, 2017, and 2018 of $100 million except for an additional income of $40 million from installment sales and $5 million interest from investments in municipal bonds in 2016. […]

Accounting Chapter 16 Homework Pretax Accounting Income Temporary Difference Installment Income

C CH HA AP PT TE ER R 1 16 6 A Ac cc co ou un nt ti in ng g f fo or r I In nc co om me e T Ta ax xe es s Overview […]

Accounting Chapter 16 Homework Please Let Know You Have Any Questions

CASES Analysis Case 16–1 Requirement 1 Temporary differences originate in one or more years and reverse in one or more future years. Differing depreciation methods are a common example of a temporary difference. On the other hand, permanent differences are […]

Accounting Chapter 16 Homework Deltas Disclosure Note States We Periodically Assess

Problem 16–8 (continued) Requirement 4 ($ in millions) Current Future Future Year Taxable Deductible 2017 Amounts Amounts [2018] [2018] Pretax accounting income 183 Permanent difference: Life insurance premiums 2 Temporary differences: Casualty insurance (reversing) 30 Subscriptions—2016 (reversing)* (18) Subscriptions—2017 ($35 […]

Accounting Chapter 16 Homework Deferred Tax Liability Determined Above Income Tax

Problem 16–1 (continued) Requirement 2 ($ in thousands) Current Future Year Taxable 2017 Amount Pretax accounting income 220 Temporary difference: 2016 services (10) 10 2017 services (25) 25 Taxable income (income tax return) 205 Enacted tax rate 40% 40% Tax […]

Accounting Chapter 16 Homework Straight-line depreciation for financial reporting

Exercise 16–20 (concluded) Requirement 2 ($ in thousands) Operating loss before income taxes $(375 ) Income tax benefit—net operating loss 150 Net loss $(225) Solutions Manual, Vol.2, Chapter 16 16–41 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction […]

Accounting Chapter 16 Homework Temporary Differences Depreciation Warranty Expense 977 Taxable

Exercise 16–7 1. Liability—loss contingency 2. Liability—subscriptions 3. Prepaid rent 4. Accrued bond interest payable 5. Prepaid insurance 6. Unrealized loss on investments (shareholders’ equity account) 7. Warranty liability 8. Liability—unearned rent revenue 9. Accumulated depreciation; and thus depreciable assets […]

Accounting Chapter 16 Homework Income Tax Expense To Balance Deferred Tax

Chapter 16 Accounting for Income Taxes _____________________________________________________________________________ QUESTIONS FOR REVIEW OF KEY TOPICS Question 16–1 Income tax expense is comprised of both the current and the deferred tax consequences of events and transactions already recognized. Specifically, the $12.3 million expense […]

Accounting Chapter 16 Homework Tax Payable Currently Deferred Tax Liability Future

Alternate Exercises and Problems 16–1 Deferred tax asset ($90,000 x 40%) 36,000 Income tax payable (given) 285,000 Deferred tax liability ([$80 million – 50 million] x 35%) 10.5 Income tax payable ($50 million x 35%) 17.5 Chapter 16 Accounting for […]

Accounting Chapter 15 Homework Implicit Interest Rate Years 300000 Years 365760

Student Name: Class: 365,760$ 348,685$ 17,075 365,760$ Correct! (b) By Rhone-Metro (the lessor) (a) By Western Soya Co. (the lessee) Present value of minimum lease payments Plus: Present value of the lessee-guaranteed residual value Since at least one criterion is […]

Accounting Chapter 15 Homework Topic Est Time Min Operating Lease Operating

15-32 Intermediate Accounting, 8/e INTERNATIONAL FINANCIAL REPORTING STANDARDS Present value of minimum lease payments. Under IAS No. 17, both parties to a lease generally use the rate implicit in the lease to discount minimum lease payments. Under U.S. GAAP, lessors […]

Accounting Chapter 15 Homework The residual value influences the lessee only by the fact

EFFECT OF A BARGAIN PURCHASE OPTION A bargain purchase option (BPO) is a provision of some lease contracts that gives the lessee the option of purchasing the leased property at a “bargain” price. The expectation that the option price will […]

Accounting Chapter 15 Homework Under Ias No 17 Both Parties Lease

C CH HA AP PT TE ER R 1 15 5 L Le ea as se es s Overview In the previous chapter, we saw how companies account for their long-term debt. The focus of that discussion was bonds and […]

Accounting Chapter 15 Homework Total 1250958 Since Interstates Cost 1050000 Was

Problem 15-25 (concluded) 4. Expenses for year ended December 31, 2016 June 30, 2016 interest ………………………………………. $ 0 Dec. 31, 2016 interest ………………………………………. 121,855** Interest for 2016 ………………………………………….. $121,855 June 30, 2016 amortization……………………………….. 0 Dec. 31, 2016 amortization ………………………………. 441,052** […]

Accounting Chapter 15 Homework So Ifrs Would Produce The Same Results

Problem 15-19 Requirement 1 Application of Classification Criteria 1 Does the agreement specify that ownership of the asset transfers to the lessee? NO 2 Does the agreement contain a bargain purchase option? NO 3 Is the lease term equal to […]

Accounting Chapter 15 Homework Requirement December 31 2017 Yard Art Landscaping

Problem 15-15 (continued) Not required in the problem, but helpful to see that the present value calculation is precisely the reverse of the lessor’s calculation of quarterly payments: Amount to be recovered (fair value) $26,427 Less: Present value of the […]

Accounting Chapter 15 Homework Requirement Since 1 Title The Conveyer Does

Problem 15-9 (continued) Requirement 2 The lessee’s incremental borrowing rate (12%) is more than the lessor’s implicit rate (10%). So, both parties’ calculations should be made using a 10% discount rate: Application of Classification Criteria 1 Does the agreement specify […]

Accounting Chapter 15 Homework For both sales-type and direct-financing leases, the lessor’s gross investment

CPA Exam Questions (concluded) 5. a. In a capital lease with a bargain purchase option, the lessee will control the asset for its total useful life. Therefore, the depreciation should be allocated over the 8-year life of the asset. $240,000 […]

Accounting Chapter 15 Homework Type Lease Amortization Schedule Lease Payments

Exercise 15-23 1. January 1, 2016 Lease receivable (fair value / present value) …………………… 500,000 Inventory of equipment (lessor’s cost) …………………….. 500,000 Lease receivable ……………………………………………………. 4,242 Cash (initial direct costs) ………………………………………… 4,242 Cash (lease payment)…………………………………………………. 184,330 Lease receivable ………………………………………………… 184,330 […]

Accounting Chapter 15 Homework Present Value Minimum Lease Payments Discounted Lower

Exercise 15-9 1. Receivable at December 31, 2016 $562,907 x 5.32948 = $3,000,000 (rounded) present value of an annuity due of $1: n=6, i=5% Net Receivable Initial balance, June 30, 2016 …………. $3,000,000 June 30, 2016 reduction …………………. […]

Accounting Chapter 15 Homework In a Type B lease, the lessee records interest the normal way

Brief Exercise 15-17 Income Statement: Lease revenue (straight-line amount) ……………………… $25,000* Depreciation ($176,000 ÷ 12 years) …………………………….. (14,667)** Increase in earnings (pretax) ………………………… $10,333 In a Type B lease, the lessor records lease revenue on a straight-line basis. The lessor, […]

Accounting Chapter 15 Homework The Impact Any Changes Will Significant Us

Chapter 15 Leases QUESTIONS FOR REVIEW OF KEY TOPICS Question 15-1 Regardless of the legal form of the agreement, a lease is accounted for as either a rental agreement or a purchase/sale accompanied by debt financing depending on the substance […]

Accounting Chapter 15 Homework Requirement Capital Lease Lessee Direct Financing Lease

Cash …………………………………….. 40,000 December 31, 2016 Rent expense …………………………….. 40,000 Cash …………………………………….. 40,000 Cash ………………………………………… 40,000 Rent revenue …………………………. 40,000 December 31, 2016 Cash ………………………………………… 40,000 Rent revenue …………………………. 40,000 Depreciation expense ($350,000 ÷ 5 years) 70,000 Accumulated depreciation ………. […]

Accounting Chapter 14 Homework Interest Expense Discount Bonds Payable Cash July

Student Name: Class: Cash Effective Increase in Outstanding Pay- Payment Interest Balance Balance ment 4.5% 5% 96,768 14,500 4,838 338 97,106 24,500 4,855 355 97,461 Cash Recorded Increase in Outstanding Pay- Payment Interest Balance Balance ment 4.5% 100,000 96,768 34,500 […]

Accounting Chapter 14 Homework Communication Skills Addition Communication Cases 141

14-36 Intermediate Accounting, 8/e DEBT CONTINUED, WITH MODIFIED TERMS WHEN TOTAL CASH PAYMENTS EXCEED THE BOOK VALUE OF THE DEBT If the payments exceed the amount owed, the restructured debt agreement still provides interest on the debt – but less […]

Accounting Chapter 14 Homework December 31 December 31 Hsa Recorded The

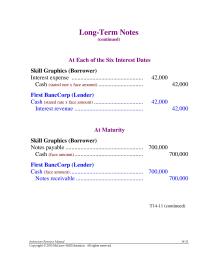

Long-Term Notes (continued) At Each of the Six Interest Dates Skill Graphics (Borrower) Interest expense ………………………………………… 42,000 Cash (stated rate x face amount) ………………………… 42,000 First BancCorp (Lender) Cash (stated rate x face amount) …………………………… 42,000 Interest revenue ………………………………………. 42,000 […]