Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 1

Chapter 1

Accounting in Business

QUESTIONS

1. The purpose of accounting is to provide decision makers with relevant and reliable

information to help them make better decisions. Examples include information for

people making investments, loans, and business plans.

2. Technology reduces the time, effort, and cost of recordkeeping. There is still a

demand for people who can design accounting systems, supervise their operation,

3. External users and their uses of accounting information include: (a) lenders, to

measure the risk and return of loans; (b) shareholders, to assess whether to buy,

4. Business owners and managers use accounting information to help answer

questions such as: What resources does an organization own? What debts are

owed? How much income is earned? Are expenses reasonable for the level of

sales? Are customers’ accounts being promptly collected?

5. Service businesses include: Standard and Poor’s, Dun & Bradstreet, Merrill Lynch,

6. The internal role of accounting is to serve the organization’s internal operating

7. Accounting professionals offer many services including auditing, management

advice, tax planning, business valuation, and money management.

8. Marketing managers are likely interested in information such as sales volume,

10. Some accounting-related professions include consultant, financial analyst,

11. Ethics rules require that auditors avoid auditing clients in which they have a direct

12. In addition to preparing tax returns, tax accountants help companies and individuals

plan future transactions to minimize the amount of tax to be paid. They are also

13. The objectivity concept means that financial statement information is supported by

14. This treatment is justified by both the cost principle and the going-concern

assumption.

15. The revenue recognition principle provides guidance for managers and auditors so

they know when to recognize revenue. If revenue is recognized too early, the

16. Business organizations can be organized in one of three basic forms: sole

proprietorship, partnership, or corporation. These forms have implications for legal

liability, taxation, continuity, number of owners, and legal status as follows:

17. (a) Assets are resources owned or controlled by a company that are expected to

18. Equity is increased by investments from the owner and by net income (which is the

3

19. Accounting principles consist of (a) general and (b) specific principles. General

principles are the basic assumptions, concepts, and guidelines for preparing

21. Net income (also called income, profit, or earnings) equals revenues minus

22. The four basic financial statements are: income statement, statement of owner’s

equity, balance sheet, and statement of cash flows.

24. Rent expense, utilities expense, administrative expenses, advertising and promotion

25. The statement of owner’s equity explains the changes in equity from net income or

loss, and from any owner contributions and withdrawals over a period of time.

27. The statement of cash flows reports on the cash inflows and outflows from a

company’s operating, investing, and financing activities.

28. Return on assets, also called return on investment, is a profitability measure that is

useful in evaluating management, analyzing and forecasting profits, and planning

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 1

4

31B. An organization’s financing activities (liabilities and equity) pay for investing

32. The dollar amounts in Google’s financial statements are rounded to the nearest

33. The independent auditor for Apple is Ernst & Young, LLP. The auditor expressly

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 1

5

QUICK STUDIES

Quick Study 1-1 (10 minutes)

Quick Study 1-2 (10 minutes)

a.

E

g.

E

Quick Study 1-3 (10 minutes)

1. A. Opportunity

Quick Study 1-4 (5 minutes)

1. c. constraint

6

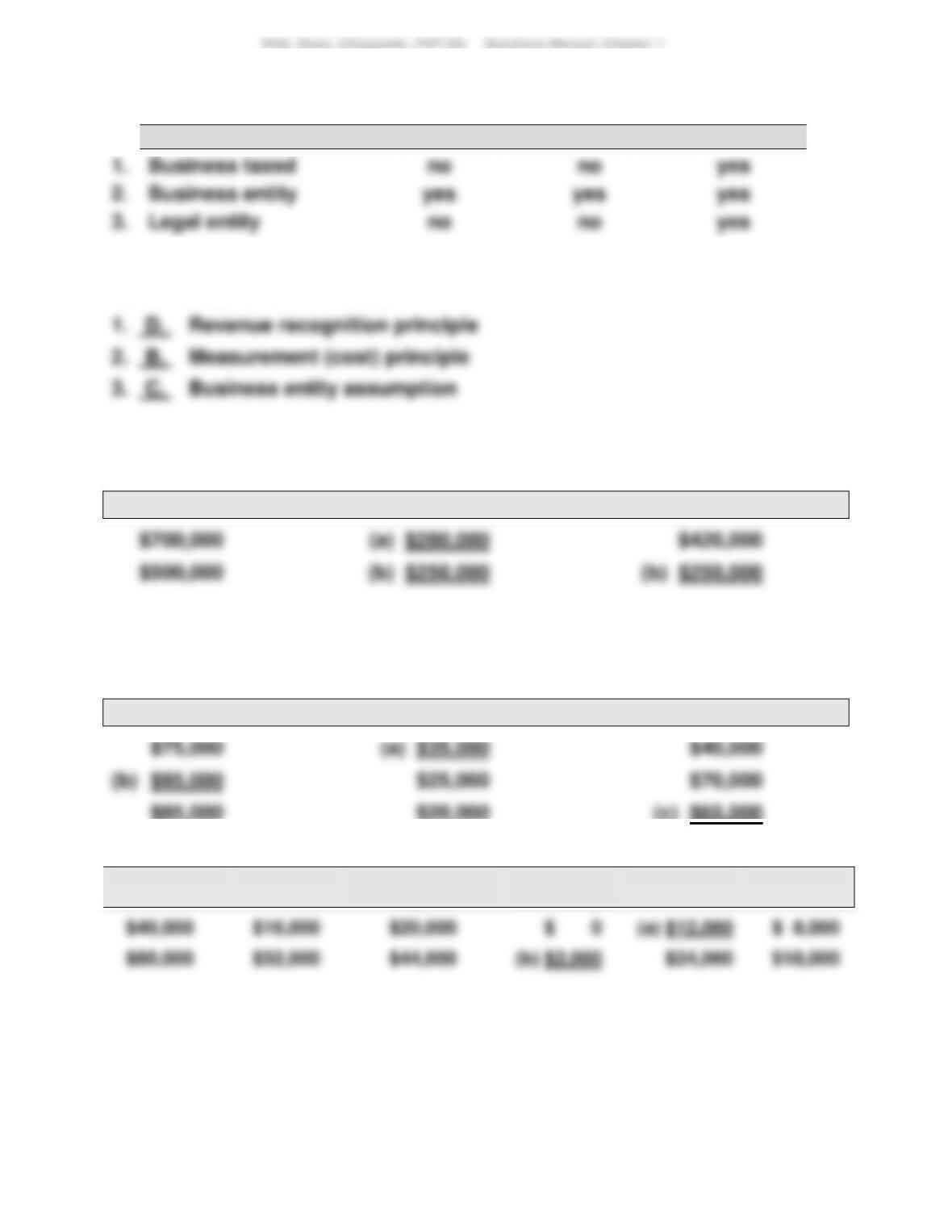

Quick Study 1-5 (10 minutes)

Attribute Present

Proprietorship

Partnership

Corporation

Business taxed

Business entity

Legal entity

Quick Study 1-6 (10 minutes)

Quick Study 1-7 (5 minutes)

Assets = Liabilities + Equity

Quick Study 1-8 (10 minutes)

1.

Assets = Liabilities + Equity

2.

Assets =

Liabilities

+ Owner,

Capital

– Owner,

Withdrawals

+ Revenues

– Expenses

7

Quick Study 1-9 (10 minutes)

a. For December 31, 2015, the accounts and their dollar amounts (in $

millions) for Google are:

b. Using Google’s amounts from (a) we verify that (in $ millions):

Assets

=

Liabilities

+

Equity

=

+

Quick Study 1-10 (15 minutes)

Assets

=

Liabilities

+

Equity

Cash

+

Accounts

Recble.

=

Accounts

Payable

+

Owner,

Capital

–

Owner,

Withdrawals

+

Revenues

–

Expenses

8

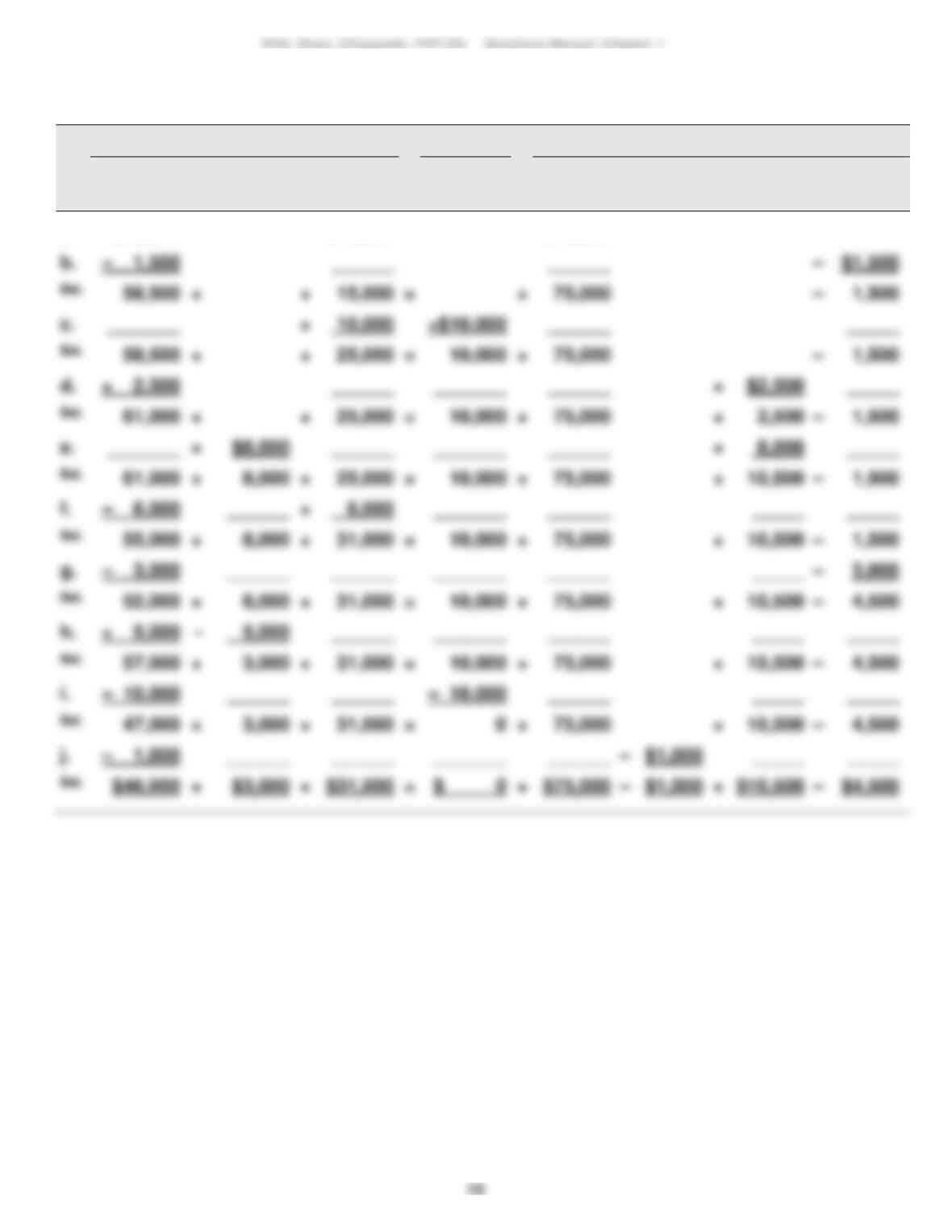

Quick Study 1-11 (15 minutes)

Assets

=

Liabilities

+

Equity

Cash

+

Supplies

+

Equip.

+

Land

=

Accts.

Pay.

+

A. Carr,

Capital

–

A.Carr,

With-

drawals

+

Rev.

–

Exp.

Quick Study 1-12 (10 minutes)

[Code: Income statement (I), Balance sheet (B), Statement of owner’s equity (E), or

Statement of cash flows (CF).]

9

Quick Study 1-13 (5 minutes)

Quick Study 1-14 (5 minutes)

Quick Study 1-15 (10 minutes)

Quick Study 1-16 (10 minutes)

Quick Study 1-17 (10 minutes)

a. For December 31, 2015, the accounts and their dollar amounts (in KRW

millions) for Samsung are:

b. Using Samsung’s amounts from (a) we verify (in KRW millions):

Assets

=

Liabilities

+

Equity

=

+

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 1

10

EXERCISES

Exercise 1-1 (10 minutes)

C 1. Analyzing and interpreting reports.

Exercise 1-2 (20 minutes)

Part A.

1.

I

5.

I

3.

I

7.

I

Part B.

1.

I

5.

I

2.

I

6.

E

4.

E

8.

I

Exercise 1-3 (10 minutes)

11

Exercise 1-4 (10 minutes)

Exercise 1-5 (20 minutes)

1. I

Exercise 1-6 (10 minutes)

a.

(C) Corporation

e.

(C) Corporation

c.

(SP) Sole proprietorship

(C) Corporation

Exercise 1-7 (10 minutes)

Code

Description

Principle/Assumption

H

1.

A company reports details behind financial

statements that would impact users’ decisions.

Full disclosure

principle

G

Financial statements reflect the assumption that

the business continues operating.

Going-concern

assumption

F

3.

A company records the expenses incurred to

generate the revenues reported.

Matching (expense

recognition) principle

A

4.

Derived from long-used and generally accepted

accounting practices.

General accounting

principle

C

5.

its owner or owners.

Business entity

assumption

D

6.

Revenue is recorded when products and

services are delivered.

Revenue recognition

principle

E

7.

Usually created by a pronouncement from an

authoritative body.

Specific accounting

principle

B

8.

Information is based on actual costs incurred in

transactions.

Cost principle

Exercise 1-8 (10 minutes)

Assets

=

Liabilities

+

Equity

13

Exercise 1-9 (20 minutes)

a. Using the accounting equation at the beginning of the year:

Assets

=

Liabilities

+

Equity

$300,000

=

?

+

$100,000

Assets

=

Liabilities

+

Equity

=

+

$380,000

=

+

b. Using the accounting equation:

Assets

=

Liabilities

+

Equity

$123,000

=

+

Assets

=

Liabilities

+

Equity

$190,000

=

+

$190,000

=

+

$125,000

Assets

=

Liabilities

+

Equity

=

+

$130,000

=

+

Exercise 1-10 (20 minutes)

1. d

Exercise 1-11 (20 minutes)

1. f

Exercise 1-12 (15 minutes)

a. 3

Exercise 1-13 (30 minutes)

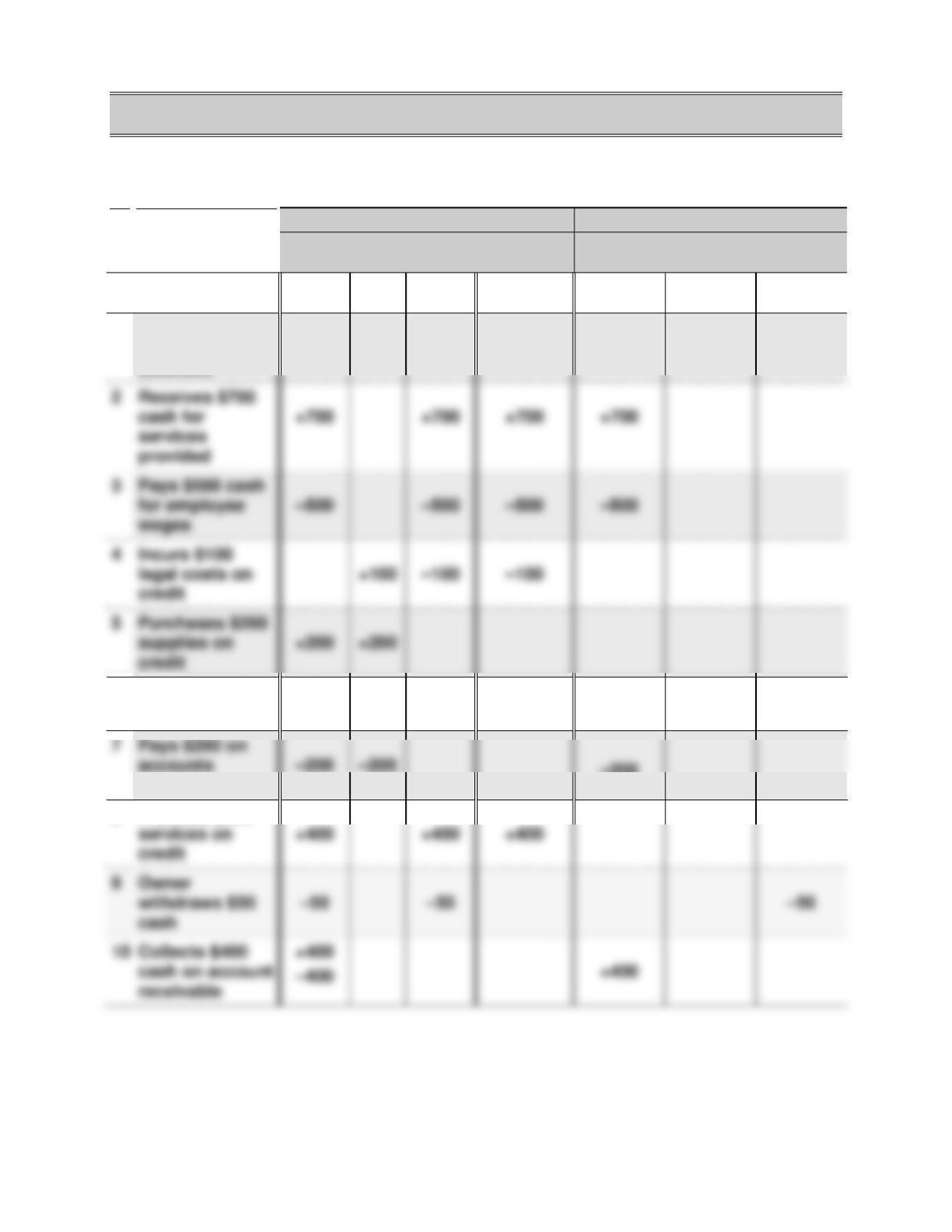

Assets

=

Liabilities

+

Equity

Cash

+

Accounts

Receivable

+

Equip-

ment

=

Accounts

Payable

+

M.Chen,

Capital

–

M.Chen,

With-

drawals

+

Revenues

–

Expenses

a.

+$60,000

+

$15,000

=

+

$75,000

+

+

=

+

c.

_______

+

10,000

+

+

=

+

+ 2,500

+

+

+

=

+

+

e.

_______

+

+

+

+

=

+

+

+

+

+

=

+

+

+

+

=

+

+

+ 5,000

+

+

=

+

+

+

+

=

0

+

+

16

Exercise 1-14 (10 minutes)

Return on assets

=

Net income / Average total assets

Exercise 1-15 (15 minutes)

ERNST CONSULTING

Income Statement

For Month Ended October 31

Revenues

Consulting revenue ………………………. $14,000

Exercise 1-16 (15 minutes)

ERNST CONSULTING

Statement of Owner’s Equity

For Month Ended October 31

E. Ernst, Capital, October 1 ……………………….. $ 0

17

Exercise 1-17 (15 minutes)

ERNST CONSULTING

Balance Sheet

October 31

Assets Liabilities

Exercise 1-18 (15 minutes)

ERNST CONSULTING

Statement of Cash Flows

For Month Ended October 31

Cash flows from operating activities

Exercise 1-19 (10 minutes)

Exercise 1-20 (20 minutes)

Ford Motor Company

Income Statement

For Year Ended December 31, 2015

($ millions)

Revenues …………………………..……………………………….. $149,558

Exercise 1-21B (10 minutes)

a. Financing

19

Exercise 1-22 (15 minutes)

BMW GROUP

Income Statement

For Year Ended December 31, 2015

(Euros in millions)

Revenues …………………………..……………………………….. € 92,175

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 1

20

PROBLEM SET A

Problem 1-1A (25 minutes)

a.

b.

Balance Sheet

Income

Statement

Statement of Cash Flows

Transaction

Total

Assets

Total

Liab.

Total

Equity

Net

Income

Operating

Activities

Investing

Activities

Financing

Activities

1

Owner invests

$900 cash in

business

+900

+900

+900

6

Buys equipment

for $300 cash

+300

–300

–300

payable

–200

8

Provides $400

provided

3

Pays $500 cash

wages

credit

credit