Archives: Solution Manual

Accounting Chapter 14 Homework Teaching Transparency Masters The Following Can Reproduced

CHAPTER 14 Bonds and Long-Term Notes Overview This chapter continues the presentation of liabilities. Specifically, the discussion focuses on the accounting treatment of long-term liabilities. Long-term notes and bonds are discussed, as well as the extinguishment of debt and troubled […]

Accounting Chapter 14 Homework In general, debt increases risk. Debt places owners in a subordinate position

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Judgment Case 14–9 Requirement 1 The debt to equity ratio is computed by dividing total liabilities by total shareholders’ equity. […]

Accounting Chapter 14 Homework Those Who Support Separate Recognition

Real World Case 14–2 Requirement 1 ($ in millions) Cash (price given) ………………………………………………. 968 Discount on notes (difference) …………………………….. 832 Notes payable (face amount) ……………………………. 1,800 Requirement 2 ($ in millions) Fiscal Increase Outstanding Year-end Cash Interest Expense in Balance […]

Accounting Chapter 14 Homework The 2016 Statement Comprehensive Income Unrealized

Problem 14–20 (concluded) Requirement 4 Microsoft’s note states that “Because the convertible debt may be wholly or partially settled in cash, we are required to separately account for the liability and equity components of the notes.” As indicated in the […]

Accounting Chapter 14 Homework Present Value Ordinary Annuity 10 Table

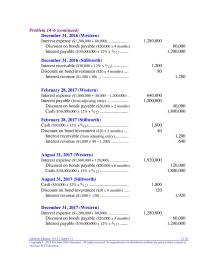

Problem 14–6 (continued) December 31, 2016 (Western) Interest expense ($1,200,000 + 80,000) …………………. 1,280,000 Discount on bonds payable ($20,000 x 4 months) 80,000 Interest payable ($30,000,000 x 12% x 4/12) …….. 1,200,000 December 31, 2016 (Stillworth) Interest receivable ($30,000 x […]

Accounting Chapter 14 Homework No interest should be recorded after the restructuring

Exercise 14–34 Analysis: Book value: $12 million + 1.2 million = $13,200,000 Future payments: ($1 million x 2) + $11 million = 13,000,000 Gain to debtor $ 200,000 1. January 1, 2016 Interest payable (10% x $12,000,000) ……………………. 1,200,000 Notes […]

Accounting Chapter 14 Homework Because none of the change is due to the change in general interest rates

Exercise 14–20 1. January 1, 2016 Machinery ……………………………………………………………….. 4,000,000 Notes payable ………………………………………………………… 4,000,000 2. Amortization schedule $4,000,000 ÷ 3.16987 = $1,261,881 amount (from Table 4) installment of loan n = 4, i = 10% payment Cash Effective Decrease in Outstanding […]

Accounting Chapter 14 Homework Discount Bonds Payable Difference Bonds Payable

Exercise 14–4 1. January 1, 2016 Interest $4,000,000¥ x 11.46992 * = $45,879,680 Principal $80,000,000 x 0.31180 ** = 24,944,000 Present value (price) of the bonds $70,823,680 ¥ 5% x $80,000,000 * Present value of an ordinary annuity of $1: […]

Accounting Chapter 14 Homework Under The Modified Terms Total Cash Paid

Chapter 14 Bonds and Long-Term Notes QUESTIONS FOR REVIEW OF KEY TOPICS Question 14–1 Periodic interest is calculated as the effective interest rate times the amount of the debt outstanding during the period. This same principle applies to the flip […]

Accounting Chapter 14 Homework Unnatural will report the loss from the change in the fair value of the bonds in net

Principal $240,000,000 x 0.31180 ** = 74,832,000 Present value (price) of the bonds $212,471,040 ¥ 5% x $240,000,000 * present value of an ordinary annuity of $1: n=20, i=6% ** present value of $1: n=20, i=6% Cash (price determined above) […]

Accounting Chapter 13 Homework Liability Refundable Deposits Sales Taxes Payable Accrued

Student Name: Class: Debit Credit 14,000,000 Maturity (January 31, 2017) 420,000 14,000,000 14,560,000 «- Correct! 14,560,000 «- Correct! 140,000 420,000 14,000,000 Interest payable Notes payable Cash Cash Interest revenue L & T Bank Interest receivable Notes receivable 140,000 Issuance of […]

Accounting Chapter 13 Homework Professional Skills Development Activities The Following Are

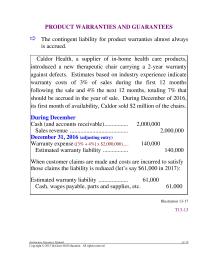

PRODUCT WARRANTIES AND GUARANTEES The contingent liability for product warranties almost always is accrued. Caldor Health, a supplier of in-home health care products, introduced a new therapeutic chair carrying a 2-year warranty against defects. Estimates based on industry experience […]

Accounting Chapter 13 Homework Most liabilities obligate the debtor to pay cash at specified times and

C CH HA AP PT TE ER R 1 13 3 C Cu ur rr re en nt t L Li ia ab bi il li it ti ie es s a an nd d C Co on nt ti […]

Accounting Chapter 13 Homework A liability is accrued if it is both probable that a loss will

13–78 Intermediate Accounting, 8/e Communication Case 13–10 Suggested Grading Concepts and Grading Scheme: Content (80% ) 20 Identifies the situation as a change in estimate. The liability was originally (appropriately) estimated as $750,000. The final settlement indicates the estimate should […]

Accounting Chapter 13 Homework Paid Sabbatical Leave Expense And Related Liability

Problem 13–12 (continued) Requirement 5 December 31, 2016 ($ in millions) Current Liabilities Accounts payable and accruals $ 43 6.5% bonds maturing on July 31, 2025, callable July 31, 2017 90 Current portion of 7% notes payable due May 2017 […]

Accounting Chapter 13 Homework Company Seeking Civil Penalties And Injunctive Relief

CMA Exam Questions 1. b. If an enterprise intends to refinance short-term obligations on a long- term basis and demonstrates an ability to consummate the refinancing, the obligations should be excluded from current liabilities and classified as noncurrent. Under U.S. […]

Accounting Chapter 13 Homework Such Disclosure Would Alert The Other Party

Exercise 13–8 Requirement 1 Cash …………………………………………………………….. 7,500 Deferred sales revenue ……………………………….. 7,500 Requirement 2 Cash …………………………………………………………….. 25,500 Liability—refundable deposits ……………………. 25,500 Requirement 3 Accounts receivable ……………………………………….. 856,000 Sales revenue ……………………………………………. 800,000 Sales taxes payable ([5% + 2%] x $800,000) ……… […]

Accounting Chapter 13 Homework The Low End The Range Accrued

Chapter 13 Current Liabilities and Contingencies QUESTIONS FOR REVIEW OF KEY TOPICS Question 13–1 A liability involves the past, the present, and the future. It is a present responsibility, to sacrifice assets in the future, caused by a transaction or […]

Accounting Chapter 13 Homework Problem 131 Requirement Schilling Motors Cash

Cash ……………………………………………………… 6,000,000 Notes payable ………………………………………. 6,000,000 Interest expense ($6,000,000 x 14% x 4/12) …….. 280,000 Interest payable …………………………………… 280,000 Interest expense ($6,000,000 x 14% x 2/12) …….. 140,000 Interest payable (from adjusting entry) ………….. 280,000 Notes payable (face amount) […]

Accounting Chapter 12 Homework Investment in NXS common shares

Student Name: Class: Debit Credit 28 2 30 «- Correct! Cash Loss on sale of investments Investment in Kansas Abstractors bonds 5.6 5.6 «- Correct! 44 44 «- Correct! 5.7 «- Correct! 5.6 0.1 3 3 «- Correct! Gain on […]

Accounting Chapter 12 Homework This Fact The Case Stated Media Generals

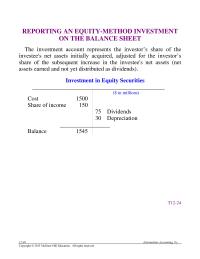

12-40 Intermediate Accounting, 8/e REPORTING AN EQUITY-METHOD INVESTMENT ON THE BALANCE SHEET The investment account represents the investor’s share of the investee’s net assets initially acquired, adjusted for the investor’s share of the subsequent increase in the investee’s net assets […]

Accounting Chapter 12 Homework Classification Depends 1 Whether The Investments Contractual

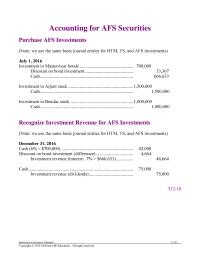

Accounting for AFS Securities Purchase AFS Investments (Note: we use the same basic journal entries for HTM, TS, and AFS investments) July 1, 2016 Investment in Masterwear bonds ……………………………………….. 700,000 Discount on bond investment …………………………………… 33,367 Cash ………………………………………………………………………. 666,633 Investment […]

Accounting Chapter 12 Homework Footnote Disclosures About The Reliability The Inputs

C CH HA AP PT TE ER R 1 12 2 I In nv ve es st tm me en nt ts s Overview In this chapter we cover various approaches used to account for investments that companies make in […]

Accounting Chapter 12 Homework Company Does Not Intend Sell The Impaired

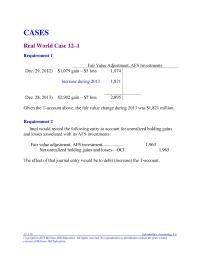

12–120 Intermediate Accounting, 8/e Real World Case 12–1 Requirement 1 Fair Value Adjustment, AFS Investments Dec. 29, 2012) $1,079 gain – $5 loss 1,074 Increase during 2013 1,821 Dec. 28, 2013) $2,902 gain – $7 loss 2,895 Given the T-account […]

Accounting Chapter 12 Homework Donald Company Bonds Include Only Interest And

Problem 12–11 Requirement 1 (note: requirement 1 has the same answer as does P 12–10) Purchase ($ in millions) Investment in Lavery Labeling shares …………………………………… 324 Cash …………………………………………………………………………….. 324 Net income No entry Dividends Cash (10 million shares x $2) […]

Accounting Chapter 12 Homework Corporation Shares American Instruments Bonds Totals Dec 31

Problem 12–4 (concluded) Then, to record it at fair value, we increase the investment by $70 – 66.21 = $3.79 million: Fair value adjustment ………………………… ……….. 3.79 Net unrealized holding gains and losses—I/S ($70 – 66.21) 3.79 Because these are […]

Accounting Chapter 12 Homework So to reclassify that unrealized loss, Bloom would reverse that entry.

So, net income will be decreased by $250,000, OCI by $150,000, and comprehensive income by $400,000. Solutions Manual, Vol.1, Chapter 12 12–61 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of […]

Accounting Chapter 12 Homework Moving from a negative $145 (Jan.1) to a positive $30 requires an increase of

Exercise 12–12 (continued) Requirement 2 Accumulated ($ in 000s) Unrealized Available-for-Sale Securities Cost Fair Value Gain (Loss) IBM shares—Dec. 31, 2016 $1,345 $1,275 $(70) Moving from a negative $145 (Jan.1) to a negative $70 requires an increase of $75: ——————————————————————————–———– […]

Accounting Chapter 12 Homework Exercise 126 The Fasb Accounting Standards Codification

Brief Exercise 12–15 Because the drop in the market price of stock is considered to be other-than- temporary, LED records the impairment of $450,000 ($4.50 x 100,000 shares) and reclassifies previously recognized unrealized losses of $100,000 ($1.00 x 100,000 shares) […]

Accounting Chapter 12 Homework However Only The Credit Loss Component Recognized

Question 12–1 Investment securities are classified as “held–to–maturity,” “trading,” or “available-for-sale” securities. Question 12–2 Increases and decreases in the market value between the time a debt security is acquired and the day it matures to a prearranged maturity value are […]

Accounting Chapter 12 Homework Unlike for trading securities, unrealized holding gains and losses are not

Investment in Oracle bonds ………………………………………………… 200 Cash …………………………………………………………………………….. 200 Cash ………………………………………………………………………………… 3 Investment revenue ………………………………………………………… 3 Cash ………………………………………………………………………………… 10 Investment revenue ………………………………………………………… 10 Cash ………………………………………………………………………………… 205 Investment in Oracle bonds …………………………………………….. 200 Gain on sale of investments …………………………………………….. 5 Investment […]

Accounting Chapter 11 Homework Machine Selling Price 2016 Depreciation Through Date

Student Name: Class: Balance Balance 12/31/2015 Increase Decrease 12/31/2016 Land (1) 175,000$ 312,500$ –$ 487,500$ Land improvements – 192,000 – 192,000 Market price 50$ Fair value of shares 1,250,000$ Correct! (1) Plant facility acquired from King 1/6/2016 – allocation to […]

Accounting Chapter 11 Homework Buildings Including Leasehold Improvements Are Generally Depreciated

IMPAIRMENT OF VALUE – A SUMMARY Type of Asset When to Test for Impairment Impairment Test To Be Held and Used: Tangible and finite- life intangible assets book value may not be recoverable. (undiscounted sum of estimated future cash flows […]

Accounting Chapter 11 Homework When Impairment Loss Recognized The Carrying Amount

INTERNATIONAL FINANCIAL REPORTING STANDARDS Valuation of Intangible Assets. IAS No. 38 allows a company to value an intangible asset subsequent to initial valuation at (1) cost less accumulated amortization or (2) fair value, if fair value can be determined by […]

Accounting Chapter 11 Homework Intermediate Accounting 8e Measuring Cost Allocation

CHAPTER 11 PROPERTY, PLANT, AND EQUIPMENT AND INTANGIBLE ASSETS: UTILIZATION AND IMPAIRMENT Overview This chapter completes our discussion of accounting for property, plant, and equipment and intangible assets. We address the allocation of the cost of these assets to the […]

Accounting Chapter 11 Homework The Approximate Average Service Life Caterpillars Depreciable

fair value less cost to sell. An impairment loss is recognized for any write-down to fair value less cost to sell. Solutions Manual, Vol.1, Chapter 11 11–93 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without […]

Accounting Chapter 11 Homework Information is material if it can have an effect on a decision made by users

Problem 11–13 Requirement 1 Hecala’s cost of the mineral mine is $13,721,871, determined as follows: Mining site $10,000,000 Development costs 3,200,000 Restoration costs 521,871 † $13,721,871 † $600,000 x 30% = $180,000 700,000 x 30% = 210,000 800,000 x 40% […]

Accounting Chapter 11 Homework The loss is the difference between book value and the recoverable amount

Problem 11–2 (continued) Requirement 2 CORD COMPANY Depreciation and Amortization Expense For the Year Ended December 31, 2016 Land Improvements: Cost $192,000 Straight-line rate (1 ÷ 12 years) x 8 1/3% Annual depreciation 16,000 Depreciation on land improvements for 2016: […]

Accounting Chapter 11 Homework Because book value (£220 million) exceeds this amount, a loss is indicated

Exercise 11–24 Requirement 1 IFRS requires an impairment loss to be recognized when an asset’s book value exceeds the higher of the asset’s value–in-use (present value of estimated future cash flows) and fair value less costs to sell. In this […]

Accounting Chapter 11 Homework If a revaluation surplus account relating to the same asset had existed

Exercise 11–3 (concluded) 5. Units-of-production: $115,000 – 5,000 = $.50 per unit depreciation rate 220,000 units 2016 10,000 units x $.50 = $ 5,000 2017 25,000 units x $.50 = $12,500 Exercise 11–4 Building depreciation: $5,000,000 – 200,000 = $160,000 […]

Accounting Chapter 11 Homework This amount is the difference between the initial value of

Question 11–1 The terms depreciation, depletion, and amortization all refer to the process of allocating the cost of property, plant, and equipment and finite-life intangible assets to periods of use. The only difference between the terms is that they refer […]

Accounting Chapter 11 Homework During The Three year Period Accumulated Depreciation Was

Sum-of-the-digits is {[8 (8 + 1)]÷2} = 36 2016 $220,000 x 8/36 = $48,889 2017 $220,000 x 7/36 = 42,778 Straight-line rate is 12.5% (1 ÷ 8 years) x 2 = 25% DDB rate 2016 $240,000 x 25% = $60,000 […]

Accounting Chapter 10 Homework Gain or Loss From Plant Asset Disposals

Student Name: Class: Requirement 1: Balance Balance 12/31/2015 Increase Decrease 12/31/2016 350,000$ 438,000$ 788,000$ 180,000 180,000 35,000 438,000$ Correct! 260,000$ 27,000 287,000$ Correct! 3,750$ 15,250 19,000$ Correct! Invoice cost Installation cost Cost recorded for new automobile 12/31/2016: Fair value of […]

Accounting Chapter 10 Homework Communication Skills Addition Communication Case 1011 Judgment

RESEARCH AND DEVELOPMENT ➢ All research and development costs are charged to expense in the period incurred. R&D costs entail a high degree of uncertainty of future benefits. It is difficult to match R&D costs with future revenues. […]

Accounting Chapter 10 Homework Illustration 1014 Retirements And Abandonments Are

GOODWILL (continued) The Smithson Corporation acquired all of the outstanding common stock of the Rider Corporation in exchange for $18 million in cash. Smithson assumed all of Rider’s long-term debt which had a fair value of $12 million at date […]

Accounting Chapter 10 Homework Requires The Capitalization In process Ramp’d Indefinite

C CH HA AP PT TE ER R 1 10 0 P PR RO OP PE ER RT TY Y, , P PL LA AN NT T, , A AN ND D E EQ QU UI IP PM ME EN […]

Accounting Chapter 10 Homework English Sentences Grammatically Clear And Well

Case 10–4 (concluded) Requirement 5 The three steps used to determine the amount of interest capitalized during a period are: 1. Determine the average accumulated expenditures for the period. 2. Multiply average accumulated expenditures by the appropriate interest rate(s). 3. […]

Accounting Chapter 10 Homework No reproduction or distribution without the prior written consent

Problem 10–8 (concluded) Requirement 3 If the exchange lacked commercial substance, no gain is recognized. Book value of old land + cash given = Initial value of new land $500,000 + 50,000 = $550,000 Journal entry (not required): New land […]

Accounting Chapter 10 Homework Present Value 1 I8 From Table Record

Exercise 10–30 Requirement 1 According to U.S. GAAP, the following costs would be expensed as R&D: Research for new formulas $2,425,000 Development of a new formula 1,600,000 Total $4,025,000 The legal and filing fees are capitalized as an intangible asset. […]

Accounting Chapter 10 Homework Instead, IFRS requires that government grants be recognized in income

Exercise 10–9 Requirement 1 Tractor ($5,000 cash + 18,783† present value of note) …………. 23,783 Discount on note payable (difference) ……………………….. 6,217 Cash …………………………………………………………………. 5,000 Note payable (face amount) ……………………………………. 25,000 † Present value of note payment: PV = $25,000 […]