Archives

Chapter 1 2 Statement Iii The Securities And Exchange Commission

Test Bank for Intermediate Accounting, Fifteenth Edition 1 – 12 61. FASB Technical Bulletins a. are similar to FASB Interpretations in that they establish enforceable standards under the AICPA’s Code of Professional Ethics. b. are issued monthly by the FASB […]

Chapter 10 1 Interest Cost That Capitalized Should Written Off

CHAPTER 10 ACQUISITION AND DISPOSITION OF PROPERTY, PLANT, AND EQUIPMENT IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Definition of plant assets. b 22. Characteristics of plant […]

Chapter 10 2 Dodson Company traded in a manual pressing machine

Acquisition and Disposition of Property, Plant, and Equipment 10 – 21 88. What is the avoidable interest for Arlington Company? a. $288,000 b. $927,615 c. $328,562 d. $704,415 89. What is the actual interest for Arlington Company? a. $1,758,000 b. […]

Chapter 10 3 Machinery With Cost 720000 And Accumulated Depreciation

Acquisition and Disposition of Property, Plant, and Equipment 10 – 37 Solution 10-133 EXERCISES Ex. 10-134—Nonmonetary exchange. A machine cost $240,000, has annual depreciation expense of $48,000, and has accumulated depreciation of $120,000 on December 31, 2014. On April 1, […]

Chapter 11 1 Composite Group Depreciation Depreciation System Whereby The

CHAPTER 11 DEPRECIATION, IMPAIRMENTS, AND DEPLETION IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Knowledge of depreciation accounting. b 22. Conceptual rationale for depreciation accounting. c 23. Depreciation and retaining […]

Chapter 11 2 The straight-line method is used for depreciation

Depreciation, Impairments, and Depletion 11 – 21 89. Falcon Corporation purchased a depreciable asset for $630,000 on January 1, 2012. The estimated salvage value is $63,000, and the estimated total useful life is 9 years. The straight-line method is used […]

Chapter 11 3 The methods of depreciation based upon output assume

Test Bank for Intermediate Accounting, Fifteenth Edition 11 – 34 BE. 11-127 (cont.) ____ 9. The methods of depreciation based upon output assume that obsolescence will not significantly affect the usefulness of the asset. ____ 10. The revision of prior […]

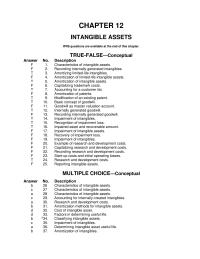

Chapter 12 1 What Type Intangible Asset This Agreement Between

CHAPTER 12 INTANGIBLE ASSETS IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description b 26 Characteristics of intangible assets. c 27 Characteristics of intangible assets. a 28 Characteristics of intangible […]

Chapter 12 2 Costs Goodwill From Costs Developing Business Combination

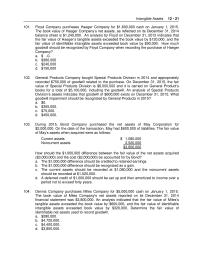

Intangible Assets 12 – 21 101. Floyd Company purchases Haeger Company for $1,600,000 cash on January 1, 2015. The book value of Haeger Company’s net assets, as reflected on its December 31, 2014 balance sheet is $1,240,000. An analysis by […]

Chapter 12 3 Wasserman Company Instructions Determine The Amount Goodwill

Test Bank for Intermediate Accounting, Fifteenth Edition 12 – 34 Ex. 12-138 What factors are considered in estimating the useful life of an intangible asset? Solution 12-138 Ex. 12-139 Barkley Corp. obtained a trade name in January 2013, incurring legal […]

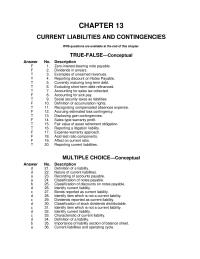

Chapter 13 1 Which The Following Situations May Give Rise

CHAPTER 13 CURRENT LIABILITIES AND CONTINGENCIES IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Definition of a liability. d 22. Nature of current liabilities. a 23. Recording […]

Chapter 13 2 Rao Co Introduced New Line Machines That

Current Liabilities and Contingencies 13 – 21 94. Craig borrowed $350,000 on October 1, 2014 and is required to pay $360,000 on March 1, 2015. What amount is the note payable recorded at on October 1, 2014 and how much […]

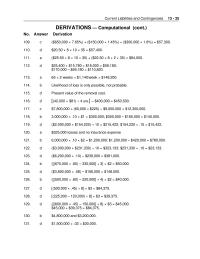

Chapter 13 3 Current Liabilities Interest Payable Note Payable rao Company

Current Liabilities and Contingencies 13 – 35 DERIVATIONS — Computational (cont.) No. Answer Derivation 109. c ($650,000 × 7.65%) + ($150,000 × 1.45%) + ($300,000 × 1.8%) = $57,300. 110. d $20.50 × 8 × 10 × 35 = $57,400. […]

Chapter 14 1 Amortization of premium and discount

CHAPTER 14 LONG-TERM LIABILITIES IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description a 21. Liability identification. a 22. Bond terms. b 23. Definition of “debenture bonds.” a P24. Definition […]

Chapter 14 2 April And October What Amount Did Spear

Long-Term Liabilities 14 – 21 83. On January 1, Martinez Inc. issued $5,000,000, 11% bonds for $5,325,000. The market rate of interest for these bonds is 10%. Interest is payable annually on December 31. Martinez uses the effective-interest method of […]

Chapter 14 3 Use The Effective interest Method Credit Cash Debit

Long-Term Liabilities 14 – 33 Solution 14-117 BE. 14-118—Bond issue price and premium amortization. On January 1, 2015, Piper Co. issued ten-year bonds with a face value of $3,000,000 and a stated interest rate of 10%, payable semiannually on June […]

Chapter 15 1 Porter Corp Purchased Its Own Par Value

CHAPTER 15 STOCKHOLDERS’ EQUITY IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description c 21. Nature of stockholders’ interest. b 22. Pre-emptive right. d 23. Pre-emptive right. b S24. Definition […]

Chapter 15 2 Pierson Corporation owned 10,000 shares of Hunter Corporation

Stockholders’ Equity 15 – 21 87. Luther Inc., has 4,000 shares of 6%, $50 par value, cumulative preferred stock and 100,000 shares of $1 par value common stock outstanding at December 31, 2015, and December 31, 2014. The board of […]

Chapter 15 3 Cash Preferred Stock Paid in Capital

Stockholders’ Equity 15 – 37 DERIVATIONS — CPA Adapted (cont.) No. Answer Derivation EXERCISES Ex. 15-131—Lump sum issuance of stock. Parker Corporation has issued 2,000 shares of common stock and 400 shares of preferred stock for a lump sum of […]

Chapter 16 1 The Discount From Market Price Small The

CHAPTER 16 DILUTIVE SECURITIES AND EARNINGS PER SHARE IFRS questions are available at the end of this chapter. TRUE-FALSE—Dilutive Securities—Conceptual Answer No. Description MULTIPLE CHOICE—Dilutive Securities, Conceptual Answer No. Description d 21. Nature of convertible bonds. d 22. Recording conversion […]

Chapter 16 2 What amount of compensation expense should Korsak recognize

Dilutive Securities and Earnings per Share 16 – 21 70. Weiser Corp. on January 1, 2012, granted stock options for 40,000 shares of its $10 par value common stock to its key employees. The market price of the common stock […]

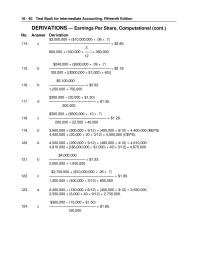

Chapter 16 3 Prepare the entry to record the interest expense

Test Bank for Intermediate Accounting, Fifteenth Edition 16 – 40 DERIVATIONS — Earnings Per Share, Computational (cont.) No. Answer Derivation $3,000,000 + ($10,000,000 × .06 × .7) 114. c ————————————————— = $2.85. 3 800,000 + (160,000 × —– ) + […]

Chapter 17 1 Accrued Interest Will Received The Seller Even

CHAPTER 17 INVESTMENTS IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description c 21. Debt securities. b 22. Valuation of debt securities. c 23. Held-to-maturity securities. c 24. Unrealized gain/loss […]

Chapter 17 2 Kramer Company’s trading securities portfolio which is

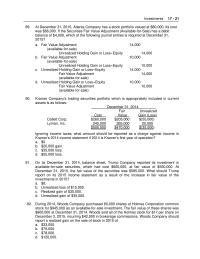

Investments 17 – 21 89. At December 31, 2015, Atlanta Company has a stock portfolio valued at $80,000. Its cost was $66,000. If the Securities Fair Value Adjustment (Available-for-Sale) has a debit balance of $4,000, which of the following journal […]

Chapter 17 3 Each Investment Considered Dopplers Management Available

Test Bank for Intermediate Accounting, Fifteenth Edition 17 – 34 Ex. 17-125—Fair value and equity methods. Fill in the dollar changes caused in the Investment account and Dividend Revenue or Investment Revenue account by each of the following transactions, assuming […]

Chapter 18 1 None These Answers Are Correct 41 Cost

CHAPTER 18 REVENUE RECOGNITION IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual MULTIPLE CHOICE—Conceptual Answer No. Description c 21. Revenue recognition principle. b 22. Definition of “realized.” a 23. Definition of “earned.” b S24. Revenue recognition representations. […]

Chapter 18 2 Gorman uses the completed-contract method

Revenue Recognition 18 – 21 85. Hiser Builders, Inc. is using the completed-contract method for a $9,800,000 contract that will take two years to complete. Data at December 31, 2015, the end of the first year, are as follows: Costs […]

Chapter 18 3 Instructions A Compute The Percentage Completion The

Revenue Recognition 18 – 37 Solution 18-123 (cont.) EXERCISES Ex. 18-124—Journal entries—percentage-of-completion. Dixon Construction Company was awarded a contract to construct an interchange at the junction of U.S. 94 and Highway 30 at a total contract price of $12,000,000. The […]

Chapter 19 1 Interest Received Municipal Bonds Fines Resulting From

CHAPTER 19 ACCOUNTING FOR INCOME TAXES IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description b 21. Differences between taxable and accounting income. c 22. Differences between taxable and accounting […]

Chapter 19 2 which of the following deferred tax accounts and balances

Accounting for Income Taxes 19 – 21 80. At the end of 2015, which of the following deferred tax accounts and balances is reported on Rowen, Inc.’s balance sheet? Account _ Balance a. Deferred tax asset $25,600 b. Deferred tax […]

Chapter 19 3 When should a deferred tax asset be reduced by a valuation

Test Bank for Intermediate Accounting, Fifteenth Edition 19 – 34 Accounting for Income Taxes 19 – 35 Solution 19-108 (cont.) Ex. 19-109—Recognition of deferred tax asset. (a) Describe a deferred tax asset. (b) When should a deferred tax asset be […]

Chapter 2 1 Provide Information That Useful Those Making Investing

CHAPTER 2 CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description c 21. GAAP defined. d 22. Purpose of conceptual framework. c 23. Conceptual framework. […]

Chapter 2 2 Relevance And Faithful Representation 3 Comparability And

Test Bank for Intermediate Accounting, Fifteenth Edition 2 – 18 89. The measurement principle includes the a. fair value principle only. b. historical cost principle only. c. revenue recognition principle and expense recognition principle. d. historical cost principle and the […]

Chapter 20 1 All These Are Included The Computation 35

CHAPTER 20 ACCOUNTING FOR PENSIONS AND POSTRETIREMENT BENEFITS IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Factors considered by actuaries. c 22. Process of funding a pension […]

Chapter 20 2 Test Bank For Intermediate Accounting

Accounting for Pensions and Postretirement Benefits 20–21 77. The balance of the projected benefit obligation at December 31, 2015 is a. $2,490,000. b. $2,355,000. c. $2,340,000. d. $2,310,000. 78. The fair value of plan assets at December 31, 2015 is […]

Chapter 20 3 Plan Assets Fair Value Projected Benefit Obligation

Test Bank for Intermediate Accounting, Fifteenth Edition 20–38 Instructions (a) Compute the amount of postretirement expense for 2015. (Show computations.) (b) Compute the amount of the APBO at December 31, 2015. PROBLEMS Pr. 20-119—Measuring, recording, and reporting pension expense and […]

Chapter 23 2 Based upon this information what amount will be shown

Statement of Cash Flows 23 – 21 73. During 2015, Orton Company earned net income of $464,000 which included deprecia- tion expense of $78,000. In addition, the company experienced the following changes in the account balances listed below: Increases Decreases […]

Chapter 23 3 Noncash Investing And Financing Activities Purchase Machinery

Statement of Cash Flows 23 – 41 Ex. 23-121—Calculations for statement of cash flows. Milner Co. sold a machine that cost $74,000 and had a book value of $44,000 for $48,000. Data from Milner’s comparative balance sheets are: 12/31/15 12/31/14 […]

Chapter 23 4 The Accumulated Depreciation account has been credited

Test Bank for Intermediate Accounting, Fifteenth Edition 23 – 52 Pr. 23-128 (cont.) 5. The wholly owned subsidiary reported a net loss for the year of $20,000. The loss was recorded by the parent. 6. At January 1, 2015, the […]

Chapter 3 2 The following balances have been excerpted from Olsen’s balance

The Accounting Information System 3 – 21 98. Big-Mouth Frog Corporation had revenues of $300,000, expenses of $200,000, and dividends of $45,000. When Income Summary is closed to Retained Earnings, the amount of the debit or credit to Retained Earnings […]

Chapter 3 3 Prepare The Entry Record Cash Interest Received

The Accounting Information System 3 – 35 *Ex. 3-131—Accrual basis. The records for Kiley Company showed the following for 2014: Jan. 1 Dec. 31 Unearned revenue $1,100 $2,160 Accrued revenue 1,260 920 Cash collected during the year for revenue, $65,000 […]

Chapter 4 1 Changes Estimates Are Considered Errors Extraordinary Items

CHAPTER 4 INCOME STATEMENT AND RELATED INFORMATION IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description c 21. Elements of the income statement. d 22. Usefulness of the income statement. […]

Chapter 4 2 It declared and paid common stock dividends

Income Statement and Related Information 4 – 21 90. In 2014, Esther Corporation reported net income of $600,000. It declared and paid preferred stock dividends of $150,000 and common stock dividends of $60,000. During 2014, Esther had a weighted average […]

Chapter 4 3 Income Before Extraordinary Item Extraordinary Loss Earthquake

Test Bank for Intermediate Accounting, Fifteenth Edition 4 – 36 Solution 4-119 Ex. 4-120—Income statement classifications. Indicate the major section or subsection of a multiple-step income statement in which each of the following items would usually appear: a. Advertising b. […]

Chapter 5 1 Unearned Revenue Stock Dividends Distributable The Currently

CHAPTER 5 BALANCE SHEET AND STATEMENT OF CASH FLOWS IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Limitation of the balance sheet. c 22. Uses of the […]

Chapter 5 3 The reserve for contingencies has been created

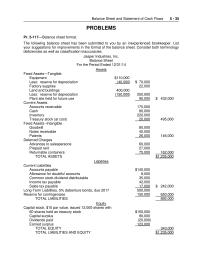

Balance Sheet and Statement of Cash Flows 5 – 35 PROBLEMS Pr. 5-117—Balance sheet format. The following balance sheet has been submitted to you by an inexperienced bookkeeper. List your suggestions for improvements in the format of the balance sheet. […]

Chapter 6 1 Accounting And The Time Value Money

CHAPTER 6 ACCOUNTING AND THE TIME VALUE OF MONEY IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description a 21. Appropriate use of an annuity due table. d 22. Time […]

Chapter 6 2 Hiller Corporation makes an investment today

Accounting and the Time Value of Money 6 – 21 95. Spencer Corporation will invest $20,000 every December 31st for the next six years (2014 – 2019). If Spencer will earn 12% on the investment, what amount will be in […]

Chapter 6 3 Carey Wishes Sell The Land Now Has

Test Bank for Intermediate Accounting, Fifteenth Edition 6 – 34 BE. 6–135—Present value of an investment in equipment. (Tables needed.) Find the present value of an investment in equipment if it is expected to provide annual savings of $30,000 for […]

Chapter 7 1 Classification of cash restricted for plant expansion

CHAPTER 7 CASH AND RECEIVABLES IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 26. Identification of cash items. b 27. Identification of cash items. d 28. Classification of […]

Chapter 7 2 Maxwell Estimates The Recourse Obligation 2400 What

Cash and Receivables 7 – 21 98. Wellington Corp. has outstanding accounts receivable totaling $6.5 million as of December 31 and sales on credit during the year of $24 million. There is also a credit balance of $12,000 in the […]

Chapter 7 3 Note Discount Amortization For Green Company Under

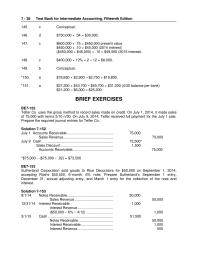

Test Bank for Intermediate Accounting, Fifteenth Edition 7 – 36 BRIEF EXERCISES BE7–152 Telfer Co. uses the gross method to record sales made on credit. On July 1, 2014, it made sales of 75,000 with terms 2/10 n/30. On July […]

Chapter 8 1 Merchandising and manufacturing inventory accounts

CHAPTER 8 VALUATION OF INVENTORIES: A COST-BASIS APPROACH IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description c 21. Identify manufacturer inventory similar to merchandise inventory. d 22. Sales with […]

Chapter 8 2 Hudson, Inc. is a calendar-year corporation

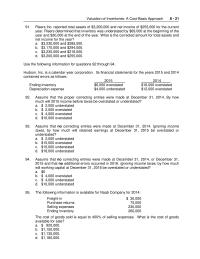

Valuation of Inventories: A Cost-Basis Approach 8 – 21 91. Risers Inc. reported total assets of $3,200,000 and net income of $255,000 for the current year. Risers determined that inventory was understated by $69,000 at the beginning of the year […]

Chapter 8 3 Payment was made thirty days after the purchase

Valuation of Inventories: A Cost-Basis Approach 8 – 37 No. Answer Derivation DERIVATIONS — CPA Adapted No. Answer Derivation 134. a Conceptual. 135. c $380,000 + $8,000 – $2,000 = $386,000. 136. d $130,000 + $14,000 + $525,000 + $70,000 […]

Chapter 9 1 Reason for reporting inventory at sales price

CHAPTER 9 INVENTORIES: ADDITIONAL VALUATION ISSUES IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Knowledge of lower-of-cost-or-market valuations. d 22. Recording inventory loss under the loss method. […]

Chapter 9 2 Cost Goods Available For Sale Ending Inventory

Inventories: Additional Valuation Issues 9 – 21 87. Confectioners, a chain of candy stores, purchases its candy in bulk from its suppliers. For a recent shipment, the company paid $1,500 and received 8,500 pieces of candy that are allocated among […]

Chapter 9 3 Then enter the amount that should be used for lower of

Test Bank for Intermediate Accounting, Fifteenth Edition 9 – 38 BRIEF EXERCISES BE. 9–139—Lower-of-cost-or-market. Determine the proper unit inventory price in the following independent cases by applying the lower of cost or market rule. Circle your choice. 1 2 3 […]

Exam D Show the proper disclosures in the stockholders’

COMPREHENSIVE EXAMINATION D PART 4 (Chapters 15-17) Approximate Problem Topic Time D-I Treasury Stock. 20 min. D-II *Cash Dividends. 10 min. D-III Stock Dividends and Stock Splits. 10 min. D-IV Earnings Per Share Concepts. 10 min. D-V Earnings Per Share […]

Exam E Pinkley Company For Machinery Which Was Carried

COMPREHENSIVE EXAMINATION E PART 5 (Chapters 18-21) Approximate Problem Topic Time E-I Long-Term Contracts. 15 min. E-II Installment Sales Method. 20 min. E-III Deferred Income Taxes. 25 min. E-IV Pensions. 15 min. E-V Leases. 25 min. 100 min. Test Bank […]

Exam F The Following Calculations Present Depreciation Both Bases

COMPREHENSIVE EXAMINATION F PART 6 (Chapters 22-24) Approximate Problem Topic Time F-I Multiple Choice Questions. 25 min. F-II Statement of Cash Flows. 25 min. F-III Accounting Changes, Error Corrections, and Prior Period Adjustments. 30 min. F-IV * Analysis of Financial […]