Archives

978-0077862206 Chapter 1 Lecture Note

CHAPTER 1 INTRODUCTION TO INTERNATIONAL ACCOUNTING Chapter Outline I. International accounting is an extremely broad topic. A. At a minimum it focuses on the accounting issues unique to multinational corporations, especially with respect to foreign operations. B. At the other […]

978-0077862206 Chapter 1 Solution Manual

Chapter 01 – Introduction to International Accounting 1. In 2011, companies worldwide exported over $18.3 trillion worth of merchandise. Although international trade has existed for thousands of years, recent growth in trade has been phenomenal. Over the period 1996-2011, U.S. […]

978-0077862206 Chapter 10 Lecture Note

CHAPTER 10 ANALYSIS OF FOREIGN FINANCIAL STATEMENTS Chapter Outline I. Reasons to analyze financial statements of foreign companies include: making foreign portfolio investment decisions, making foreign merger and acquisition decisions, making credit decisions about foreign customers, evaluating foreign suppliers, and […]

978-0077862206 Chapter 10 Solution Manual Part 1

Chapter 10 – Analysis of Foreign Financial Statements Answers to Questions 1. Investors can diversify their risk by including shares of foreign companies in their investment portfolio. Correlations in the returns (increases and decreases in stock prices) earned 2. Ford […]

978-0077862206 Chapter 10 Solution Manual Part 2

Chapter 10 – Analysis of Foreign Financial Statements 11. Vale S.A. (Statement of Added Value) a. The external parties who might be most interested in Vale’s Statement of Added Value b. Personnel; Taxes, rates and contribution less Taxes paid recover; […]

978-0077862206 Chapter 10 Solution Manual Part 3

Ratio Local GAAP U.S. GAAP Current ratio 2.70 2.71 Total asset turnover 0.40 0.40 Debt/equity ratio 0.74 0.75 Times interest earned 25.9 27.6 Net profit margin 26.7% 25.9% Operating profit margin 39.4% 39.3% 15. (continued) Worksheet for Restatement of Balance […]

978-0077862206 Chapter 11 Lecture Note

CHAPTER 11 INTERNATIONAL TAXATION Chapter Outline I. Taxes are one of the most significant costs incurred by business enterprises. Taxes can be an important factor in making decisions related to foreign operations including: in which country should an operation be […]

978-0077862206 Chapter 11 Solution Manual Part 1

Chapter 11 – International Taxation Answers to Questions 1. MNCs can finance their foreign operations by making capital contributions (equity) or 2. In some countries, local governments impose a separate tax on business income in addition to that levied by […]

978-0077862206 Chapter 11 Solution Manual Part 2

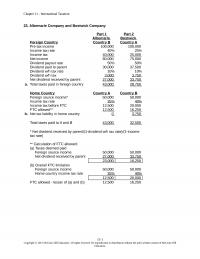

Chapter 11 – International Taxation 23. Albemarle Company and Bostwick Company Part 1 Part 2 Albemarle Bostwick Foreign Country Country B Country A Home Country Country A Country B Foreign source income* 50,000 50,000 Income tax rate 25% 40% Income […]

978-0077862206 Chapter 12 Lecture Note

CHAPTER 12 INTERNATIONAL TRANSFER PRICING Chapter Outline I. Two factors heavily influence the manner in which international transfer prices are determined: (a) corporate objectives, and (b) national tax laws. There are a variety of cost, especially tax, minimization objectives that […]

978-0077862206 Chapter 12 Solution Manual Part 1

Chapter 12 – International Transfer Pricing Answers to Questions 1. Transfer prices must be determined for the following intercompany transfers: 2. Cost minimization objectives that companies might wish to achieve through transfer pricing include: minimization of income taxes, withholding taxes […]

978-0077862206 Chapter 12 Solution Manual Part 2

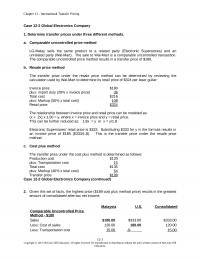

Chapter 12 – International Transfer Pricing Case 12-2 Global Electronics Company 1. Determine transfer prices under three different methods. a. Comparable uncontrolled price method LG-Malay sells the same product to a related party (Electronic Superstores) and an b. Resale price […]

978-0077862206 Chapter 13 Lecture Note

CHAPTER 13 STRATEGIC ACCOUNTING ISSUES IN MULTINATIONAL CORPORATIONS Chapter Outline I. The strategic issues faced by a MNC are related to strategy formulation and strategy implementation. A. Strategy formulation is the process of deciding on the goals of the organization […]

978-0077862206 Chapter 13 Solution Manual Part 1

Answers to Questions 1. A strategy indicates the general direction in which a firm plans to move to attain its goals. 2. A strategy indicates the general direction in which a firm plans to move to attain its goals. The […]

978-0077862206 Chapter 13 Solution Manual Part 2

Chapter 13 – Strategic Accounting Issues in Multinational Corporations Sales (25,000 units @ $50) 1,250,000 Project cash flow to Sedona: Cash flow to Sedona is the same as annual project cash flow in China because cash equal to depreciation may […]

978-0077862206 Chapter 14 Lecture Note

CHAPTER 14 COMPARATIVE INTERNATIONAL AUDITING AND CORPORATE GOVERNANCE Chapter Outline I. Auditing is an integral part of multinational corporate governance. A. Auditing is expected to improve the precision, quality and reliability of information made available to the market, and to […]

978-0077862206 Chapter 14 Solution Manual

Chapter 14 – Comparative International Auditing and Corporate Governance Answers to Questions 1. Auditing issues should be of concern to any firm that seeks funds from the capital market, because auditing improves the quality and reliability of the financial information […]

978-0077862206 Chapter 15 Lecture Note

CHAPTER 15 INTERNATIONAL CORPORATE SOCIAL REPORTING Chapter Outline 1. Traditionally, companies have focused on economic aspects in external reporting. However, in recent years there has been a growing global interest in CSR, based on sustainable development. 2. Sustainable development requires […]

978-0077862206 Chapter 15 Solution Manual

Chapter 15 – International Corporate Social Reporting Answers to Questions: 1. CSR is providing information by companies about both social and environmental 2. A number of theories have been used to explain CSR practices by firms, such as stakeholder theory […]

978-0077862206 Chapter 2 Lecture Note

CHAPTER 2 WORLDWIDE ACCOUNTING DIVERSITY Chapter Outline I. Considerable differences exist across countries in the accounting treatment of many items. These differences can result in significantly different amounts being reported in the financial statements prepared by companies using different GAAP. […]

978-0077862206 Chapter 2 Solution Manual

Chapter 02 – Worldwide Accounting Diversity 1. Companies in North America commonly present assets in order of liquidity, beginning with 2. The two major types of legal system are “code law” and “common law.” Code law countries tend to have […]

978-0077862206 Chapter 3 Lecture Note

CHAPTER 3 INTERNATIONAL CONVERGENCE OF FINANCIAL REPORTING Chapter Outline I. Accounting harmonization is a process that reduces alternatives while retaining a high degree of flexibility in accounting practices. A. Harmonization is different from standardization (or uniformity) which implies the elimination […]

978-0077862206 Chapter 3 Solution Manual

Chapter 03 – International Convergence of Financial Reporting Answers to Questions 1. The ultimate goal of both harmonization and convergence is to achieve international comparability in financial reporting, and both are processes that take place over time. 2. The potential […]

978-0077862206 Chapter 4 Lecture Note

CHAPTER 4 INTERNATIONAL FINANCIAL REPORTING STANDARDS: PART I Chapter Outline I. The International Accounting Standards Board (IASB) had 28 International Accounting Standards (IAS) and 13 International Financial Reporting Standards (IFRS) in force in 2013. A. In 2002, the IASB and […]

978-0077862206 Chapter 4 Solution Manual Part 1

Chapter 04 – International Financial Reporting Standards: Part I Answers to Questions 1. The types of differences that exist between IFRS and U.S. GAAP can be classified as: 2. In applying the lower of cost and market rule for inventories, […]

978-0077862206 Chapter 4 Solution Manual Part 2

Chapter 04 – International Financial Reporting Standards: Part I 23. Iptat International – Property, Plant and Equipment (revaluation model) a. Adjustment (a) relates to the depreciation of the revaluation amount on fixed assets. b. Adjustment (b) relates to the revaluation […]

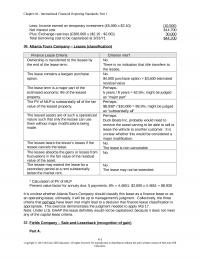

978-0077862206 Chapter 4 Solution Manual Part 3

Chapter 04 – International Financial Reporting Standards: Part I 36. Atlanta Tours Company – Leases (classification) Finance Lease Criteria Criterion met? Ownership is transferred to the lessee by the end of the lease term. No. There is no indication that […]

978-0077862206 Chapter 5 Lecture Note

CHAPTER 5 INTERNATIONAL FINANCIAL REPORTING STANDARDS: PART II Chapter Outline I. International Financial Reporting Standards (IFRS) issued by the International Accounting Standard Board (IASB) comprise a comprehensive set of standards providing guidance for the preparation and presentation of financial statements. […]

978-0077862206 Chapter 5 Solution Manual Part 1

Answers to Questions 1. A provision is a liability of uncertain timing or amount. A provision must be recognized when: 2. A contingent liability is (a) a possible obligation or (b) a present obligation that is not recognized as a […]

978-0077862206 Chapter 5 Solution Manual Part 2

Chapter 05 – International Financial Reporting Standards: Part II 28. Cypress Company – Revenue Recognition (rendering of services) IAS 18 indicates that, when the outcome of a service transaction (a) can be estimated reliably and (b) it is probable that […]

978-0077862206 Chapter 5 Solution Manual Part 3

39. Acceptable Treatments Acceptable under IFRS U.S. GAAP Both Neither the debt. Case 5-1 S. A. Harrington Company Reconciliation from U.S. GAAP to IFRS 2015 Income under U.S. GAAP $5,000,0 00 Adjustments: Restructuring charge (300,000) Past service cost 4,000 • […]

978-0077862206 Chapter 6 Lecture Note

CHAPTER 6 COMPARATIVE ACCOUNTING Chapter Outline China I. There are some unique features in the accounting profession in China. They include the following: A. Until the 1980s, those who carried out accounting work were not held in high regard in […]

978-0077862206 Chapter 6 Solution Manual

Chapter 06 – Comparative Accounting Answers to Questions 1. Gradual capital market liberalization will open up international investment opportunities for 2. The economic reforms have increased demand for accounting services in many ways. Key aspects of the economic reforms in […]

978-0077862206 Chapter 7 Lecture Note

CHAPTER 7 FOREIGN CURRENCY TRANSACTIONS AND HEDGING FOREIGN EXCHANGE RISK Chapter Outline I. There are a variety of exchange rate arrangements in use around the world. A majority of national currencies are allowed to fluctuate in value against other currencies […]

978-0077862206 Chapter 7 Solution Manual Part 1

Chapter 07 – Foreign Currency Transactions and Hedging Foreign Exchange Risk Answers to Questions 1. Under the two-transaction perspective, an export sale (import purchase) and the 2. Foreign currency receivables resulting from export sales are revalued at the end of […]

978-0077862206 Chapter 7 Solution Manual Part 2

Chapter 07 – Foreign Currency Transactions and Hedging Foreign Exchange Risk Impact on net income over both periods: $176.36 + ($20,976.36) = $20,800; equal to cash outflow. 16. Alexandria Company – Forward Contract Cash Flow Hedge of Foreign Currency Denominated […]

978-0077862206 Chapter 7 Solution Manual Part 3

Chapter 07 – Foreign Currency Transactions and Hedging Foreign Exchange Risk Case 7-1 Zorba Company 1. Unhedged Foreign Currency Liability 12/1/Y1 Inventory $50,000 Case 7-1 Zorba Company (continued) 2. Forward Contract Fair Value Hedge of a Recognized Foreign Currency Liability […]

978-0077862206 Chapter 8 Lecture Note

CHAPTER 8 TRANSLATION OF FOREIGN CURRENCY FINANCIAL STATEMENTS Chapter Outline I. In preparing consolidated financial statements on a worldwide basis, the foreign currency financial statements prepared by foreign operations must be translated into the parent company’s reporting currency. A. The […]

978-0077862206 Chapter 8 Solution Manual Part 1

Chapter 08 – Translation of Foreign Currency Financial Statements Answers to Questions 1. The two major issues related to the translation of foreign currency financial statements are: 2. Balance sheet exposure arises when a foreign currency balance is translated at […]

978-0077862206 Chapter 8 Solution Manual Part 2

Chapter 08 – Translation of Foreign Currency Financial Statements Part I (a). Polish zloty is the functional currency – Current rate method Exchange PLN Rate U.S. $ Sales 12,500,000 0.175 2,187,500 Case 8-1 Columbia Corporation (continued) Accounts payable 1,250,000 0.150 […]

978-0077862206 Chapter 9 Lecture Note

CHAPTER 9 ADDITIONAL FINANCIAL REPORTING ISSUES Chapter Outline I. In addition to issues involving the accounting for foreign currency, three financial reporting issues of international importance are: (a) accounting for changing prices (inflation accounting), (b) accounting for business combinations and […]

978-0077862206 Chapter 9 Solution Manual Part 1

Chapter 09 – Additional Financial Reporting Issues Answers to Questions 1. Historical cost accounting causes assets to be significantly understated in a country experiencing high inflation. Understated assets, such as inventory and fixed assets, leads to understated expenses, such as […]

978-0077862206 Chapter 9 Solution Manual Part 2

8. (continued) Geographic Areas The company provides disclosures for three countries, each of which has 13% or more of total external revenues. Russia has 11% of total revenues, but is not disclosed separately, which suggests that the company is using […]

AC 12735

In what countries would one expect auditing standards to evolve based on the needs perceived by the auditing profession? A. Code law countries B. Members of the European Union C. Countries that follow common law D. Countries with strong accounting […]

AC 22570

Under U.S. GAAP, when new debt is issued for old debt: A. extinguishment costs are deferred and amortized over the term of the new debt. B. debt extinguishment costs are expensed as incurred. C. modification costs are amortized over the […]

AC 34535

Which of the following is the role of a performance evaluation system in a multinational corporation? A. Monitor organizational effectiveness B. Identify areas that need improvement C. Assess how well division managers are doing D. All of the above Answer: […]

AC 51600

Which is NOT a common risk associated with local authorities’ scrutiny of a company’s transfer prices? A. Potential double taxation B. Uncertainty as to the group’s worldwide tax burden C. Problems in relationships with local tax authorities D. Discovery of […]

AC 56067

What must large Japanese corporations report for years ending after 2004 due to recent amendments to the Japanese commercial code? A. Statement of changes in financial position B. Consolidated financial statements C. Retained earnings statement D. Cash flow statement Answer: […]

AC 72451

What is the basis for Morgan Stanley Dean Witter’s “Apples to Apples” system for financial statement analysis? A. Adjustments needed to compare companies within a single country B. Adjustments needed to compare international companies within specific industries C. Adjustments needed […]

AC 77517

What is one thing that few companies tend to report on in their corporate social report disclosures? A. International disaster response B. The risk of legal action or business disruptions caused by climate issues C. The level of GHG reduction […]

Acc 13477

What does G3 represent? A. An annual summit of countries committed to the reduction of GHGs B. The third type of GHG C. The United States, Canada and Mexico D. The third generation of the GRI’s Sustainability Reporting Guidelines Answer: […]

Acc 61723

Under what condition does the IRS consider the resale price method acceptable as a transfer price? A. The subsidiary is a foreign controlled corporation. B. The related party is merely a distributor of finished goods. C. The divisions are part […]

Acc 71880

Blanco Chemical Company spent €15,000,000 in development efforts to create a fertilizer for which it was able to obtain a patent; however, the expected distribution costs make it infeasible to market the chemical in the foreseeable future. According to IAS […]

ACC 72846

What is an advance pricing agreement? A. A transfer price that is negotiated between two divisions of a decentralized organization B. A transfer pricing method accepted by the IRS before an intercompany transaction is completed C. A contract between a […]

ACC 76656

Auditors in the United Kingdom often include disclaimers of liability in their audit reports. According to the U.S. Securities and Exchange Commission, how effective is this approach to limiting civil liabilities? A. It will have no effect when included in […]

Accounting 36388

Which of the following is NOT a factor influencing the probability that an auditor will detect an accounting error? A. Competence of the auditor B. Quality review and monitoring C. Financial reporting requirements D. Independence of the auditor Answer: Which […]

Accounting 54257

Why must the two-transaction perspective be used for recording foreign currency transactions under U.S. GAAP? A. The two-transaction perspective is required under IFRS. B. U.S. GAAP requires conservatism in financial reporting. C. All other methods are excessively complicated to use […]

ACCT 56665

What is the likely outcome of using performance measures that subsidiary managers perceive to be unachievable? A. Frustrated managers B. Diligent attention to operational efficiency C. Success D. Optimal decision-making Answer: What is another name by which corporate social reporting […]

Acct 82240

Which of the following statements is true about U.S. taxation of foreign subsidiaries? A. The U.S. income taxes income generated by subsidiaries incorporated in foreign countries. B. U.S. multinationals do not pay tax on their worldwide income if incorporated in […]

ACCT 87552

In following the international norm concerning tax jurisdiction, how would double taxation be eliminated? A. The subsidiary’s home country would allow tax credits for taxes paid to the parent’s home country. B. The parent company’s home country would allow tax […]

ACT 32708

The balanced scorecard includes non-financial measures of performance with the financial measures of performance traditionally used. Which of the following are included in the balanced scorecard? A. Customer satisfaction B. Internal business processes C. Innovation and learning D. All of […]

ACT 35552

What is a key objective of a company’s performance evaluation system? A. To determine how much to pay executives in bonuses and other compensation B. To ensure that the domestic and foreign operations are achieving their objectives C. To control […]

MET MG 43302

Johnson Ltd. determined that the net present value of an investment in technological improvements at its plant in France would be €10,000,000 if pending litigation was resolved in the company’s favor and would be €2,000,000 if the courts ruled against […]

MET MG 53716

Privatization of Mexican businesses has been encouraged by: A. North American Free Trade Agreement (NAFTA). B. governmental attempts to improve long-term economic growth. C. loosening restrictions on foreign investment. D. All of the above Answer: What would be a logical […]

MET MG 54029

Which of the following statements is true about international transfer pricing? A. It is a violation of the Foreign Corrupt Practices Act. B. It is accomplished using guidelines set up by the FASB. C. It can be used to minimize […]

MET MG 79796

The Canadian Institute of Chartered Accountants (CICA) has taken a principles-based approach to auditor independence, whereas the Federation des Experts Comptables Europeens (FEE) has taken a conceptual approach. What is the difference? A. The principles-based approach has been effective, but […]

MET MG 95281

Which of the following should NOT be included in implementing performance evaluation systems? A. Feedback and review B. Fair and achievable measures C. Understandability D. Changing systems annually Answer: How is a foreign subsidiary different from a foreign branch of […]

MET MG 95438

According to legitimacy theory, corporate social reports: A. capture the impact of culture on the annual reports. B. is a means to deal with a firm’s exposure to political, economic, and social pressures. C. is in response to the stakeholders […]

SMG AC 22963

What is a “greenfield” investment? A. Farm land held for speculation B. Foreign direct investment whereby a new facility is constructed abroad C. Purchasing an existing facility as a foreign direct investment D. A foreign investment that has been approved […]

SMG AC 25416

Under IFRS 2, with respect to choice-of-settlement share-based payments, if the supplier chooses the cash settlement, the entity is deemed to have issued a compound financial instrument consisting of debt and equity. When cash is received, how does the supplier […]

SMG AC 64898

Under FASB ASC 830, Foreign Currency Matters, what group is responsible for determining the functional currency of a foreign subsidiary for many cases? A. Financial Accounting Standards Board B. International Accounting Standards Board C. Securities and Exchange Commission D. Parent […]