The balanced scorecard includes non-financial measures of performance with the

financial measures of performance traditionally used. Which of the following are

included in the balanced scorecard?

A. Customer satisfaction

B. Internal business processes

C. Innovation and learning

D. All of the above

Answer:

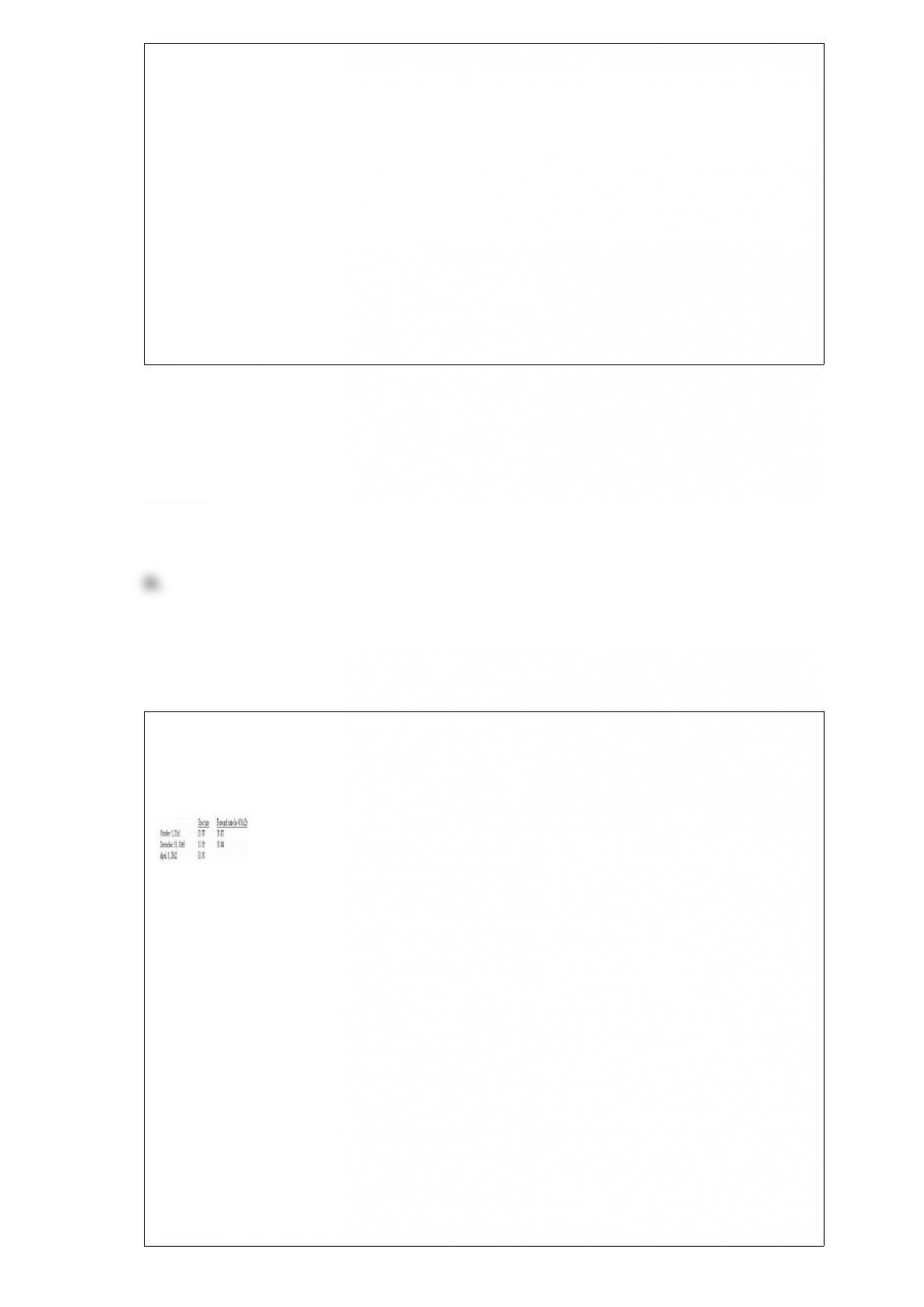

Amazing Corporation, a U.S. enterprise, sold product to a customer in Wales on

October 1, 20×1 for £100,000 with payment required on April 1, 20×2. Relevant

exchange rates are:

The discount factor corresponding to the company’s incremental borrowing rate for 6

months is 0.95.

Assume that Amazing Corporation enters a forward contract on October 1, 20×1 to sell

£100,000 six months hence, on April 1, 20×2. How should Amazing Corporation report

the forward contract on its December 31, 20×1 financial statements?

A. Asset $1,950

B. Liability $1,950

C. Asset $1,000

D. Asset $950

Answer:

How does U.S. GAAP differ from IFRS with respect to presenting consolidated

financial statements?

A. U.S. GAAP requires all controlled subsidiaries to be consolidated, whereas IFRS

allows for optional consolidated financial statements.

B. IFRS excludes subsidiaries acquired for disposal within one year from the

consolidation requirement, whereas U.S. GAAP requires all controlled subsidiaries to

be consolidated.

C. U.S. GAAP allows a company to exclude subsidiaries it is holding for sale from the

consolidation process.

D. IFRS requires the parent company to own 50% of the voting shares of the subsidiary

before consolidation is allowed.

Answer:

What measures may be used in the performance evaluation system of a multinational

corporation?

A. Financial measures such as profit, cost, and return on investment

B. Quality and customer satisfaction

C. Market share

D. All of the above

Answer:

British companies whose shares are publicly traded on exchanges in the United

Kingdom have how long after year-end to file financial statements with regulators in

the U.K.?

A. 6 months

B. 90 days

C. 60 days

D. 30 days

Answer:

What is a “foreign exchange rate?”

A. The price to buy a foreign currency

B. The price to buy foreign goods

C. The difference between the price of goods in a foreign currency and the price in a

domestic currency

D. The cost to hold all monetary assets in a single currency

Answer:

What does “multinationality” mean?

A. Geographical distribution of sales, assets, and employees of the company

B. The diversity of languages spoken at a company’s headquarters

C. The number of stock exchanges where a company’s shares are listed

D. None of the above

Answer:

Which of the following methods for translating foreign currency financial statements is

no longer allowed under U.S. GAAP?

A. Temporal method

B. Current/Noncurrent method

C. Current rate method

D. None of the above methods are allowed under GAAP.

Answer:

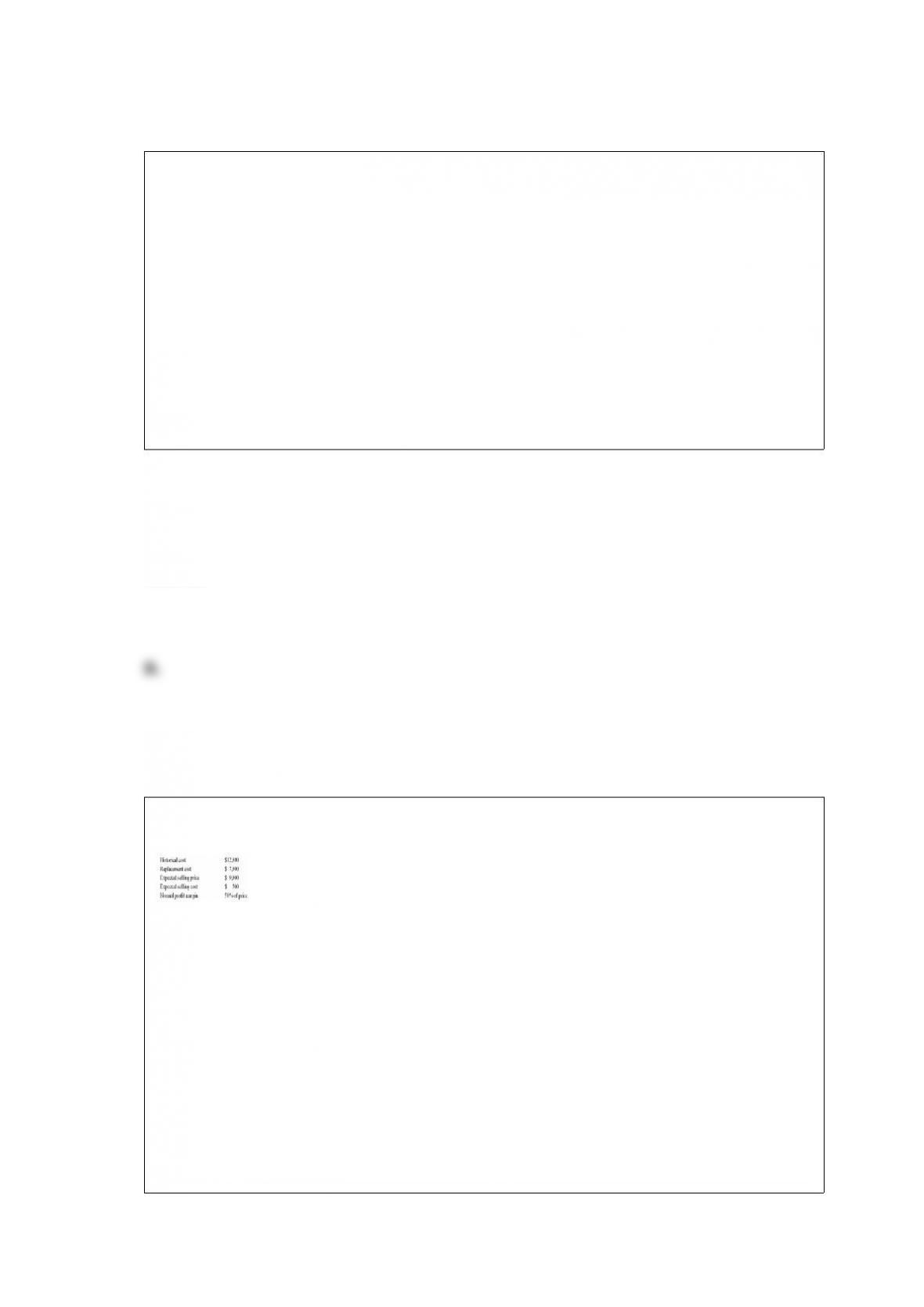

The following inventory information was taken from the records of Kleinfeld Inc.:

Under IAS 2, what should the balance sheet report for Inventory?

A. $7,000

B. $8,500

C. $7,600

D. $9,000

Answer:

What method of fixed asset valuation would most likely be used in countries that

regularly experience high rates of inflation?

A. Historical cost at subsequent balance sheet dates

B. Net realizable value at subsequent balance sheet dates

C. Fair value

D. Net present value at subsequent balance sheet dates

Answer:

Which of the following statements is true of nonlocal currency balances in the foreign

currency financial statements of foreign operations?

A. These are not reported in the consolidated financial statements.

B. Any gain is shown in the balance sheet of the company as an asset.

C. Any loss is reflected in the measurement of consolidated net income.

D. No gain or loss is reported in the financial statements.

Answer:

How does the principle of “joint and several liability” affect auditors in countries where

it is applied?

A. This limits civil liability to only those people who conducted the audit negligently.

B. All partners in the accounting firm can be personally liable for the negligence of any

one partner.

C. All audit partners are liable for the actions of the firm only up to the level of their

investment in the firm.

D. It creates limited liability for auditors accused of wrong-doing by their clients.

Answer:

Which of the following is a difference that exists between IFRS 8 and U.S. GAAP?

A. There are no differences as the two pronouncements represent total convergence in

segment reporting.

B. U.S. GAAP says that segment assets must be 5% or greater of the total combined

assets to be separately disclosed.

C. U.S. GAAP does not require reporting of segment liabilities.

D. U.S. GAAP explicitly includes intangibles in the definition of long-lived assets for

geographic disclosures.

Answer:

What is the primary focus of IAS 1?

A. To establish the guidelines for financial statement presentation

B. To provide guidance to first-time adopters of IFRS issued by the IASB

C. To establish the framework of guidelines to be used by IASB in setting accounting

standards

D. None of the above

Answer:

In 2011, the most popular location for inbound foreign direct investment (FDI) among

OECD countries was:

A. France.

B. China.

C. the United States.

D. Australia.

Answer:

Lack of information about accounting methods used, operating segments, and interim

financial results is a problem of:

A. disclosure.

B. relevance.

C. comparability.

D. format.

Answer:

What is EDGAR?

A. It is a database provided by the London, England stock exchange that provides

financial statement information on U.K. companies.

B. It is a database created by the U.S. Securities and Exchange Commission that

provides reports of all corporations listed on the U.S. stock exchanges.

C. It is a database of reports filed electronically with the U.S. Securities and Exchange

Commission.

D. It is a database that links users to U.S. company websites much like CAROL does in

the U.K.

Answer:

What is a foreign currency transaction?

A. It is another name for an international transaction.

B. It is a transaction that involves payment at a date sometime in the future.

C. It is a business deal denominated in a currency other than a company’s domestic

currency.

D. It is an economic event measured in a currency other than U.S. dollars.

Answer:

Under IAS 38, which of the following items is specifically EXCLUDED from being

recognized as an internally generated intangible asset?

A. Computer software costs

B. Copyrights

C. Customer lists

D. Motion picture films

Answer:

On December 1, 20×1 Pimlico made sales to a customer in India and recorded Accounts

Receivable of 10,000,000 rupees. The customer has until March 1, 20×2 to pay. On

December 1, 20×1, Pimlico paid $500 for a put option to sell rupees at a strike price of

$2.30 per 100 rupees on March 1, 20×2, which was the spot rate on December 1, 20×1.

On December 31, 20×1, the spot rate was $2.80 per 100 rupees and the option premium

was $0.004 per 100 rupees.

If the spot rate on March 1, 20×2 was $2.45 per 100 rupees, what is the foreign

currency exchange gain or loss that should be recorded that day?

A. $15,000 gain

B. $15,000 loss

C. $35,000 gain

D. $35,000 loss

Answer:

IFRS 8 adopts which approach to report segmented financial information?

A. Geographic approach

B. Business lines approach

C. Management approach

D. Asset test approach

Answer:

What is the term used to describe the possibility that a foreign currency will decrease in

U.S. dollar value over the life of an asset such as Accounts Receivable?

A. Foreign exchange translation

B. Foreign exchange risk

C. Hedging

D. Foreign currency options

Answer:

What is the primary problem with using discretionary transfer prices to minimize costs

in a decentralized organization?

A. They don’t really minimize tax costs.

B. The appropriate transfer price to minimize costs cannot be determined by the parent

company.

C. The benefits of decentralization may be lost.

D. They are extremely difficult to administer.

Answer:

What is meant by the “translation” of foreign currency financial statements?

A. Converting financial statements prepared under foreign GAAP into domestic GAAP

B. Converting financial statements of a foreign currency into a domestic currency

C. Converting the language used in financial statements from foreign to domestic

D. Converting historic cost financial statements into current cost financial statements

Answer:

Which of the following is likely to affect an analyst’s ability to make meaningful

comparisons of financial statement ratios for companies in different countries?

A. Accounting diversity

B. Varying business traditions

C. Unique terminology

D. All of the above

Answer:

Alpha Inc. has receivables from unrelated parties with a face value of $5,000.

It transfers these receivables to bank for $4,500, without recourse. It will continue to

collect the receivables, depositing them in a non-interest-bearing bank account with the

cash flows remitted to the bank at the end of each month. It is not allowed to sell or

pledge the receivables to anyone else and is under no obligation to repurchase the

receivables from bank. Which of the following is the appropriate treatment for these

Accounts receivables?

A. It should show these receivables in its Balance Sheet.

B. It should amortize these receivables.

C. It should derecognize these receivables.

D. It should derecognize these receivables if it retains the interest earned on these.

Answer:

The nine categories of foreign source income defined by the Tax Reform Act of 1986

are referred to as:

A. FTC rates.

B. FTC credits.

C. FTC baskets.

D. FTC brackets.

Answer:

What is the paradox of hedging balance sheet exposure?

A. Real costs can be incurred to hedge an unrealized translation adjustment.

B. The hedging process rarely works the way management intended.

C. Hedging is a conceptual process that is nearly impossible to undertake in the real

world.

D. Markets have yet to be developed that offer the kinds of derivative instruments

required for hedging.

Answer:

In Gray’s framework for accounting system development, which of the following

countries tends to show a relatively high preference for conservative accounting

standards?

A. Norway

B. United Kingdom

C. United States of America

D. Japan

Answer:

Which of the following statements is NOT true concerning reasons for analyzing

foreign financial statements?

A. It is important to determine the financial stability of foreign suppliers.

B. The stock returns of foreign corporations are nearly perfectly correlated with returns

on U.S. stocks.

C. In a global economy, managers may use foreign competitors as benchmarks for

evaluating performance.

D. Managers should determine the financial health of foreign customers before

extending credit.

Answer:

Differences in business traditions and practices could make cross-country ratio analysis

difficult. What should an analyst do to overcome this problem?

A. Learn more about the business environment in relevant countries.

B. Make all decisions using nominal monetary differences rather than ratios.

C. Translate all ratios to a common currency.

D. Avoid recommending investments in foreign companies.

Answer:

In addition to regulating the transfer prices on tangible property, the Internal Revenue

Service also provides guidance on:

A. interest charged on intercompany loans.

B. transfer prices for intangible property.

C. charges for intercompany services.

D. All of the above

Answer:

From a practical standpoint, what is the goal of accounting standards harmonization?

A. Creating one set of standards used throughout the world

B. Reducing the conflict among national accounting standards

C. Producing accounting standards that are unique for each country

D. Forcing compliance with IASB regulations

Answer:

Which term refers to an affiliate relationship between an accounting/auditing firm and

its sponsoring organization?

A. Parent/subsidiary

B. Hooking up

C. Guanxi

D. Principal/Agent

Answer:

The exchange gain or loss on repatriated funds from a foreign branch is calculated by

multiplying the nominal amount of the funds by:

A. the difference between the exchange rate at the beginning of the year and the

exchange rate at the end of the year.

B. the difference between the exchange rate on the date of repatriation and the

exchange rate used to translate the branch’s pretax income.

C. the difference between the current exchange rate and the exchange rate at the end of

the year.

D. the difference between the exchange rate on the date of repatriation and the

exchange rate at the beginning of the year.

Answer: