Chapter 10 – Analysis of Foreign Financial Statements

11. Vale S.A. (Statement of Added Value)

a. The external parties who might be most interested in Vale’s Statement of Added Value

b. Personnel; Taxes, rates and contribution less Taxes paid recover; and Remuneration on

c. Perhaps the most important story being told is the manner in which added value (AV) is

12. Babcock International Group PLC (Determine Gross Profit and Estimate Sustainable

Income)

a. Determine gross profit and gross profit margin

Note 4, Operating expenses, indicates that “Cost of sales” in 2009 was £1,685.1. Gross

profit and gross profit margin are calculated as follows:

2009

Revenue 1,901.9

b. Estimate sustainable income

Babcock reports profit for the year 2009 of £74.3, but this includes several items that are

non-recurring (and therefore not part of sustainable income) and are given special

presentation in the income statement.

10-1

Education.

Chapter 10 – Analysis of Foreign Financial Statements

Based on the presentation of the income statement and the information provided in Note

6, the following would be a reasonable estimate of sustainable income for 2009:

13. Vale S.A. (EBITDA)

a. EBITDA is a measure of the amount of income a company generates before subtracting

b. One explanation for why Vale included Note 11 in its 2009 annual report is that the

c. EBITDA can be useful in comparing the performance of companies located in different

d. The obvious limitation in using EBITDA to evaluate a company’s performance is that by

14. Arcot Company (Restatement of financial statements – Year 1)

Reconciling Entries

[1] Inventory indirect costs

[2] Revaluation of property, plant, and equipment

10-2

Education.

Chapter 10 – Analysis of Foreign Financial Statements

[3] Capitalized interest

14. (continued)

Worksheet for Restatement of Income and Retained Earnings to U.S. GAAP

For the year ended December 31, Year 1

(1) (2) (3) (4)

Reconciling

Adjustments

(millions of Crowns) Local GAAP Debit Credit U.S. GAAP

Sales 7,952 30 [6] 7,922

10-3

Education.

Chapter 10 – Analysis of Foreign Financial Statements

Retained earnings, December 31 2,043 2,086

Ratio Local GAAP U.S. GAAP

Current ratio 2.63 2.65

Total asset turnover 0.43 0.43

10-4

Education.

Chapter 10 – Analysis of Foreign Financial Statements

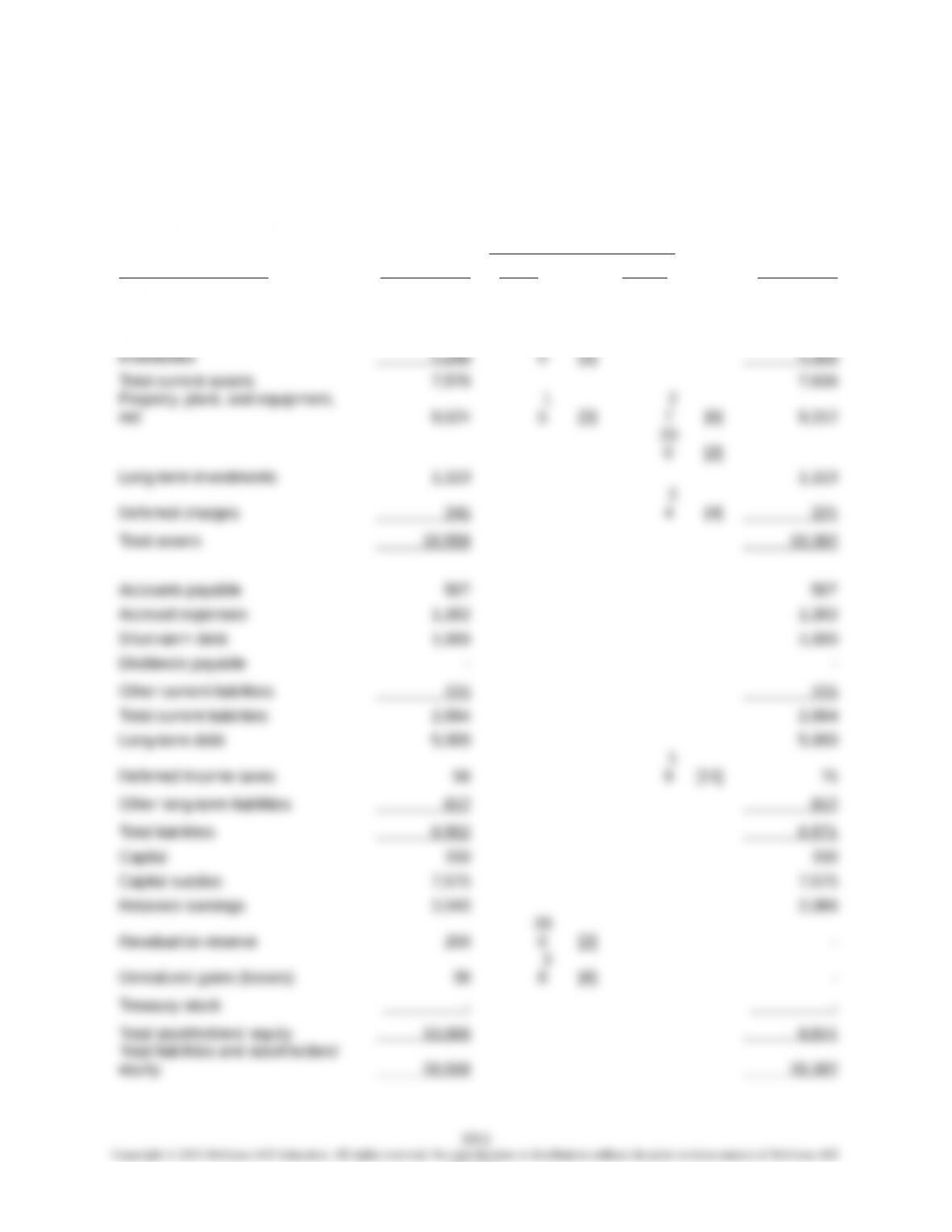

14. (continued)

Worksheet for Restatement of Balance Sheet to U.S. GAAP for the year ended

December 31, Year 1

(1) (2) (3) (4)

Reconciling Adjustments

(millions of Crowns) Local GAAP Debit Credit U.S. GAAP

Cash 1,272 1,272

Accounts receivable 2,064 2,064

6

Education.

Chapter 10 – Analysis of Foreign Financial Statements

15. Arcot Company (Restatement of financial statements – Year 2)

Reconciling Entries

[1] Inventory indirect costs

Dr. Cost of goods sold 41

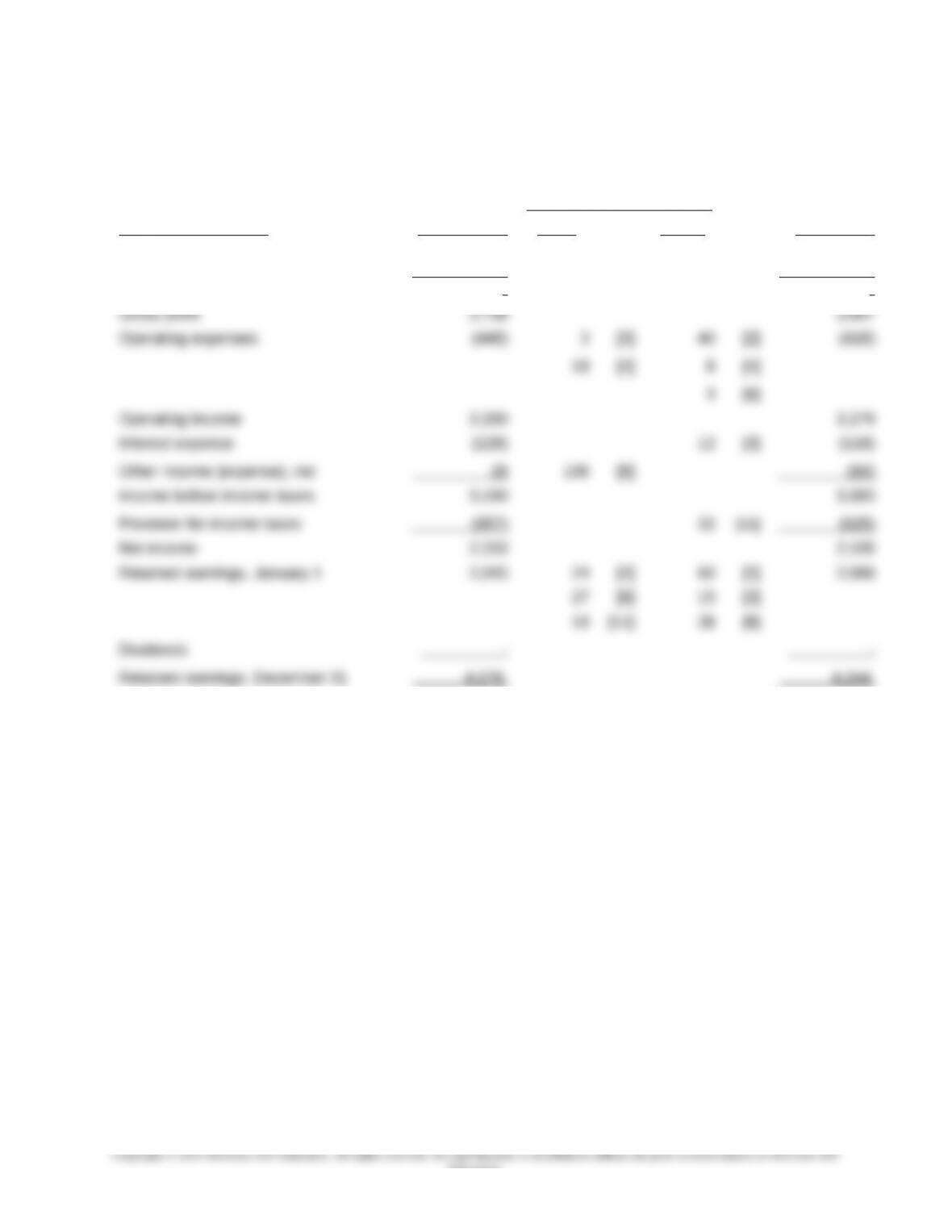

15. (continued)

Worksheet for Restatement of Income and Retained Earnings to U.S. GAAP

10-6

Education.

Chapter 10 – Analysis of Foreign Financial Statements

For the year ended December 31, Year 2

(1) (2) (3) (4)

Reconciling Adjustments

(millions of Crowns) Local GAAP Debit Credit U.S. GAAP

Sales 8,348 8,348

Cost of goods sold

(4,610

)

4

1 [1]

(4,651

)

10-7

Education.