Chapter 08 – Translation of Foreign Currency Financial Statements

Answers to Questions

1. The two major issues related to the translation of foreign currency financial statements are:

2. Balance sheet exposure arises when a foreign currency balance is translated at the current

3. The major concept underlying the current rate method is that the entire foreign investment

is exposed to foreign exchange risk. Therefore all assets and liabilities are translated at

the current exchange rate. Balance sheet exposure under this concept is equal to the net

investment.

4. The major differences relate to non-monetary assets carried at historical cost and related

5. To determine the appropriate translation method under both IFRS and U.S. GAAP, the

functional currency of a foreign subsidiary must be identified. The functional currency is

6. For foreign entities that report in the currency of a hyperinflationary economy, IAS 21

requires the parent first to restate the foreign financial statements for inflation using IAS 29

8-1

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

7. The functional currency is the currency of the subsidiary’s primary economic environment.

It is usually identified as the currency in which the company generates and expends cash.

U.S. GAAP stipulates that several factors such as the location of primary sales markets,

sources of materials and labor, the source of financing, and the amount of intercompany

8. U.S. GAAP requires use of the temporal method for operations in highly inflationary

countries. Use of the current rate method without first restating for inflation results in a

9. Although balance sheet exposure does not result in cash inflows and outflows, it does

nevertheless affect amounts reported in consolidated financial statements. If the foreign

10. The gains and losses arising from financial instruments used to hedge balance sheet

exposure are treated in a similar manner as the item the hedge is intended to cover. If the

Solutions to Exercises and Problems

8-2

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

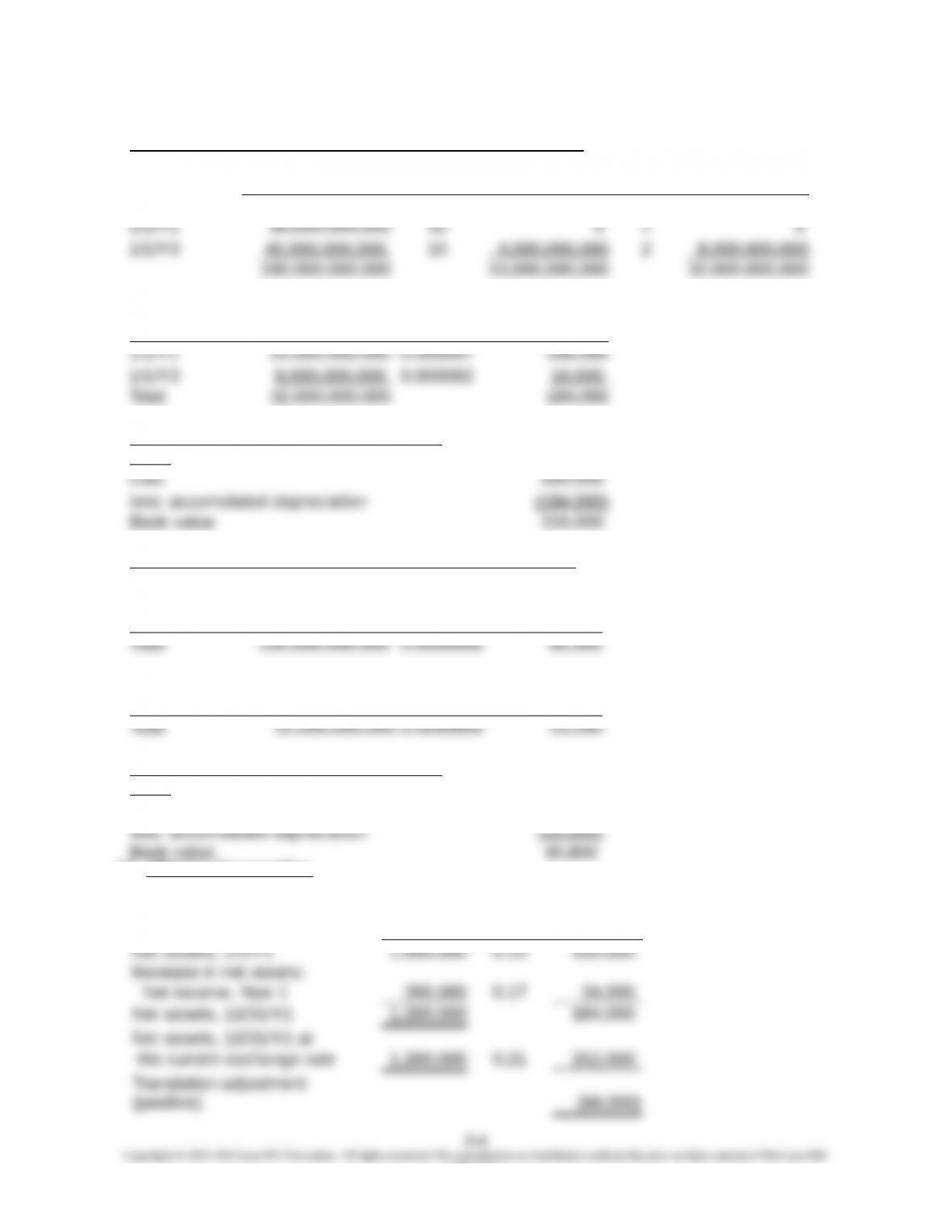

9. Armetis Corporation

a. Current Rate Method

Exchange

BRL Rate CAD

b. Temporal Method

Exchange

BRL Rate CAD

10. Simga Company

a. Highly inflationary economy (Temporal method)

Exchange

Equipment TL Rate USD

8-3

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

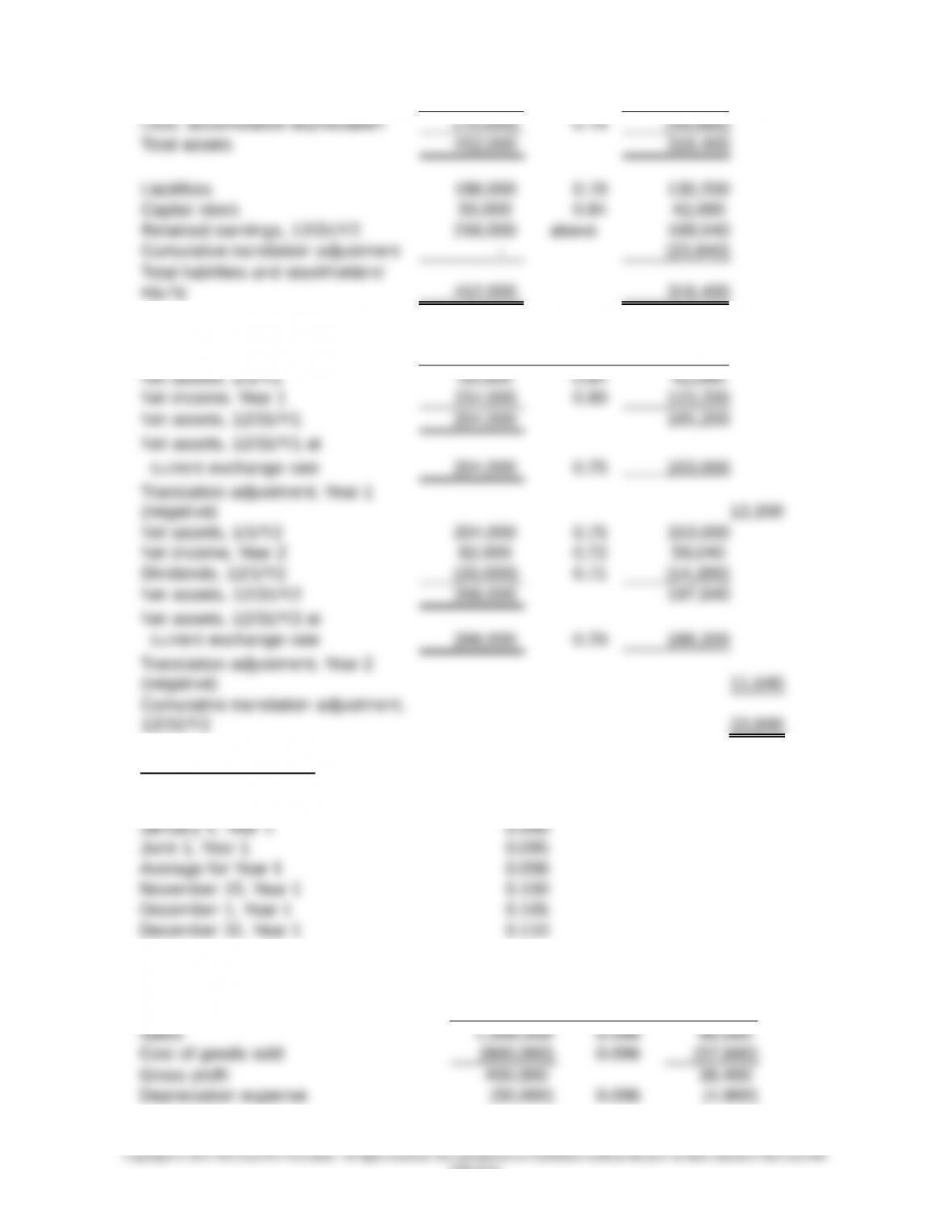

Determination of Accumulated Depreciation at 12/31/Y4

Useful Life Annual Age Accumulated

Cost in years Depreciation in years Depreciation

6,000,000,00

24,000,000,00

Accumulated Exchange

Depreciation TL Rate USD

Book value of equipment, 12/31/Y4 (in

USD)

b. Non-highly inflationary economy (Current rate method)

Exchange

Equipment TL Rate USD

Accumulated Exchange

Depreciation TL Rate USD

Book value of equipment, 12/31/Y4 (in

USD)

Cost 60,000

11. Alliance Corporation

Exchange

Marks Rate A$

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

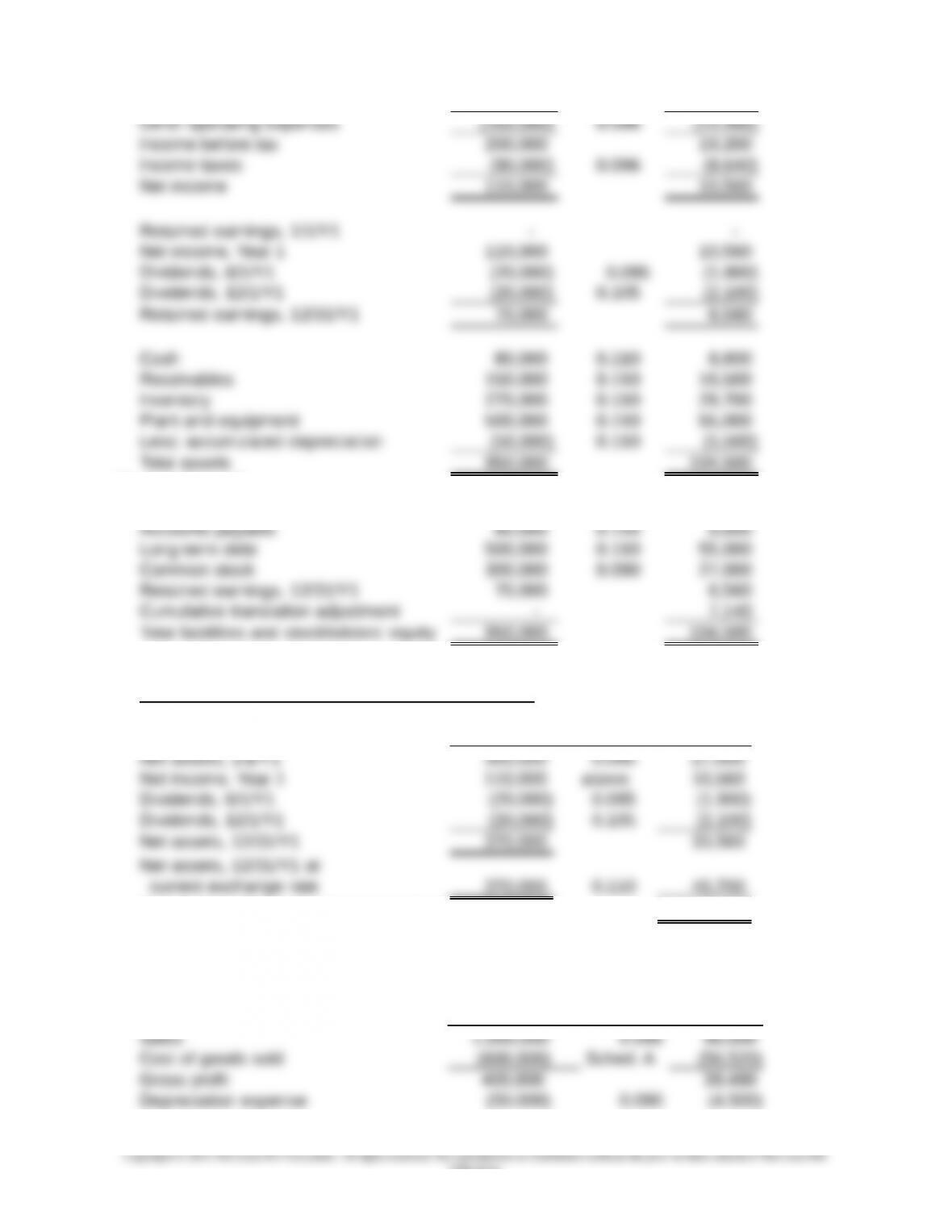

12. Zesto Company

Pesos US$

13. Alexander Corporation

a. Swiss franc is functional currency (Current rate method)

Swiss Exchange U.S.

Francs Rate Dollars

b. U.S. dollar is functional currency (Temporal method)

Swiss Exchange U.S.

Francs Rate Dollars

Economic Relevance of Translation Adjustment

The translation adjustment increases stockholders’ equity by $410,000. The positive

translation adjustment arises because the Swiss subsidiary has a net asset position

8-5

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

Economic Relevance of Remeasurement Loss

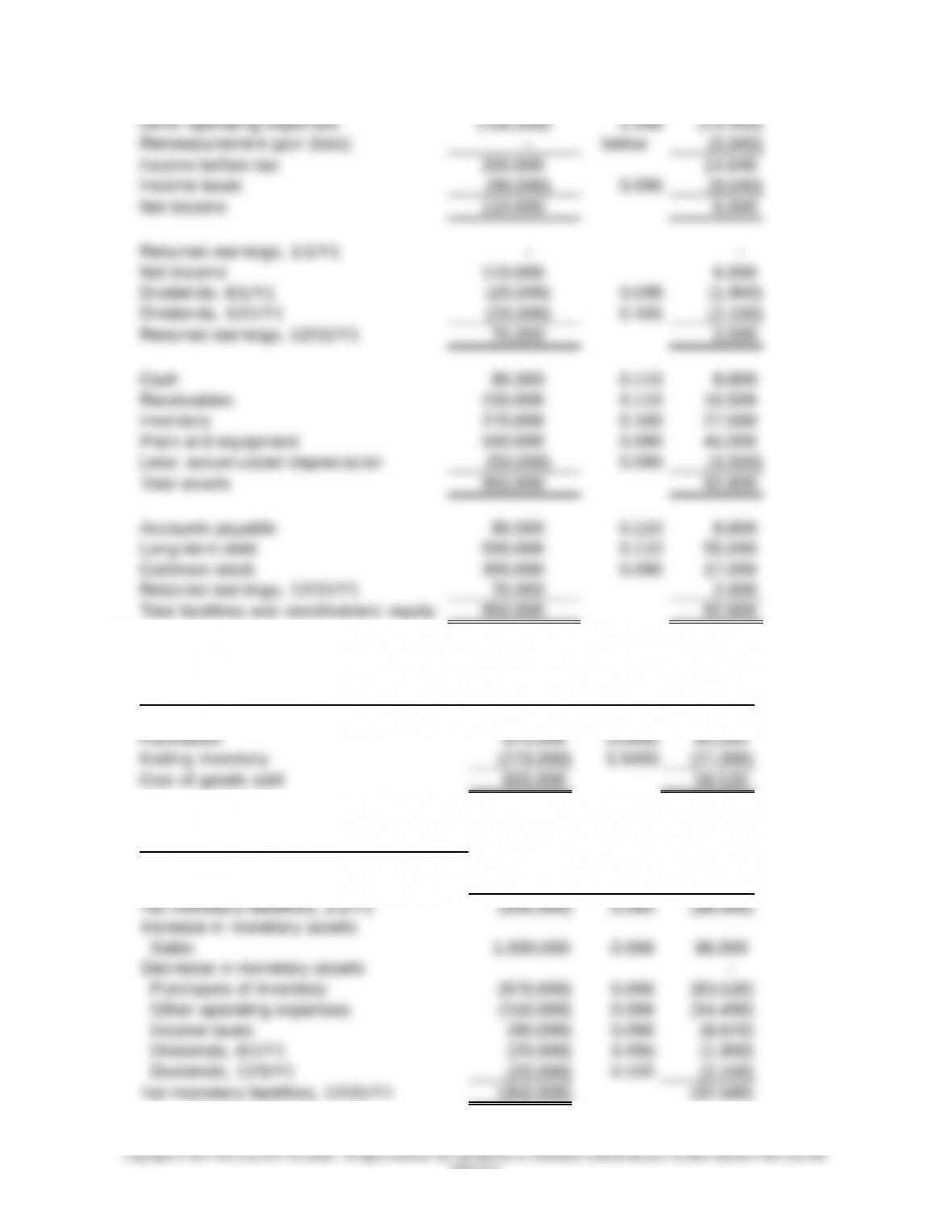

14. Gramado Company

Exchange Rates $/Cz

Exchange

Cz Rate $

388,80

14. (continued)

Exchange

Cz Rate $

8-6

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

Exchange

Cz Rate $

15. Brookhurst Company

Exchange Rates USD/ZAR

a. South African rand is functional currency (Current rate method)

Exchange

ZAR Rate USD

8-7

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

15. (continued)

Calculation of cumulative translation adjustment

Exchange

ZAR Rate USD

Translation adjustment, Year 1 (positive) (7,140)

15. (continued)

b. U.S. dollar is functional currency (Temporal method)

Exchange

ZAR Rate USD

8-8

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

15. (continued)

Schedule A. Exchange

Calculation of cost of goods sold ZAR Rate USD

Beginning inventory – –

Calculation of remeasurement gain

(loss)

Exchange

ZAR Rate USD

8-9

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

16. The solutions to this problem will depend upon the U.S.-based MNC selected by each

17. This problem requires students to examine disclosures made by ExxonMobil and

(a) In its 2012 Form 10-K, ExxonMobil disclosed the following in its Summary of Accounting

Policies: “The Corporation selects the functional reporting currency for its international

subsidiaries based on the currency of the primary economic environment in which each

(b) In 2012, ExxonMobil reported translation adjustments (in other comprehensive income) of

(c) In 2012, neither company mentioned hedges of net investment in foreign operations.

ExxonMobil indicated that it makes limited use of derivatives, with no further description.

Case 8-1 Columbia Corporation

8-10

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

Part I

Exchange Rates $/PLN

January 1, Year 1 0.25

8-11

Education.