Chapter 12 – International Transfer Pricing

Answers to Questions

1. Transfer prices must be determined for the following intercompany transfers:

2. Cost minimization objectives that companies might wish to achieve through transfer pricing

include:

3. The performance evaluation objective of transfer pricing refers to the use of intercompany

4. To achieve a specific cost minimization objective, headquarters management might need to

5. Withholding taxes are paid to a foreign government by a foreign subsidiary when it pays

dividends (or interest or royalties) to its parent located in another country. In contrast,

6. The five methods acceptable under U.S. tax regulations for determining an arm’s length

price for the sale of tangible property are:

7. The “arm’s length range” of transfer prices refers to the fact that the application of a single

method could result in a range of transfer prices that are equally reliable. No adjustment will

be made by the IRS if the transfer price falls within this range.

12-1

Education.

Chapter 12 – International Transfer Pricing

8. An international transfer price determines the amount of income taxable in the country of

9. An “advance pricing agreement” is an agreement between a company and a national tax

10. The major benefit to a company from entering into an advance pricing agreement is the

Solutions to Exercises and Problems

13. Lahdekorpi OY

a. The best transfer pricing method in this case is the comparable uncontrolled price

12-2

Education.

Chapter 12 – International Transfer Pricing

b. The best transfer pricing method in this scenario is the resale price method. Lahdekorpi

c. The best transfer pricing method in this case is the cost plus method. An acceptable

14. Superior Brakes

Superior Brakes sells directly to truck manufacturers in the United States, and to its 100%-

owned sales subsidiary in Brazil. The Brazilian sales subsidiary sells directly to Brazilian

truck makers. Superior Brakes does not sell to unaffiliated distributors in Brazil so there is

15. Akku Company

a. $1.50 transfer price b. $1.80 transfer price

Germany U.S Total Germany U.S Total

Sales price $1.50 $4.50 $4.50 $1.80 $4.50 $4.50

12-3

Education.

Chapter 12 – International Transfer Pricing

c. The lower transfer price ($1.50 vs. $1.80) results in the smaller amount of total income

16. Smith-Jones Company

a. (1) The reliability of the comparable uncontrolled price method is reduced by the fact

that Smith-Jones is a retailer of Joal handbags in the United States, whereas Joal’s

(2) The reliability of the resale price method is reduced by the fact that other U.S.

(3) The reliability of the cost plus method suffers from the fact that there are no other

b. The resale price method might be the best of the three methods because the

17. Guari Company

a. Computation of the total amount of income taxes and import duty paid on each

bicycle:

1. Before transfer pricing adjustment

Taiwan Australia

2. After transfer pricing adjustment; with correlative adjustment:

Taiwan Australia

12-4

Education.

Chapter 12 – International Transfer Pricing

3. After transfer pricing adjustment; without correlative adjustment

Taiwan Australia

17. (continued)

b. The company obtains very little benefit (A$0.92 per bicycle) from establishing the

transfer price for sales from its Taiwanese subsidiary to Guari at a price higher than it

c. Whether the Taiwanese tax authority will grant a correlative adjustment might depend on

18. ABC Company

Sale from X to Y. Strategy: transfer at a relatively high price.

Low price: $10.00 High price: $13.00

X Y Total X Y Total

12-5

Education.

Chapter 12 – International Transfer Pricing

18. (continued)

Sale from X to Z. Strategy: transfer at a relatively high price.

Low price: $10.00 High price: $13.00

X Z Total X Z Total

Sale from Y to X. Strategy: transfer at a relatively low price.

Low price: $10.00 High price: $13.00

Y X Total Y X Total

Sale from Y to Z. Strategy: transfer at a relatively high price.

Low price: $10.00 High price: $13.00

Y Z Total Y Z Total

Education.

Chapter 12 – International Transfer Pricing

2.00 1.70

18. (continued)

Sale from Z to X. Strategy: transfer at a relatively low price.

Low price: $10.00 High price: $13.00

Z X Total Z X Total

Sale from Z to Y. Strategy: transfer at a relatively low price.

Low price: $10.00 High price: $13.00

Z Y Total Z Y Total

Sale 10.00 15.00 Sale 13.00 15.00

Summary of strategy: X should always transfer at a high price; Z should always transfer at

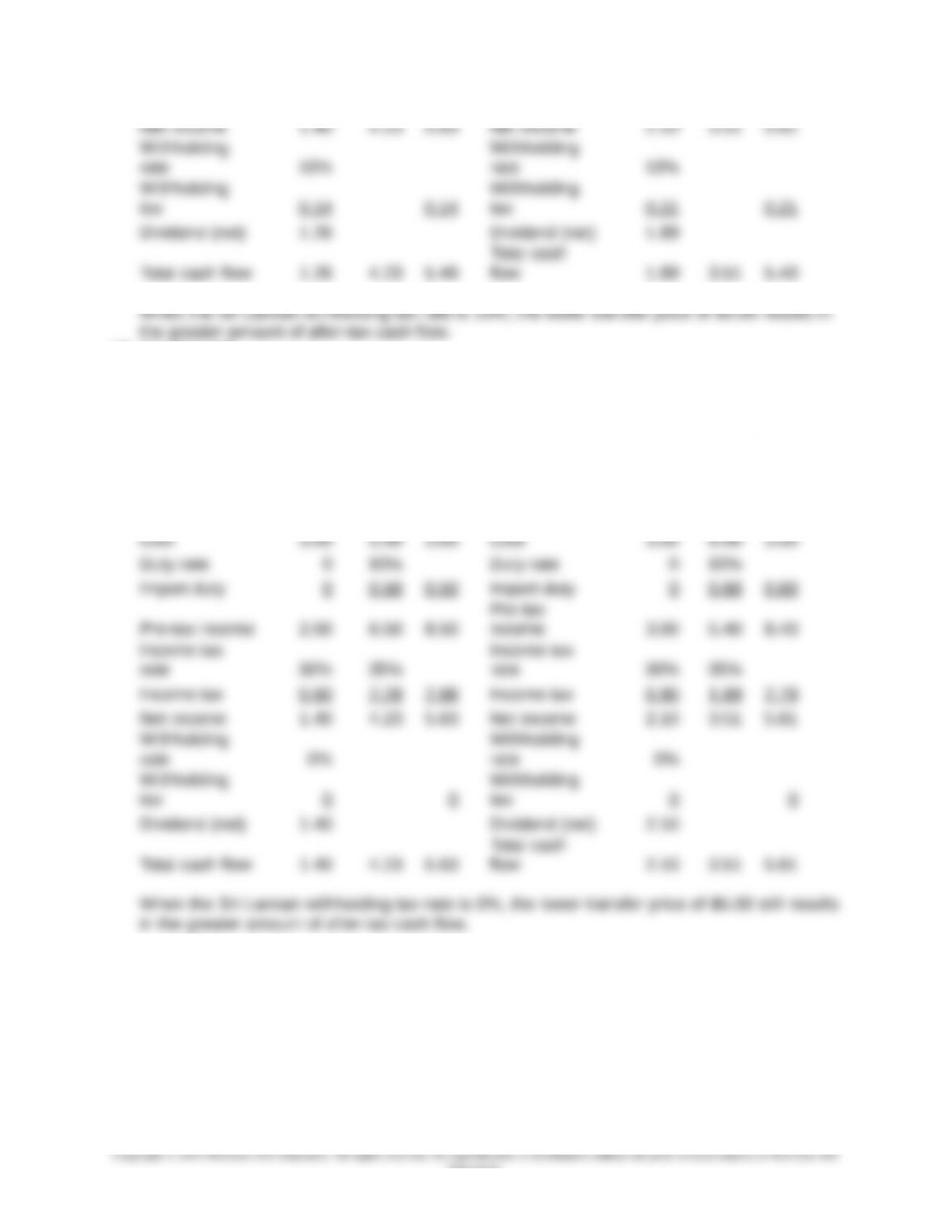

19. Denker Corporation

a. The only possible transfer prices that will maximize Denker’s after tax cash flow are the

two extremes in the arm’s length range — $5 or $6.

Transfer price = $5.00 Transfer price = $6.00

Sri

Lanka Denker Total

Sri

Lanka Denker Total

Education.

Chapter 12 – International Transfer Pricing

19. (continued)

b. The only possible transfer prices that will maximize Denker’s after tax cash flow are the

two extremes in the arm’s length range — $5 or $6.

Transfer price = $5.00 Transfer price = $6.00

Sri

Lanka Denker Total

Sri

Lanka Denker Total

Sales price 5.00 12.00 12.00 Sales price 6.00 12.00 12.00

20. Ranger Company

Yery’s operating income, excluding royalties, is $200,000 ($800,000 – $600,000). Under the

residual profit split method, the amount of Yery’s operating income attributable to Yery’s

operating assets is first determined. This amount is $60,000 ($300,000 operating assets x

20% return on operating assets). Therefore, $140,000 of Yery’s operating income is

attributable to intangibles. The next step is to determine how much of this amount is

12-8

Education.

Chapter 12 – International Transfer Pricing

Case 12-1 Litchfield Corporation

The memo to Sarah Litchfield should include the following points:

Section 482 of the U.S. Internal Revenue Code gives the Internal Revenue Service (IRS)

the authority to adjust any intercompany transfer prices that it determines are not at

arm’s length. This would include sales from Litchfield Corp. to its U.K. subsidiary.

12-9

Education.