Chapter 08 – Translation of Foreign Currency Financial Statements

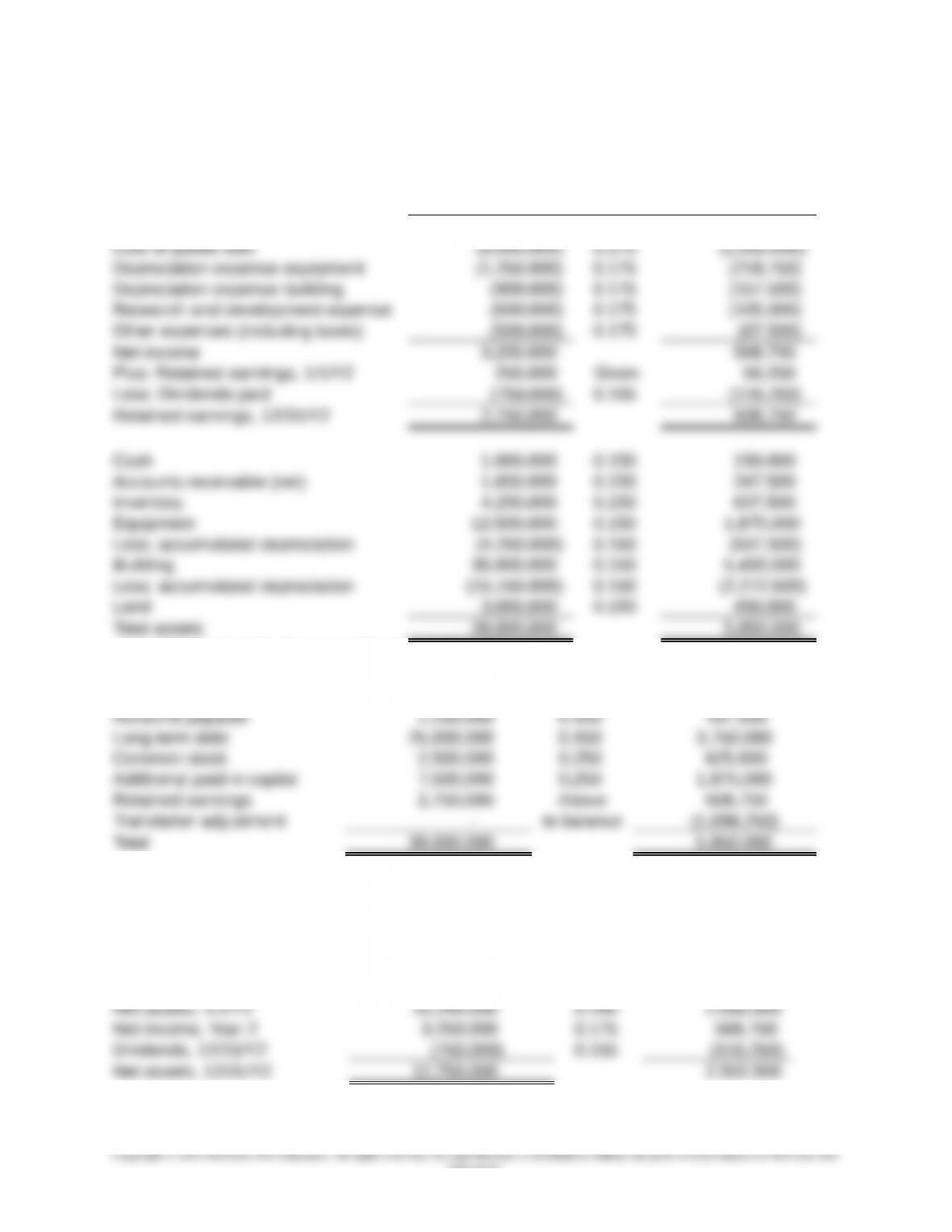

Part I (a). Polish zloty is the functional currency – Current rate method

Exchange

PLN Rate U.S. $

Sales 12,500,000 0.175 2,187,500

Case 8-1 Columbia Corporation (continued)

Calculation of Cumulative Translation Adjustment

Exchange

PLN Rate U.S. $

8-1

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

Case 8-1 Columbia Corporation (continued)

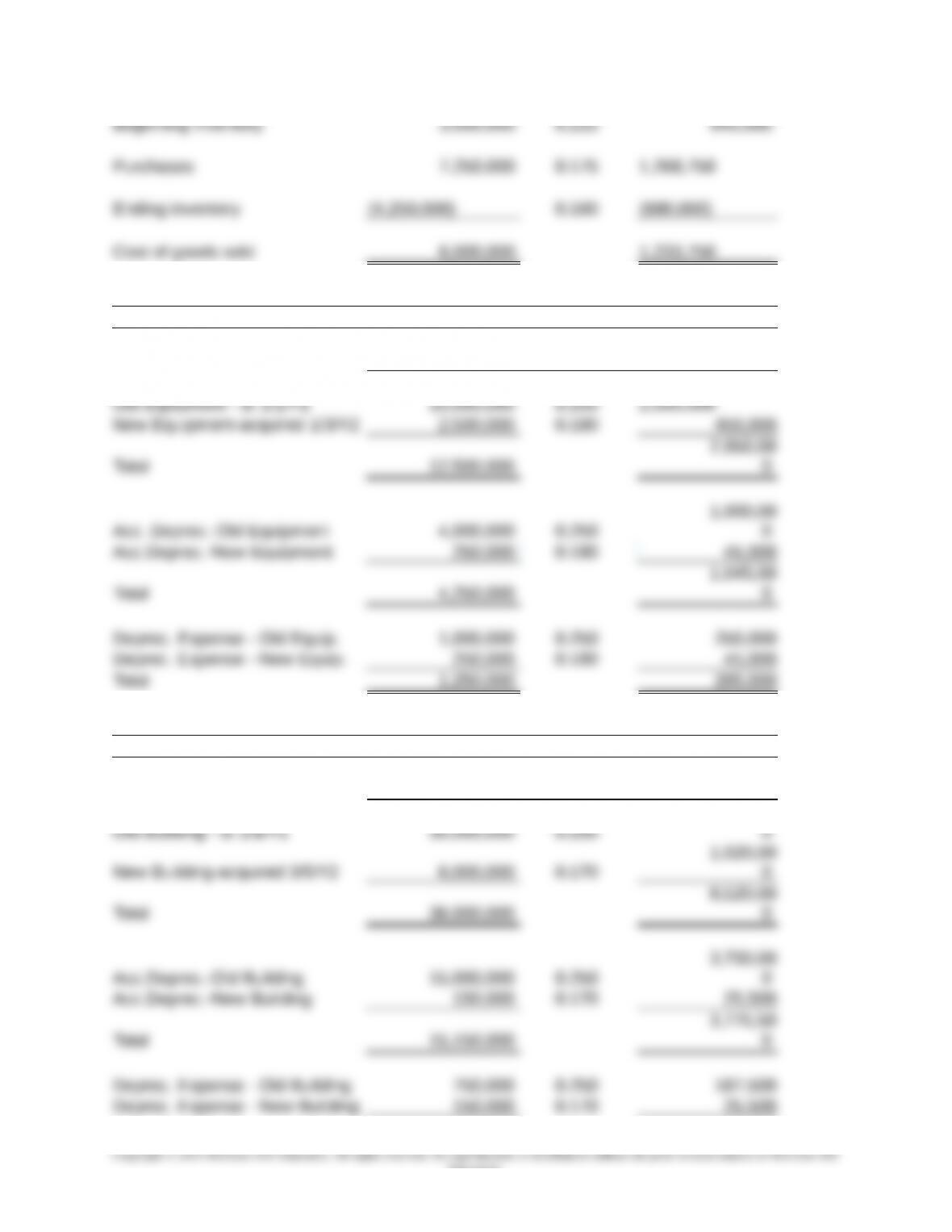

Part I (b). U.S. dollar is the functional currency – Temporal method

Exchange

PLN Rate U.S. $

Case 8-1 Columbia Corporation (continued)

Schedule A – Cost of goods

sold

Exchange

PLN Rate U.S. $

8-2

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

Schedule B – Equipment

Exchange

PLN Rate U.S. $

Schedule C – Building

Exchange

PLN Rate U.S. $

7,500,00

8-3

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

Case 8-1 Columbia Corporation (continued)

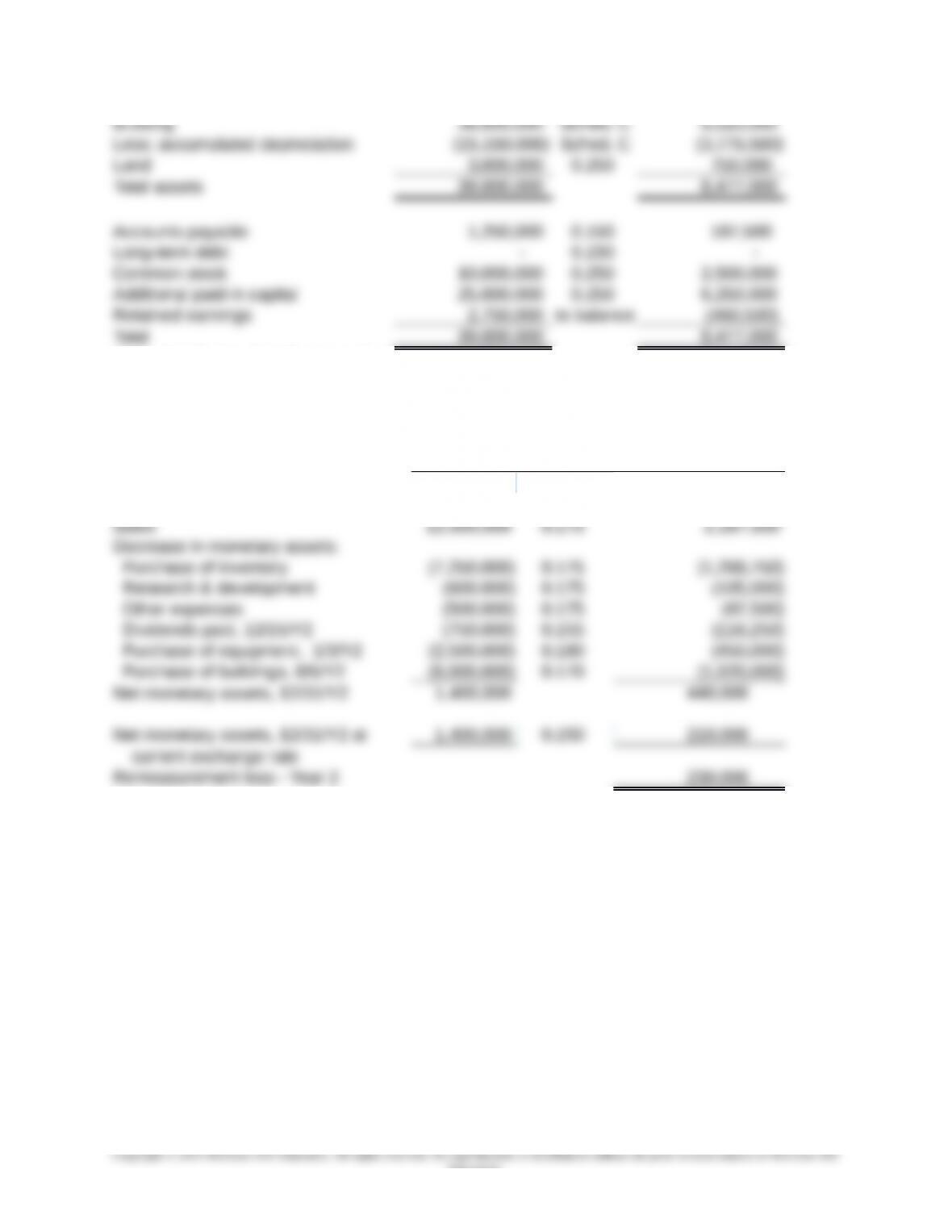

Calculation of Remeasurement Gain

Exchange

PLN Rate U.S. $

Case 8-1 Columbia Corporation (continued)

Part I (c). U.S. dollar is the functional currency – Temporal method (no long-term debt)

Exchange

PLN Rate U.S. $

8-4

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

Case 8-1 Columbia Corporation (continued)

Calculation of Remeasurement Loss

Exchange

PLN Rate U.S. $

Net monetary assets, 1/1/Y2 6,500,000 0.200 1,300,000

Increase in monetary assets:

Part II. Explain the negative translation adjustment in Part I (a) and remeasurement gain

or loss in Parts 1(b) and 1(c).

The negative translation adjustment in part 1(a) arises because of two factors: (1) there is a net

asset balance sheet exposure and (2) the Polish zloty has depreciated against the U.S. dollar

during Year 2 (from $.020 at 1/1/Y2 to $.0150 at 12/31/Y2). A net asset balance sheet exposure

exists because all assets are translated at the current exchange rate and exceeds total liabilities

which are also translated at the current exchange rate.

The remeasurement gain in part I(b) arises because of two factors: (1) there is a net liability

balance sheet exposure and (2) the Polish zloty has depreciated against the U.S. dollar. Under

the temporal method, Cash and Accounts Receivable are the only assets translated at the

current exchange rate (total PLN 2,650,000). Accounts Payable and Long-Term Debt also are

translated at the current exchange rate (total PLN 26,250,000). Because the Polish zloty

amount of liabilities translated at the current rate exceeds the Polish zloty amount of assets

8-5

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

translated at the current rate, a net liability balance sheet exposure exists.

The remeasurement loss in part I(c) arises because of two factors: (1) there is a net asset

balance sheet exposure and (2) the Polish zloty has depreciated against the U.S. dollar during

Year 2.

Cash and Accounts Receivable are the only assets translated at the current exchange rate (total

PLN 2,650,000). Because there is no Long-term Debt in part 1(c), Accounts Payable is the only

liability translated at the current exchange rate (total PLN 1,250,000). Because the Polish zloty

amount of the assets translated at the current rate exceeds the Polish zloty amount of liabilities

translated at the current rate, a net asset balance sheet exposure exists.

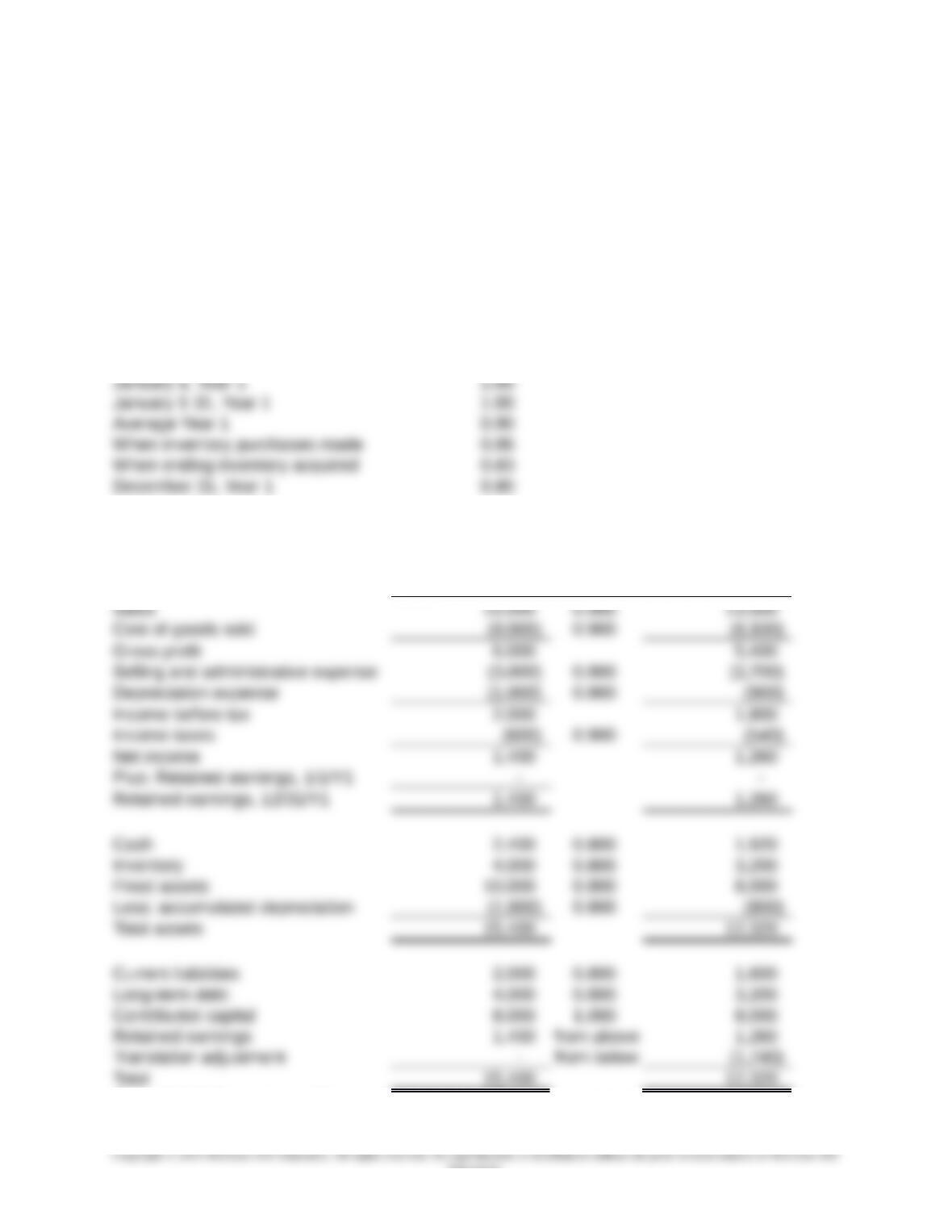

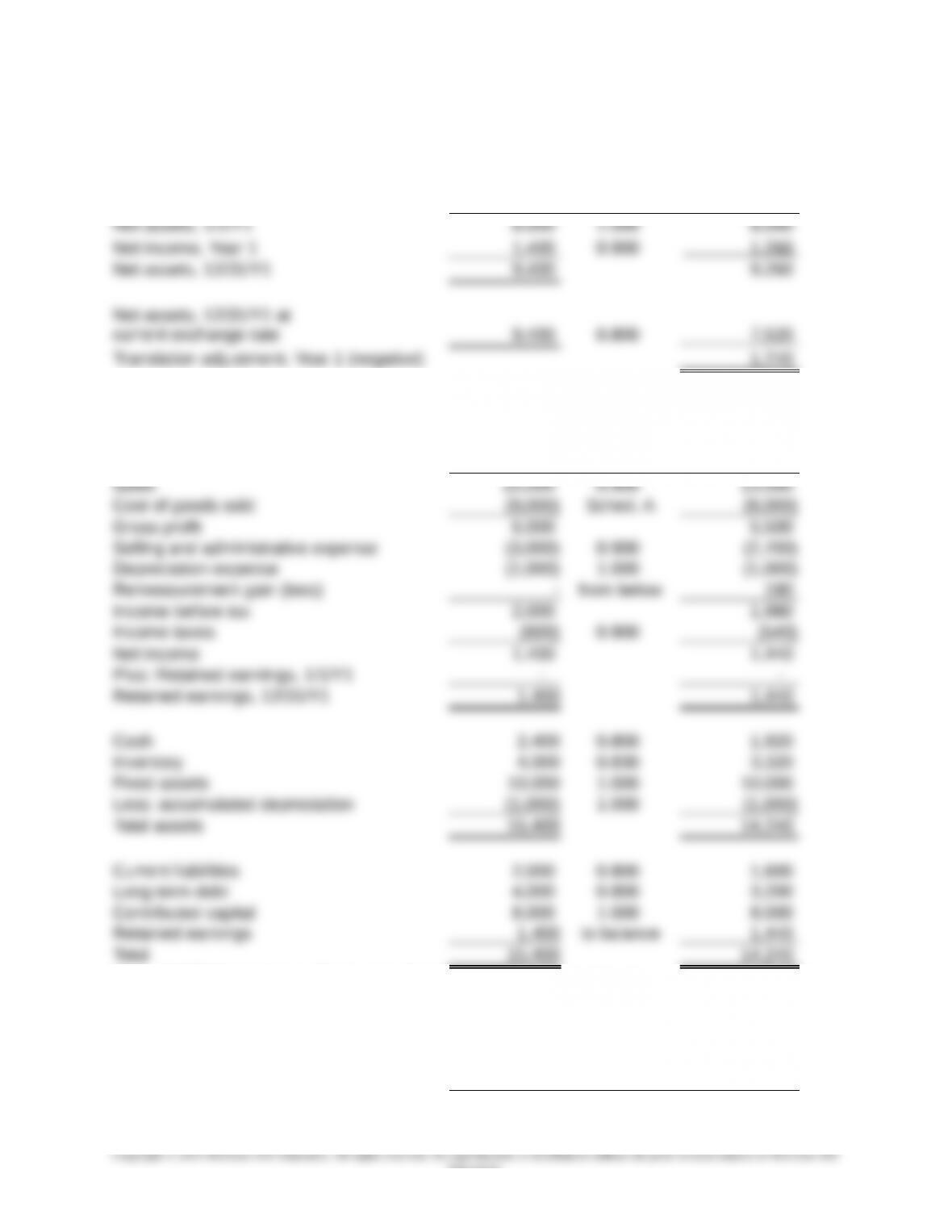

Case 8-2 Palmerstown Company

Exchange Rates $/pound

1. Pound is the functional currency – Current rate method

Exchange

Pounds Rate U.S. $

Case 8-2 Palmerstown Company (continued)

8-6

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

Calculation of Cumulative Translation Adjustment

Exchange

Pounds Rate U.S. $

2. U.S. dollar is the functional currency – Temporal method

Exchange

Pounds Rate U.S. $

Case 8-2 Palmerstown Company (continued)

Schedule A – Cost of goods sold

Exchange

Pounds Rate U.S. $

Purchase, January 10 1,000 1.000 1,000

8-7

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

Calculation of Remeasurement Gain

Exchange

Pounds Rate U.S. $

Net monetary assets, 1/1/Y1 8,000 1.000 8,000

Increase in monetary assets:

3. With the pound as functional currency, the U.S. dollar net income reflected in the

consolidated income statement is $1,260. If the U.S. dollar were the functional currency, the

amount reflected in consolidated net income would be $1,560, 24% higher. The amount of

total assets reported on the consolidated balance sheet is 17% smaller than if the U.S.

dollar were functional currency [($14,360 – $12,320)/$12,320].

The relations between the current ratio, the debt to equity ratio, and profit margin calculated

from the FC financial statements and from the translated U.S. dollar financial statements are

shown below. Case 8-2 Palmerstown Company (continued)

U.S. $ U.S $

Pounds Current Rate Temporal

Current ratio:

Profit margin:

8-8

Education.

Chapter 08 – Translation of Foreign Currency Financial Statements

Net income 1,400 1,260 1,440

Sales 15,000 13,500 13,500

0.093 0.093 0.107

8-9

Education.