Blanco Chemical Company spent €15,000,000 in development efforts to create a

fertilizer for which it was able to obtain a patent; however, the expected distribution

costs make it infeasible to market the chemical in the foreseeable future. According to

IAS 38 (Intangible Assets), how should Blanco Chemical Company record the

€15,000,000?

A. As a “Deferred Development Cost” on the Balance Sheet

B. As “Fertilizer Revenue” on the Income Statement

C. As “Development Expense” on the Income Statement

D. It should only be reported in the notes to the financial statements.

Answer:

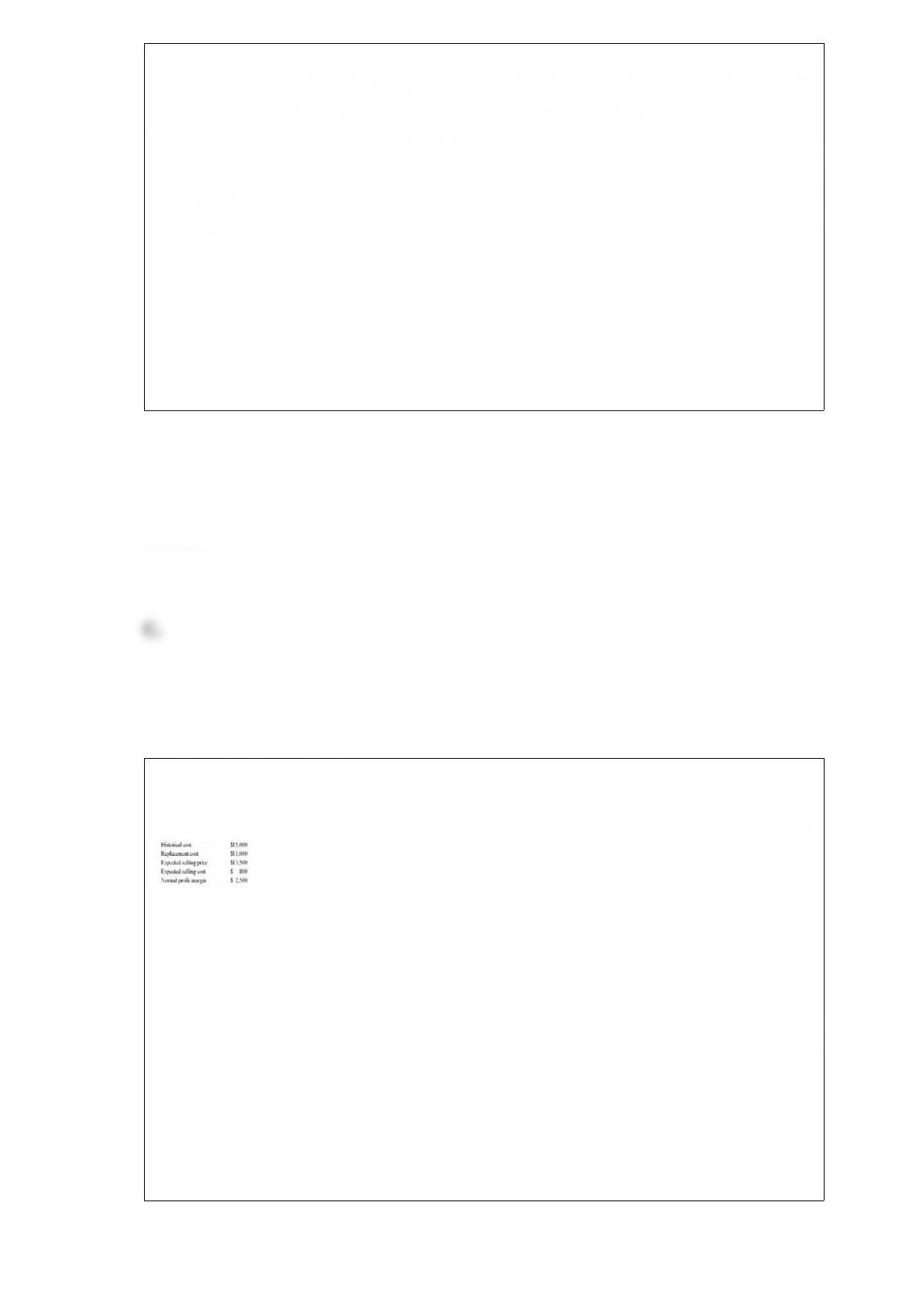

The following inventory information was taken from the records of a foreign

corporation whose stock is listed on an exchange in the U.S.

How will income under the U.S. GAAP compare to income the company reported under

IFRS after reconciliation?

A. Income will not be affected by the reconciliation.

B. Income under U.S. GAAP will be lower by $1,700.

C. Income under U.S. GAAP will be lower by $2,500.

D. Income under U.S. GAAP will be equal to income under IFRS.

Answer:

Which of the following statements is NOT true about Anglo-Saxon Accounting?

A. There is a strong reliance on professional judgment.

B. There is an agreement on the interpretation of the principle of fair presentation.

C. There is a stronger emphasis on substance of reports rather than the form of reports.

D. Audits report on the adherence to the principle of fair presentation.

Answer:

According to the IASB, what is needed for IFRS to work effectively?

A. Commitment from auditors to resist client pressures.

B. Professional judgment in the public interest on the part of companies and auditors.

C. Financial statement preparers must produce reports that faithfully represent all

transactions.

D. All of the above are conditions for effective standards.

Answer:

The corporate social reporting (CSR) theory that environmental disclosures are made in

response to a demand for environmental and social information is called the:

A. legitimacy theory.

B. stakeholder theory.

C. Superfund theory.

D. depletable resource theory.

Answer:

To be carbon neutral means that:

A. an equal amount of gas has been removed from the atmosphere as has been put

there through various emissions.

B. a company pledges not to produce carbon-based products.

C. a company has overpaid its carbon tax.

D. the type of carbon released into the atmosphere has no negative implications on the

environment.

Answer:

The operations of Silver Lights Inc. incorporated in U.S. are spread out in Ireland,

Finland, and Chile. Which of the following statements is true about the operations of

Silver Lights Inc.?

A. The financial statements of Silver Lights must be prepared in local currencies of the

branch countries for consolidation purposes.

B. The external auditor of Silver Lights must be proficient in U.S. auditing and

financial reporting standards to audit the operations of branch offices.

C. Silver Lights Inc. must give credit for the corporate tax paid as per U.S. tax laws to

provide relief from double taxation.

D. The transfer of parts between U.S. operations and other branches should be at the

highest acceptable price most profitable to Silver Lights Inc. keeping in view the rate of

tax and tax authorities in respective nations.

Answer:

Which of the following methods for translating foreign currency financial statements

require to be used under IAS 21?

A. Current/Noncurrent method

B. Monetary/Nonmonetary method

C. Temporal method

D. All of the above may be used under IAS 21.

Answer:

Which of the following true of assets?

A. Assets should be recognized only when it is probable that future economic benefits

will flow to the enterprise.

B. Assets should be recognized when it is probable that an outflow of resources will be

required to settle them.

C. Asset is defined as decrease in equity, other than from transactions with owners.

D. A resource must be owned for it to be recognized an asset of the enterprise.

Answer:

What is one major difference between IFRS and U.S. GAAP relative to correction of

errors?

A. U.S. GAAP is silent as to how to treat errors that have been discovered.

B. IFRS is silent as to how to treat errors that have been discovered.

C. Under U.S. GAAP, a prospective approach is taken.

D. Under IFRS, if it’s impractical to restate financial statements, then no restatement is

necessary.

Answer:

Under IAS 32, which of the following is a financial asset?

A. Investment in equity instruments accounted for under the equity method

B. Investment in special-purpose entities

C. A 30% investment in a subsidiary

D. Loans to other entities

Answer:

Evaluating liquidity and solvency to assess a company’s ability to meet its obligations is

an example of:

A. cash flow analysis.

B. risk analysis.

C. ROI analysis.

D. accounting analysis.

Answer:

Why do German companies willingly take a conservative position in calculating

income?

A. To minimize tax

B. To keep employees from asking for higher wages

C. To report stable income over time for dividend purposes

D. All of the above

Answer:

What is the objective in hedging balance sheet exposure?

A. Controlling the movement of foreign currency exchange rates

B. Creating an equilibrium between foreign currency asset and foreign currency

liability balances affected by exchange rates

C. To control the cash flow resulting from changes in the foreign currency exchange

rates

D. All of the above

Answer:

What is an advantage of using ratio analysis in comparing financial statements from

different countries?

A. Ratios are expressed as percentages, making currency differences irrelevant to the

analysis.

B. Ratios highlight the holding gains or losses related to currency translation.

C. Purchasing power gains and losses from currency translation show up clearly in

ratio analysis.

D. Comparing business ratios across countries removes the effect of economic

conditions and business culture.

Answer:

How is negative goodwill accounted for under U.S. GAAP?

A. There is no rule for negative goodwill, because there is no such thing.

B. It is capitalized and amortized over a period of no more than 40 years.

C. It is treated as an extraordinary loss on the consolidated income statement.

D. It is treated as an extraordinary gain on the consolidated income statement.

Answer:

What is the equivalent of the common stock account on a U.S. balance sheet on the

balance sheet of a British company?

A. Capital redemption reserve

B. Share premium account

C. Own shares held

D. Called-up share capital

Answer:

Under U.S. GAAP, which of the following conditions must be met to qualify for hedge

accounting?

A. There must be formal documentation of the hedging relationship.

B. A derivative must be used specifically to hedge fair value exposure or cash flow

exposure.

C. The hedge must be effective.

D. All of the above must be met in order to qualify for hedge accounting.

Answer:

According to the International Auditing Practices Committee, financial statements have

conformed to International Financial Reporting Standards (IFRS) if:

A. they have complied with at least 75% of the International Financial Reporting

Standards (IFRS).

B. they have complied with at least one-half of the provisions of the International

Financial Reporting Standards (IFRS).

C. they have complied with all requirements and interpretations of the International

Financial Reporting Interpretations Committee (IFRIC).

D. they have complied with most of the International Financial Reporting Standards

(IFRS) or with U.S. GAAP.

Answer:

Which of the following is a reason for the tremendous increase in the flow of foreign

direct investment from 1990 to 2011?

A. The relaxation of transfer pricing regulations

B. The liberalization of investment laws in many countries

C. The similarities in tax rates and tax laws across the globe

D. The universal application of U.S. GAAP accounting standards

Answer:

In Germany, prudence is an accounting principle established in commercial law. What

does “prudence” mean in an accounting context?

A. Reliability

B. Comparability

C. Conservatism

D. Relevance

Answer:

In keeping with Internal Revenue Code, Clarence Company transfers goods to

Marguerite Corporation, its foreign subsidiary, at the price Marguerite will sell the

product to its customers, less the industry’s average gross profit margin of 30%. What

method of transfer pricing is Clarence using?

A. Cost-plus method

B. Comparable uncontrolled price method

C. Comparable profits method

D. Resale price method

Answer:

Which of the following is NOT a characteristic which is indicative of hyperinflation

under IAS 29?

A. The cumulative inflation rate over a three-year period is 75% or higher.

B. Interest rates, wages, and prices are linked to a price index.

C. The price of credit sales includes a “buffer” to compensate for the expected loss in

purchasing power over the credit period.

D. The general population thinks about prices in terms of a stable foreign currency, and

prices may actually be quoted in that currency.

Answer:

Which of the following countries has NOT had its accounting systems significantly

influenced by Germany?

A. Switzerland

B. Denmark

C. Japan

D. France

Answer:

A cost-plus transfer pricing scheme is allowed by the Internal Revenue Service when:

A. it is easiest for the taxpayer to calculate.

B. the related party is primarily a sales subsidiary.

C. there are no comparable uncontrollable sales and the related buyer is more than just

a distributor.

D. the average industry markup is greater than the taxpayer’s standard markup.

Answer:

Which of the following is NOT an influence affecting the operating environment of

foreign subsidiaries?

A. Regulatory controls

B. Social norms and attitudes

C. Inflation rates

D. All of the above are influences.

Answer:

In the United States, conformity between presentation of the financial statements and

the tax statements is required only for:

A. goodwill.

B. depreciation.

C. gains or losses on securities.

D. the use of the LIFO inventory cost flow assumption.

Answer:

If an auditor breaks a contractual obligation, such as failing to complete an audit within

the time frame specified in the engagement letter, what kind of liability does the auditor

face?

A. Criminal liability

B. Civil liability

C. Professional sanctions

D. None of the above

Answer:

How does the U.S. government tax controlled foreign corporations (CFC) differently

from other subsidiaries?

A. All income of the CFC is taxed by the U.S. in the year it is earned rather than when

dividends are received.

B. Some income of the CFC is taxed by the U.S. in the year it is earned rather than

when dividends are received.

C. None of the income generated by the CFC is subject to U.S. tax.

D. Only interest income from CFC is taxed in the year received by the U.S.

government.

Answer:

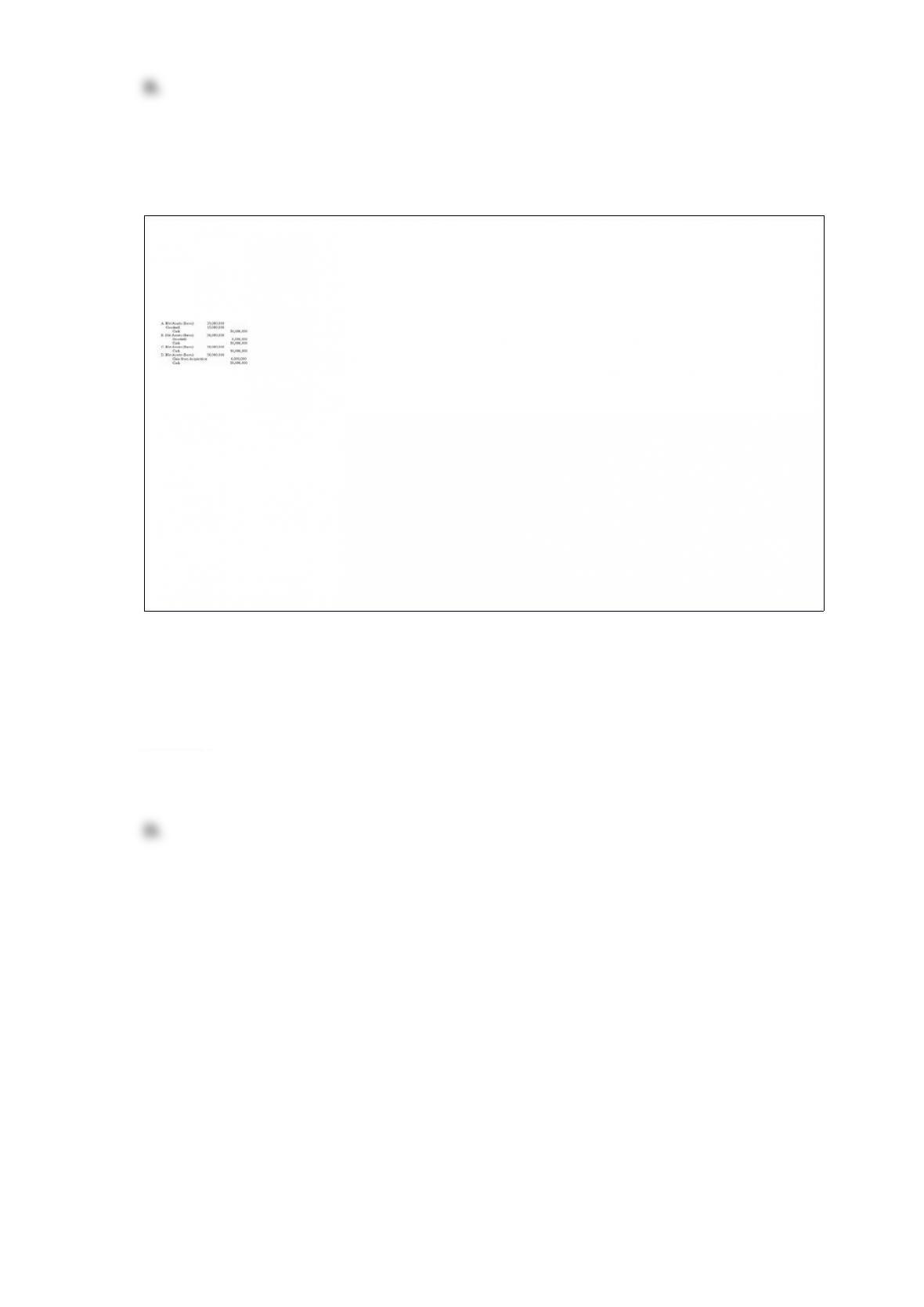

Canto Ltd, a Spanish corporation, acquired 100% interest in Bevo, Inc., a U.S.

corporation for $50,000,000. The net assets of Bevo had a book value of $35,000,000

and a fair value of $56,000,000. How should Canto record the business combination?

A. Entry A

B. Entry B

C. Entry C

D. Entry D

Answer: