Chapter 10 – Analysis of Foreign Financial Statements

Answers to Questions

1. Investors can diversify their risk by including shares of foreign companies in their investment

portfolio. Correlations in the returns (increases and decreases in stock prices) earned

2. Ford might want to include the following companies in a benchmarking study:

U.S. – General Motors, Chrysler

3. Commercial databases tend not to include notes to financial statements, which are an

important source of information about a company. They also tend to force different country

4. The first (easiest) place to look for the most recent annual report is on the company’s

5. Much financial statement analysis is conducted using ratios or percentage changes

(comparing one year with another). Ratios and percentages are not expressed in currency

6. If an analyst is unable to read a company’s annual report, they will be less likely to feel that

they have sufficient information to make an informed investment decision. This would be

7. Disclosures in the notes to financial statements can provide additional detail related to

8. The time lag between fiscal year end and when financial statements are made available to

the public can differ substantially across countries. This time lag is influenced by the stock

market regulator in many countries. For example, the SEC requires U.S. companies to file

10-1

Education.

Chapter 10 – Analysis of Foreign Financial Statements

9. The advantage of using a measure such as EBITDA to compare profitability of companies

across countries is that differences in accounting for interest (I), taxes (T), depreciation (D),

10. The different features that might be “translated” in a convenience translation are:

Language,

Currency, and

11. Analysts should be careful in comparing ratios across companies in different countries

because of differences in business environments that might affect those ratios. For

12. Conservatism implies accelerating the recognition of expenses and liabilities, and deferring

13. Companies with predominantly debt financing (rather than equity financing) will have a

larger amount of liabilities (and a smaller amount of stockholders’ equity), and a larger

amount of interest expense and therefore smaller net income. Profit margins (net

income/sales) will be smaller, and debt-to-equity ratios (total liabilities/total stockholders’

equity) will be larger. Debt financing will reduce both the numerator and the denominator in

10-2

Education.

Chapter 10 – Analysis of Foreign Financial Statements

Effect of Debt on Return on Equity:

No debt Debt 10% Debt 20% Debt 25%

Assets 2,000 2,000 2,000 2,000

Liabilities 0 1,000 1,000 1,000

14. Interest can be either capitalized as part of the cost of a depreciable asset or expensed

immediately. Adjustments to capitalize interest that was previously expensed must be made

to:

Solutions to Exercises and Problems

1. Arcot Company (Calculating ratios from Local GAAP and U.S. GAAP statements)

Ratio Formula

Local

GAAP a.1.

U.S.

GAAP a.2 b. % Diff.

Total asset turnover Sales 9,148 9,148

10-3

Education.

Chapter 10 – Analysis of Foreign Financial Statements

Debt/equity ratio TL 9,148 8,875

a. The profitability ratios using operating income and the current ratio are the ratios most

affected by differences in the two sets of accounting principles. There also is a relatively

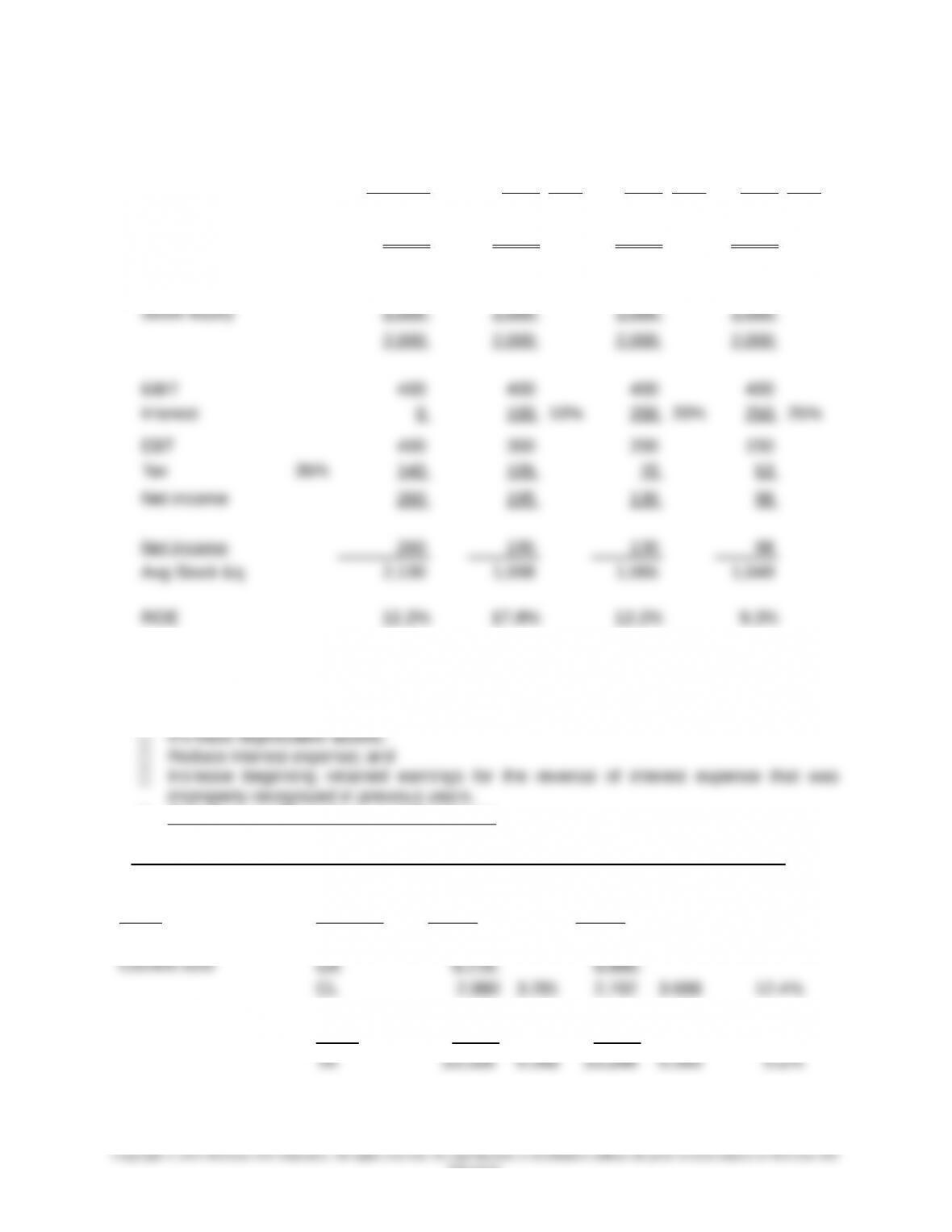

2. China Petroleum & Chemical Corporation (Sinopec) (Comparison of ROE under

different accounting rules)

Accounting Rules

PRC IFRS U.S. GAAP

Profit, 2006 50,664 55,408 54,862

IFRS/PRC U.S./PRC U.S./IFRS

a. % difference in profit 9.4% 8.3% -1.0%

% difference in average equity 3.1% 3.1% 0%

10-4

Education.

Chapter 10 – Analysis of Foreign Financial Statements

IFRS/PRC U.S./PRC U.S./IFRS

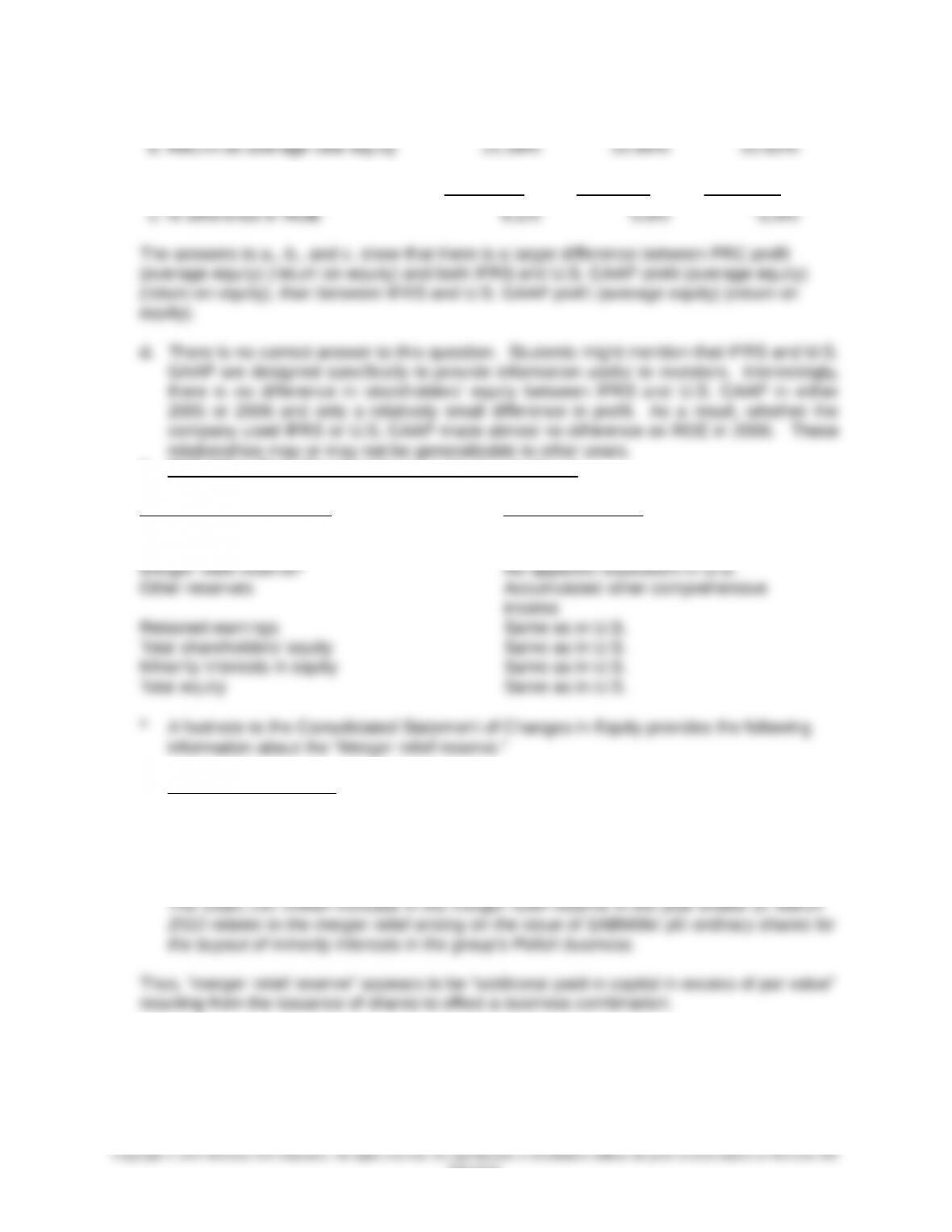

3. SAB Miller PLC (Stockholders’ equity terminology)

SAB Miller Terminology U.S. Terminology

Share capital Common stock

Share premium Paid in capital in excess of par value

Merger relief reserve

In accordance with section 131 of The Companies Act, 1985, the group recorded the

US$3,395 million excess of value attributed to the shares issued as consideration for

Miller Brewing Company over the nominal value of those shares as a merger relief

reserve in the year ended 31 March 2003.

10-5

Education.

Chapter 10 – Analysis of Foreign Financial Statements

4. Babcock International (Reformatting of balance sheet)

Babcock International

Balance Sheet

As at 31 March 2010

Assets £m

Liabilities and stockholders’ equity

5. China Eastern Airlines (Useful life)

a. Adjustment (1) relates to Item (a). Item (a) indicates that flight equipment is depreciated

over 20 years under IFRS and amortized over only 5 years under PRC rules. The larger

amount of amortization expense recognized under PRC rules must be added back to

PRC profit to obtain IFR profit.

10-6

Education.

Chapter 10 – Analysis of Foreign Financial Statements

b. Both adjustments affect retained earnings. Item (a) will require an adjustment in the

6. China Eastern Airlines (Revaluation of fixed assets)

a. Under IFRS, the company has revalued its fixed assets, which resulted in a revaluation

surplus (increase in stockholders’ equity). Under U.S. GAAP, revaluation is not allowed.

6. (continued)

The revaluation of fixed assets must have taken place several years ago. Each year

since revaluation, depreciation expense on the revaluation amount has been taken

under IFRS, with a corresponding reduction in retained earnings. In addition, some of

b. The revaluation of fixed assets causes noncurrent assets (and therefore total assets)

and owners’ equity to be larger and income to be smaller under IFRS than under U.S.

GAAP.

10-7

Education.

Chapter 10 – Analysis of Foreign Financial Statements

7. Novartis Group (Share-based compensation)

a. The amount of expense related to share-based compensation under IFRS was USD 5

million less than would have been recognized under U.S. GAAP. The entry to adjust to

a U.S. GAAP basis would be as follows:

b. Ratio (under U.S. GAAP rather than IFRS) Under U.S. GAAP

Current ratio (CA/CL) ↔/↔ No effect*

Debt to equity ratio (TL/TSE) ↑/↓ Higher

* The company does not provide sufficient information to determine whether the

** Both net income and average stockholders’ equity are smaller under U.S. GAAP. But

10-8

Education.

Chapter 10 – Analysis of Foreign Financial Statements

8. Gamma Holdings NV (Provisions)

a. Percentage change in income (loss) before tax (group result before taxation):

b. Provisions are estimated, accrued liabilities; recognition of a provision increases

c. Provisions are increased at the time that (a) an accrued liability is recognized (increase

provision, increase expense). (Note: Some companies will intentionally overstate a

d.

Calculation of change in “other provisions” 2009 2008 2007

Calculation of income (loss) before tax with no change in “other

provisions” 2009 2008

(34

e. Gamma provides a significant amount of detail about what causes the change in “other

provisions” over time. Analysts would like to know whether the decrease in provisions

results (a) from incurring the cost that had been accrued as a liability or (b) from

9. Gamma Holding NV (Estimation of gross profit)

10-9

Education.

Chapter 10 – Analysis of Foreign Financial Statements

a. Because the “change in finished products (FP) and work in progress (WIP)” is subtracted

in calculating total operating income, the balance in FP and WIP inventory must have

b. To calculate cost of goods sold for the year, an analyst would need to know the amount

c. Operating expenses Total Manufacturing

Raw materials and consumables 212.9 90% 191.6

d. Estimated gross profit margin = 35.8% [235.5/658.5]

10. Neopost SA (Development costs)

a. Calculation of average expected useful life of development costs

Development costs 2009 2008

10-10

Education.

Chapter 10 – Analysis of Foreign Financial Statements

b. Calculation of income before tax and net income assuming development costs

were not capitalized

The “capitalization” of development costs must be subtracted from income before tax

The “charges” (amortization expense) related to capitalized development costs must

be added back to income before tax

The effective tax rate is determined based on actual reported amounts

2009 2008

Calculation of effective tax rate 2009 2008

c. Determination of net profit margin

Calculation of proft margin 2009 2008

Reported amounts

10-11

Education.