Chapter 11 – International Taxation

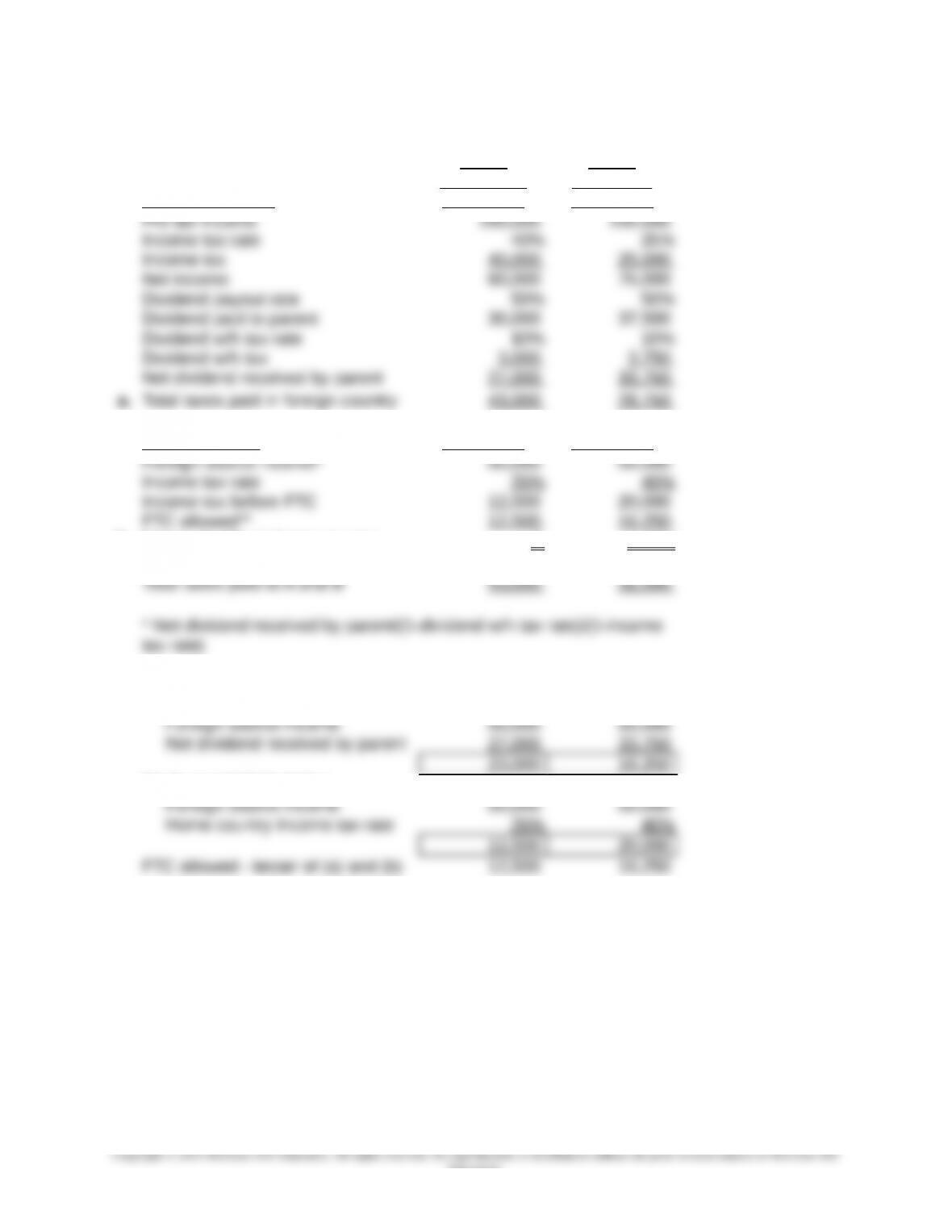

23. Albemarle Company and Bostwick Company

Part 1 Part 2

Albemarle Bostwick

Foreign Country Country B Country A

Home Country Country A Country B

b. Net tax liability in home country 0 3,750

** Calculation of FTC allowed:

(a) Taxes deemed paid

(b) Overall FTC limitation

11-1

Education.

Chapter 11 – International Taxation

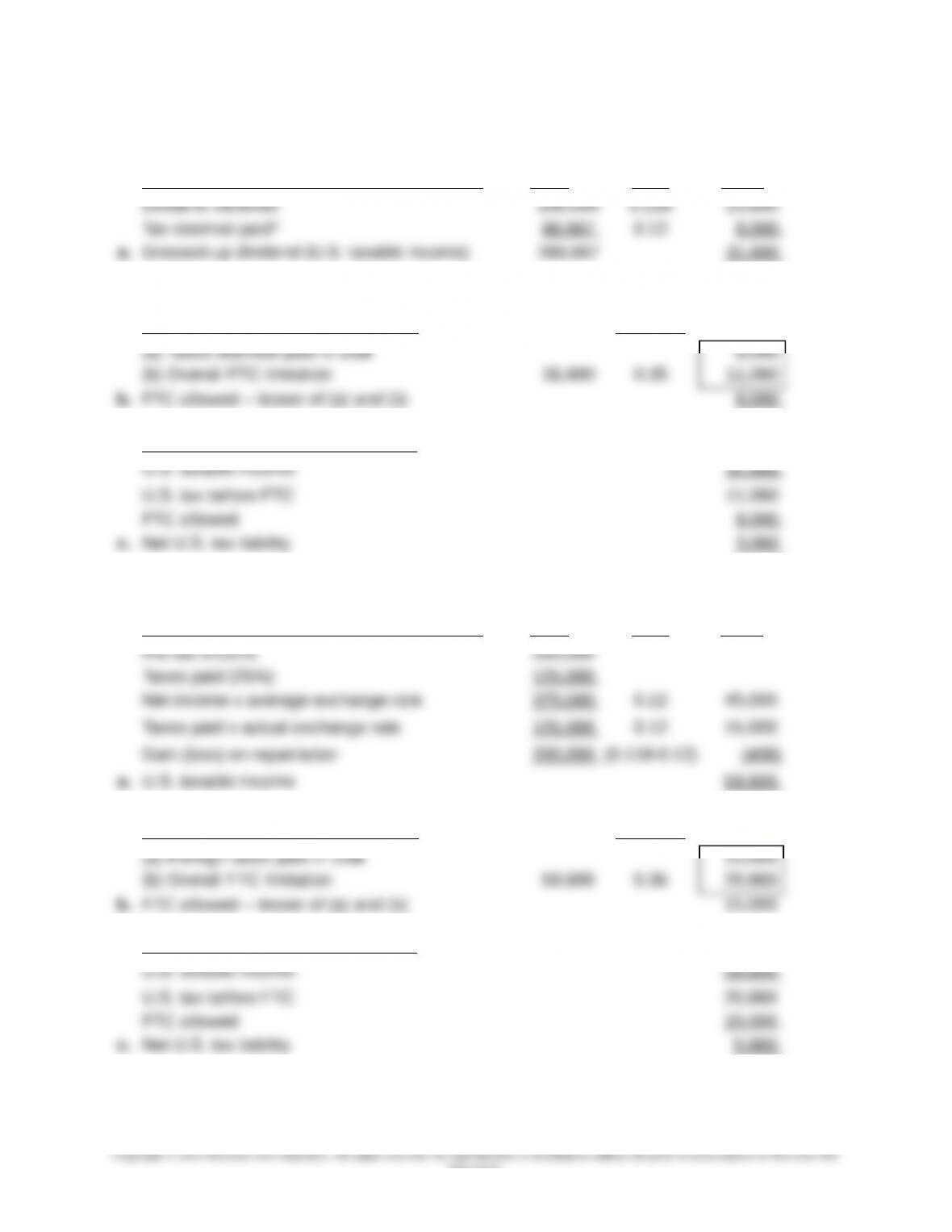

24. Intec Company – foreign subsidiary

Exchange

Calculation of U.S. Taxable Income in US$ RMB Rate U.S.$

* (Dividend / 1 – Chinese tax rate) – Dividend

Calculation of FTC allowed in U.S. Tax Rate

Calculation of net U.S. tax liability

25. Intec Company – foreign branch

Exchange

Calculation of U.S. Taxable Income in US$ RMB Rate U.S.$

Calculation of FTC allowed in U.S. Tax Rate

Calculation of net U.S. tax liability

11-2

Education.

Chapter 11 – International Taxation

26. Brown Corporation

Basic Facts Euros

Exchange rates

a. Brun SA is organized as a branch

Ex Rate Euros Dollars Dollars

Branch profits included in U.S. taxable

income

Loss on July 1 distribution

Gain on December 31 distribution

Determination of foreign tax credit

11-3

Education.

Chapter 11 – International Taxation

26. (continued)

b. Brun SA is organized as a subsidiary

Brown Company includes in its U.S. taxable income — dividends received translated

at actual exchange rate at date of distribution plus taxes paid on those dividends (to

gross-up to a before tax basis)

Ex Rate Euros Dollars Dollars

July 1 Dividend

December 31 Dividend

Actual tax deemed paid on dividends

Proportion of net profit distributed as

dividends)

0

Determination of foreign tax credit

11-4

Education.

Chapter 11 – International Taxation

27. C The U.S. government does not provide U.S. taxpayers with a dividend income exclusion.

28. Horace Gardner

29. Elizabeth Welch

* Calculation of FTC allowed

11-5

Education.

Chapter 11 – International Taxation

Case 11-1 U.S. International Corporation

Note to instructors: The Income Tax Rates in this case for Canada, Japan, and New

Zealand (and the dividend withholding rate in New Zealand) are different from

what they were in the Third Edition of the book, due to actual changes in tax rates

in those countries that took place in 2011.

Determination of Which Countries are Tax Havens

Dividend

Income Withholding Tax

Entity Country Tax Rate Tax Rate Effective Tax Rate on Dividends Haven*

A Argentina 35% 0% 35% + (65% x 0%) = 35% No

Determination of U.S. Taxable Income, Actual Tax Paid, and FTC Basket for Each Entity

A: Argentina – branch

B: Brazil – subsidiary; not a tax haven

C: Canada – subsidiary; tax haven; no subpart F income

D: Hong Kong – subsidiary; tax haven; subpart F income–passive income

Passive Income Basket

E: Liechtenstein – subsidiary; tax haven; subpart F income–foreign base company sales

income

11-6

Education.

Chapter 11 – International Taxation

Case 11-1 U.S. International Corporation (continued)

F: Japan – subsidiary; not a tax haven

G: New Zealand – subsidiary; not a tax haven

Calculation of Foreign Tax Credit

Passive General

Income Income

Basket Basket Total

Calculation of Net U.S. Tax Liability

Foreign Source Income

U.S. Passive General

Source Income Income

U.S. Tax Return Income Basket Basket Total

Excess Foreign Tax Credits

There are no excess foreign tax credits in the current year

11-7

Education.