What must large Japanese corporations report for years ending after 2004 due to recent

amendments to the Japanese commercial code?

A. Statement of changes in financial position

B. Consolidated financial statements

C. Retained earnings statement

D. Cash flow statement

Answer:

What is the term used for intercompany transactions from a subsidiary to a parent?

A. Upstream transfer

B. Horizontal transfer

C. International transfer

D. None of the above

Answer:

Under IFRS 2, with respect to choice-of-settlement share-based payments, if it is the

entity that has the right to choose between equity settlement and cash settlement, when

must the entity choose the cash settlement?

A. If the supplier provides services

B. If the supplier provides goods

C. If the entity has a present obligation to settle in cash

D. The entity always has the option to choose either method.

Answer:

An auditor may be subject to criminal liability under which of the following situations?

A. He/she willingly participates in defrauding the company’s stockholders.

B. He/she breaks a contract with the client.

C. He/she violates a rule on the manner of advertising allowed by the professional

accounting and auditing association.

D. None of the above

Answer:

A Danish subsidiary of a U.S. corporation recorded a building it purchased in 2010 for

100,000,000 krone, when the exchange rate was $0.132/krone. The current exchange

rate is $0.163/krone. Under the current rate method, how should the translated amount

of the restated asset be interpreted?

A. The U.S. parent would have to pay $16,300,000 to acquire the building today.

B. The U.S. parent would have had to pay $13,200,000 to acquire the building in 2010.

C. The building is worth $13,200,000 to the U.S. parent today.

D. None of the above

Answer:

A “bottom-up” test and “top-down” test must be applied under IASB standards to

determine:

A. impairment of tangible fixed assets.

B. impairment of patents.

C. impairment of goodwill.

D. allocation of overhead costs.

Answer:

What kind of exposure exists for foreign currency firm commitments?

A. Fair value exposure

B. Cash flow exposure

C. Both fair value exposure and cash flow exposure

D. Neither fair value exposure nor cash flow exposure

Answer:

Sigma Company issued $12 million in 10 percent bonds 6 years ago currently having a

carrying amount of $10.7 million. The bond agreement allows for early extinguishment

by Sigma Company beginning in the current year. Sigma’s investment bank has

arranged for the company to issue $10 million of new 8 percent bonds at face value to a

group of investors. The proceeds will be used to extinguish the 10 percent bonds. The

banking, legal, and accounting costs to execute the transaction total $200,000. The

journal entry to record the debt extinguishment will include:

A. a debit to Bonds Payable8% for $10,000,000.

B. a credit to Gain on Extinguishment of 10% Bonds for $500,000.

C. a credit to Bonds Payable10% for $12,000,000.

D. a debit to Loss on Extinguishment of 10% Bonds for of $200,000.

Answer:

Which of the following is NOT a share-based payment transaction under IFRS 2?

A. Equity-settled share-based payment

B. Cash-settled share-based payment

C. Choice-of-settlement share-based payment

D. All of the above are share-based payment transactions under IFRS 2.

Answer:

A representative market basket of products cost $250 at the beginning of the year, and

the same collection of products costs $280 at the end of the year. What is the annual rate

of inflation?

A. 10.7%

B. 12%

C. 112%

D. -10.7%

Answer:

For U.S. companies whose shares are publicly traded on U.S. stock exchanges, how

long after year-end must annual reports be filed with the Securities and Exchange

Commission (SEC)?

A. 6 months

B. 90 days

C. 60 days

D. 30 days

Answer:

A plan for next year expressed in quantitative terms is referred to as:

A. strategy.

B. capital budget.

C. operating budget.

D. management control system.

Answer:

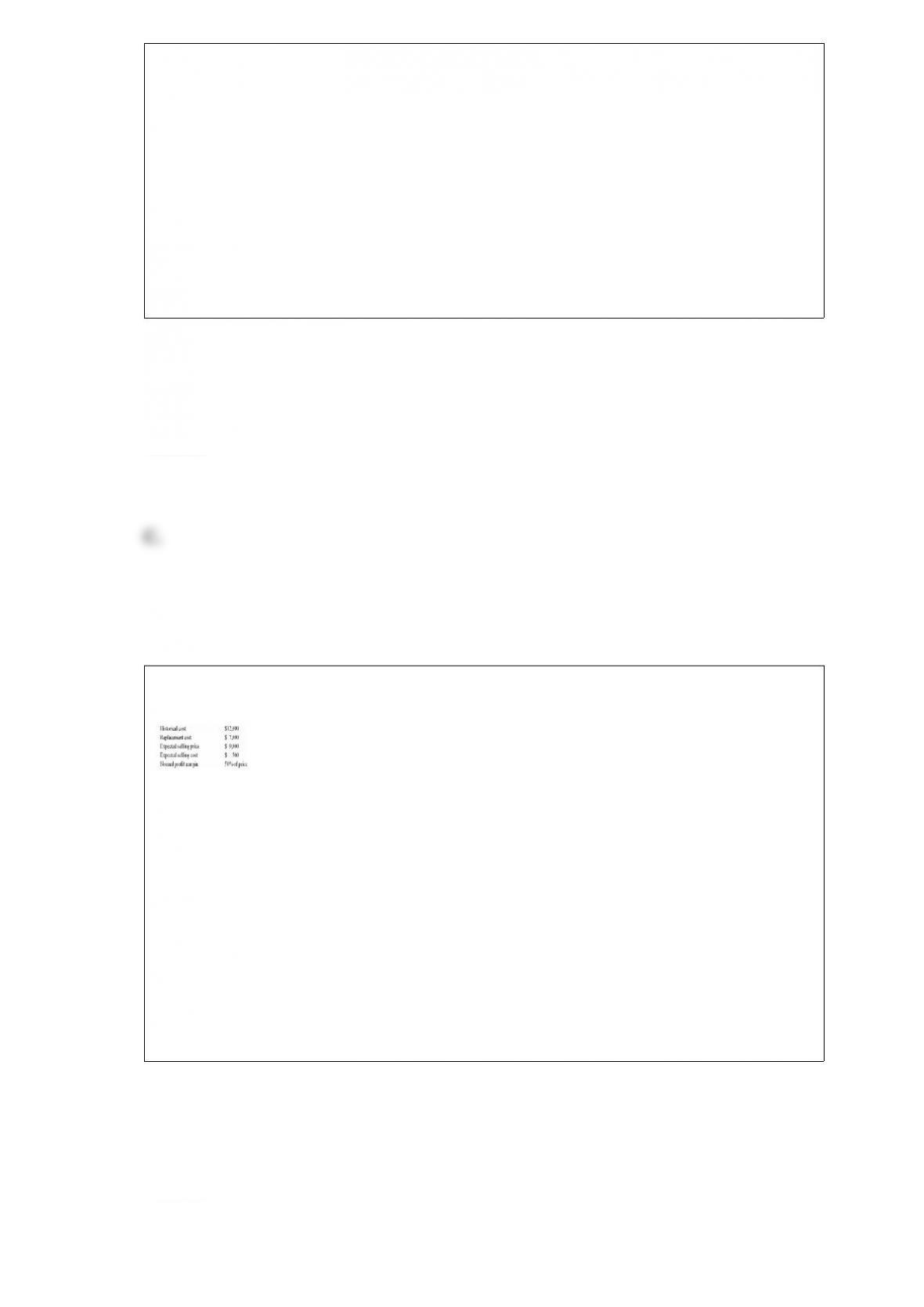

The following inventory information was taken from the records of Kleinfeld Inc.:

Under U.S. GAAP, what should the balance sheet report for Inventory?

A. $9,000

B. $8,500

C. $7,000

D. $10,000

Answer:

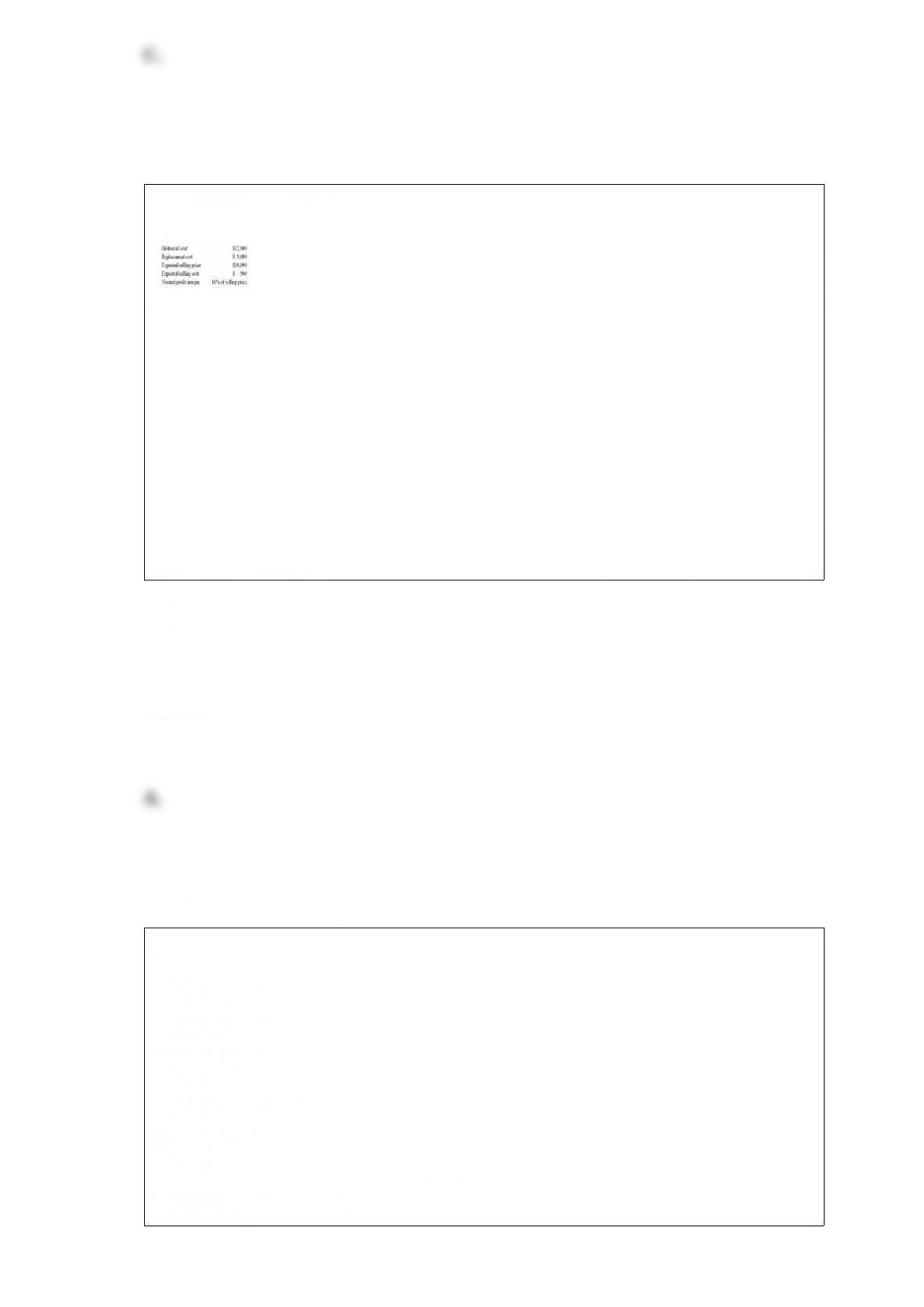

The following inventory information was taken from the records of GlobeKom Ltd.:

Under U.S. GAAP, what should the balance sheet report for Inventory?

A. $9,000

B. $8,500

C. $9,500

D. $10,000

Answer:

Under IAS 27, how is “control” defined?

A. Ownership of 50% of more of the voting shares of another entity

B. Representation on another entity’s board of directors

C. The power to govern financial and operating policies of an entity so as to obtain the

benefits from its activities

D. Ownership of 30% or more of the voting shares of another entity

Answer:

According to the Internal Revenue Service, the most reliable measure of an arm’s-length

prices for sales of tangible property in intercompany transactions is:

A. cost-plus method.

B. comparable profits method.

C. comparable uncontrolled price method.

D. resale price method.

Answer:

According to the study published by Professors Chan and Lo in 2004, which of the

following variables is important when market-based methods of determining transfer

prices are preferred?

A. Restrictions on profit repatriation

B. Good relationship with local government

C. Minimization of import duties

D. Risk of expropriation and nationalization

Answer:

Why did the European Commission stop issuing directives related to accounting in

1990?

A. The EU was leaving the formulation of accounting standards up to the IASC.

B. The European Commission had finished the task of formulating accounting

standards for the European Union.

C. Accounting harmonization had been completed.

D. The Commission found that its directives were unenforceable.

Answer:

According to IFRS 8 (Segment Reporting), which is NOT one of the three criteria for

defining an operating segment?

A. An operating segment can’t merely be a lessor.

B. An operating segment is a component of a business that generates revenues.

C. An operating segment is a component of a business whose operating results are

regularly reviewed by the chief operating officer.

D. An operating segment has separate financial information available.

Answer:

Worldwide, which type of transfer is most likely to be audited?

A. Rental or lease payment made for use of tangible property

B. Sale of tangible property

C. Intercompany services

D. Exports

Answer:

Since 2003, what method for supplemental disclosure of inflation-adjusted financial

statements is required of all companies affected by the IASB standards?

A. No rule is currently in place that generally requires inflation-adjusted financial

statements.

B. General purchasing power method must be used.

C. Current replacement cost method must be used.

D. Companies have the option of using current cost or historical cost.

Answer:

Under IAS 2, what adjustment needs to be made after an inventory write-down if the

selling price subsequently increases?

A. No adjustment is necessary. Once inventory is written down, it cannot be increased

under IASB standards.

B. It should be sold at the replacement cost.

C. The inventory write-down should be reversed to bring it in line with the new net

realizable value.

D. Recovery of inventory loss should be debited to reflect the increase in inventory

value.

Answer:

The “price” for using intangible property is called:

A. interest.

B. rent.

C. royalty.

D. service charge.

Answer:

Which of the following financial statements is NOT required in Mexico?

A. Statement of financial position

B. Statement of cash flows

C. Statement of changes in financial position

D. Income statement

Answer:

What has occurred when one company arranges to buy a foreign currency sometime in

the future, at an exchange rate quoted today?

A. The company has purchased a foreign currency option.

B. The company has entered a forward contract.

C. The currency has been devalued.

D. None of the above

Answer:

Under IAS 1, Presentation of Financial Statements, which of the following is NOT a

criterion in the definition of a current liability?

A. It is a liability that is expected to be settled in an entity’s normal operating cycle.

B. It is a liability primarily held for the purpose of trading.

C. It is a liability that does not have the right to defer until 18 months after the balance

sheet date.

D. It is a liability that is expected to be settled within 12 months of the balance sheet

date.

Answer:

Imperial Chemical Industries, a U.K. corporation, recorded interest incurred in

constructing fixed assets as an expense of £128,000,000. When reconciling its financial

statements to U.S. GAAP, what should be done with this interest?

A. It should be subtracted from the fixed asset account balance.

B. It should be added to the fixed asset account balance.

C. It should be deducted from retained earnings.

D. This amount should be charged to accumulated depreciation.

Answer:

According to IAS 16 (Property, Plant and Equipment), what is the term used to indicate

the amount for which an asset could be exchanged between knowledgeable, willing

parties in an arm’s length transaction?

A. Replacement cost

B. Net realizable value

C. Fair value

D. Historical cost

Answer:

What information would most likely NOT be available on the EDGAR system?

A. Form 10-K for a U.S. corporation listed on the New York Stock Exchange (NYSE)

B. Quarterly financial statements for a foreign corporation listed on the American

Stock Exchange (AMEX)

C. The annual report for a corporation listed only on the London and Tokyo stock

exchanges

D. The notes to the financial statements of a foreign corporation listed on the NYSE

Answer:

Which of the following represents the difference between UK GAAP and IFRS with

respect to proposed dividends?

A. Under UK GAAP, proposed dividends should not be recognized as a liability at the

balance sheet date, whereas IFRS mandates proposed dividends to be accrued as a

liability.

B. UK GAAP has provided no guidance on this issue, whereas IFRS prohibits the

recognition of proposed dividends as accrued liability.

C. Under UK GAAP, proposed dividends should be accrued as a liability, whereas

under IFRS, it should not be recognized as a liability at the balance sheet date.

D. IFRS has no specific guidance regarding the treatment of proposed dividends,

whereas UK GAAP mandates proposed dividends to be recognized as accrued liability.

Answer:

Which method of accounting for changing prices (inflation) updates assets by applying

inflation rates to historical costs?

A. Current replacement cost method

B. Current rate method

C. Temporal method

D. General purchasing power method

Answer:

Prior to 2007, which method of accounting for inflation most closely represented the

supplemental reporting required in Mexico?

A. Current replacement cost

B. Current cost

C. General purchasing power

D. Historical cost

Answer: