Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 05 - International Financial Reporting Standards: Part II

28. Cypress Company – Revenue Recognition (rendering of services)

IAS 18 indicates that, when the outcome of a service transaction (a) can be estimated

reliably and (b) it is probable that economic benefits of the transaction will flow to the

enterprise, revenue from the rendering of services should be recognized on a stage of

completion basis. The outcome of a transaction can be estimated reliably when (1) the

amount of revenue, (2) the costs incurred and the costs to be incurred, (3) and the stage of

completion can all be measured reliably. Whether it is appropriate for Cypress Company to

use the stage of completion method for its contract with the Gervais Group depends on

whether these three criteria are met:

29. Phil’s Sandwich Company – Revenue Recognition (customer loyalty program)

Phil’s Sandwich Company has a customer loyalty program that must be accounted for in

accordance with IFRIC 13. In the first quarter of the current year, Phil’s had sales of $84,000

($7.00 average price x 12,000 sandwiches). Phil’s must allocate this amount between

sandwich sales revenue and award credits (deferred revenue) based on the fair value of the

credits awarded. The amount to be allocated to the free sandwich awards is determined as

follows:

Education.

Chapter 05 - International Financial Reporting Standards: Part II

Deferred revenue 4,200

30. Saffron Enterprises, Inc. – Available-for-Sale Financial Asset (foreign currency bonds)

Journal Entries in Year 1

31. Spectrum Fabricators Inc. – Convertible Bonds (initial recognition and interest)

5-2

Education.

Chapter 05 - International Financial Reporting Standards: Part II

Interest expense

31. (continued)

Interest expense by year is determined as follows:

Beginning

Balance in

Bonds

Interest

Expense

(8.122%)

Interest

Payment

Ending

Balance in

Bonds

Year 1 $18,310,901 $1,487,218 $1,200,000 $18,598,119

32. Bockster Company – Preferred Shares (classification)

Part A. Preferred Shares Redeemable at Option of Shareholder

5-3

Education.

Chapter 05 - International Financial Reporting Standards: Part II

Part B. Preferred Shares Convertible into Common Stock

33. Tempe Company – Long-term Debt (extinguishment)

The carrying value of the 10% bonds of $9,950,000 along with the issuance costs on the 9%

bonds of $100,000 are both included in the calculation of the gain or loss on extinguishment

of debt.

34. Macro Arco Corporation – Long-term Debt (troubled debt restructuring)

Macro Arco Corporation (MAC) records a gain on the debt restructuring, calculated as

follows:

The journal entry would be as follows:

Friendly Neighbor Bank (FNB) would record a loss on the restructuring calculated as follows:

5-4

Education.

Chapter 05 - International Financial Reporting Standards: Part II

The journal entry to record the debt restructuring and loss would be as follows:

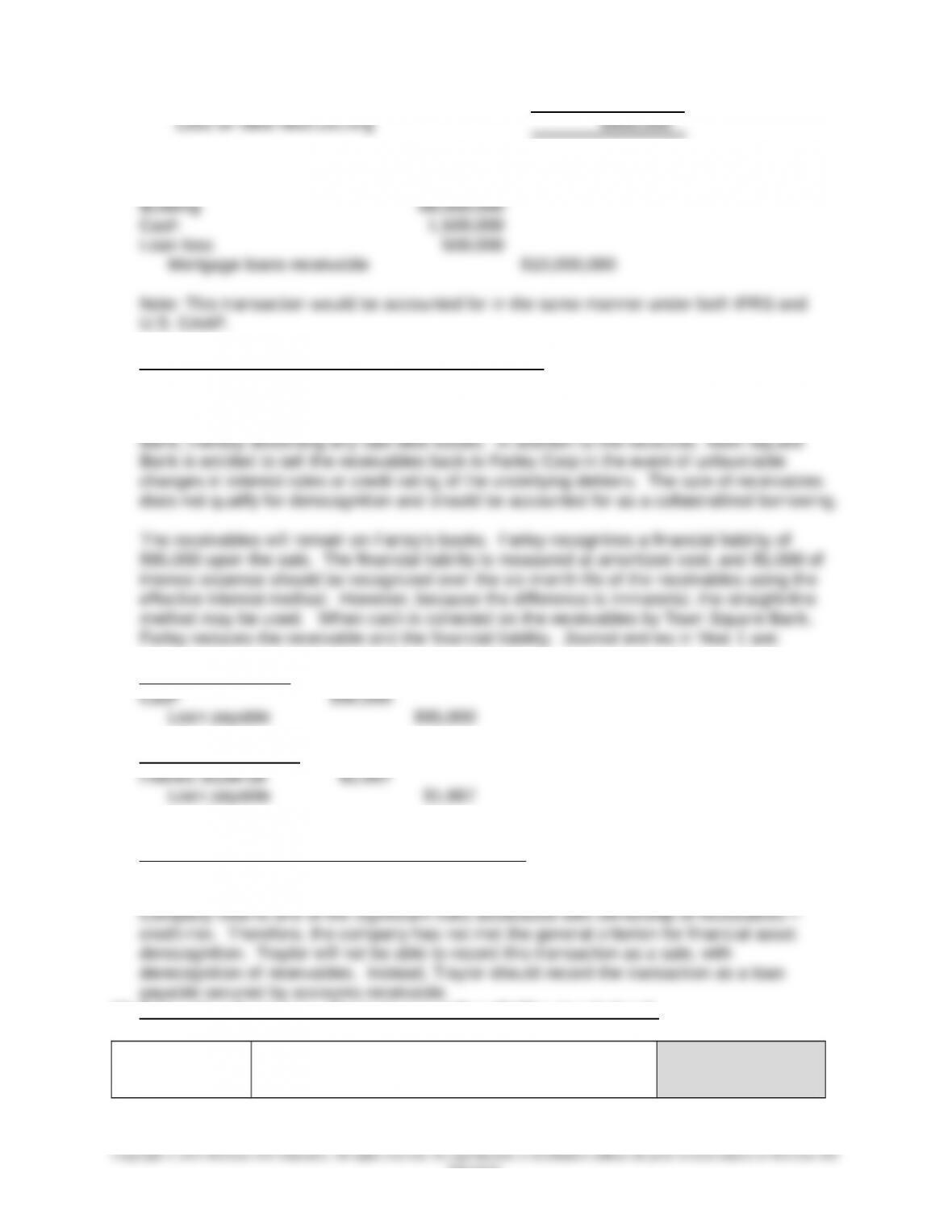

35. Farley Corporation – Receivables (derecognition)

Farley has retained substantially all of the risks and rewards associated with the financial

assets. Under the right of recourse, Farley ultimately must deliver $100,000 to Town Square

November 1, Year 1

December 31, Year 1

36. Traylor Company – Receivables (derecognition)

By guaranteeing to buy back up to 15% of the receivables that cannot be collected, Traylor

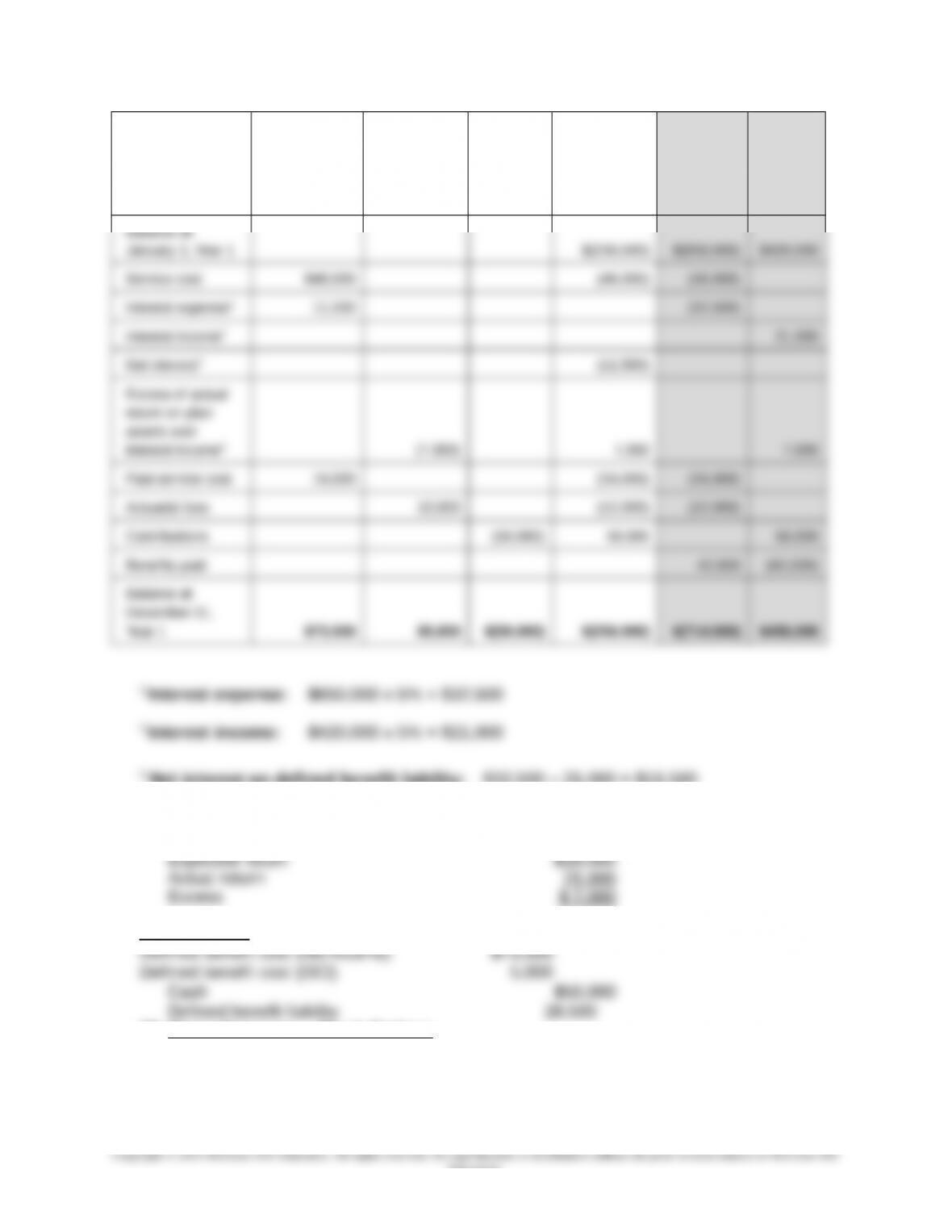

37. Campolino Company – Postretirement Benefit Plan (worksheet)

Campolino Company

General Ledger

Benefit Fund

General Ledger

5-5

Education.

Chapter 05 - International Financial Reporting Standards: Part II

Defined

benefit cost

recognized

in

net income

Defined

benefit cost

recognized

in

OCI Cash

Defined

benefit

asset

(liability) PVDBO FVPA

4 Excess of actual return on plan assets over net interest on defined benefit liability:

Journal Entry

38. Stone Company – Stock Options

Part A.

5-6

Education.

Chapter 05 - International Financial Reporting Standards: Part II

According to IFRS 2.35, because Stone has granted employees stock options that can be

settled either in cash or in shares of stock, this is a compound financial instrument.

Calculation of Compensation Expense for Year 1 (and Year 2)

For equity-settled share-based payment (SBP) transactions, the services received and

equity recognized is measured at the fair value of the equity instrument at grant date.

Because the fair value of the equity component for Stone is zero, there is no compensation

expense recognized related to the equity component.

38. (continued)

Compensation expense related to the debt component for Year 1:

Education.

Chapter 05 - International Financial Reporting Standards: Part II

Calculation of Compensation Expense for Year 3

Settlement on December 31, Year 3

38. (continued)

Part B.

Under this scenario, employees receive a 10% discount on the exercise price if they choose

to settle in shares of stock. As a result, the equity-settlement alternative has a larger fair

value than the cash-settlement alternative, and therefore, the equity component has a value

greater than zero.

5-8

Education.

Chapter 05 - International Financial Reporting Standards: Part II

Calculation of Fair Value of Stock Options at Grant Date

Calculation of Compensation Expense for Year 1

Compensation expense related to the debt component in Year 1 is $1,867 (same as in Part

A).

5-9

Education.