Answers to Questions

1. A provision is a liability of uncertain timing or amount. A provision must be recognized when:

2. A contingent liability is (a) a possible obligation or (b) a present obligation that is not

3. A constructive obligation exists when an entity, through past actions or current statements,

4. An onerous contract exists when the unavoidable costs of meeting the obligation of the

5. Under IAS 19, the net amount recognized as a defined pension benefit liability (or asset) is

measured as:

Under U.S. GAAP, the pension liability or asset is simply measured as:

6. Under IAS 19, past service costs are recognized immediately in net income and actuarial

7. Compensation cost in an equity-settled share-based payment (SBP) transaction with non-

8. Compensation cost associated with stock options that vest on a single date is recognized as

9. In a choice-of-settlement share-based payment (SBP) transaction in which the supplier of

10. Income tax rates that have been enacted or substantively enacted should be used in

11. A deferred tax asset is recognized only when it is probable that a tax benefit will be realized

12. IAS 12 requires an explanation of the relationship between tax expense and accounting

13. Deferred taxes are classified as noncurrent items on the balance sheet.

14. Five criteria must be met to recognize revenue from the sale of goods:

1. The significant risks and rewards of ownership of the goods have been transferred to the

buyer.

2. Neither continuing managerial involvement normally associated with ownership nor

16. There is no gain or loss recognized when assets that are similar in nature and value are

17. Revenue may be recognized on a bill and hold sale when:

a. It is probable that delivery will be made,

18. A customer loyalty program provides customers with “award credits” at the time a purchase

is made that the customer can convert into goods and/or services when a sufficient number

of credits have been accumulated. Airline frequent flyer programs are an example. The fair

19. The five steps to follow in revenue recognition as proposed in the IASB-FASB exposure

draft Revenue from Contracts with Customers are:

20. The four classes of financial assets are:

Financial assets at fair value through profit or loss (FVPL)

21. Preferred shares should be recognized as a liability on the balance sheet when they are

22. Convertible bonds are a compound financial instrument subject to “split accounting.” Upon

23. When (1) a financial instrument measured at fair value through profit or loss is hedged with

24. An entity is prohibited from classifying financial instruments as held-to-maturity for two years

25. Bond issuance costs reduce the fair value of the bonds payable and are subtracted in

26. Debt extinguishment costs are included in the calculation of the gain/loss on debt

27. Derecognition of receivables in a so-called pass through arrangement is appropriate only if

each of the following criteria is met:

Solutions to Exercises and Problems

1. B

15. Charley Horse Company – Provision (onerous contract)

The contract to purchase organic hay on January 30, Year 2 is an onerous contract. The

16. Chestnut, Inc. – Provision (restructuring)

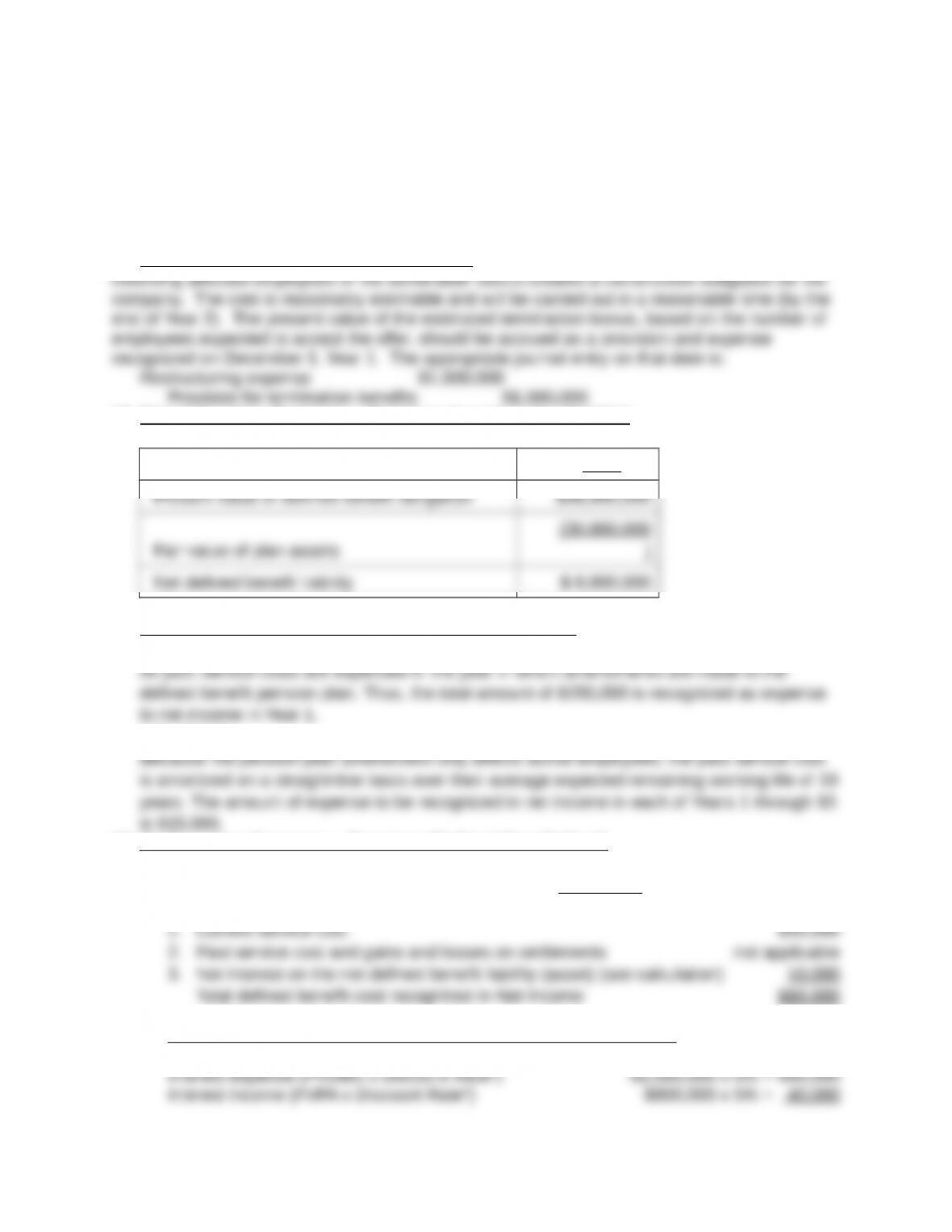

17. Kissel Trucking Company – Pensions (pension plan liability)

IFRS

18. Hoverman Corporation – Pensions (past service cost)

IFRS:

U.S. GAAP:

19. Northeastern Company – Pensions (Defined Benefit Cost)

a. The components of defined benefit cost reported in net income are:

Calculation of net interest on the net defined benefit liability (asset):

b. Remeasurements of the net defined benefit liability (asset) are the component of defined

benefit cost reported in other comprehensive income (OCI). Remeasurements consist

of:

Calculation of difference in actual return on plan assets and interest income component

of NIDBLA:

White River Company – Pensions (pension plan asset)

IFRS:

The amount at which a defined benefit asset may be reported on the balance sheet is the

lesser of two amounts:

U.S. GAAP:

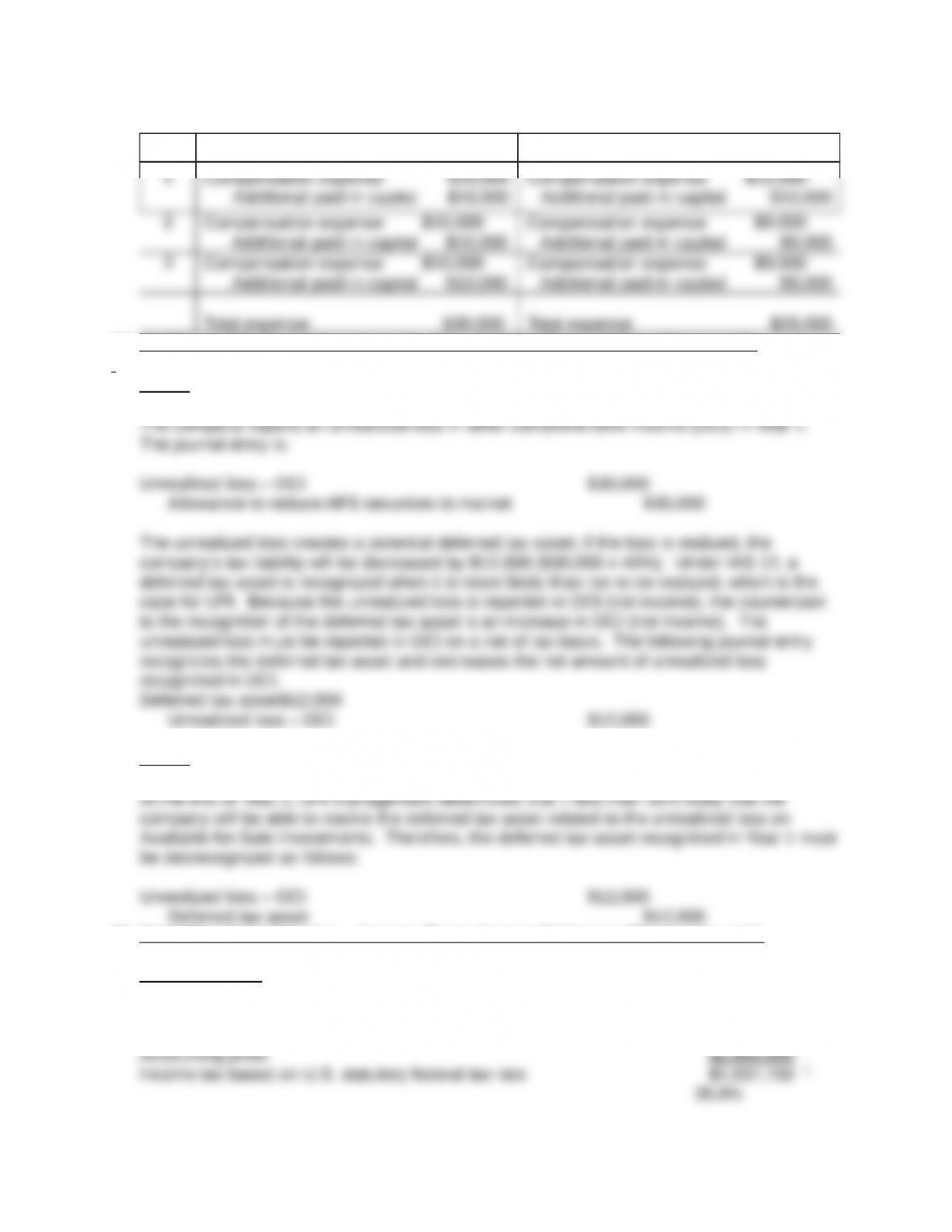

21.Argy Company – Stock Options (graded vesting)

IFRS:

Tranche

Compensation Cost

per Tranche Year 1 Year 2 Year 3

U.S. GAAP:

22. SC Masterpiece Company – Stock Options (modification)

IFRS:

US GAAP:

Journal Entries

Year IFRS U.S. GAAP

23. Updike and Patterson Investments, Inc. – Income Taxes (deferred tax asset)

Year 1

Year 2

24. Gotti Manufacturing, Inc. – Income Taxes (reconciliation to effective tax rate)

Presentation 1.

Reconciliation of domestic tax rate to effective tax rate:

Presentation 2.

Reconciliation of average tax rate to effective tax rate:

25. Mishima Technologies Company – Revenue Recognition (right of return)

26. Ultima Company – Revenue Recognition (bill and hold sale)

c. the buyer specifically acknowledges the deferred delivery instructions; and

d. the usual payment terms apply.”

The facts of the problem indicate that customers take title at the date of sale, so the

question is whether the four criteria are met:

Criterio

n

Criterion met? Evidence

27. Miller-Porter Company – Revenue Recognition (multiple elements)

This problem involves a so-called “multiple-element arrangement.” The sale of powder

coating equipment should be accounted for as separate units of account. Because delivery,

installation, and initial testing occur at one point of time, these elements may be combined

into one unit of account, and the revenue allocated to this unit of account may be recognized

at the date at which these elements are fulfilled.

Revenue recognition policy

Journal entries

Revenue $45,200

Deferred revenue 4,800

Date of service call – Deferred revenue $400

Revenue $400