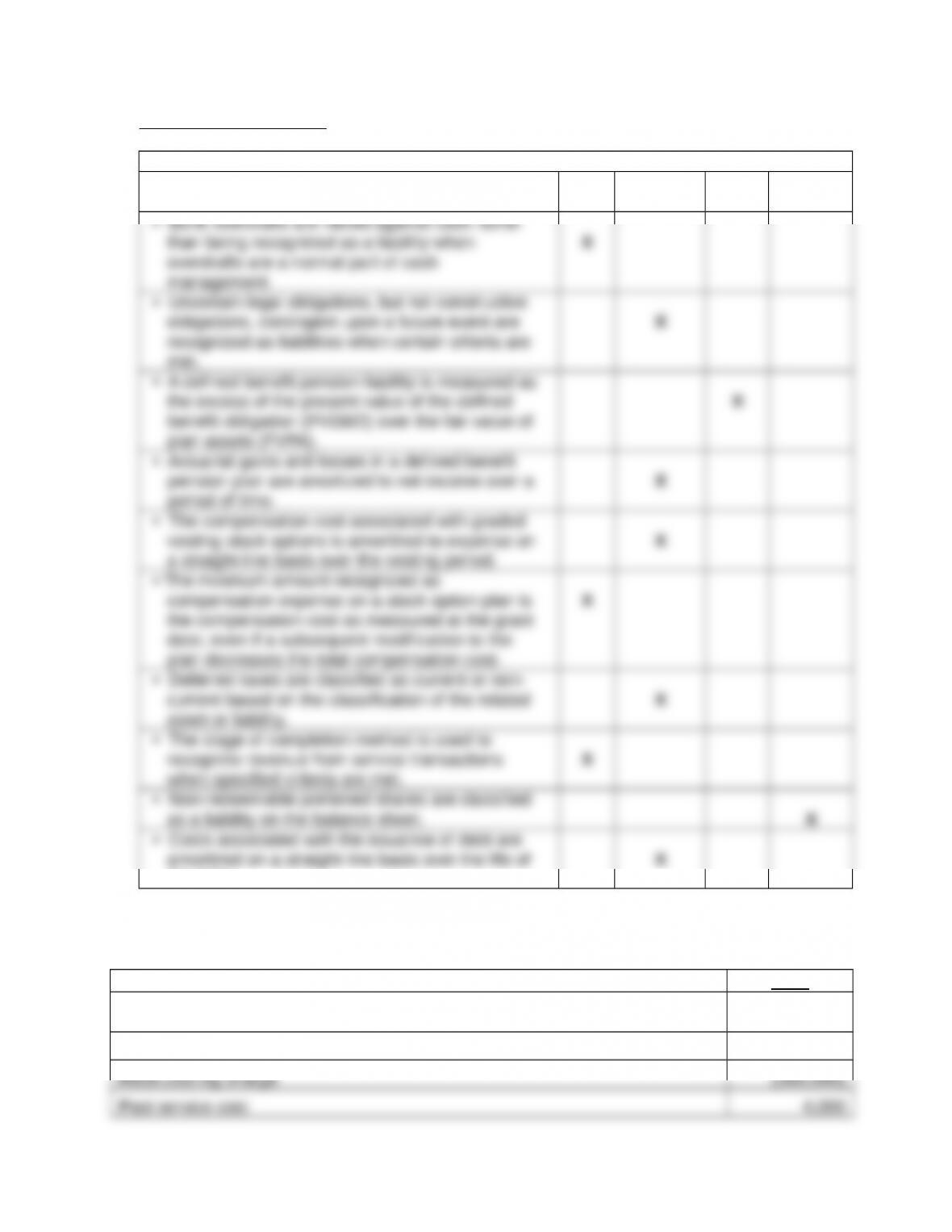

39. Acceptable Treatments

Acceptable under

IFRS

U.S.

GAAP Both Neither

the debt.

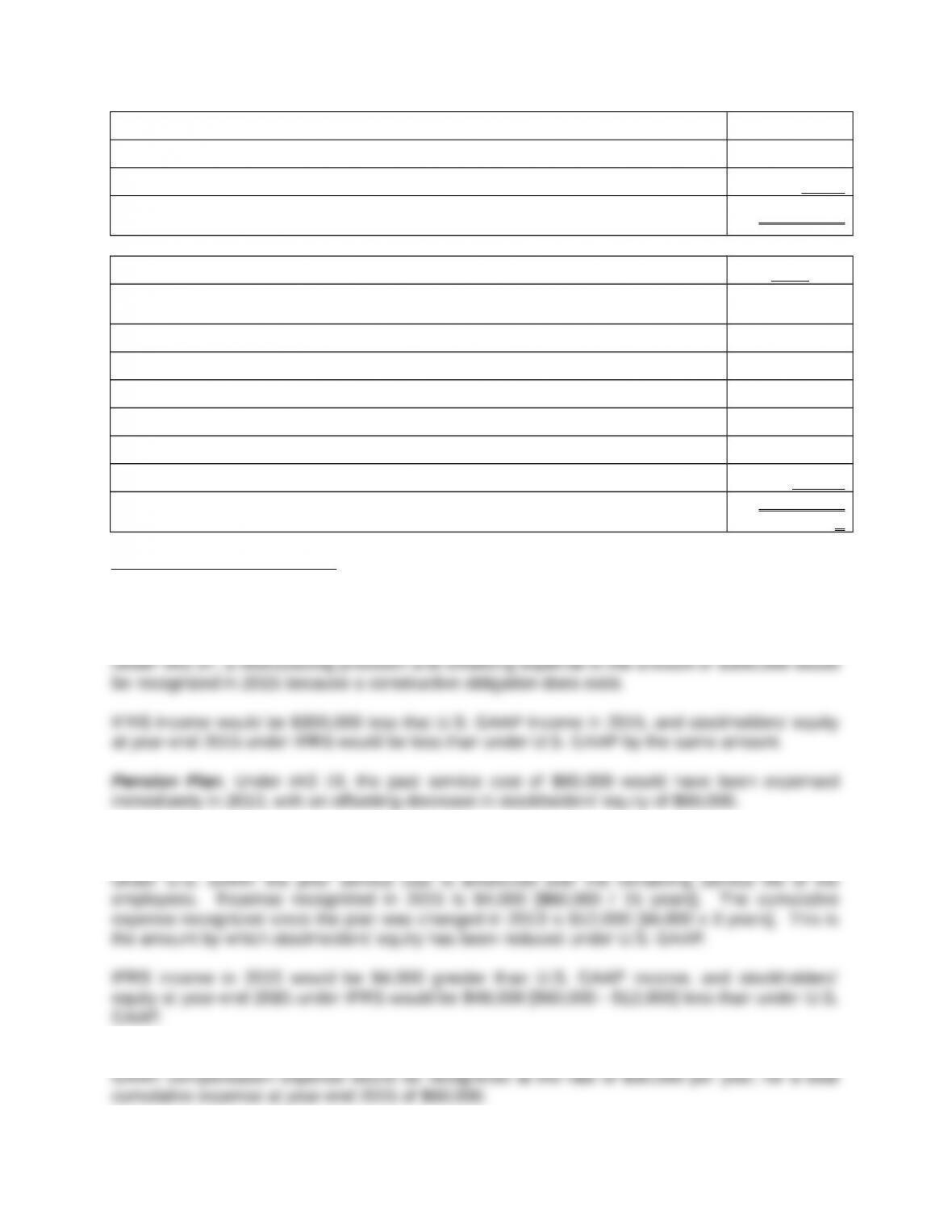

Case 5-1 S. A. Harrington Company

Reconciliation from U.S. GAAP to IFRS

2015

Income under U.S. GAAP

$5,000,0

00

Adjustments:

Explanation of Adjustments

Restructuring. Under U.S. GAAP, the restructuring is not recognized in 2015 because a legal

obligation does not yet exist.

Case 5-1 S. A. Harrington Company (continued)

Stock Options. The total compensation cost related to the stock options is $90,000. Under U.S.

Under IFRS, compensation expense would be recognized as follows:

Installment

Compensation

Cost per

Installment

Compensation

Expense

2014

Compensation

Expense

2015

Compensation

Expense

2015

Revenue Recognition. No revenue would be recognized on this service contract under U.S.

GAAP because the services have not yet been completed.

Case 5-1 S. A. Harrington Company (continued)

Under IFRS, the bond issuance costs reduce the carrying amount of the bonds to $9,500,000,

and the effective interest rate is determined to be 6.193% [$9,500,000 cash inflow on January 1,

2014; $500,000 cash outflow on December 31, 2014 – 2018; and $10,000,000 cash outflow on