Chapter 11 – International Taxation

Answers to Questions

1. MNCs can finance their foreign operations by making capital contributions (equity) or

2. In some countries, local governments impose a separate tax on business income in

3. Tax havens are tax jurisdictions with abnormally low corporate income tax rates or no

4. Under the worldwide approach to taxation, all income of a resident of a country or a

5. The combination of a worldwide approach to taxation and the various bases for taxation

can lead to overlapping tax jurisdictions that can lead to double or perhaps triple taxation.

11-1

Education.

Chapter 11 – International Taxation

7. U.S. companies are allowed either to (1) deduct all foreign taxes paid or (2) take a credit

for foreign income taxes paid. “Income” taxes include both income taxes and withholding

8. The U.S. treats foreign branches as U.S. residents for tax purposes and taxes foreign

9. The maximum amount of foreign tax credit a U.S. company will be allowed to take related

10. An excess foreign tax credit is created when the amount of taxes paid to the foreign

government on foreign source income is greater than the amount of foreign tax credit

allowed to be taken by the U.S. government. This occurs when the effective tax rate paid

11. The excess FTC generated from one basket of income may only be carried back and

12. Tax treaties are bilateral agreements between two countries as to how companies and

13. Treaty shopping is where a resident of Country A uses a corporation in Country B to get the

14. A controlled foreign corporation is any foreign corporation in which U.S. shareholders hold

more than 50% of the combined voting power or fair market value of the stock. Only those

11-2

Education.

Chapter 11 – International Taxation

15. Subpart F income of a controlled foreign corporation (CFC) is taxed currently (like foreign

branch income). The amount of CFC income currently taxable in the U.S. depends upon

the percentage of CFC income generated from Subpart F activities. Assuming that none of

a CFC’s income is repatriated as a dividend:

16. Determining the appropriate U.S. tax treatment of foreign source income can be quite

complicated. The four factors that determine the manner in which income earned by a

17. Foreign branch net income is translated into US$ using the average exchange rate for the

year. Foreign branch net income is then grossed-up by adding taxes paid to the foreign

11-3

Education.

Chapter 11 – International Taxation

18. U.S. trading partners argued that both the Domestic International Sales Corporation and

19. The Foreign Earned Income Exclusion allows U.S. taxpayers to exclude a certain amount

20. To qualify for the Foreign Earned Income Exclusion U.S. taxpayers must:

1. have their tax home in a foreign country and

2. meet either (a) a bona fide residence test or (b) a physical presence test.

Solutions to Exercises and Problems

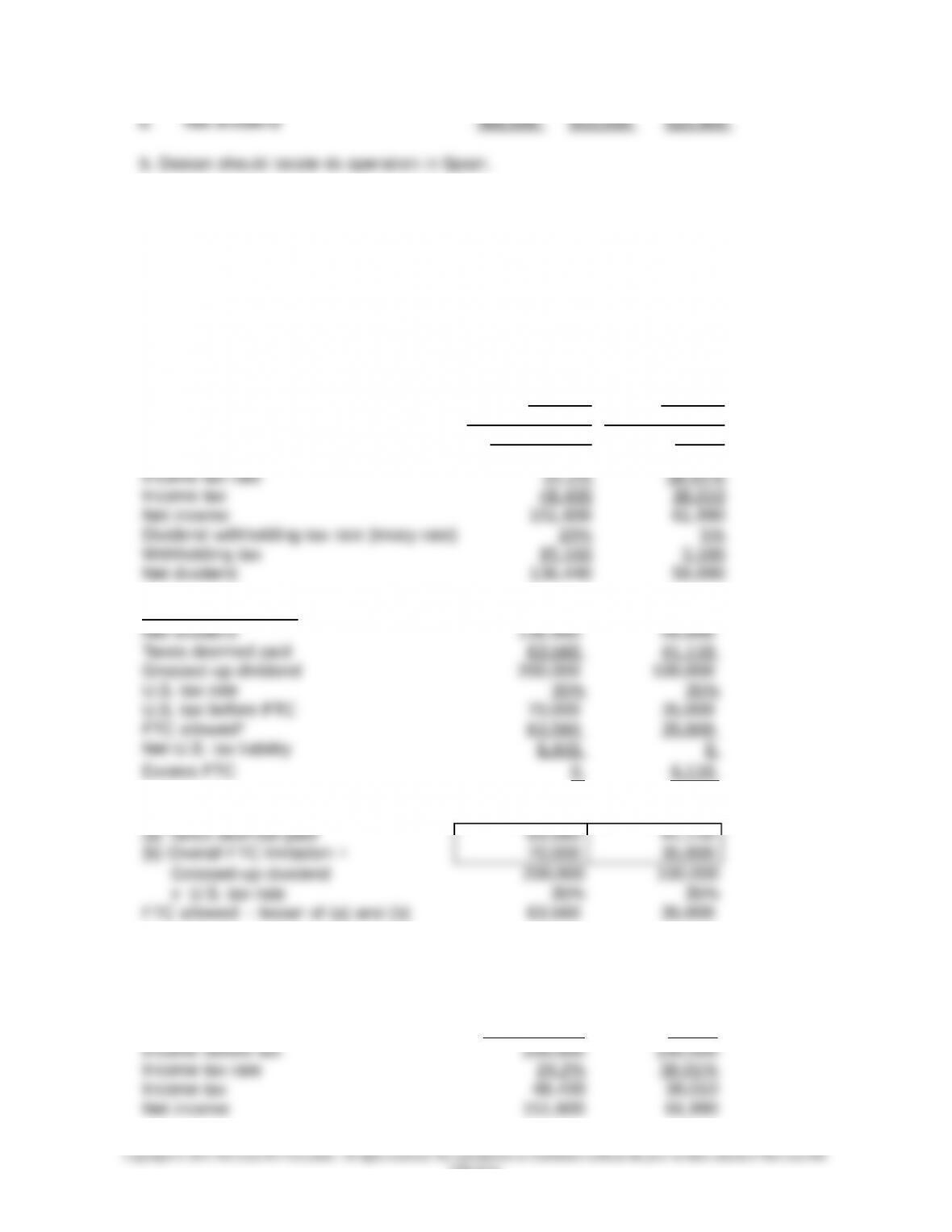

14.

Foreign Branch

Calculation of U.S. taxable income

11-4

Education.

Chapter 11 – International Taxation

Calculation of FTC allowed in U.S.

Calculation of net U.S. tax liability

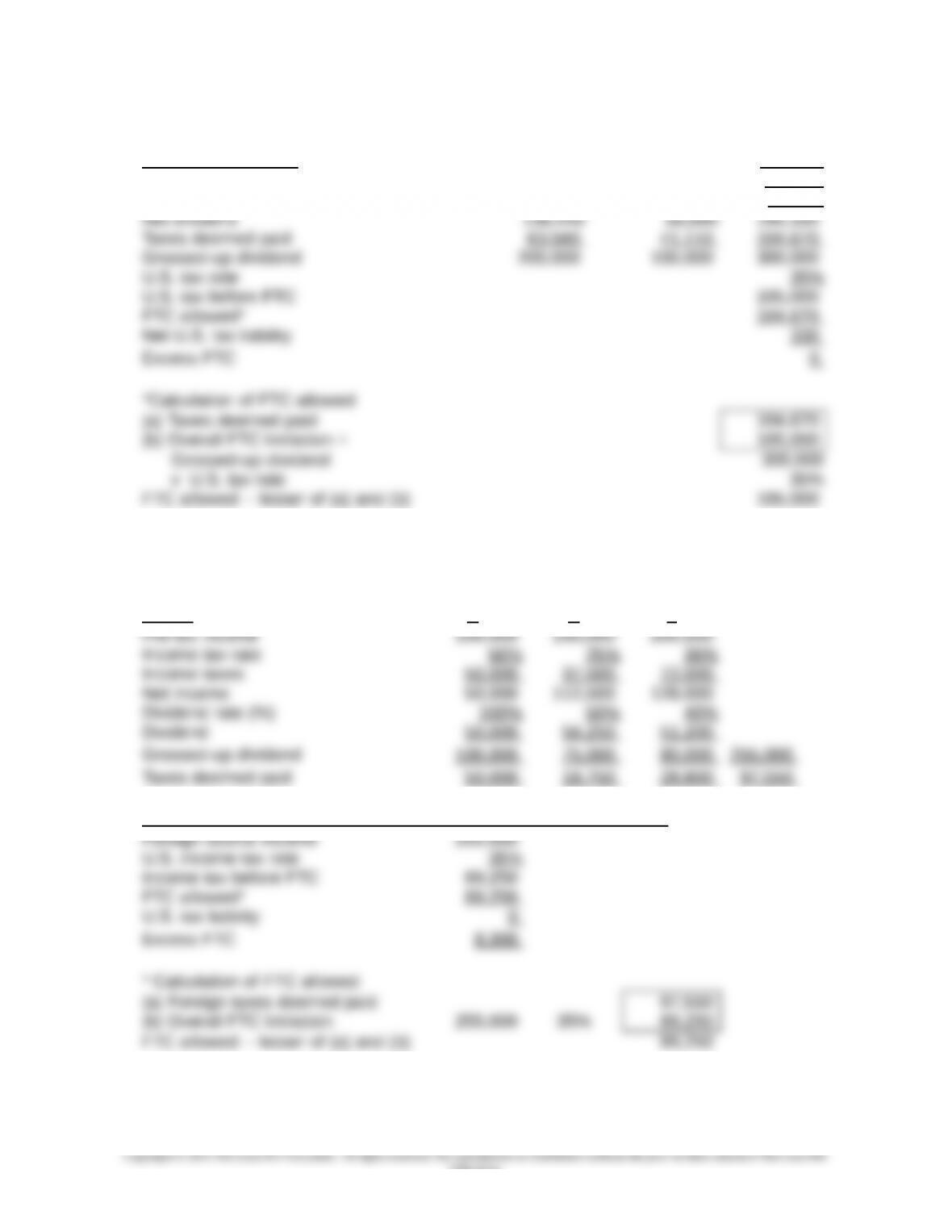

15.

Foreign Subsidiary

Calculation of Grossed-up Dividend

Calculation of FTC allowed in U.S.

Calculation of net U.S. tax liability

16. Mama Corporation

By purchasing finished goods from its parent company and selling those goods outside of

the Bahamas, Bahamamama Ltd. generates foreign base company sales income, which is

Subpart F income.

11-5

Education.

Chapter 11 – International Taxation

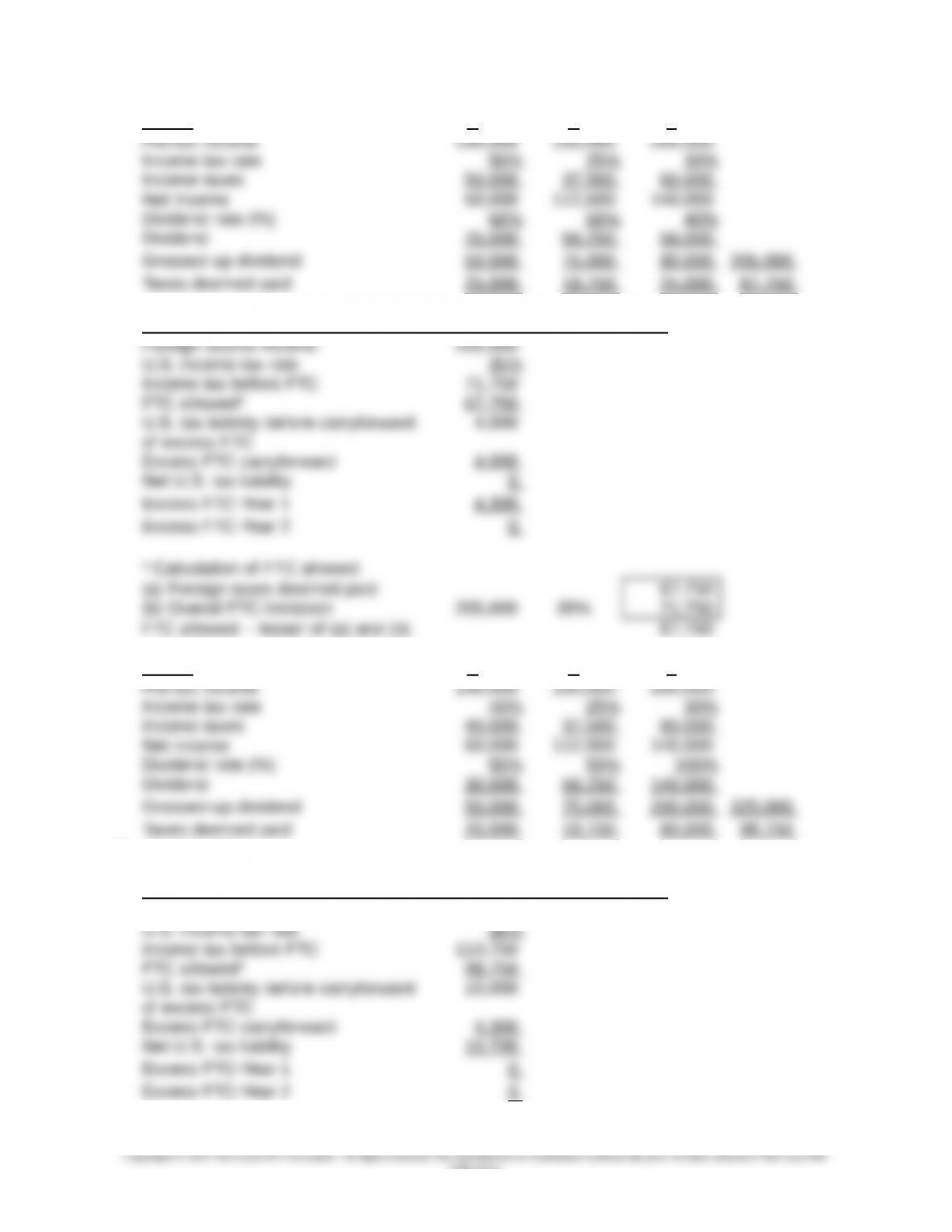

a. 80% of Bahamamama’s income is subpart F income, so 100% of its income will be

b. 60% of Bahamamama’s income is subpart F income, so 60% of its income will be taxed

17. Lionais Company

Calculation of Home Country Tax Liability

Deduction Credit

18. Avioco Limited

19. Daisan Company

France Spain Sweden

11-6

Education.

Chapter 11 – International Taxation

20. Pendleton Company

a. The South Korean subsidiary generates income from manufacturing and sales (General

Income Basket) and the Japanese subsidiary generates income from passive investments

(Passive Income Basket). The excess FTC in the Passive Income Basket of $6,110 can be

carried back one year and carried forward ten years only to reduce taxes paid to the U.S.

government on Passive Income Basket income. The excess FTC cannot be used to pay

the net U.S. tax liability on General Income Basket income of $6,440.

General

Income Basket

Passive

Income Basket

South Korea Japan

Income before tax 200,000 100,000

Calculation of FTC

*Calculation of FTC allowed

b. The South Korean subsidiary generates income from manufacturing and sales, and the

Japanese subsidiary generates income from sales and distribution, both of which are

allocated to the General Income Basket.

South Korea Japan

11-7

Education.

Chapter 11 – International Taxation

Dividend withholding tax rate 10% 5%

11-8

Education.

Chapter 11 – International Taxation

20. (continued)

Calculation of FTC General

Income

Basket

21. Eastwood Company

Year 1 X Y Z

Calculation of FTC allowed, excess FTC, and net U.S. tax liability

21. (continued)

11-9

Education.

Chapter 11 – International Taxation

Year 2 X Y Z

Calculation of FTC allowed, excess FTC, and net U.S. tax liability

Year 3 X Y Z

21. (continued)

Calculation of FTC allowed, excess FTC, and net U.S. tax liability

Foreign source income 325,000

11-10

Education.

Chapter 11 – International Taxation

Summary Year 1 Year 2 Year 3

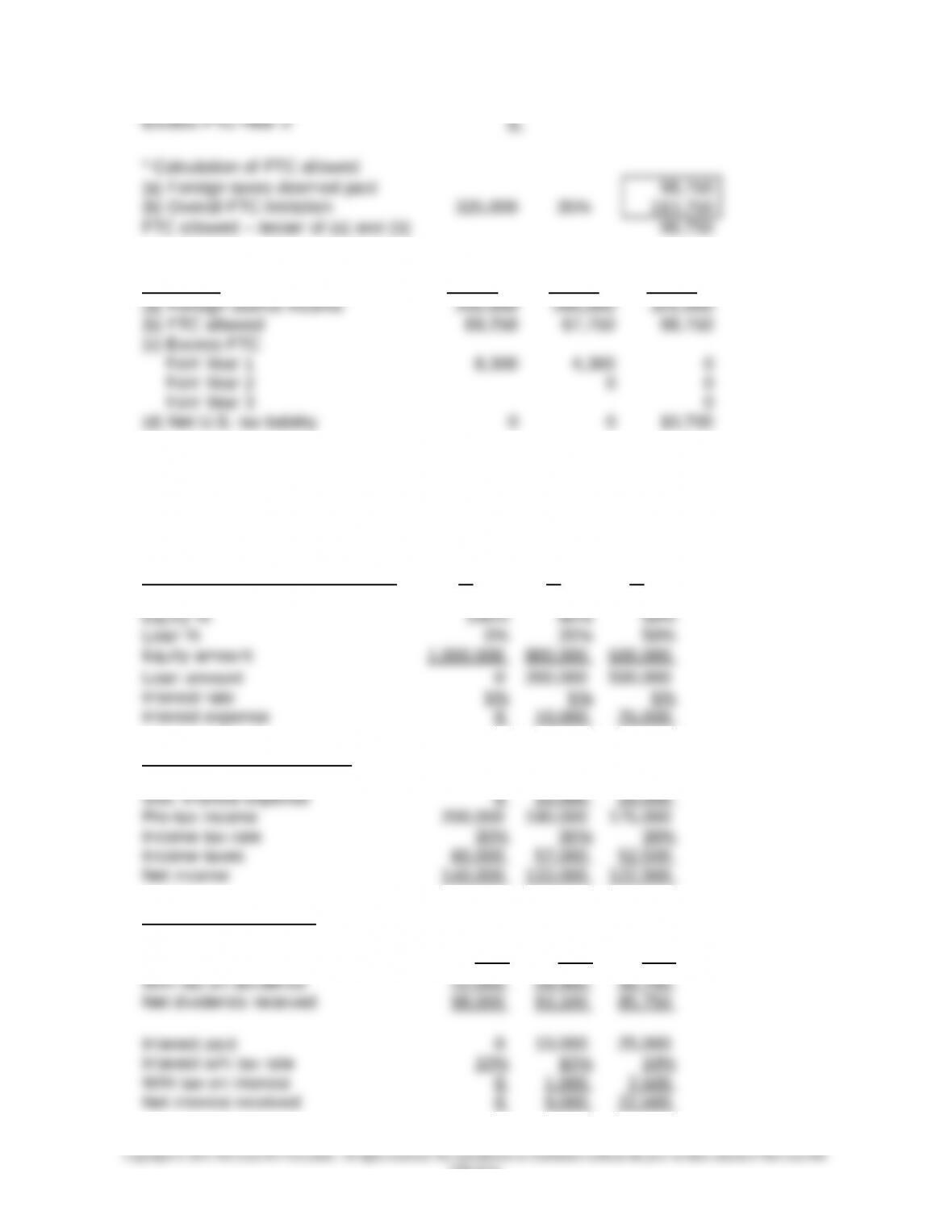

22. Heraklion Company

a. Ignoring any tax treaty, investment alternative 3 results in the least amount of taxes paid to

the Australian government.

Investment Alternative

Calculation of Interest Expense 1 2 3

Total investment 1,000,000 1,000,000 1,000,000

Calculation of Net Income

Income before interest and taxes 200,000 200,000 200,000

Cash Flows to Parent

Dividends (100% x net income) 140,000 133,000 122,500

Dividend w/h tax rate 30% 30% 30%

11-11

Education.

Chapter 11 – International Taxation

22. (continued)

b. Even with the tax treaty that reduces the dividend withholding rate from 30% to 5%,

investment alternative 3 still results in the least amount of taxes paid to the Australian

government.

Investment Alternative

Calculation of Interest Expense 1 2 3

Total investment 1,000,000 1,000,000 1,000,000

Calculation of Net Income

Income before interest and taxes 200,000 200,000 200,000

Cash Flows to Parent

11-12

Education.