Chapter 04 – International Financial Reporting Standards: Part I

Answers to Questions

1. The types of differences that exist between IFRS and U.S. GAAP can be classified as:

2. In applying the lower of cost and market rule for inventories, IAS 2 defines market as net

3. The estimated costs of dismantling and removing an asset must be included in the asset’s

4. The two models allowed by IAS 16 are the cost model and the revaluation model. Under the

5. Any item of property, plant, and equipment may be accounted for under the revaluation

6. The revaluation surplus is an element of other comprehensive income in stockholders’

7. When an item of property, plant, and equipment is comprised of significant parts that have

8. Under the fair value model for investment property, changes in fair value are recognized in

9. Under IAS 36, an impairment loss arises when an asset’s recoverable amount is less than

4-1

Education.

Chapter 04 – International Financial Reporting Standards: Part I

10. A previously impaired asset may be written back up only to what it’s carrying amount would

11. The three types of intangible assets are: (1) purchased, (2) acquired in a business

12. Under IAS 36, expenditures giving rise to a potential intangible are classified as either

13. Indefinite-lived intangibles and goodwill are subject to impairment testing at least annually.

14. Goodwill is measured as the excess of (a) consideration transferred plus noncontrolling

15. A gain on bargain purchase exists when (a) consideration transferred plus noncontrolling

16. Goodwill must be tested for impairment annually. Goodwill that can be allocated to a

17. IAS 23 (revised in 2007) requires borrowing costs to be capitalized to the extent they are

18. Borrowing costs are defined more broadly in IAS 23 than are interest costs in U.S. GAAP.

4-2

Education.

Chapter 04 – International Financial Reporting Standards: Part I

19. IAS 17 describes five situations that would normally lead to a lease being classified as a

finance lease, but does not describe these as being absolute tests. (The standard provides

20. A difference in accounting for a sale-and-leaseback gain exists between IFRS and U.S.

GAAP when the lease is classified as an operating lease. Under U.S. GAAP, the gain must

21. U.S. GAAP requires interest paid and received and dividends received to be classified as

22. IAS 10 establishes the date that financial statements are authorized for issuance as the cut-

23. IAS 8 establishes the following hierarchy of authoritative pronouncements to be followed in

selecting accounting policies to apply to a specific transaction or event:

Solutions to Exercises and Problems

4-3

Education.

Chapter 04 – International Financial Reporting Standards: Part I

4. D Total $100,000

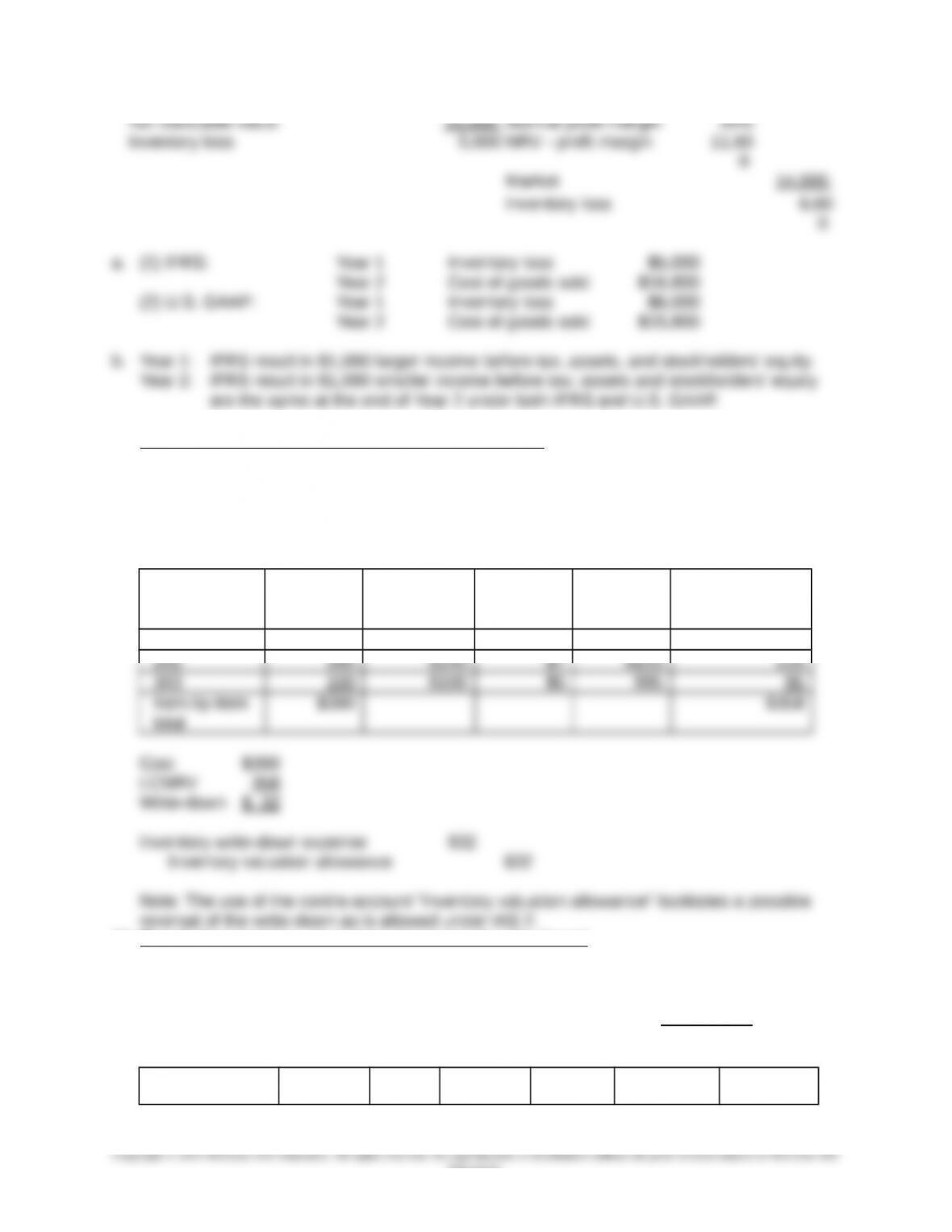

13. Optiplex Company – Inventory (determination of cost)

Cost to complete the design of the generators $ 3,000

14. Monroe Company – Inventory (LCNRV valuation)

IFRS U.S. GAAP

0

4-4

Education.

Chapter 04 – International Financial Reporting Standards: Part I

15. Beech Corporation – Inventory (LCNRV valuation)

IAS 2.29 indicates that inventories are usually written down to NRV item by item. Grouping

is acceptable when several criteria are met, including relating to the same product line.

Because these three products relate to three different product lines, grouping would not be

allowed.

Product Cost

Selling

price

12/31/Y1

Selling

costs

(5%)

NRV

12/31/Y1

LCNRV

(item by item)

12/31/Y1

101 $130 $160 $8 $152 $130

16. Beech Corporation – Inventory (reversal of write-down)

IAS 2 indicates that an inventory write-down is reversed when, for example, inventory is still

on hand and its selling price has increased. The reversal is limited to the amount of the

original write-down. The new carrying amount should be the lower of original cost and

current NRV.

Product Carrying

Amount

Cost Selling

price

Selling

costs

NRV

12/31/Y2

LCNRV

12/31/Y2

4-5

Education.

Chapter 04 – International Financial Reporting Standards: Part I

12/31/Y1 12/31/Y2 (5%)

101 $130 $130 $190 $9.50 $180.50 $130.00

17. Steffen-Zweig Company – Exchange of Assets

Because the exchange transaction lacks commercial substance, no gain would be

recognized. The acquired printing press is measured at the carrying value of the asset given

up ($24,000) less cash received ($3,000).

18. Stevenson Corporation – Property, Plant and Equipment (component depreciation)

IAS 16.44 states: “an entity allocates the amount initially recognized in respect of an item of

property, plant and equipment to its significant parts and depreciates separately each such

part.” This is referred to as “component depreciation.” Thus, the total cost of $500,000

4-6

Education.

Chapter 04 – International Financial Reporting Standards: Part I

must be allocated to carpeting, roof, HVAC system, and the rest of the building, and each

component is depreciated separately over its expected useful life.

Depreciable base Useful Life Depreciation

Carpeting $ 10,000 5 years $ 2,000

19. Quick Company – Property, Plant, and Equipment (impairment)

a. IAS 36 requires companies to assess annually whether there are any indicators that an

asset is impaired. If so, then an impairment loss calculation must be made. External

b.

December 31, Year 4

Cost $100,000

Accumulated depreciation ($10,000 x 4) 40,000

Carrying amount, 12/31/Y4 $60,000

December 31, Year 5

December 31, Year 6

4-7

Education.

Chapter 04 – International Financial Reporting Standards: Part I

20. Godfrey Company – Property, Plant and Equip (dismantling and inspection costs)

Calculation of Initial Cost, January 1, Year 2: Amount

PV Factor

(10%)

Building

Construction cost $ 1,500,000

Journal entry at January 1, Year 2:

4-8

Education.

Chapter 04 – International Financial Reporting Standards: Part I

Building $ 1,722,965

Calculation of Depreciation Expense, Year 2

Building

Cost $1,722,965

Useful life 20 years

21. Jefferson Company – Property, Plant and Equipment (measurement subsequent to

acquisition)

Cost, 1/2/Y1 $10,000,000

Useful life 5 years

4-9

Education.

Chapter 04 – International Financial Reporting Standards: Part I

Equipment (book value) 1 2 3 4 5

IFRS

Beginning $10 mn $8 mn $6 mn $8 mn $4 mn

U.S. GAAP

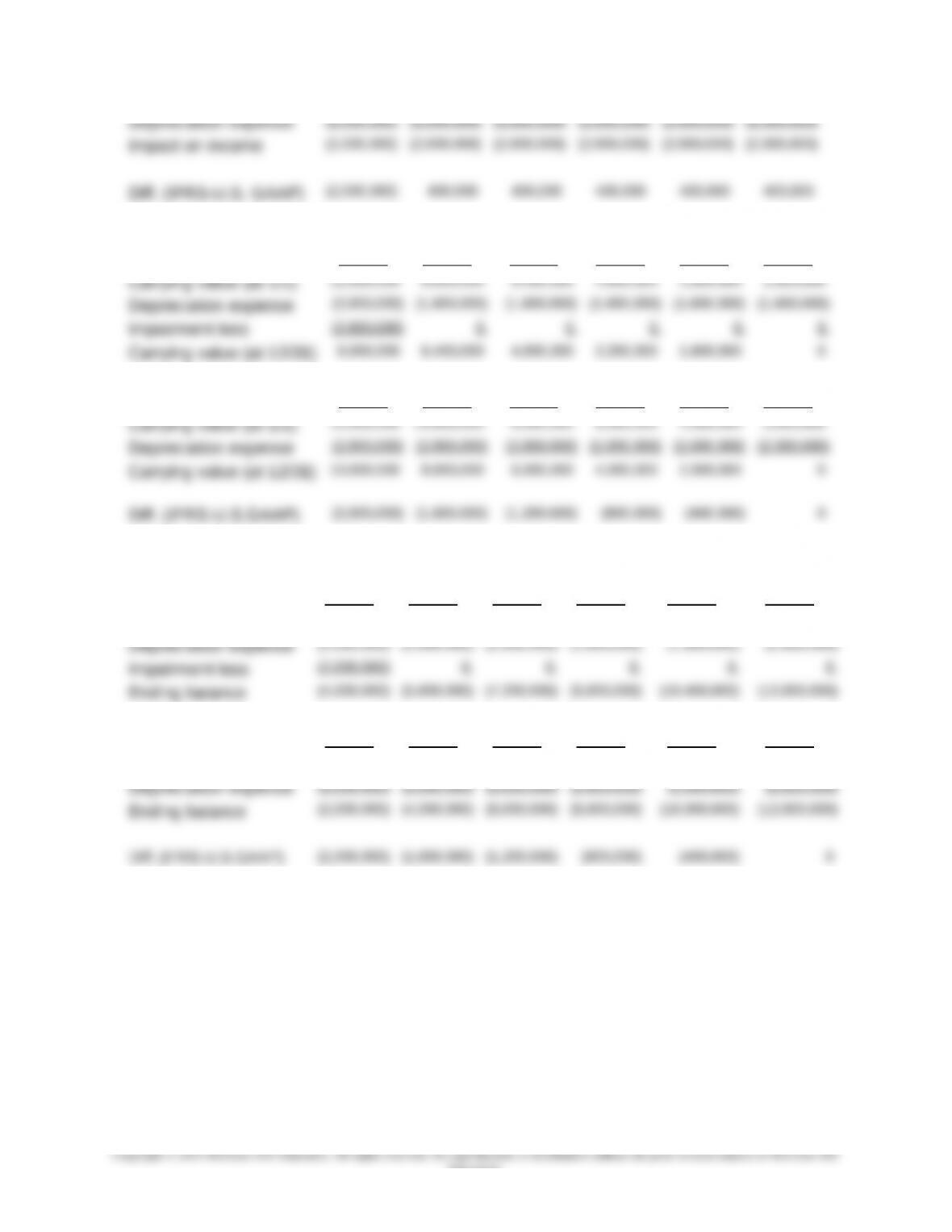

22. Madison Company – Property, Plant and Equipment (impairment)

IFRS U.S. GAAP

a. (1) IFRS:

b. Income before tax

IFRS Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

U.S. GAAP Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

4-10

Education.

Chapter 04 – International Financial Reporting Standards: Part I

Total Assets

IFRS Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

U.S. GAAP Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Total Stockholders’ Equity (ignoring income taxes)

IFRS Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Beginning balance 0 (4,000,000) (5,600,000) (7,200,000) (8,800,000) (10,400,000)

U.S. GAAP Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Beginning balance 0 (2,000,000) (4,000,000) (6,000,000) (8,000,000) (10,000,000)

4-11

Education.