Chapter 04 – International Financial Reporting Standards: Part I

36. Atlanta Tours Company – Leases (classification)

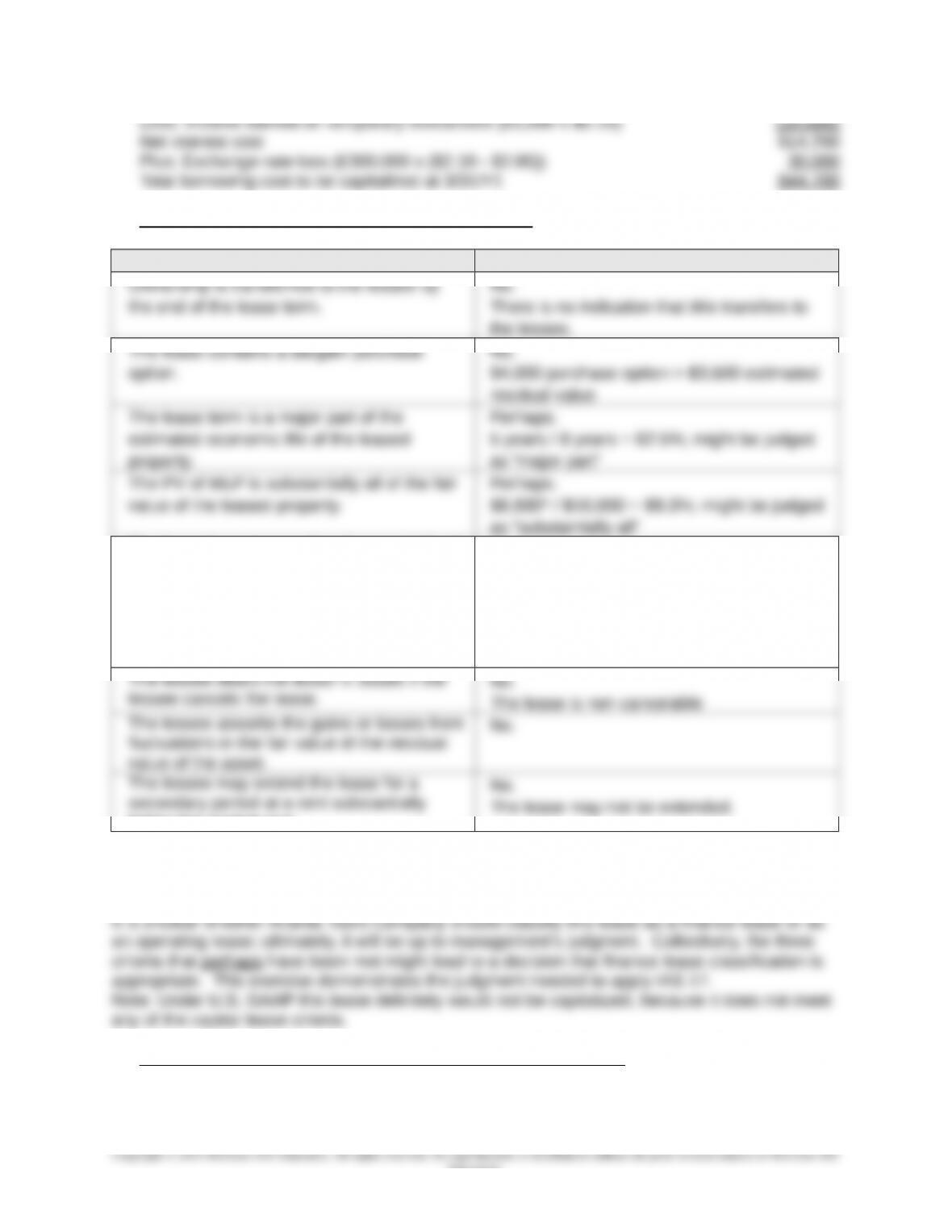

Finance Lease Criteria Criterion met?

The leased assets are of such a specialized

nature such that only the lessee can use

them without major modifications being

made.

Perhaps.

Duck Boats Inc. probably would need to

remove the wood carving to be able to sell or

lease the vehicle to another customer. It is

unclear whether this would be considered a

major modification.

below the market rent.

* Calculation of PV of MLP

Present value factor for annuity due, 5 payments, 6% = 4.4651: $2,000 x 4.4651 = $8,930

37. Fields Company – Sale-and-Leaseback (recognition of gain)

Part A.

4-1

Education.

Chapter 04 – International Financial Reporting Standards: Part I

Part B.

Part C.

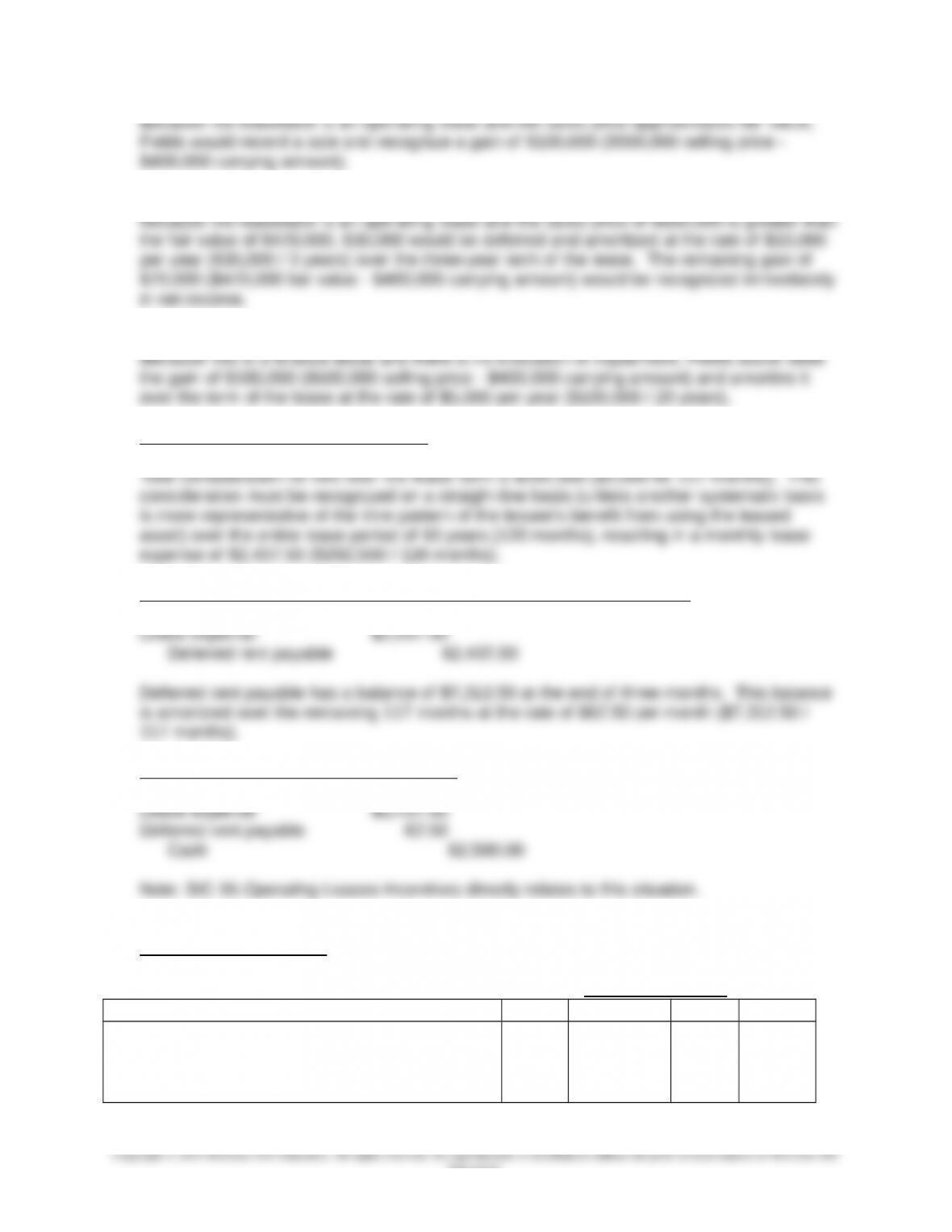

38. Bridget’s Bakery – Operating Lease

Monthly journal entry for each of the first three months of the lease:

Journal entry in months 4 through 120:

39. Acceptable Treatments

Acceptable under

IFRS U.S. GAAP Both Neither

A company takes out a loan to finance the

construction of a building that will be used by

the company. The interest on the loan is

capitalized as part of the cost of the building.

X

4-2

Education.

Chapter 04 – International Financial Reporting Standards: Part I

CASE 4-1 Bessrawl Corporation

Reconciliation from U.S. GAAP to IFRS

2014

Income under U.S. GAAP

$1,000,0

00

Adjustments:

4-3

Education.

Chapter 04 – International Financial Reporting Standards: Part I

Income under IFRS $1,030,000

2014

Stockholders’ equity under U.S. GAAP

$8,000,0

00

Adjustments:

Stockholders’ equity under IFRS $8,720,000

Explanation of Adjustments

Equipment. Under U.S. GAAP, the company reports depreciation expense of $100,000

[($2,750,000 – $250,000) / 25 years] in 2013 and in 2014.

4-4

Education.

Chapter 04 – International Financial Reporting Standards: Part I

Intangible Assets. Under U.S. GAAP, an asset is impaired when its carrying amount exceeds

the undiscounted future cash flows expected to arise from continued use of the asset. The

brand acquired in 2011 has a carrying amount of $40,000 and future expected cash flows are

$42,000, so it is not impaired under U.S. GAAP.

Research and Development Costs. Under U.S. GAAP, research and development expense in

the amount of $200,000 would be recognized in determining 2014 income.

Under IAS 38, $120,000 (60% x $200,000) of research and development costs would be

expensed in 2014, and $80,000 (40% x $200,000) of development costs would be capitalized as

an intangible asset (deferred development costs).

Sale and Leaseback. Under U.S. GAAP, the gain on the sale and leaseback (operating lease)

4-5

Education.