Chapter 01 – Introduction to International Accounting

1. In 2011, companies worldwide exported over $18.3 trillion worth of merchandise. Although

international trade has existed for thousands of years, recent growth in trade has been

phenomenal. Over the period 1996-2011, U.S. exports increased from $625 billion to

$1,480 billion per year, a 137% increase. During the same period, Chinese exports

2. Companies engaged in international trade with imports and exports denominated in foreign

currencies are faced with the accounting issue of translating foreign currency amounts into

the company’s reporting currency and reporting the effects of changes in exchange rates in

the financial statements.

3. As listed in Exhibit 1-1, following are several reasons why companies might want to invest

overseas:

Increase sales and profits

Enter rapidly growing or emerging markets

Reduce costs

Gain an foothold in economic blocs

Protect domestic markets

Protect foreign markets

4. FDI is playing a larger and more important role in the world economy. Global sales of

foreign affiliates were about 1.5 times as high as global exports in 2011, compared to almost

parity about three decades earlier. Global sales of foreign affiliates comprises about one

5. Financial reporting issues that result from foreign direct investment are (a) conversion of

foreign GAAP to parent company GAAP and (b) translation of foreign currency to parent

company reporting currency to prepare consolidated financial statements. In addition,

6. Two major taxation issues related to a foreign direct investment are (a) taxation of the

investee’s income by the host country in which the investment is located and (b) taxation of

the investee’s income by the investor’s home country. Companies with foreign direct

investments need to develop an expertise in the host country’s income tax rules so as to

minimize the amount of taxes paid to the host country, as well as in the home country’s tax

7. Companies must make several decisions in designing the system for evaluating the

performance of foreign operations. Two of these are (a) deciding whether to evaluate

performance on the basis of foreign currency or parent company reporting currency and (b)

deciding whether to factor out of the performance measure those items over which the

foreign operation’s managers have no control.

8. Two reasons to have stock listed on the stock exchange of a foreign country are (a) to

obtain capital in that country, perhaps at a more reasonable cost than is available at home,

and (b) to have an “acquisition currency” for acquiring firms in that country through stock

swaps.

9. The United Nations measures the multinationality of companies based on the average of

three factors: the ratio of foreign sales to total sales, the ratio of foreign assets to total

assets, and the ratio of foreign employees to total employees. Information about foreign

sales, foreign assets, and the number of foreign employees might be provided in a

company’s annual report or other publications through which a company provides

information to the public.

10. A single set of accounting standards used worldwide would have the following benefits for

multinational corporations:

Reduce the cost of preparing consolidated financial statements

Reduce the cost of gaining access to capital in foreign countries

Facilitate the analysis and comparison of financial statements of competitors and

potential acquisitions

1. Sony uses the following procedures to translate the foreign currency financial statements of

its foreign subsidiaries into Japanese yen:

All assets and liabilities are translated at the year-end exchange rate

All income and expense accounts are translated at the exchange rate prevailing on the

transaction date

The resulting translation adjustment is included in accumulated other comprehensive

income (stockholders’ equity)

[Students familiar with U.S. GAAP will recognize this approach as being procedures required

by FASB Statement No. 52 for foreign subsidiaries with a foreign currency as their functional

currency.]

2. Sony has intercompany transactions that result in one affiliate paying foreign currency to (or

receiving foreign currency from) another affiliate. The company uses foreign exchange

forward contracts and foreign currency option contracts to fix the local currency value of the

foreign currency that will be paid to (or received from) the affiliate. Sony does this for

transactions that have already occurred (receivables and payables), as well as for

transactions that are expected to occur (forecasted). For example, assume that Sony

Mexico purchases goods from the parent company in Japan on February 1 with payment of

50 million Japanese yen to be made on March 31. Sony Mexico could enter into a two-

month forward contract on February 1 that fixes the number of Mexican pesos it will need to

pay to acquire 50 million Japanese yen on March 31. Alternatively, Sony Mexico could

purchase a foreign currency option on February 1 that expires on March 31 that would give

the company the option to purchase yen on that date at a predetermined price.

In addition, Sony uses forward contracts to fix the amount of local currency it will need to

expend to be able to repay foreign currency loans (debt). For example, assume Sony has a

loan of 10 million Swiss francs that comes in six months, and the company is concerned that

1-2

Education.

3. a. The BRL pre-tax income becomes a USD pre-tax loss because Sales and Expenses are

translated at different exchange rates. Specifically, Sales are translated at an exchange

rate of USD0.30/BRL and Expenses are translated at an exchange rate of

USD0.347368/BRL.

b. The question is whether Acme Brush should use BRL income or USD income to

evaluate Cooper Grant’s performance. There is no unequivocally correct answer to this

question. Issues that might be discussed include:

What is the Brazilian subsidiary’s objective? To generate profits that can be

distributed to U.S. stockholders?

Does Cooper Grant have the ability to “control” USD income?

4. The New York Stock Exchange (NYSE) provides a PDF file titled “Current List of All Non-

U.S. Listed Issuers” on its website under Investor Relations > Financial. This document can

be accessed either by using a web browser to search for “NYSE List of Non-U.S. Listed

Issuers” or by searching for “List of Non-U.S. Listed Issuers” within the NYSE website

(www.nyse.com).

Note: The answers to a. and b. provided below were as of December 31, 2012. The

instructor should update these answers to the current date.

a. A total of 525 non-U.S. companies representing 46 different countries were listed on the

NYSE, NYSE MKT exchanges.

b. On December 31, 2012, the foreign countries with the most companies listed on the

NYSE were: Canada (157); China (82); Brazil (26); U.K. (29); and Bermuda (19).

c. Companies in Canada, China, Brazil, and Bermuda probably have listed on the NYSE to

tap into the much larger U.S. capital market. The reasons for U.K. companies to list on

the NYSE are less clear. One reason a foreign company might want to list its shares in

the United States is to enhance the company’s ability to acquire U.S. companies through

an exchange of shares of stock. U.S. stockholders are more likely to trade in their

shares of stock in a U.S. company in exchange for shares of a foreign company if that

foreign company’s shares are traded on a U.S. stock exchange.

5. The London Stock Exchange (LSE) provides an Excel file containing a list of all companies

listed on the exchange on its website (www.londonstockexchange.com). In 2013, this could

be found by searching for “List of All Companies” in the LSE website.

Note: The answers below come from an Excel spreadsheet “All Companies on the

London Stock Exchange – At 31 December 2012.” The instructor should update these

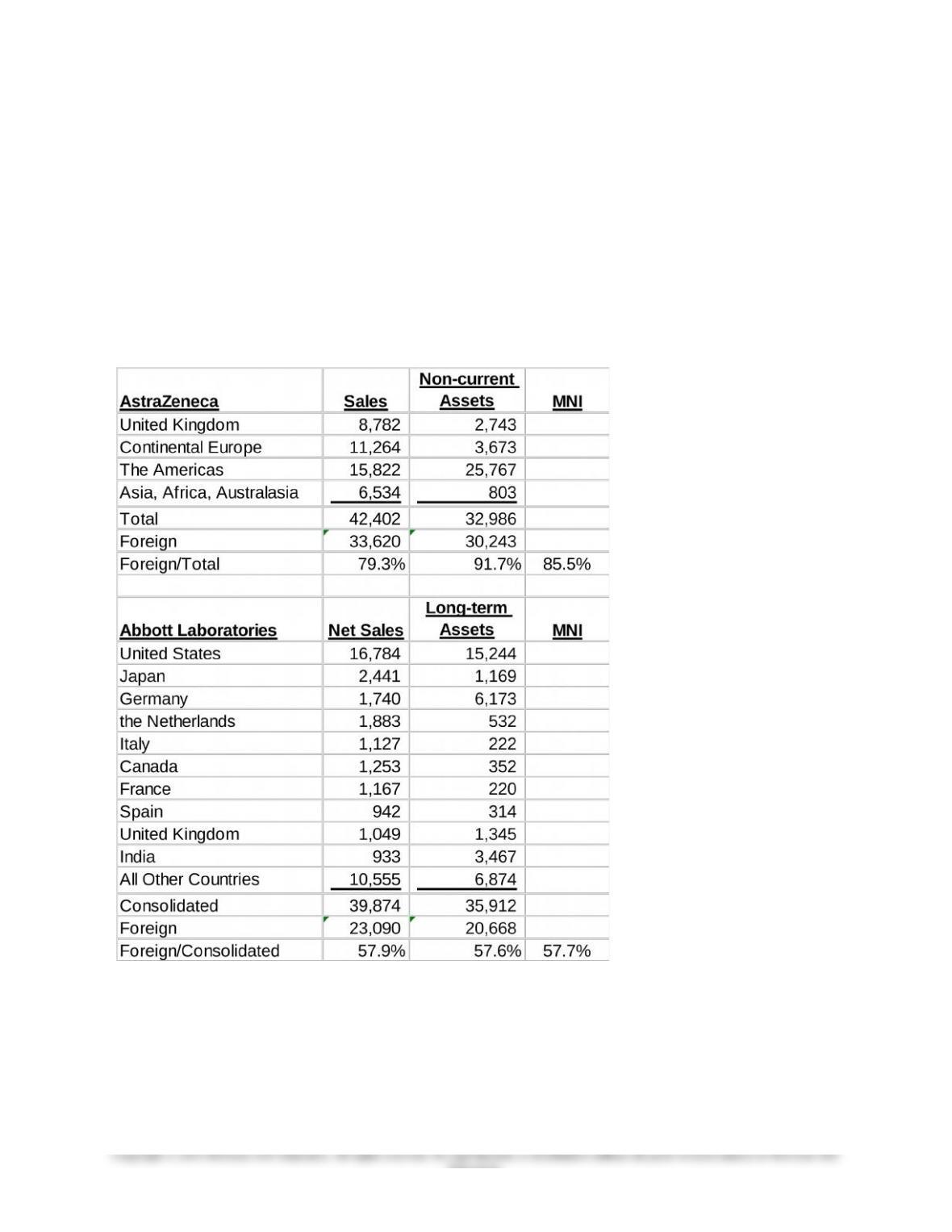

6. Based on the geographical distribution of Revenues (Net Sales) and Non-current (Long-

term) Assets, AstraZeneca has a multinationality index (MNI) of 0.86 and Abbott Labs has a

multinationality index of 0.58.

1-4

Education.

1. International Trade: Imports from Czech Republic; exports to China

Translation of foreign currency payables and receivable resulting from import and export

transactions.

2. Foreign direct investment in China

Conversion of BB Pijio’s profit from Chinese GAAP to German GAAP.

3. Pricing of intercompany sales made by Besserbrau (Germany) to BB Pijio (China)

Compliance with German and Chinese transfer pricing regulations.

4. Cross-listing on London Stock Exchange

Compliance with London Stock Exchange financial reporting requirements.

1. Individual investors can diversify the risk associated with investing in companies in only one

country by investing in mutual funds that invest in the stock of foreign companies.

2. According to information provided in the fund’s prospectus, the International Growth Fund is

subject to:

Investment style risk, which is the chance that returns from the types of stocks in which it

invests will trail returns from the overall stock market.

3. The Plain Talk About International Investing box discusses the fact that because foreign

companies are not subject to the same accounting, auditing, and financial reporting

1-5

Education.

4. The fund’s assets are distributed by region as follows: Europe (55%), Pacific (17%),

Emerging Markets (23%), North America (3.8%), and Middle East (1.3%). Other than North

America, this allocation might be affected by the number of firms listed on stock exchanges

in those regions; relative risks – country and currency – across regions; relative growth

potentials across regions; and/or differences in the quality and quantity of information

5. The fund is most heavily invested in the U.K. (20%), Japan (8.9%), China (8.1%).

6. The fund is most heavily invested in the following sectors: financials, consumer

discretionary, and industrials. These industries might be the most profitable or have the

highest growth potential. As a regulated industry, financials might be perceived as providing

more reliable information for making investment decisions than other sectors.