Archives: Solution Manual

978-0078025426 Chapter 10 Part 5

Case 10–26 (30 minutes) It is difficult to imagine how Lance Prating could ethically agree to go along with reporting the favorable $6,000 variance for industrial engineering on the final report, even if the bill were not actually received by […]

978-0078025426 Chapter 10 Part 4

Problem 10–23 (45 minutes) 1. The cost reports are of little use for assessing how well costs were controlled. The problem is that the company is comparing budgeted costs at one level of activity to actual costs at another level […]

978-0078025426 Chapter 10 Part 3

Exercise 10–17 (20 minutes) Gelato Supremo Revenue and Spending Variances For the Month Ended July 31 Flexible Budget Actual Results Revenue and Spending Variances Liters (q) ………………………………. 4,900 4,900 Revenue ($13.50q) …………………. $66,150 $69,420 $3,270 F Expenses: Raw materials ($5.10q) […]

978-0078025426 Chapter 10 Part 2

Exercise 10-9 (15 minutes) Auto Lavage Planning Budget For the Month Ended October 31 Budgeted cars washed (q) ……………………….. 8,000 Revenue ($5.90q) ………………………………….. $47,200 Expenses: Cleaning supplies ($0.70q) …………………….. 5,600 Electricity ($1,400 + $0.10q) …………………. 2,200 Maintenance ($0.30q)…………………………… 2,400 Wages […]

978-0078025426 Chapter 10 Part 1

Chapter 10 Flexible Budgets and Performance Analysis Solutions to Questions 10-1 The planning budget is prepared for the planned level of activity. It is static because it is not adjusted even if the level of activity subsequently changes. activity variance […]

978-0078025426 Chapter 9 Part 6

Problem 9-27 (continued) 6. Balance sheet: Nordic Company Balance Sheet June 30 Assets Current assets: Cash (Part 4) ……………………………………………………….. $ 8,400 Accounts receivable (80% × $90,000) ……………………….. 72,000 Inventory (Part 2) …………………………………………………. 9,000 Total current assets …………………………………………………. 89,400 Buildings and […]

978-0078025426 Chapter 9 Part 5

Problem 9-26 (120 minutes) 1. Schedule of expected cash collections: January February March Quarter Cash sales ……………………… $28,000 $32,000 $34,000 $ 94,000 Credit sales* ………………….. 36,000 42,000 48,000 126,000 Total collections ………………. $64,000 $74,000 $82,000 $220,000 *60% of the preceding […]

978-0078025426 Chapter 9 Part 4

Problem 9-21 (continued) 2. Cash budget: Month July August Sept. Quarter Cash balance, beginning … $ 43,000 $ 28,700 $ 24,300 $ 43,000 Add receipts: Collections from customers ……………… 290,700 355,600 391,000 1,037,300 Total cash available ………. 333,700 384,300 415,300 […]

978-0078025426 Chapter 9 Part 3

Problem 9-16 (30 minutes) 1. September cash sales ………………………………………. $ 7,400 September collections on account: July sales: $20,000 × 18% ……………………………… 3,600 August sales: $30,000 × 70% …………………………. 21,000 September sales: $40,000 × 10% ……………………. 4,000 Total cash collections ……………………………………….. […]

978-0078025426 Chapter 9 Part 2

Exercise 9-9 (20 minutes) Academic Copy Budgeted Balance Sheet Assets Current assets: Cash* ………………………………………… $ 4,400 Accounts receivable ………………………. 6,500 Supplies inventory …………….………….. 2,100 Total current assets ………………………… $13,000 Plant and equipment: Equipment ………………………………….. 28,000 Accumulated depreciation ..…………….. (9,000) Plant […]

978-0078025426 Chapter 9 Part 1

Chapter 9 Profit Planning Solutions to Questions 9-1 A budget is a detailed quantitative plan for the acquisition and use of financial and other resources over a given time period. Budgetary control involves using budgets to increase the budget is […]

978-0078025426 Chapter 8 Part 6

Appendix 8A The Concept of Present Value Exercise 8A-1 (10 minutes) a. From Exhibit 8B–1, the present value factor for 8% for three periods is 0.794. Therefore, the present value of the investment in the garage is $317,600 (=$400,000 × […]

978-0078025426 Chapter 8 Part 5

Problem 8–31 (45 minutes) 1. A net present value computation for each investment follows: Item Year(s) Amount of Cash Flows 20% Factor Present Value of Cash Flows Common stock: Purchase of the stock …….. Now $(80,000) 1.000 $(80,000) Sale of […]

978-0078025426 Chapter 8 Part 4

Problem 8–26 (continued) 4. The formula for the internal rate of return is: Investment required Factor of the internal = rate of return Net annual cash inflow €480,000 = = 4.4 (rounded) €108,000 Looking at Exhibit 8B-2 in Appendix 8B, […]

978-0078025426 Chapter 8 Part 3

Problem 8–19 (30 minutes) 1. The annual net cost savings is computed as follows: Reduction in labor costs ……………………………….. $240,000 Reduction in material costs …………………………… 96,000 Total cost reductions …………………………………… 336,000 Less increased maintenance costs ($4,250 × 12) . 51,000 […]

978-0078025426 Chapter 8 Part 2

Exercise 8-9 (30 minutes) 1. Item Year(s) Amount of Cash Flows 15% Factor Present Value of Cash Flows Initial investment ….. Now $(40,350) 1.000 $(40,350) Annual cash inflows .. 1-4 $15,000 2.855 42,825 Net present value ….. $ 2,475 Yes, […]

978-0078025426 Chapter 8 Part 1

Chapter 8 Capital Budgeting Decisions Solutions to Questions 8-1 A capital budgeting screening decision is concerned with whether a proposed investment project passes a preset hurdle, such as a 15% rate of return. A capital budgeting preference interest paid on […]

978-0078025426 Chapter 7 Part 7

Case 7-30 (continued) 4. Factors that should be considered by Mobile Seating Corporation before making a decision include: a. Alternative uses of the building and equipment. b. Any tax implications. c. The outside supplier’s prices in future years. d. The […]

978-0078025426 Chapter 7 Part 6

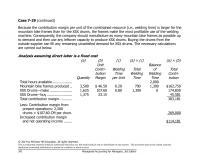

Case 7-29 (continued) Because the contribution margin per unit of the constrained resource (i.e., welding time) is larger for the mountain bike frames than for the XSX drums, the frames make the most profitable use of the welding machine. Consequently, […]

978-0078025426 Chapter 7 Part 5

Problem 7-25 (continued) 3. Other factors that the company should consider include: a. Will volume in future years increase, or will it remain constant at 40,000 units per year? (If volume increases, then renting the new equipment becomes more desirable, […]

978-0078025426 Chapter 7 Part 4

Problem 7–22 (60 minutes) 1. The fixed overhead costs are common and will remain the same regardless of whether the cartridges are produced internally or purchased outside. Hence, they are not relevant. The variable manufacturing overhead cost per box of […]

978-0078025426 Chapter 7 Part 3

Exercise 7–16 (15 minutes) Relevant Costs Item Make Buy Direct materials (60,000 @ $4.00) …………. $240,000 Direct labor (60,000 @ $2.75) ………………. 165,000 Variable manufacturing overhead (60,000 @ $0.50) …………………………….. 30,000 Fixed manufacturing overhead, traceable (1/3 of $180,000) …………………………….. 60,000 […]

978-0078025426 Chapter 7 Part 2

Exercise 7-7 (10 minutes) Product X Product Y Product Z Sales value after further processing .. $80,000 $150,000 $75,000 Sales value at split-off point …………. 50,000 90,000 60,000 Incremental revenue …………………… 30,000 60,000 15,000 Cost of further processing ……………. 35,000 […]

978-0078025426 Chapter 7 Part 1

Chapter 7 Differential Analysis: The Key to Decision Making Solutions to Questions 7-1 A relevant cost is a cost that differs in total between the alternatives in a decision. 7-2 An incremental cost (or benefit) is the the fixed costs […]

978-0078025426 Chapter 6 Part 5

Exercise 6A-3 (30 minutes) Supporting Direct Labor Batch Processing Order Processing Customer Service Total Total activity for the order ………………….. 1,920 4 1 1 direct labor- hours* batches order customer Manufacturing overhead: Indirect labor ………………………………… $ 3,456 $288 $ 18 […]

978-0078025426 Chapter 6 Part 4

Problem 6-18 (continued) The traditional and activity-based cost assignments differ for two reasons. First, the traditional system assigns all $2,200,000 of manufacturing overhead to products. The ABC system assigns only $2,127,500 of manufacturing overhead to products. The ABC system does […]

978-0078025426 Chapter 6 Part 3

Exercise 6-15 (30 minutes) 1. The first step is to determine the activity rates: Activity Cost Pools (a) Total Cost (b) Total Activity (a) ÷ (b) Activity Rate Serving parties ……. $12,000 5,000 parties $2.40 per party Serving diners …….. […]

978-0078025426 Chapter 6 Part 2

Exercise 6-9 (30 minutes) 1. Total revenue received: City General County General Cost of goods sold to the hospital (a) ……….. $30,000 $30,000 Markup percentage ………………………………. × 5% × 5% Markup in dollars (b) …………………………….. $1,500 $1,500 Revenue received from […]

978-0078025426 Chapter 6 Part 1

Chapter 6 Activity-Based Costing: A Tool to Aid Decision Making Solutions to Questions 6-1 Activity-based costing differs from traditional costing systems in a number of ways. In activity-based costing, nonmanufacturing as ABC system. Tapping the knowledge of cross– functional employees […]

978-0078025426 Chapter 5 Part 6

Case 5-27 (continued) 4 a. The unit product costs under absorption costing: Year 1 Year 2 Year 3 Direct materials ……………………………… $30 $30 $30.00 Direct labor …………………………………… 18 18 18.00 Variable manufacturing overhead ………. 6 6 6.00 Fixed manufacturing overhead […]

978-0078025426 Chapter 5 Part 5

Problem 5-25 (continued) 2. a. Year 1 Year 2 Year 3 Variable manufacturing cost …………. $ 4 $ 4 $ 4 Fixed manufacturing cost: $600,000 ÷ 50,000 units …………… 12 $600,000 ÷ 60,000 units …………… 10 $600,000 ÷ 40,000 units […]

978-0078025426 Chapter 5 Part 4

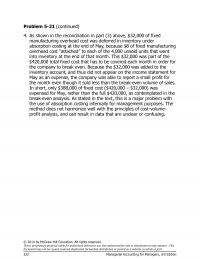

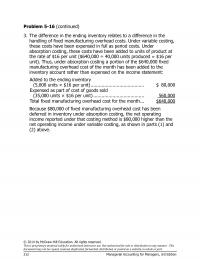

Problem 5-21 (continued) 4. As shown in the reconciliation in part (3) above, $32,000 of fixed manufacturing overhead cost was deferred in inventory under absorption costing at the end of May, because $8 of fixed manufacturing overhead cost “attached” to […]

978-0078025426 Chapter 5 Part 3

Problem 5-16 (continued) 3. The difference in the ending inventory relates to a difference in the handling of fixed manufacturing overhead costs. Under variable costing, these costs have been expensed in full as period costs. Under absorption costing, these costs […]

978-0078025426 Chapter 5 Part 2

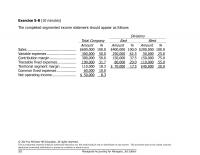

Exercise 5-8 (10 minutes) The completed segmented income statement should appear as follows: Divisions Total Company East West Amount % Amount % Amount % Sales ……………………………………….. $600,000 100.0 $400,000 100.0 $200,000 100.0 Variable expenses ………………………. 300,000 50.0 250,000 62.5 50,000 […]

978-0078025426 Chapter 5 Part 1

Chapter 5 Variable Costing and Segment Reporting: Tools for Management Solutions to Questions 5-1 Absorption and variable costing differ in how they handle fixed manufacturing overhead. Under absorption costing, fixed manufacturing the products? These costs are incurred to have the […]

978-0078025426 Chapter 4 Part 6

Exercise 4A-2 (30 minutes) 1. The overhead applied to Ms. Miyami’s account would be computed as follows: 2010 2011 Estimated overhead cost (a) ……………………….. $144,000 $144,000 Estimated professional staff hours (b) …………… 2,400 2,250 Predetermined overhead rate (a) ÷ (b) […]

978-0078025426 Chapter 4 Part 5

Case 4-25 (continued) However, use of a plantwide overhead rate in effect redistributes overhead costs proportionately between the three departments (at 160% of direct labor cost) and results in a large amount of overhead cost being charged to the Hastings […]

978-0078025426 Chapter 4 Part 4

Problem 4-20 (30 minutes) 1. The predetermined overhead rate was: Y = $1,275,000 + $3.00 per hour × 85,000 hours Estimated fixed manufacturing overhead ……………… $1,275,000 Estimated variable manufacturing overhead $3.00 per computer hour × 85,000 hours…………… 255,000 Estimated total […]

978-0078025426 Chapter 4 Part 3

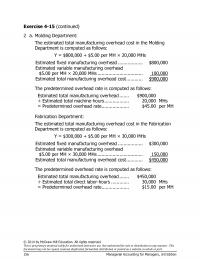

Exercise 4-15 (continued) 2 a. Molding Department: The estimated total manufacturing overhead cost in the Molding Department is computed as follows: Y = $800,000 + $5.00 per MH × 20,000 MHs Estimated fixed manufacturing overhead ……………… $800,000 Estimated variable manufacturing […]

978-0078025426 Chapter 4 Part 2

Exercise 4-8 (20 minutes) 1. The estimated total manufacturing overhead cost is computed as follows: Y = $750,000 + $4.00 per MH × 150,000 MHs Estimated fixed manufacturing overhead ……………. $ 750,000 Estimated variable manufacturing overhead $4.00 per MH × […]

978-0078025426 Chapter 4 Part 1

Chapter 4 Job-Order Costing Solutions to Questions 4-1 By definition, manufacturing overhead consists of costs that cannot be practically traced to products or jobs. Therefore, if these costs are to be assigned to products or jobs, they must be be […]

978-0078025426 Chapter 3 Part 8

Case 3-32 (75 minutes) 1. The contribution format income statements (in thousands of dollars) for the three alternatives are: 18% Commission 20% Commission Own Sales Force Sales …………………………………………. $30,000 100 % $30,000 100 % $30,000 100 % Variable expenses: Variable […]

978-0078025426 Chapter 3 Part 7

Problem 3-29 (75 minutes) 1. a. Selling price ………………… $37.50 100% Variable expenses ………… 22.50 60% Contribution margin ………. $15.00 40% Profit = Unit CM × Q − Fixed expenses $0 = $15 × Q − $480,000 $15Q = $480,000 […]

978-0078025426 Chapter 3 Part 6

Problem 3-26 (60 minutes) 1. The income statements would be: Present Amount Per Unit % Sales ………………………… $800,000 $20 100% Variable expenses ………… 560,000 14 70% Contribution margin ……… 240,000 $6 30% Fixed expenses ……………. 192,000 Net operating income …… […]

978-0078025426 Chapter 3 Part 5

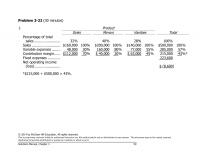

Problem 3-22 (30 minutes) 1. Product Sinks Mirrors Vanities Total Percentage of total sales ……………………. 32% 40% 28% 100% Sales ……………………… $160,000 100 % $200,000 100 % $140,000 100 % $500,000 100 % Variable expenses …….. 48,000 30 % 160,000 […]

978-0078025426 Chapter 3 Part 4

Problem 3-19 (60 minutes) 1. Profit = Unit CM × Q − Fixed expenses $0 = ($40 − $25) × Q − $300,000 $0 = ($15) × Q − $300,000 $15Q = $300,000 Q = $300,000 ÷ $15 per shirt […]

978-0078025426 Chapter 3 Part 3

Exercise 3-13 (30 minutes) 1. The contribution margin per person would be: Price per ticket ………………………………………….. $30 Variable expenses: Dinner …………………………………………………… $7 Favors and program …………………………………. 3 10 Contribution margin per person …………………….. $20 The fixed expenses of the Extravaganza […]

978-0078025426 Chapter 3 Part 2

Exercise 3-6 (10 minutes) 1. The equation method yields the required unit sales, Q, as follows: Profit = Unit CM × Q − Fixed expenses $6,000 = ($140 − $60) × Q − $40,000 $6,000 = ($80) × Q − […]

978-0078025426 Chapter 3 Part 1

Chapter 3 Cost-Volume-Profit Relationships Solutions to Questions 3-1 The contribution margin (CM) ratio is the ratio of the total contribution margin to total sales revenue. It is used in target profit and break-even analysis and can be used to quickly […]

978-0078025426 Chapter 2 Part 6

Problem 2A-4 (45 minutes) 1. a. Quarter Tons Mined (X) Utilities Cost (Y) Year 1: 1st 15,000 $50,000 2nd 11,000 $45,000 3rd 21,000 $60,000 4th 12,000 $75,000 Year 2: 1st 18,000 $100,000 2nd 25,000 $105,000 3rd 30,000 $85,000 4th 28,000 […]