Chapter 5

Variable Costing and Segment Reporting:

Tools for Management

Solutions to Questions

overhead is treated as a product cost and hence

is an asset until products are sold. Under

variable costing, fixed manufacturing overhead

5-2 Selling and administrative expenses are

treated as period costs under both variable

product costs, along with direct materials, direct

labor, and variable manufacturing overhead. If

sold, the fixed manufacturing overhead cost that

has been carried over with the units is included

costs with revenues than variable costing. They

argue that all manufacturing costs must be

assigned to products to properly match the costs

variable and fixed manufacturing costs for the

purposes of matching costs and revenues.

made or not, the total fixed manufacturing costs

will be exactly the same. Therefore, how can

one say that these costs are part of the costs of

that period as period costs according to the

matching principle.

production equals sales, inventories do not

increase or decrease and therefore under

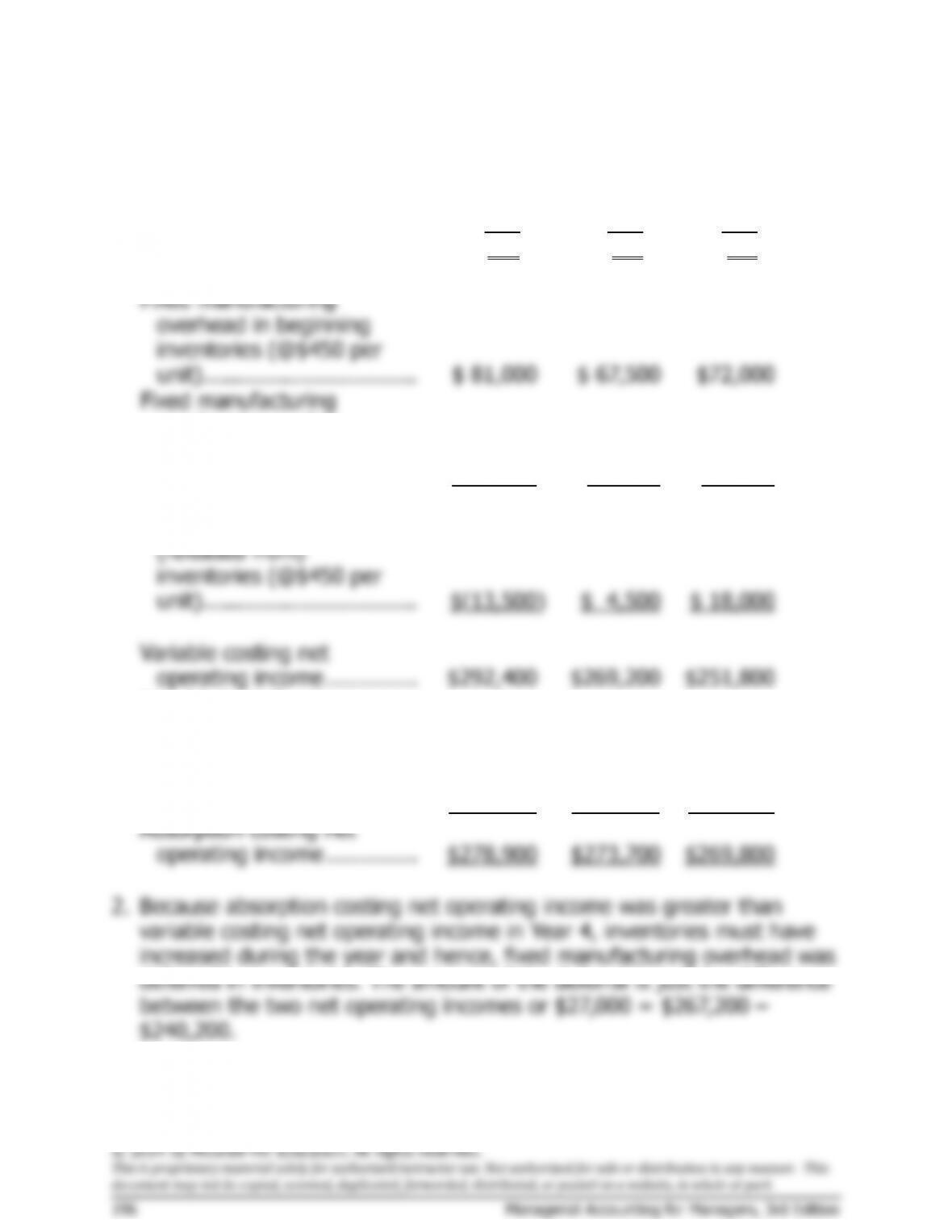

5-7 If production exceeds sales, absorption

costing will usually show higher net operating

manufacturing overhead cost of the current

period is deferred in inventory to the next

5-8 If fixed manufacturing overhead cost is

released from inventory, then inventory levels

5-9 Under absorption costing net operating

income can be increased by simply increasing

the level of production without any increase in

manufacturing overhead costs into the inventory

account, reducing the current period’s reported

© 2014 by McGraw-Hill Education. All rights reserved.

This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This

document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Solutions Manual, Chapter 5 193

income between absorption and variable costing

arise because of changing levels of inventory. In

lean production, goods are produced strictly to

customers’ orders. With production geared to

sales, inventories are largely (or entirely)

5-11 A segment is any part or activity of an

organization about which a manager seeks cost,

revenue, or profit data. Examples of segments

include departments, operations, sales

be avoided if the segment were eliminated).

Common costs are not allocated to segments

under the contribution approach.

5-13 A traceable cost of a segment is a cost

or in part to any one of the segments. If the

departments of a company are treated as

segments, then examples of the traceable costs

headquarters building, corporate image

advertising, and periodic depreciation of

machines shared by several departments.

5-14 The contribution margin is the difference

particularly those in which fixed costs don’t

change. The segment margin is useful in

assessing the overall profitability of a segment.

5-15 If common costs were allocated to

were eliminated because of the existence of

arbitrarily allocated common costs, the overall

profit of the company would decline and the

common cost that had been allocated to the

segment would be reallocated to the remaining

become common as that segment is divided into

smaller segment units. For example, the costs of

national TV and print advertising might be

Exercise 5-2 (20 minutes)

1. 2,000 units in ending inventory × R60 fixed manufacturing overhead per

unit = R120,000.

2. The variable costing income statement appears below:

Sales ………………………………………….

R4,000,000

Variable expenses:

Variable cost of goods sold

(8,000 units × R310 per unit) ……..

R2,480,000

Variable selling and administrative

(8,000 units × R20 per unit) ……….

160,000

2,640,000

Contribution margin ……………………….

1,360,000

Fixed expenses:

Fixed manufacturing overhead ……….

600,000

Fixed selling and administrative ……..

400,000

1,000,000

Net operating income …………………….

R 360,000

The difference in net operating income between variable and absorption

costing can be explained by the deferral of fixed manufacturing

overhead cost in inventory that has taken place under the absorption

costing approach. Note from part (1) that R120,000 of fixed

manufacturing overhead cost has been deferred in inventory to the next

period. Thus, net operating income under the absorption costing

approach is R120,000 higher than it is under variable costing.