Exercise 3-6 (10 minutes)

1. The equation method yields the required unit sales, Q, as follows:

Profit

= Unit CM × Q − Fixed expenses

$6,000

= ($140 − $60) × Q − $40,000

$6,000

= ($80) × Q − $40,000

$80 × Q

= $6,000 + $40,000

Q

= $46,000 ÷ $80

Q

= 575 units

Exercise 3-7 (continued)

4. The formula method also gives an answer that is identical to the

Exercise 3-9 (20 minutes)

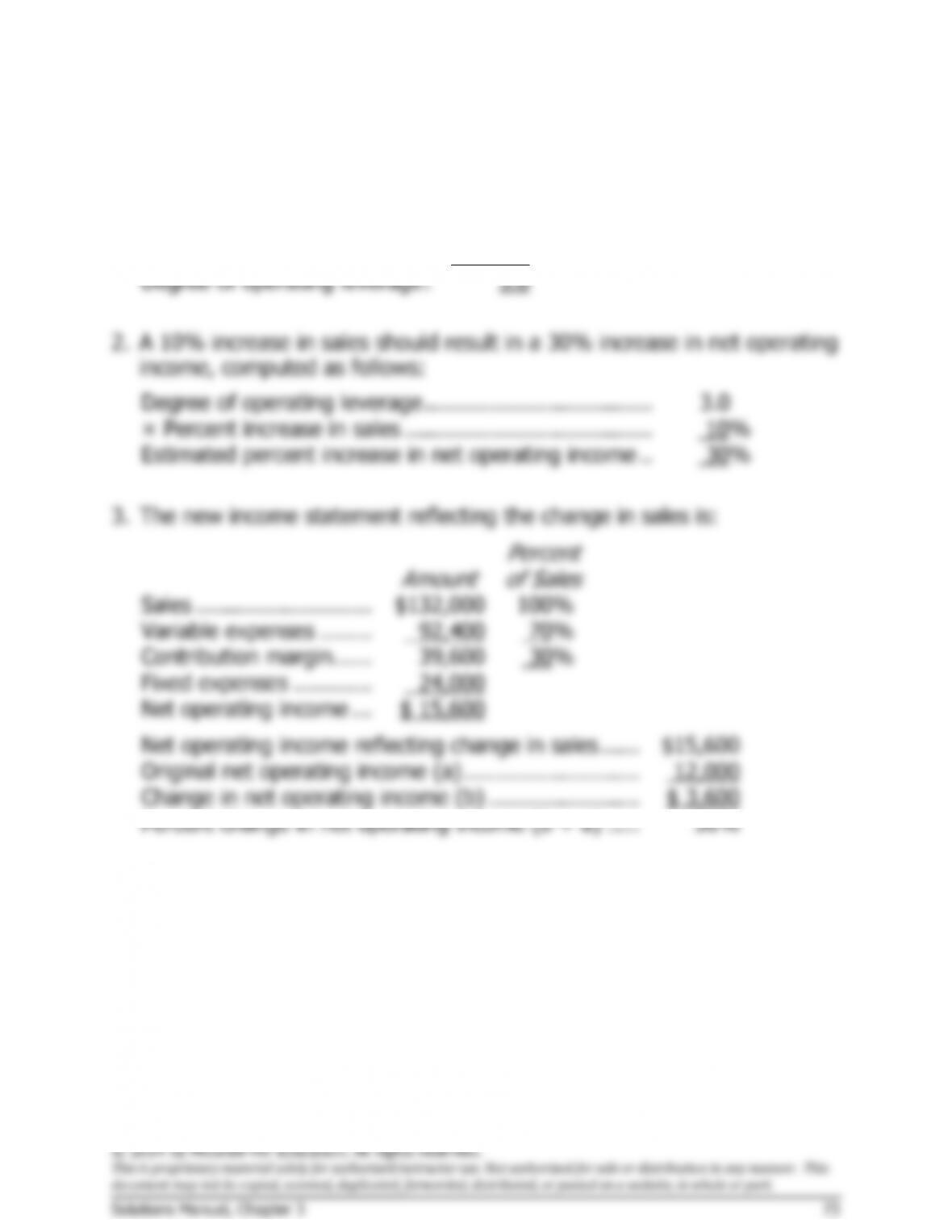

1. The company’s degree of operating leverage would be computed as

follows:

Contribution margin ……………

$36,000

÷ Net operating income ………

$12,000

Degree of operating leverage .

3.0

2. A 10% increase in sales should result in a 30% increase in net operating

income, computed as follows:

Degree of operating leverage ……………………………..

3.0

× Percent increase in sales …………………………..……

10%

Estimated percent increase in net operating income ..

30%

3. The new income statement reflecting the change in sales is:

Amount

Percent

of Sales

Sales …….………………..

$132,000

100%

Variable expenses ……..

92,400

70%

Contribution margin ……

39,600

30%

Fixed expenses …………

24,000

Net operating income …

$ 15,600

Net operating income reflecting change in sales ……

$15,600

Original net operating income (a) ………………………

12,000

Change in net operating income (b) …………………..

$ 3,600

Percent change in net operating income (b ÷ a) …..

30%

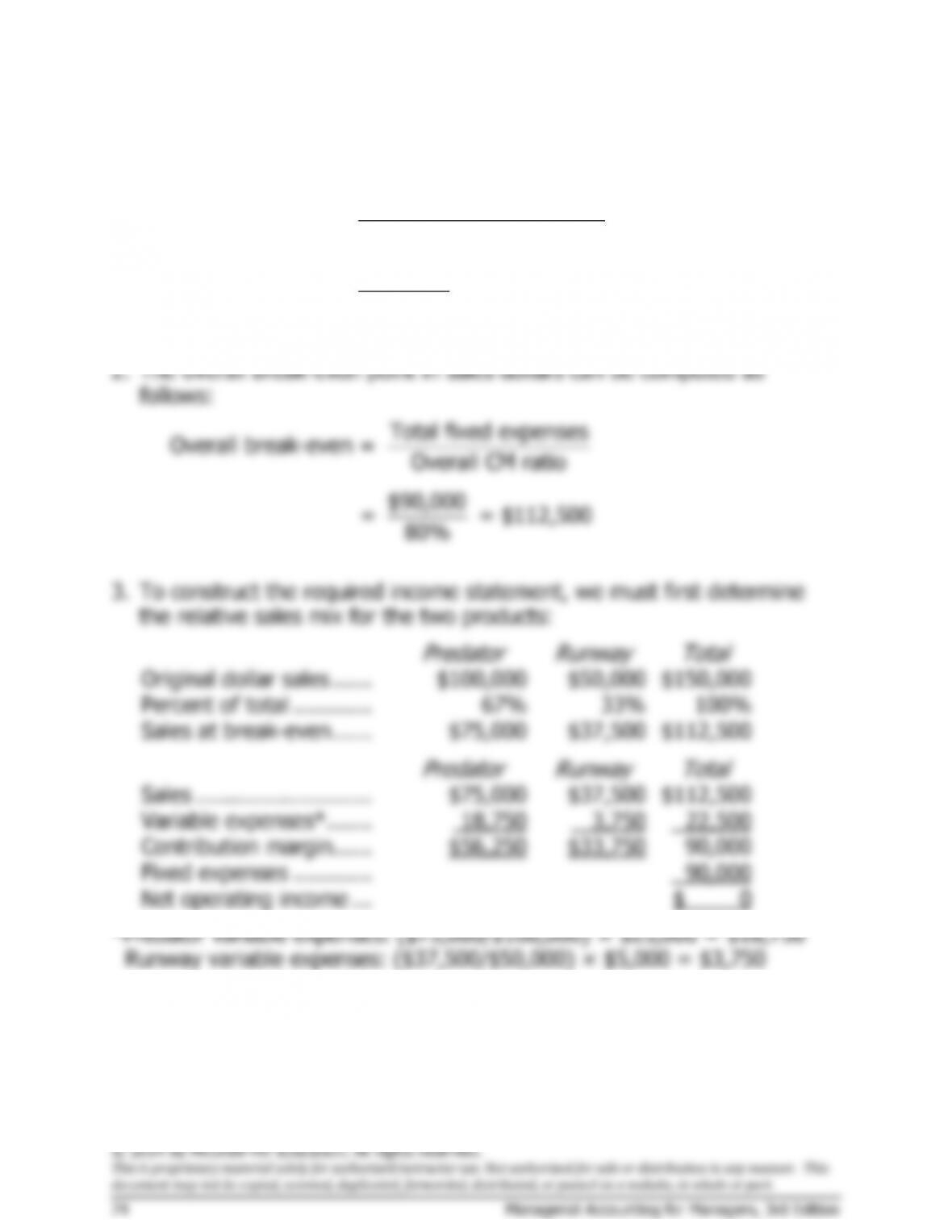

Exercise 3-11 (30 minutes)

1.

Profit

=

Unit CM × Q − Fixed expenses

$0

=

($40 − $28) × Q − $150,000

$0

=

($12) × Q − $150,000

$12Q

=

$150,000

Q

=

$150,000 ÷ $12 per unit

Q

=

12,500 units, or at $40 per unit, $500,000

Fixed expenses

Unit sales =

to break even Unit contribution margin

$150,000

= =12,500 units

$12 per unit

or, at $40 per unit, $500,000.

2. The contribution margin at the break-even point is $150,000 because at

Sales (14,000 units × $40 per unit) …………..

Exercise 3-11 (continued)

4. Margin of safety in dollar terms:

Margin of safety = Total sales – Break-even sales

in dollars

= $600,000 – $500,000 = $100,000

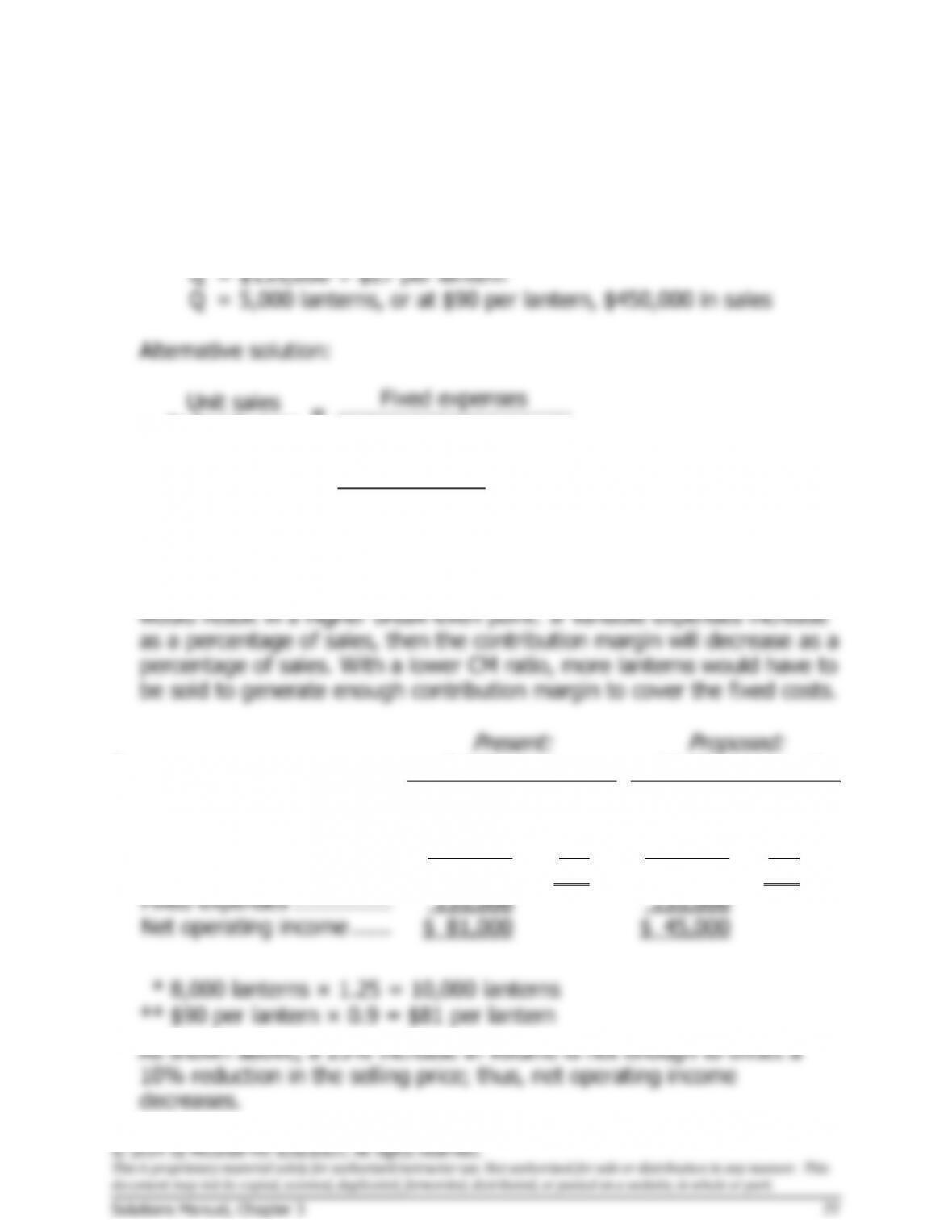

Exercise 3-12 (30 minutes)

1.

Profit

=

Unit CM × Q − Fixed expenses

$0

=

($90 − $63) × Q − $135,000

$0

=

($27) × Q − $135,000

$27Q

=

$135,000

Q

=

$135,000 ÷ $27 per lantern

Q

=

5,000 lanterns, or at $90 per lantern, $450,000 in sales

Fixed expenses

Unit sales =

to break even Unit contribution margin

$135,000

= = 5,000 lanterns,

$27 per lantern

or at $90 per lantern, $450,000 in sales

2. An increase in variable expenses as a percentage of the selling price

3.

Present:

8,000 Lanterns

Proposed:

10,000 Lanterns*

Total

Per Unit

Total

Per Unit

Sales …….…………………..

$720,000

$90

$810,000

$81

**

Variable expenses ………..

504,000

63

630,000

63

Contribution margin ………

216,000

$27

180,000

$18

Fixed expenses ……………

135,000

135,000

Net operating income ……

$ 81,000

$ 45,000

*

8,000 lanterns × 1.25 = 10,000 lanterns

**

$90 per lantern × 0.9 = $81 per lantern