Problem 3-19 (60 minutes)

1.

Profit

=

Unit CM × Q − Fixed expenses

$0

=

($40 − $25) × Q − $300,000

$0

=

($15) × Q − $300,000

$15Q

=

$300,000

Q

=

$300,000 ÷ $15 per shirt

Q

=

20,000 shirts

20,000 shirts × $40 per shirt = $800,000

Alternative solution:

Fixed expenses

Unit sales =

to break even Unit contribution margin

$300,000

= = 20,000 shirts

$15 per shirt

Fixed expenses

Dollar sales =

to break even CM ratio

$300,000

= = $800,000 in sales

0.375

Break-even sales ……………..

20,000 shirts

Actual sales …………………….

19,000 shirts

Sales short of break-even ….

1,000 shirts

1,000 shirts × $15 contribution margin per shirt = $15,000 loss

Alternative solution:

Sales (19,000 shirts × $40 per shirt) …………………….

Variable expenses (19,000 shirts × $25 per shirt) …….

475,000

Contribution margin …………………………………………..

285,000

Fixed expenses …………………………………………………

300,000

Net operating loss …………………………………………….

$(15,000)

Problem 3-19 (continued)

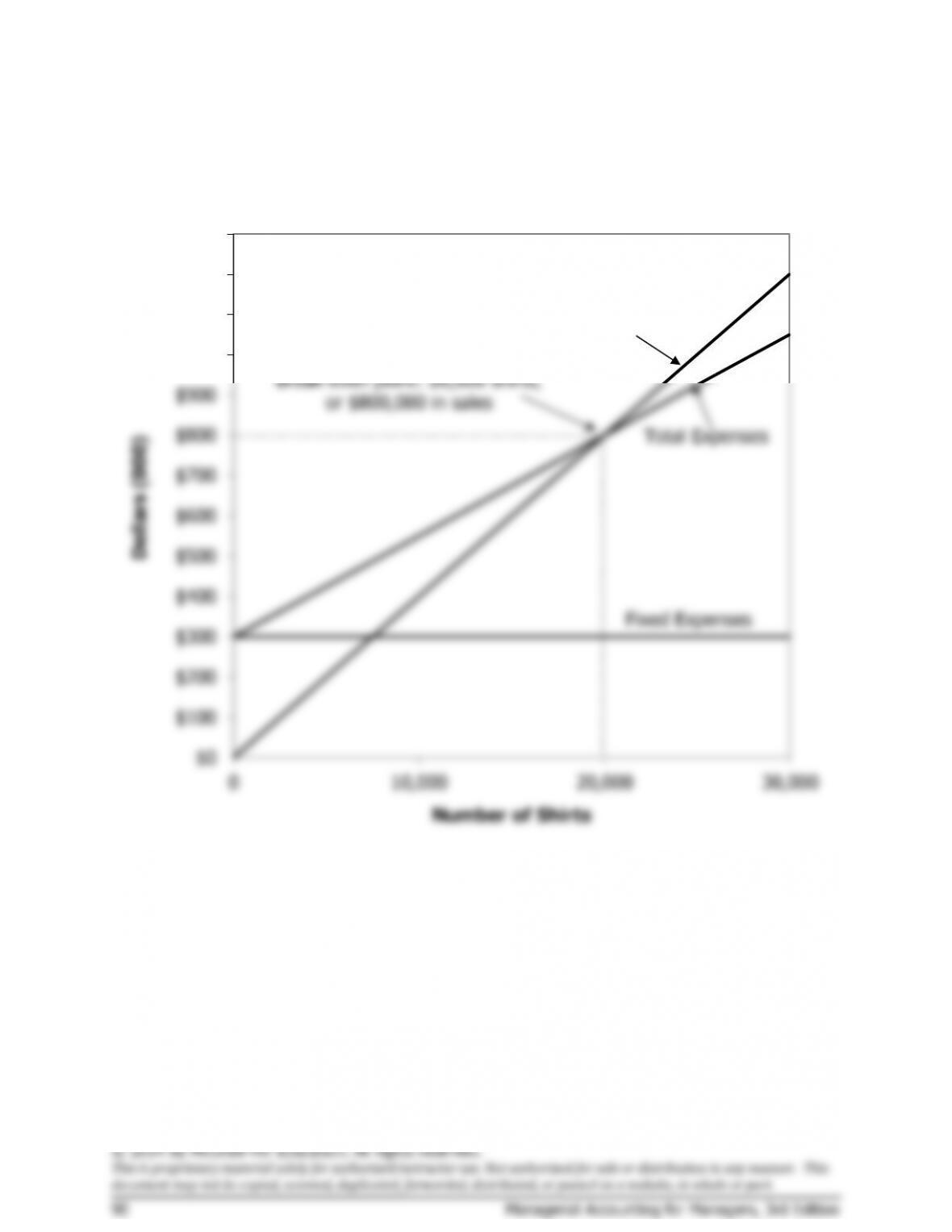

2. Cost-volume-profit graph:

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

$1,100

$1,200

$1,300

0 10,000 20,000 30,000

Dollars (000)

Number of Shirts

Break-even point: 20,000 shirts,

or $800,000 in sales

Fixed Expenses

Total Expenses

Total Sales

Problem 3-19 (continued)

4. The variable expenses will now be $28 ($25 + $3) per shirt, and the

contribution margin will be $12 ($40 – $28) per shirt.

Profit

=

Unit CM × Q − Fixed expenses

$0

=

($40 − $28) × Q − $300,000

$0

=

($12) × Q − $300,000

$12Q

=

$300,000

Q

=

$300,000 ÷ $12 per shirt

Q

=

25,000 shirts

25,000 shirts × $40 per shirt = $1,000,000 in sales

Alternative solution:

Fixed expenses

Unit sales =

to break even Unit contribution margin

$300,000

= = 25,000 shirts

$12 per shirt

Fixed expenses

Dollar sales =

to break even CM ratio

$300,000

= = $1,000,000 in sales

0.30

5. The simplest approach is:

Actual sales …………………………….

23,500 shirts

Break-even sales ……………………..

20,000 shirts

Excess over break-even sales ……..

3,500 shirts

3,500 shirts × $12 per shirt* = $42,000 profit

*$15 present contribution margin – $3 commission = $12 per shirt

Problem 3-20 (60 minutes)

1. The CM ratio is 30%.

Total

Per Unit

Percentage

Sales (13,500 units) ………

$270,000

$20

100%

Variable expenses …………

189,000

14

70%

Contribution margin ………

$ 81,000

$ 6

30%

The break-even point is:

Profit

=

Unit CM × Q − Fixed expenses

$0

=

($20 − $14) × Q − $90,000

$0

=

($6) × Q − $90,000

$6Q

=

$90,000

Q

=

$90,000 ÷ $6 per unit

Q

=

15,000 units

15,000 units × $20 per unit = $300,000 in sales

Alternative solution:

Fixed expenses

Unit sales =

to break even Unit contribution margin

$90,000

= = 15,000 units

$6 per unit

Fixed expenses

Dollar sales =

to break even CM ratio

$90,000

= = $300,000 in sales

0.30

2.

Incremental contribution margin:

$70,000 increased sales × 30% CM ratio ………..

$21,000

Less increased fixed costs:

Increase in monthly net operating income …………

month.

Problem 3-20 (continued)

The new break-even point would be:

Fixed expenses

Unit sales =

to break even Unit contribution margin

$208,000

= = 16,000 units

$13 per unit

Fixed expenses

Dollar sales =

to break even CM ratio

$208,000

= = $320,000 in sales

0.65

b. Comparative income statements follow:

Not Automated

Automated

Total

Per Unit

%

Total

Per Unit

%

Sales (20,000 units) ….

$400,000

$20

100

$400,000

$20

100

Variable expenses …….

280,000

14

70

140,000

7

35

Contribution margin ….

120,000

$ 6

30

260,000

$13

65

Fixed expenses ………..

90,000

208,000

Net operating income ..

$ 30,000

$ 52,000

Problem 3-20 (continued)

c. Whether or not one would recommend that the company automate

its operations depends on how much risk he or she is willing to take,

and depends heavily on prospects for future sales. The proposed

changes would increase the company’s fixed costs and its break-even

made.

The greatest risk of automating is that future sales may drop back

down to present levels (only 13,500 units per month), and as a

result, losses will be even larger than at present due to the

company’s greater fixed costs. (Note the problem states that sales

are erratic from month to month.) In sum, the proposed changes will

between the two alternatives in terms of units sold; i.e., the point

where profits will be the same under either alternative. At this point,

total revenue will be the same; hence, we include only costs in our

equation:

Let Q

=

Point of indifference in units sold

$14Q + $90,000

=

$7Q + $208,000

$7Q

=

$118,000

Q

=

$118,000 ÷ $7 per unit

Q

=

16,857 units (rounded)

If more than 16,857 units are sold, the proposed plan will

yield the greatest profit; if less than 16,857 units are sold, the present plan

will yield the greatest profit (or the least loss).

Problem 3-21 (60 minutes)

1. The CM ratio is 60%:

Selling price ………………….

$15

100%

Variable expenses …………..

6

40%

Contribution margin ………..

$ 9

60%

2.

Fixed expenses

Break-even point in=

total sales dollars CM ratio

$180,000

= =$300,000 sales

0.60

3. $45,000 increased sales × 60% CM ratio = $27,000 increase in

contribution margin. Since fixed costs will not change, net operating

income should also increase by $27,000.

4. a.

Contribution margin

Degree of operating leverage = Net operating income

$216,000

= = 6

$36,000

b. 6 × 15% = 90% increase in net operating income. In dollars, this

increase would be 90% × $36,000 = $32,400.