Problem 3-22 (30 minutes)

1.

Product

Sinks

Mirrors

Vanities

Total

Percentage of total

sales …………………….

32%

40%

28%

100%

Sales ………………………

$160,000

100

%

$200,000

100

%

$140,000

100

%

$500,000

100

%

Variable expenses ……..

48,000

30

%

160,000

80

%

77,000

55

%

285,000

57

%

Contribution margin ……

$112,000

70

%

$ 40,000

20

%

$ 63,000

45

%

215,000

43

%*

Fixed expenses …………

223,600

Net operating income

(loss) ……………………

$ (8,600)

*$215,000 ÷ $500,000 = 43%.

Problem 3-23 (45 minutes)

1.

a.

Alvaro

Bazan

Total

%

%

%

Sales ……………………..

€800

100

€480

100

€1,280

100

Variable expenses

480

60

96

20

576

45

Contribution margin ….

€320

40

€384

80

704

55

Fixed expenses ………..

660

Net operating income ..

€ 44

b.

Fixed expenses €660

Dollar sales to = = = €1,200

break even CM ratio 0.55

Margin of safety = Actual sales – Break-even sales

= €1,280 – €1,200 = €80

Margin of safety Margin of safety in euros

=

percentage Actual sales

€80

= = 6.25%

€1,280

Problem 3-23 (continued)

b.

Fixed expenses €660

Euro sales to = = = €1,347(rounded)

break even CM ratio 0.49

Margin of safety = Actual sales – Break-even sales

= €1,600 – €1,347 = €253

Margin of safety Margin of safety in euros

=

percentage Actual sales

€253

= = 15.81%

€1,600

3. The reason for the increase in the break-even point can be traced to the

decrease in the company’s average contribution margin ratio when the

third product is added. Note from the income statements above that this

ratio drops from 55% to 49% with the addition of the third product.

This product, called Cano, has a CM ratio of only 25%, which causes the

average contribution margin ratio to fall.

This problem shows the somewhat tenuous nature of break–even

analysis when more than one product is involved. The manager must be

very careful of his or her assumptions regarding sales mix when making

decisions such as adding or deleting products.

It should be pointed out to the president that even though the break-

even point is higher with the addition of the third product, the

company’s margin of safety is also greater. Notice that the margin of

Problem 3-24 (continued)

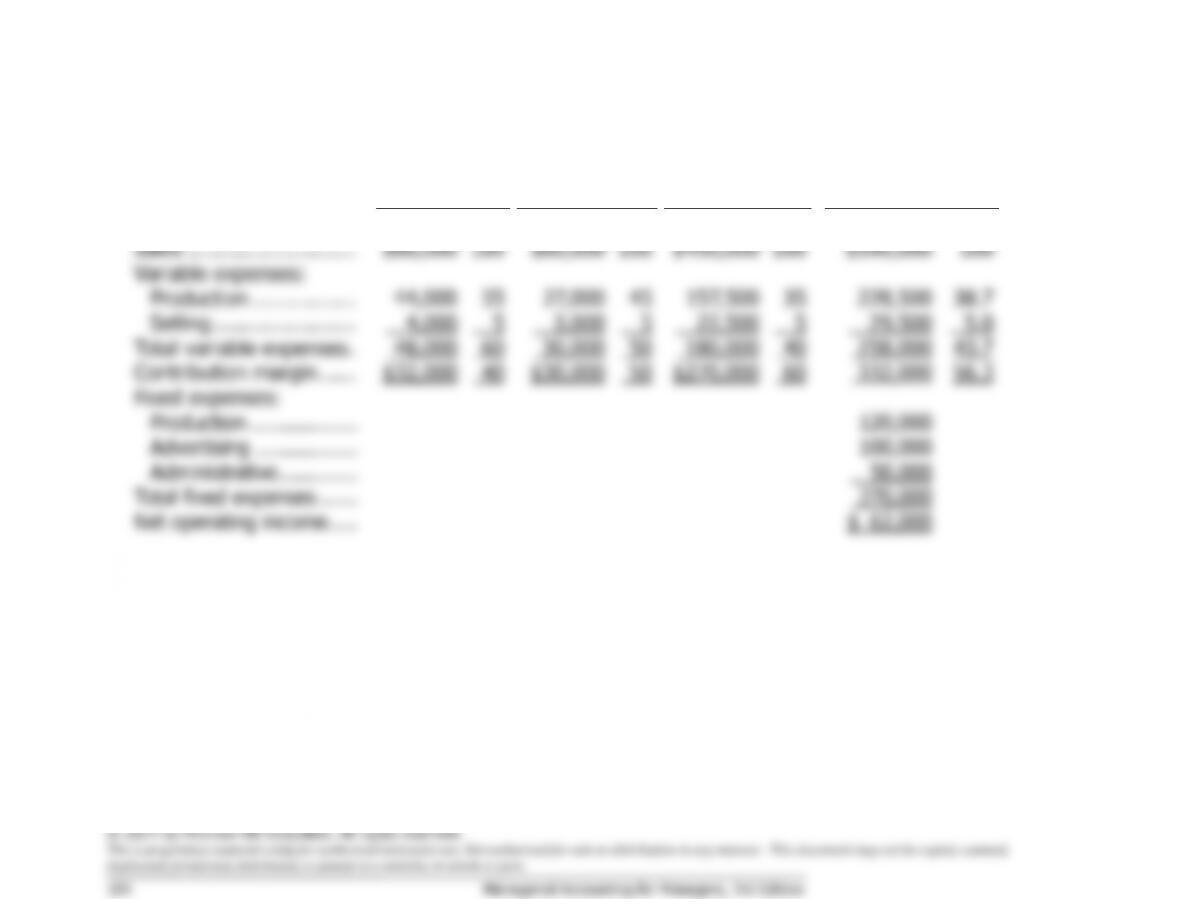

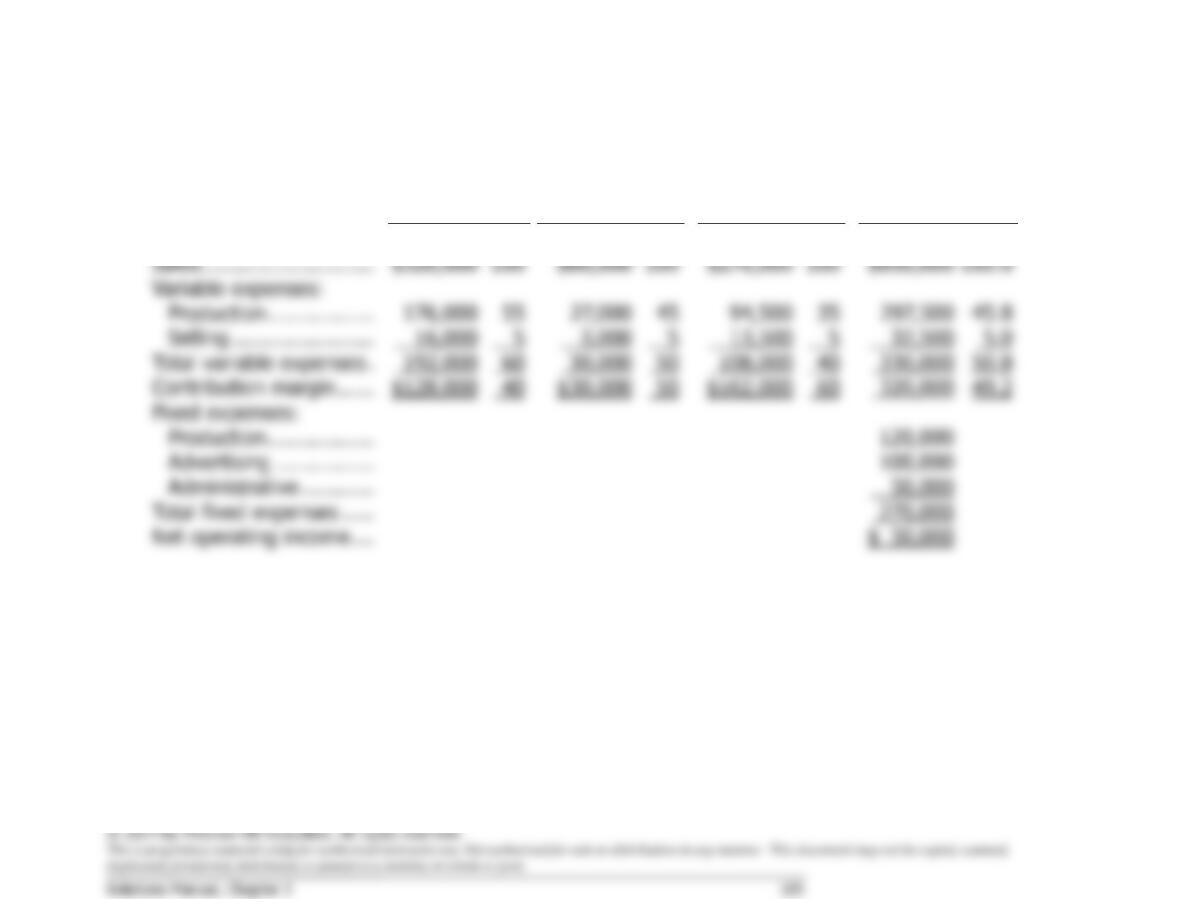

May’s Income Statement:

Standard

Deluxe

Pro

Total

Amount

%

Amount

%

Amount

%

Amount

%

Sales ……………………….

$320,000

100

$60,000

100

$270,000

100

$650,000

100.0

Variable expenses:

Production ……………..

176,000

55

27,000

45

94,500

35

297,500

45.8

Selling …………………..

16,000

5

3,000

5

13,500

5

32,500

5.0

Total variable expenses .

192,000

60

30,000

50

108,000

40

330,000

50.8

Contribution margin ……

$128,000

40

$30,000

50

$162,000

60

320,000

49.2

Fixed expenses:

Production ……………..

120,000

Advertising …………….

100,000

Administrative ………...

50,000

Total fixed expenses …..

270,000

Net operating income ….

$ 50,000

Problem 3-25 (45 minutes)

1.

Sales (25,000 units × SFr 90 per unit) ………………

SFr 2,250,000

Variable expenses

(25,000 units × SFr 60 per unit) ……………………

1,500,000

Contribution margin ………………..…………………….

750,000

Fixed expenses ……………………………………………

840,000

Net operating loss ………………………………………..

SFr (90,000)

2.

Fixed expenses

Unit sales =

to break even Unit contribution margin

SFr 840,000

= = 28,000 units

SFr 30 per unit

28,000 units × SFr 90 per unit = SFr 2,520,000 to break even.

3. See the next page.

4. At a selling price of SFr 80 per unit, the contribution margin is SFr 20

per unit. Therefore:

Fixed expenses

Unit sales =

to break even Unit contribution margin

SFr 840,000

= SFr 20 per unit

= 42,000 units

42,000 units × SFr 80 per unit = SFr 3,360,000 to break even.