Case 3-32 (75 minutes)

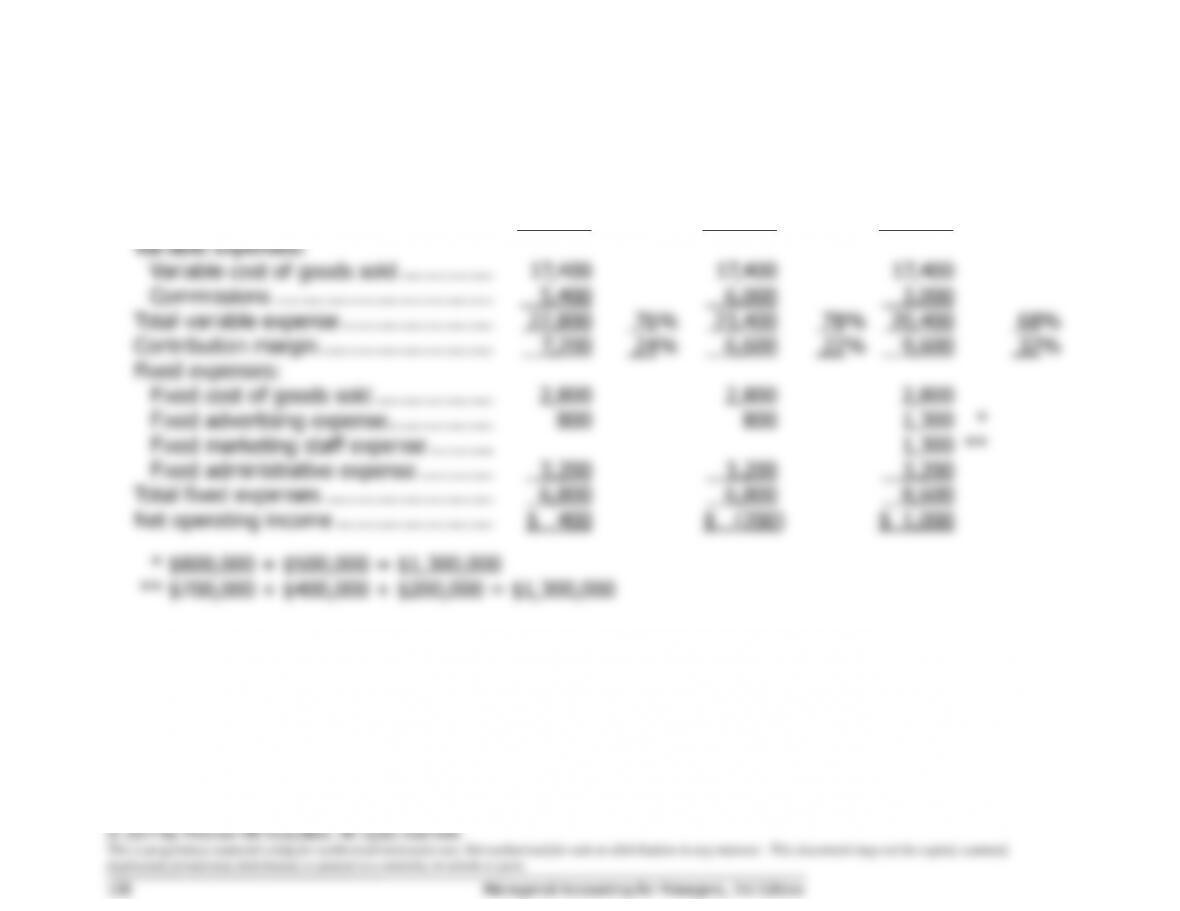

1. The contribution format income statements (in thousands of dollars) for the three alternatives are:

18% Commission

20% Commission

Own Sales Force

Sales ………………………………………….

$30,000

100

%

$30,000

100

%

$30,000

100

%

Variable expenses:

Variable cost of goods sold ……………

17,400

17,400

17,400

Commissions ……………………………..

5,400

6,000

3,000

Total variable expense ……………………

22,800

76

%

23,400

78

%

20,400

68

%

Contribution margin ……………………….

7,200

24

%

6,600

22

%

9,600

32

%

Fixed expenses:

Fixed cost of goods sold ……………….

2,800

2,800

2,800

Fixed advertising expense ……………..

800

800

1,300

*

Fixed marketing staff expense ……….

1,300

**

Fixed administrative expense …………

3,200

3,200

3,200

Total fixed expenses ………………………

6,800

6,800

8,600

Net operating income …………………….

$ 400

$ (200)

$ 1,000

*

$800,000 + $500,000 = $1,300,000

**

$700,000 + $400,000 + $200,000 = $1,300,000

Case 3-32 (continued)

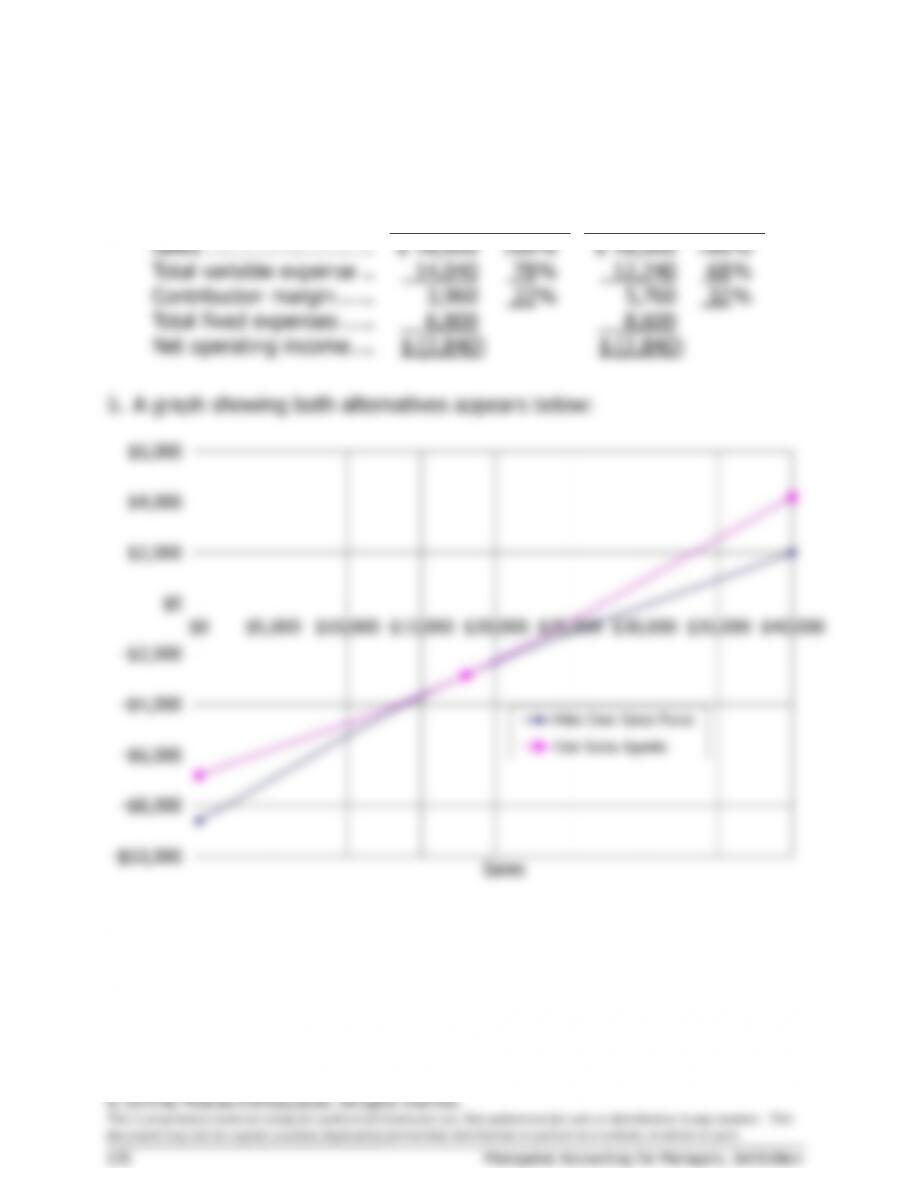

2. Given the data above, the break-even points can be determined using

total fixed expenses and the CM ratios as follows:

a.

Fixed expenses $6,800,000

Dollar sales = = = $28,333,333

to break even CM ratio 0.24

b.

Fixed expenses $6,800,000

Dollar sales = = = $30,909,091

to break even CM ratio 0.22

c.

Fixed expenses $8,600,000

Dollar sales = = = $26,875,000

to break even CM ratio 0.32

3.

Target profit + Fixed expenses

Dollar sales to attain=

target profit CM ratio

-$200,000 + $8,600,000

= 0.32

= $26,250,000

4.

X = Total sales revenue

Net operating income = 0.32X – $8,600,000

with company sales force

Net operating income = 0.22X – $6,800,000

with the 20% commissions

The two net operating incomes are equal when:

0.32X – $8,600,000

=

0.22X – $6,800,000

0.10X

=

$1,800,000

X

=

$1,800,000 ÷ 0.10

X

=

$18,000,000

Case 3-32 (continued)

6.

To: President of Marston Corporation

Fm: Student’s name

Assuming that a competent sales force can be quickly hired and trained

and the new sales force is as effective as the sales agents, this is the

The major concern I have with this recommendation is the assumption

that the new sales force will be as effective as the sales agents. The

sales agents have been selling our product for a number of years, so

they are likely to have more field experience than any sales force we

hire. And, our own sales force would be selling just our product instead

number of salespersons each of whom sells only a single product. Even

so, we can afford some decrease in sales because of the lower cost of

maintaining our own sales force. For example, assuming that the sales

agents make the budgeted sales of $30,000,000, we would have a net

operating loss of $200,000 for the year. We would do better than this

force.

CASE 3-33 (60 minutes)

Note: This is a problem that will challenge the very best students’ conceptual

and analytical skills. However, working through this case will yield substantial

dividends in terms of a much deeper understanding of critical management

accounting concepts.

Frog

Minnow

Worm

Total

Sales …………………….

$200,000

$280,000

$240,000

$720,000

Variable expenses …….

120,000

160,000

150,000

430,000

Contribution margin ….

$ 80,000

$120,000

$ 90,000

290,000

Fixed expenses ……….

282,000

Net operating income .

$ 8,000

Contribution margin $290,000

CM ratio= = =0.4028

Sales $720,000

Fixed expenses $282,000

Dollar sales = = =$700,100 (rounded)

to break even CM ratio 0.4028

2. The issue is what to do with the common fixed costs when computing

the break-evens for the individual products. The correct approach is to

ignore the common fixed costs. If the common fixed costs are included

in the computations, the break-even points will be overstated for

individual products and managers may drop products that in fact are

profitable.

Unit selling price …………….

Variable cost per unit ………

Unit contribution margin (a)

Product fixed expenses (b) .

Case 3-33 (continued)

b. If the company were to sell exactly the break-even quantities

computed above, the company would lose $108,000—the amount of

the common fixed cost. This occurs because the common fixed costs

have been ignored in the calculations of the break-evens.

Frog

Minnow

Worm

Total

Unit sales …………….

22,500

160,000

200,000

Sales …………………..

$45,000

$224,000

$160,000

$ 429,000

Variable expenses ….

27,000

128,000

100,000

255,000

Contribution margin .

$18,000

$ 96,000

$ 60,000

174,000

Fixed expenses ……..

282,000

Net operating loss ….

$(108,000)

At this point, many students conclude that something is wrong with

their answer to part (a) because the company loses money operating

at the break-evens for the individual products. They also worry that

managers may be lulled into a false sense of security if they are given

the break-evens computed in part (a). Total sales at the individual

product break-evens is only $429,000 whereas the total sales at the

overall break-even computed in part (1) is $700,100.

Many students (and managers, for that matter) attempt to resolve

this apparent paradox by allocating the common fixed costs among

Case 3-33 (continued)

It would be natural to interpret a break-even for a product as the

level of sales below which the company would be financially better off

dropping the product. Therefore, we should not be surprised if

managers, based on the erroneous break-even calculation on the

Frog

Minnow

Worm

Total

Sales ……………………..

$200,000

dropped

dropped

$200,000

Variable expenses …….

120,000

120,000

Contribution margin ….

$ 80,000

80,000

Fixed expenses* ………

126,000

Net operating loss …….

$(46,000)

*By dropping the two products, the company reduces its fixed

expenses by only $156,000 (= $96,000 + $60,000). Therefore, the

total fixed expenses would be $126,000 (= $282,000 − $156,000).

By dropping the two products, the company would have a loss of

$46,000 rather than a profit of $8,000. The reason is that the two

products dropped were contributing $54,000 toward covering

common fixed expenses and toward profits. This can be verified by

looking at a segmented income statement like the one that will be

introduced in a later chapter.

Frog

Minnow

Worm

Total

Sales …………………………

$200,000

$280,000

$240,000

$720,000

Variable expenses ………..

120,000

160,000

150,000

430,000

Contribution margin ……..

80,000

120,000

90,000

290,000

Product fixed expenses ….

18,000

96,000

60,000

174,000

Product segment margin .

$ 62,000

$ 24,000

$ 30,000

116,000

Common fixed expenses ..

108,000

Net operating income ……

$ 8,000

$54,000