Archives: Solution Manual

978-0078025778 Chapter 14 Solution Manual Part 3

e. PROBLEM 14.2 A NELSON, INC. (concluded) Favorable and unfavorable trends: Favorable trends. One favorable trend is the $360,000 increase in net sales, which represented an increase of about 14% over the prior year. A second favorable trend is the […]

978-0078025778 Chapter 14 Solution Manual Part 2

Ex. 14.4 a. (1) (2) $ 207.0 72.3 32.0 Total current assets …………………………………. $ 311.3 b. (1) $ 207.0 130.1 Quick ratio ($207 ÷ $130.1) …………………………. 1.6 to 1 Quick ratio: Total quick assets (part a) ……………………………….. Current liabilities ……………………………………….. […]

978-0078025778 Chapter 14 Solution Manual Part 1

Brief Learning Exercises Objectives Skills B. Ex. 14.1 Dollar and percentage change 14-1 Analysis B. Ex. 14.2 Trend percentages 14-1 Analysis B. Ex. 14.3 Component percentages 14-1 Analysis B. Ex. 14.4 Working capital and current ratio 14-4 Analysis B. Ex. […]

978-0078025778 Chapter 14 Lecture Note Part 2

Chapter 14 – Financial Statement Analysis Financial and Managerial Accounting, 17e 14-7 CHAPTER 14 NAME # 10-MINUTE QUIZ A SECTION Indicate the best answer to each question in the space provided. 1 The quick ratio is considered more useful than […]

978-0078025778 Chapter 14 Lecture Note Part 1

Chapter 14 – Financial Statement Analysis Financial and Managerial Accounting, 17e 14-1 14 FINANCIAL STATEMENT ANALYSIS Chapter Summary Although earlier chapters have touched on topics from financial statement analysis, we now present a comprehensive overview of the subject. The chapter […]

978-0078025778 Chapter 13 Solution Manual Part 6

25 Minutes, Strong a. spent an unusually large amount ($160,000) to purchase plant assets during the year. This expenditure for plant assets may increase net operating cash flow above the levels of prior years. Second, the company issued $100,000 of […]

978-0078025778 Chapter 13 Solution Manual Part 5

25 Minutes, Medium a. Cash flows from o p eratin g activities: Net income 928,000$ Add: De p reciation ex p ense 49,000$ Increase in accounts p a y able to su pp liers 5,000 Subtotal 984,000$ Less: Increase in […]

978-0078025778 Chapter 13 Solution Manual Part 4

c. PROBLEM 13.7 A SATELLITE WORLD (concluded) Satellite World’s credit sales resulted in $750,000 in new receivables, which were uncollected as of year-end. These credit sales all were included in the computation of net income, but those that remained uncollected […]

978-0078025778 Chapter 13 Solution Manual Part 3

25 Minutes, Easy a. Cash p aid to ac q uire p lant assets ( see p art b ) (60,000) Proceeds from sales of p lant assets ( 2 ) 12 , 000 Net cash used for investin g […]

978-0078025778 Chapter 13 Lecture Note Part 2

Chapter 13 – Statement of Cash Flows Financial and Managerial Accounting, 17e 13-7 CHAPTER 13 NAME # 10-MINUTE QUIZ B SECTION Use the following information for questions 1 through 4. Lester Corporation’s statement of cash flows for 2009 shows the […]

978-0078025778 Chapter 13 Lecture Note Part 1

Chapter 13 – Statement of Cash Flows Financial and Managerial Accounting, 17e 13-1 13 STATEMENT OF CASH FLOWS Chapter Summary The statement of cash flows was introduced in Chapter 1. This chapter begins by reviewing the purpose of the statement. […]

978-0078025778 Chapter 12 Solution Manual Part 6

30 Minutes, Strong a. (2) The diluted earnings per share figures show the effect that conversion of all of the convertible preferred stock into common shares would have had upon this year’s earnings. Earnings per share from continuing operations would […]

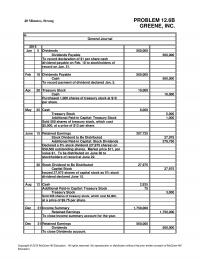

978-0078025778 Chapter 12 Solution Manual Part 5

40 Minutes, Strong Jan 5 Dividends 560,000 Dividends Pa y able 560 , 000 Cash 560 , 000 A p r 20 10 , 000 10 , 000 Au g 12 2 , 925 75 Treasur y Stock 3 , […]

978-0078025778 Chapter 12 Solution Manual Part 4

50 Minutes, Strong a. Stockholders’ equit y : Capital stock: Common stock, $10 par, 500,000 shares authorized, 150,000 shares issued, of which 10,000 are held in the treasur y 1,500,000$ Stock dividend to be distributed ( 1 ) 140,000 ( […]

978-0078025778 Chapter 12 Solution Manual Part 3

30 Minutes, Medium a. Discontinued o p erations: O p eratin g income ( net of income tax ) 140 , 000 $ Loss on dis p osal ( net of income tax benefit ) ( 550 , 000 ) […]

978-0078025778 Chapter 12 Lecture Note Part 2

Chapter 12 – Income and Changes in Retained Earnings Financial and Managerial Accounting, 17e 12-7 CHAPTER 12 NAME _________ # ____________ 10-MINUTE QUIZ B SECTION The stockholders’ equity section of the balance sheet of Global Publishing at December 31, 2009, […]

978-0078025778 Chapter 12 Lecture Note Part 1

Chapter 12 – Income and Changes in Retained Earnings Financial and Managerial Accounting, 17e 12-1 12 INCOME AND CHANGES IN RETAINED EARNINGS Chapter Summary Chapter 12 continues the coverage of stockholders’ equity but shifts the focus from paid– in capital […]

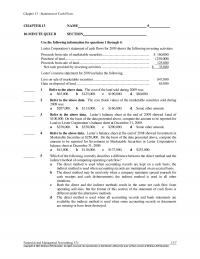

978-0078025778 Chapter 11 Solution Manual Part 5

e. f. The two principal factors that cause one preferred to yield less than another are: (1) the appearance of greater ability to pay the preferred dividends each year, and (2) special features that appeal to investors, such as Toasty’s […]

978-0078025778 Chapter 11 Solution Manual Part 4

15 Minutes, Medium Stockholders’ e q uit y : Common stock, $1 par, 50,000 shares authorized, issued, and 50,000$ outstanding Additional p aid-in ca p ital: Common stoc k 350,000 Total p aid-in ca p ital 405,000$ Retained earnin g […]

978-0078025778 Chapter 11 Solution Manual Part 3

Ex. 11.15 a. The par value is $.05 per share. The common stock originally sold significantly above par value because the paid-in capital in excess of par value is large. worth. The total stockholders’ equity figure represents the amount invested […]

978-0078025778 Chapter 11 Lecture Note Part 2

Chapter 11 – Stockholders’ Equity: Paid-In Capital Financial and Managerial Accounting, 17e 11-7 CHAPTER 11 NAME # __________________ 10-MINUTE QUIZ B SECTION Shown below is information relating to the stockholders’ equity of Revere Corporation at December 31, 2009 8% cumulative […]

978-0078025778 Chapter 11 Lecture Note Part 1

Chapter 11 – Stockholders’ Equity: Paid-In Capital Financial and Managerial Accounting, 17e 11-1 11 STOCKHOLDERS’ EQUITY: PAID-IN CAPITAL Chapter Summary This, the first of two chapters on stockholders’ equity, treats topics concerned with the paid-in capital of a corporation. Consideration […]

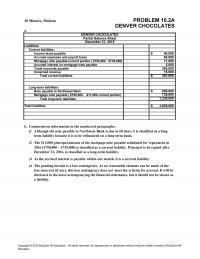

978-0078025778 Chapter 10 Solution Manual Part 5

20 Minutes, Strong a. Liabilities: Unearned revenues 268,000$ 462,500$ Long-term liabilities: 750,000$ 123,000 Note payable (approved for extension at maturity) 90,000 11 5, 000 ● ● Deferred income taxes** The lawsuit pending against the company is a loss contingency. It […]

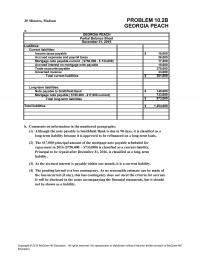

978-0078025778 Chapter 10 Solution Manual Part 4

30 Minutes, Medium a. b. (1) (2) (3) (4) PROBLEM 10.2B GEORGIA PEACH December 31, 2015 Partial Balance Shee t GEORGIA PEACH The pending lawsuit is a loss contingency. As no reasonable estimate can be made of the loss incurred […]

978-0078025778 Chapter 10 Solution Manual Part 3

30 Minutes, Medium a. Accrued interest on mortgage note payabl e 5,000 Trade accounts payable 250,000 Unearned revenu e 1 5, 000 Total current liabilities 381 , 000 $ 500,000$ 7 39 , 000 Note payable to Northwest Bank Mortgage […]

978-0078025778 Chapter 10 Solution Manual Part 2

Ex. 10.1 Annual Unpaid Payment Balance Ex. 10.2 Trans- Net Current Owners’ action Revenue – Expenses= Income Assets = Liab. + Liab. + Equity Net Cash Current Net from all Liabilities Income Sources Long-Term Liabilities Long-Term Ex. 10.3 Net Cash […]

978-0078025778 Chapter 10 Solution Manual Part 1

Brief Learning Exercises Objectives B. Ex. 10.1 Cash effects of borrowing 10-2 B. Ex. 10.2 Effective interest rate 10-5 B. Ex. 10.3 Bonds issued at a discount 10-6 B. Ex. 10.4 Bonds issued a premium 10-6 Analysis B. Ex. 10.5 […]

978-0078025778 Chapter 10 Lecture Note Part 2

Chapter 10 – Liabilities CHAPTER 10 NAME # 10-MINUTE QUIZ B SECTION Shown below is a summary of the annual payroll data of Rose Co.: Wages and salaries expense (gross pay) $2,250,000 Amounts withheld from employees’ pay: Income taxes ………………………………………………….. […]

978-0078025778 Chapter 10 Lecture Note Part 1

Chapter 10 – Liabilities Financial and Managerial Accounting, 17e 10-1 10 LIABILITIES Chapter Summary At the outset, the chapter distinguishes between current and long-term liabilities before addressing the accounting issues surrounding each category. Among current liabilities, notes payable and payroll […]

978-0078025778 Chapter 1 Lecture Note Part 2

Chapter 01 – Accounting: Information for Decision Making Financial and Managerial Accounting, 17e 1-7 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. CHAPTER 1 NAME # 10-MINUTE QUIZ […]

978-0078025778 Chapter 1 Lecture Note Part 1

Chapter 01 – Accounting: Information for Decision Making Financial and Managerial Accounting, 17e 1-1 1 ACCOUNTING: INFORMATION FOR DECISION MAKING Chapter Summary Our financial reporting system has changed greatly over the past 50 years and will continue to change. The […]

978-0078025778 Chapter 1 Case Part 2

a. & d. D e bit C re dit B a l ance D e bit C re dit B a l ance Dec 31 700 700 31 700 0 To close D e bit C re dit B a […]

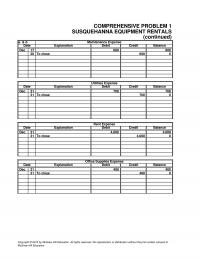

978-0078025778 Chapter 1 Case Part 1

5 to 6 hours Strong COMPREHENSIVE PROBLEM 1 Susquehanna Equipment Rentals A mini-practice set illustrating the complete accounting cycle for a service-type business. Includes computation of income taxes expense (as a percentage of income before taxes) and an evaluation of […]

978-0078025778 Appendix C Appendix Part 3

PROBLEM C.10 COMEDY TODAY (concluded) b. General Journal Journal entry to close Income Summary account (Case 3 from part a above) Income Summary 110,000 Abbott, Capital 42,000 Martin, Capital 68,000 To close the Income Summary account by crediting each partner […]

978-0078025778 Appendix C Appendix Part 2

PROBLEM C.6 FRONTIER WESTERN WEAR, INC. (concluded) d. FRONTIER WESTERN WEAR, INC. Partial Balance Sheet December 31, 2015 Stockholders’ equity: Capital stock 800,000$ Retained earnings (computation below) 34,000 Total stockholders’ equity 834,000 Computation of retained earnings at December 31, 2015: […]

978-0078025778 Appendix C Appendix Part 1

FORMS OF BUSINESS ORGANIZATIONS Problems C.1 E-Z Manufacturin g Com p an y 15 Easy LO C-3, C-10 Students are required to calculate partners’ share of net income, determine the effects of income taxes for partners, and prepare a statement […]

978-0078025778 Appendix B Appendix

B.1 15 Eas y LO B.2 20 Medium LO B-3, B- 4 B.3 15 Medium LO B.4 15 Medium LO B.5 20 Medium LO B.6 35 Strong LO B.7 25 Strong LO B-5, B- 6 B-1, B-2, B-4 B-1, B-2, […]

978-0078025426 Chapter 12 Part 7

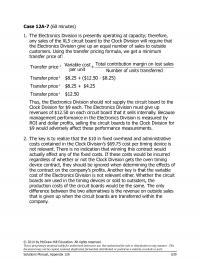

Case 12A–7 (60 minutes) 1. The Electronics Division is presently operating at capacity; therefore, any sales of the XL5 circuit board to the Clock Division will require that the Electronics Division give up an equal number of sales to outside […]

978-0078025426 Chapter 12 Part 6

Exercise 12A-3 (continued) 2. a. Each of the 10,000 units transferred to the Motor Division must displace a sale to an outsider at a price of $40. Therefore, the selling division would demand a transfer price of at least $40. […]

978-0078025426 Chapter 12 Part 5

Problem 12–22 (30 minutes) 1. a., b., and c. Month 1 2 3 4 Throughput time in days: Process time ……………………………… 0.6 0.6 0.6 0.6 Inspection time ………………………….. 0.1 0.3 0.6 0.8 Move time ………………………………… 1.4 1.3 1.3 1.4 Queue […]

978-0078025426 Chapter 12 Part 4

Problem 12–18 (20 minutes) 1. Operating assets do not include investments in other companies or in undeveloped land. Ending Balances Beginning Balances Cash ………………………………… $ 130,000 $ 125,000 Accounts receivable …………….. 480,000 340,000 Inventory ………………………….. 490,000 570,000 Plant and equipment […]

978-0078025426 Chapter 12 Part 3

Exercise 12–12 (30 minutes) 1. Net operating income Margin = Sales $16,000 = = 2% $800,000 Sales Turnover = Average operating assets $800,000 = = 8 $100,000 ROI = Margin × Turnover = 2% × 8 = 16% 2. Net […]

978-0078025426 Chapter 12 Part 2

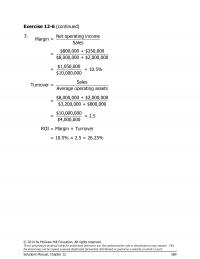

Exercise 12-6 (continued) 3. Net operating income Margin = Sales $800,000 + $250,000 = $8,000,000 + $2,000,000 $1,050,000 = = 10.5% $10,000,000 Sales Turnover = Average operating assets $8,000,000 + $2,000,000 = $3,200,000 + $800,000 $1 = 0,000,000 = 2.5 […]

978-0078025426 Chapter 11 Part 7

Problem 11A–10 (45 minutes) 1. £31,500 + £72,000 Total rate: =£5.75 per MH 18,000 MHs £31,500 Variable element: =£1.75 per MH 18,000 MHs £72,000 Fixed element: =£4.00 per MH 18,000 MHs 2. 16,000 standard MHs × £5.75 per MH = […]

978-0078025426 Chapter 11 Part 6

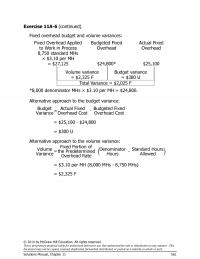

Exercise 11A-6 (continued) Fixed overhead budget and volume variances: Fixed Overhead Applied to Work in Process Budgeted Fixed Overhead Actual Fixed Overhead 8,750 standard MHs × $3.10 per MH = $27,125 $24,800* $25,100 Volume variance = $2,325 F Budget variance […]

978-0078025426 Chapter 11 Part 5

Problem 11–16 (continued) 3. The computations to follow will require the standard quantities allowed for the actual output for direct labor in each department. Standard Hours Allowed Sintering: Production of Alpha8 (0.20 hours per unit × 1,500 units) .. 300 […]

978-0078025426 Chapter 11 Part 4

Problem 11–13 (continued) 2. a. Labor efficiency variance = SR (AH – SH) $9.00 per hour (AH – 3,500 hours*) = $4,500 F $9.00 per hour × AH – $31,500 = –$4,500** $9.00 per hour × AH = $27,000 AH […]

978-0078025426 Chapter 11 Part 3

Problem 11–10 (continued) Note that all of the price variance is due to the hospital’s 4% quantity discount. Also note that the $8,000 quantity variance for the month is equal to nearly 30% of the standard cost allowed for plates. […]

978-0078025426 Chapter 11 Part 2

Exercise 11-6 (continued) 2. Standard Hours Allowed for Actual Output, at Standard Rate (SH × SR) Actual Hours of Input, at Standard Rate (AH × SR) Actual Hours of Input, at Actual Rate (AH × AR) 1,000 hours* × $10.00 […]

978-0078025426 Chapter 11 Part 1

Chapter 11 Standard Costs and Variances Solutions to Questions 11-1 A quantity standard indicates how much of an input should be used to make a unit of output. A price standard indicates how much the input should cost. indicate that […]