Exercise 12–12 (30 minutes)

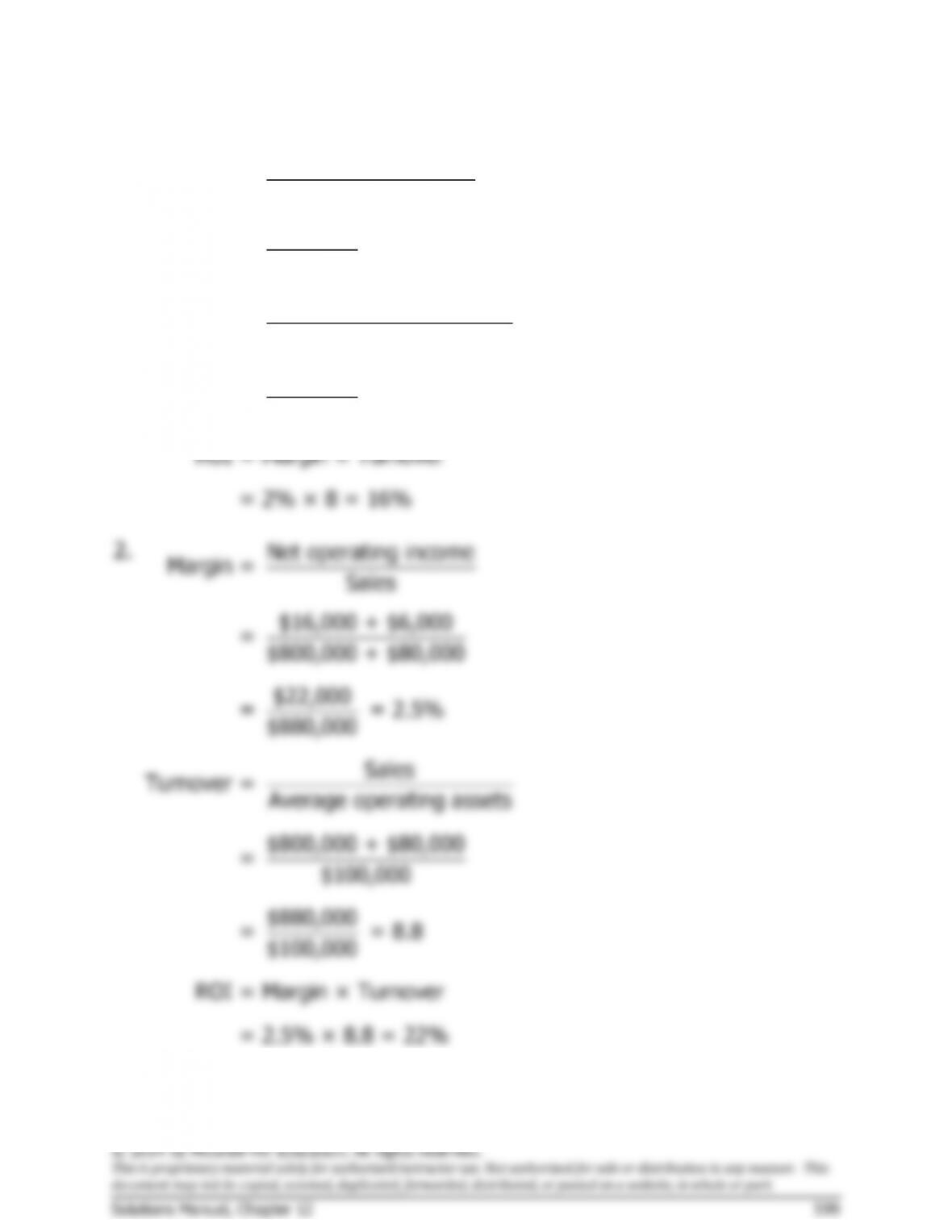

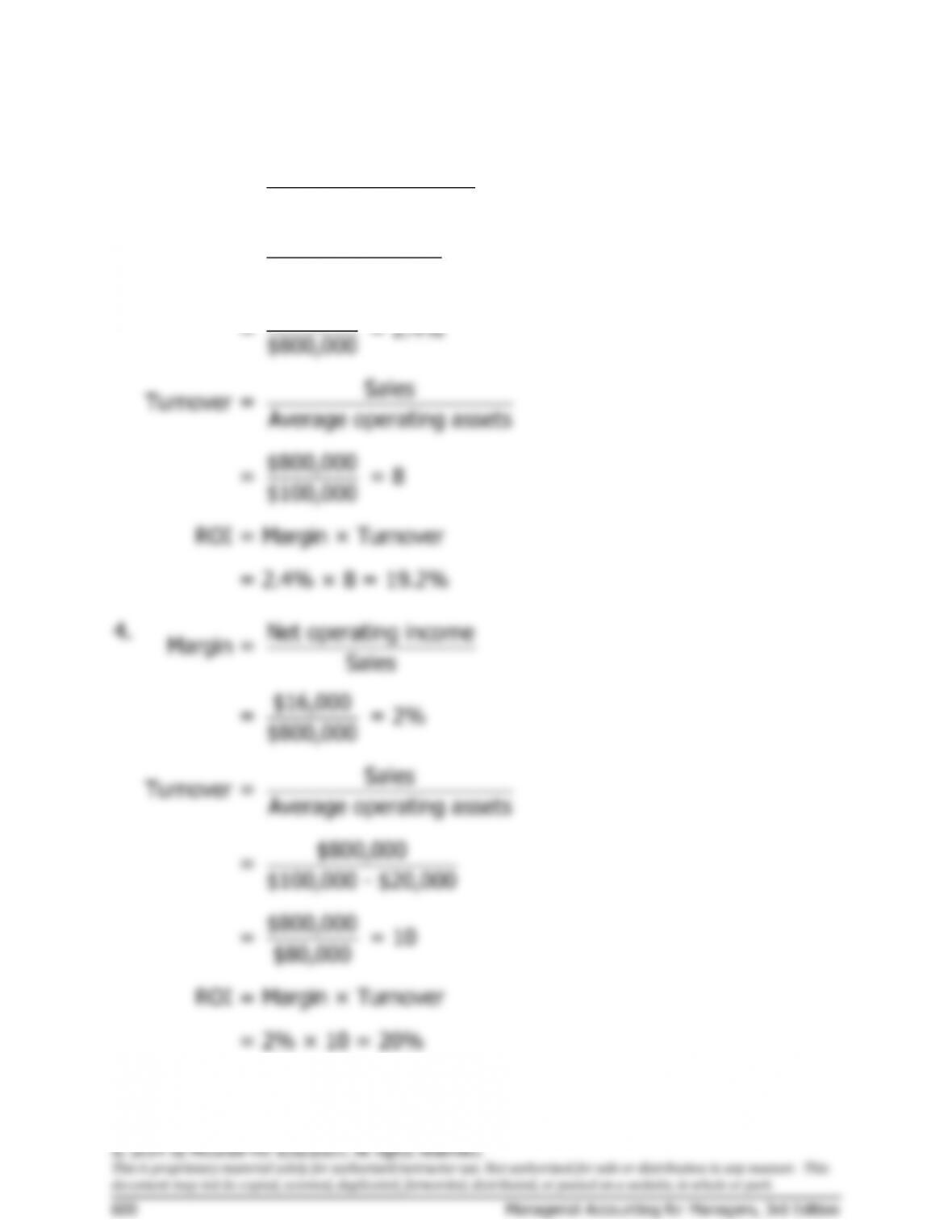

1.

Net operating income

Margin = Sales

$16,000

= = 2%

$800,000

Sales

Turnover = Average operating assets

$800,000

= = 8

$100,000

ROI = Margin × Turnover

= 2% × 8 = 16%

Problem 12–15 (30 minutes)

1. Breaking the ROI computation into two separate elements helps the

manager to see important relationships that might remain hidden. First,

the importance of turnover of assets as a key element to overall

profitability is emphasized. Prior to use of the ROI formula, managers

company may shave its margins slightly hoping for a large enough

increase in turnover to increase the overall rate of return. Fourth, it

permits a manager to reduce important profitability elements to ratio

form, which enhances comparisons between units (divisions, etc.) of the

organization.

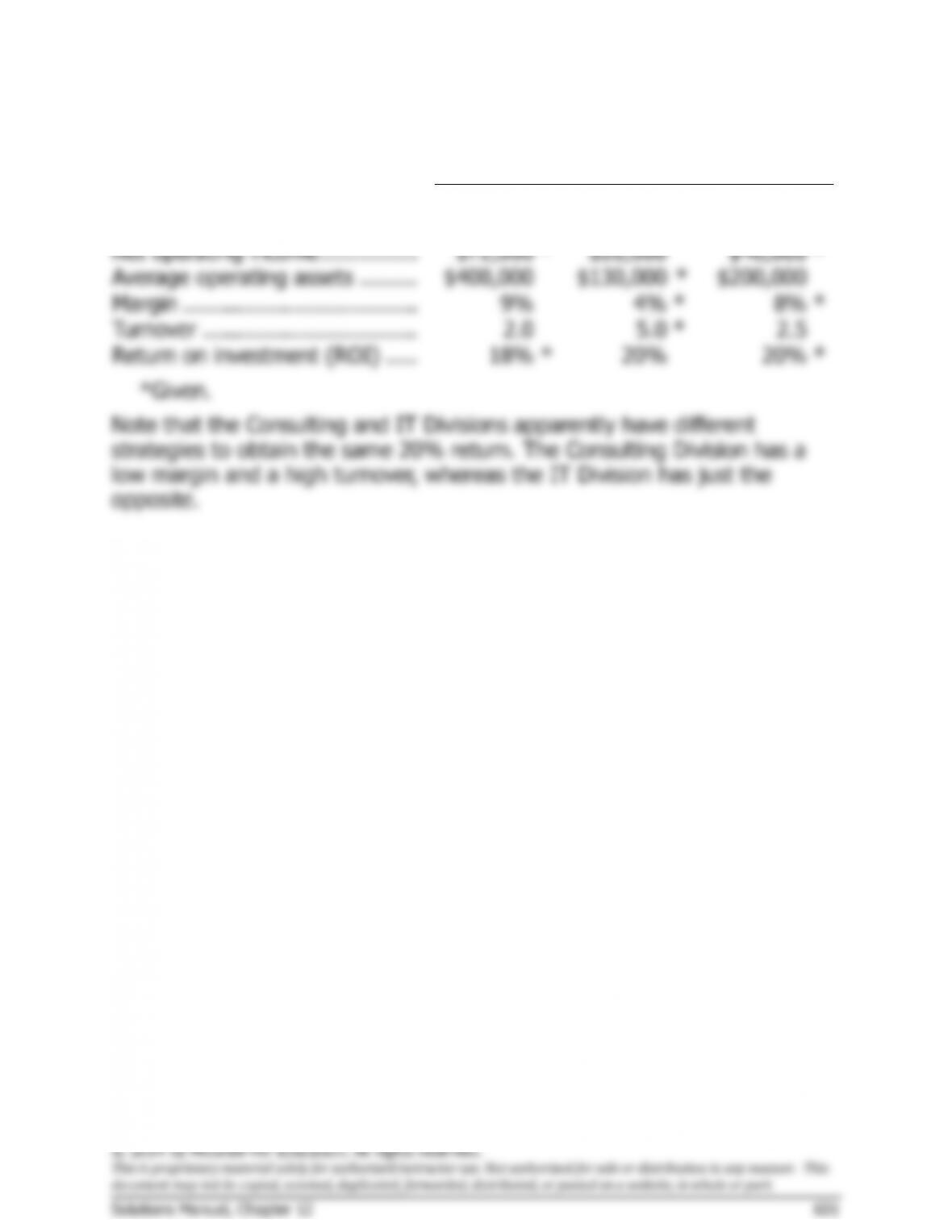

2.

Companies in the Same Industry

A

B

C

Sales …………………………….

$4,000,000

*

$1,500,000

*

$6,000,000

Net operating income ……….

$560,000

*

$210,000

*

$210,000

Average operating assets …..

$2,000,000

*

$3,000,000

$3,000,000

*

Margin …………………………..

14%

14%

3.5%

*

Turnover ………………………..

2.0

0.5

2.0

*

Return on investment (ROI) .

28%

7%

*

7%

*Given.

NAA Report No. 35

states (p. 35):

supports two dollars in sales each period, a dollar investment in

Company B supports only 50 cents in sales each period. This suggests

that the analyst should look carefully at Company B’s investment. Is the

company keeping an inventory larger than necessary for its sales

© 2014 by McGraw-Hill Education. All rights reserved.