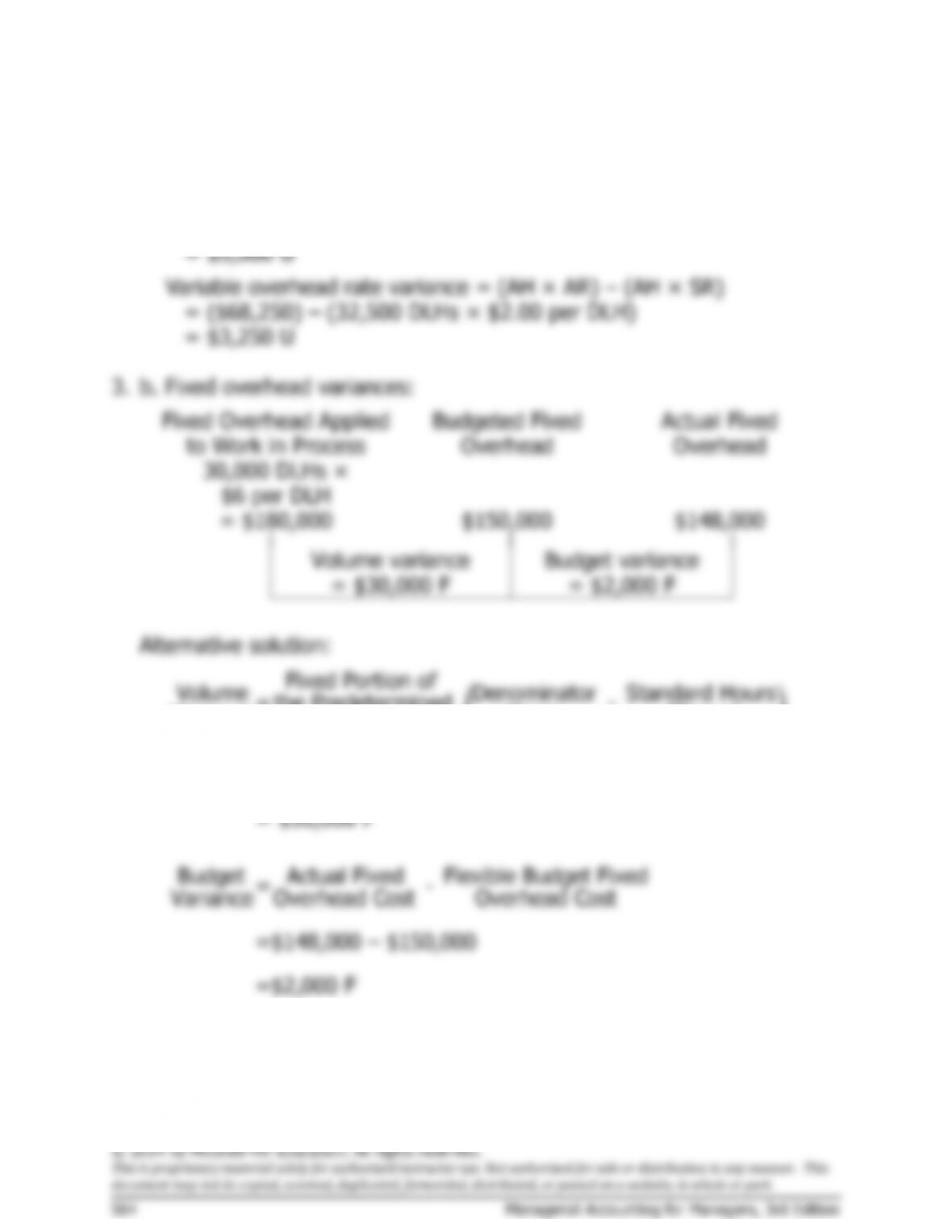

Exercise 11A-6 (continued)

Fixed overhead budget and volume variances:

Fixed Overhead Applied

to Work in Process

Budgeted Fixed

Overhead

Actual Fixed

Overhead

8,750 standard MHs

× $3.10 per MH

= $27,125

$24,800*

$25,100

Volume variance

= $2,325 F

Budget variance

= $300 U

Total Variance = $2,025 F

*8,000 denominator MHs × $3.10 per MH = $24,800.

Alternative approach to the budget variance:

Budget Actual Fixed Budgeted Fixed

= –

Variance Overhead Cost Overhead Cost

= $25,100 – $24,800

= $300 U

Alternative approach to the volume variance:

( )

Fixed Portion of

Volume Denominator Standard Hours

=the Predetermined –

Variance Hours Allowed

Overhead Rate

= $3.10 per MH (8,000 MHs – 8,750 MHs)

= $2,325 F