Problem 11A–10 (45 minutes)

1.

£31,500 + £72,000

Total rate: =£5.75 per MH

18,000 MHs

£31,500

Variable element: =£1.75 per MH

18,000 MHs

£72,000

Fixed element: =£4.00 per MH

18,000 MHs

2. 16,000 standard MHs × £5.75 per MH = £92,000

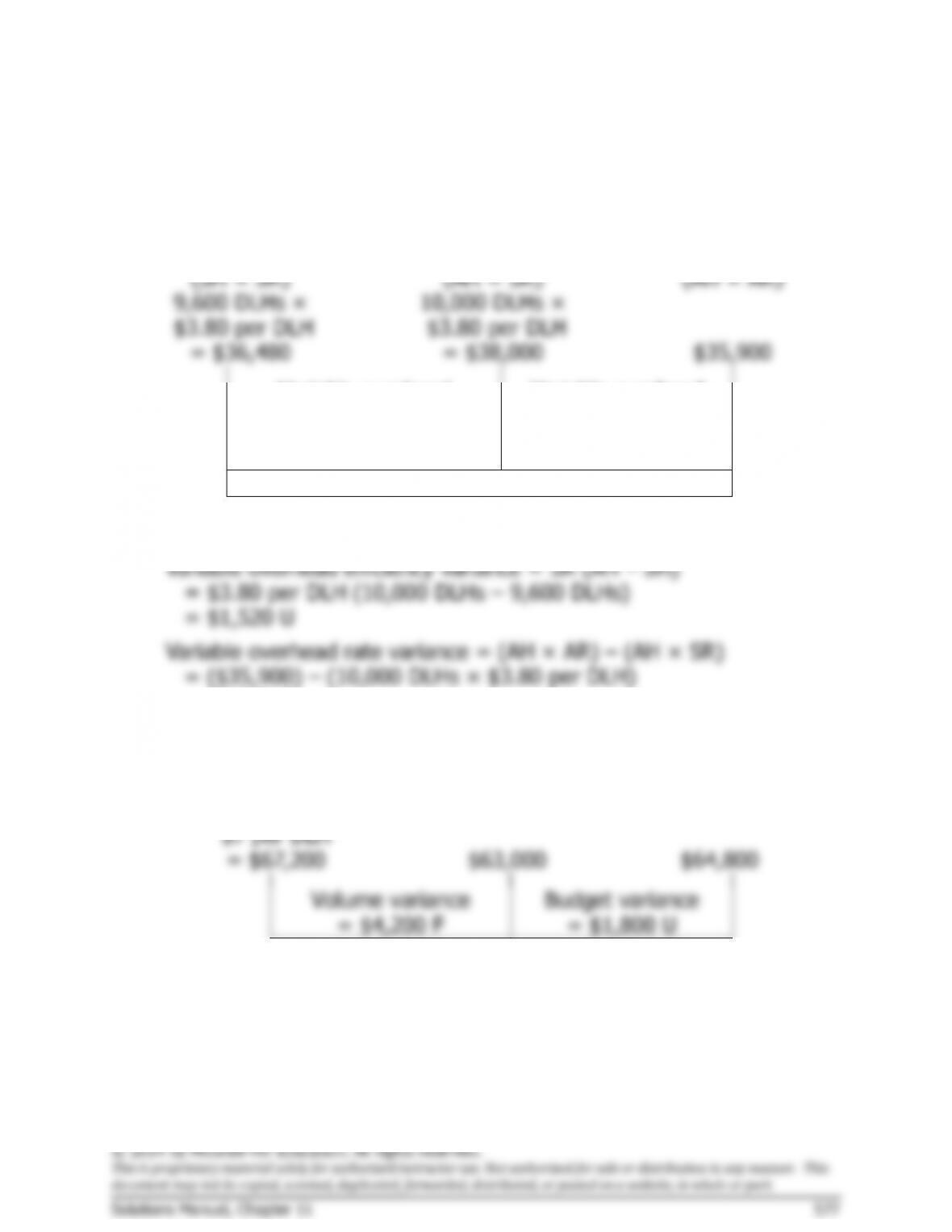

3. Variable manufacturing overhead variances:

Standard Hours Allowed

for Actual Output,

at Standard Rate

(SH × SR)

Actual Hours of Input,

at Standard Rate

(AH × SR)

Actual Hours of Input,

at Actual Rate

(AH × AR)

16,000 MHs ×

£1.75 per MH

= £28,000

15,000 MHs ×

£1.75 per MH

= £26,250

£26,500

Variable overhead

efficiency variance

= £1,750 F

Variable overhead

rate variance

= £250 U

Alternative solution:

Variable overhead efficiency variance = SR (AH – SH)

= £1.75 per MH (15,000 MHs – 16,000 MHs)

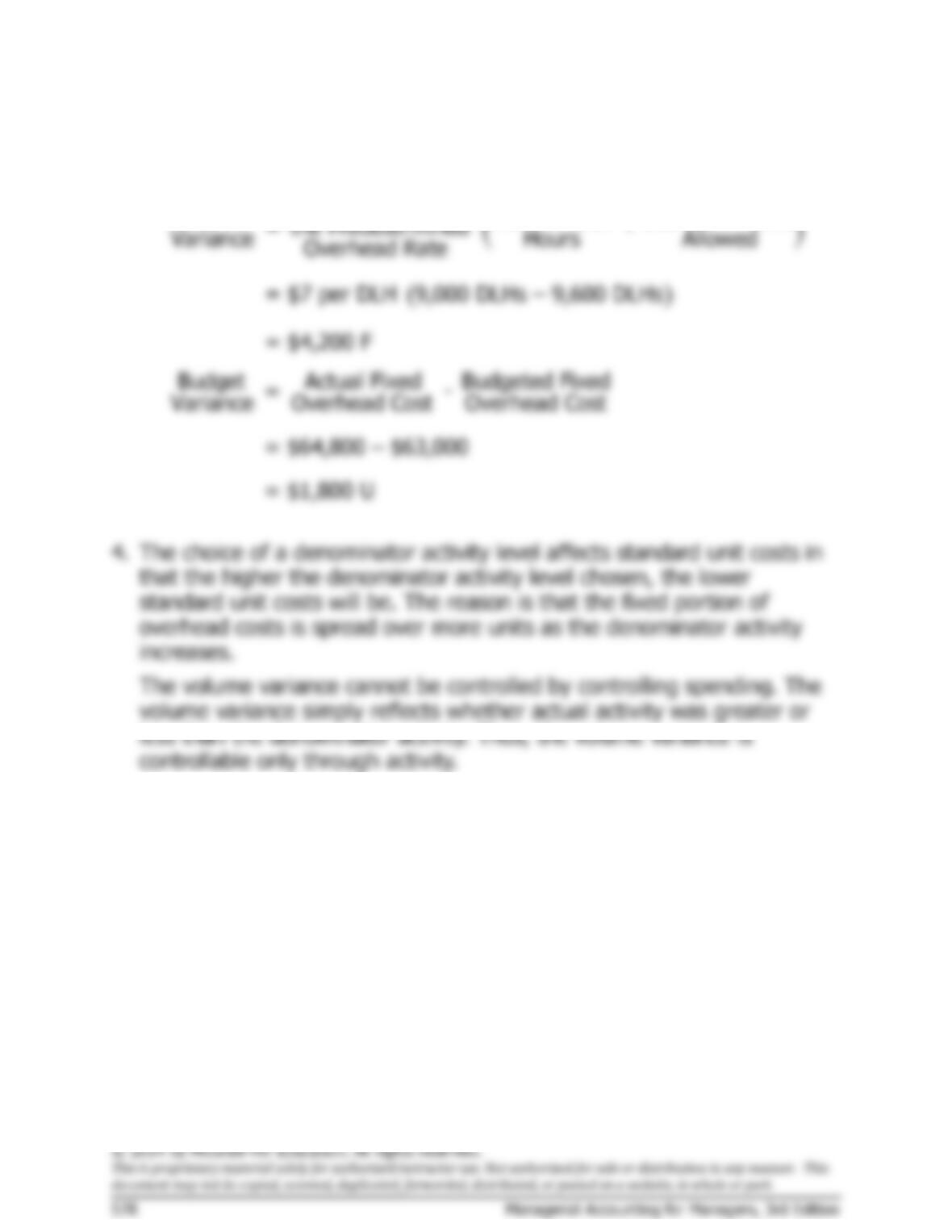

Problem 11A–11 (continued)

Alternative solution:

Variable overhead efficiency variance = SR (AH – SH)

= $2.00 per DLH (35,000 DLHs – 33,000 DLHs)

( )

( )

Fixed Portion of

Volume Denominator Standard Hours

= the Predetermined –

Variance Hours Allowed

Overhead Rate

= $6 per DLH 30,000 DLHs – 33,000 DLHs

= $18,000 F

Budget Actual Fixed Flexible Budget Fixed

= –

Variance Overhead Cost Overhead Cost

= $1,000 U

Problem 11A–12 (continued)

Alternative solution:

( )

Fixed Portion of

Volume Denominator Standard Hours

= the Predetermined –

Variance Hours Allowed

Overhead Rate